Artificial Intelligence in Agriculture Market Report Scope & Overview:

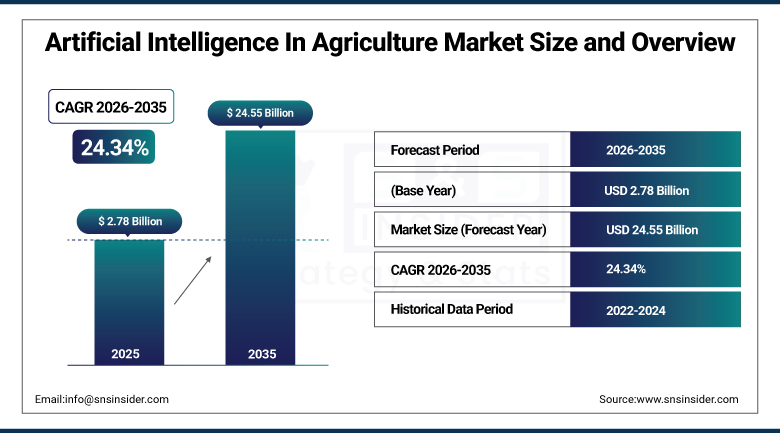

The Artificial Intelligence in Agriculture Market was valued at USD 2.78 Billion in 2025 and is expected to reach USD 24.55 Billion by 2035, growing at a CAGR of 24.34% from 2026 to 2035.

The global artificial intelligence in agriculture market is experiencing transformative and accelerating growth as the world’s food production systems face unprecedented simultaneous pressures from climate variability, labour shortages, population growth, and natural resource constraints. Artificial intelligence technologies encompassing machine learning, computer vision, predictive analytics, robotics, and natural language processing are enabling farmers to make precise, data driven decisions from vast volumes of farm data collected through satellites, drones, IoT sensors, and weather stations. AI tools are helping farmers optimise planting schedules, irrigation programmes, nutrient applications, and harvest timing while simultaneously detecting crop diseases and pest infestations before visible symptoms cause yield loss. The market is propelled by the increasing need to enhance crop yields while minimising environmental impact, growing government support for digital agriculture programmes, venture capital investment in agri tech startups, and the progressive commoditisation of AI software platforms that reduces the technology adoption barrier for farm operators of all sizes.

In August 2024, Bayer Crop Science began developing a new AWS based data science platform with generative AI capabilities to create innovative agricultural solutions. The platform, built with Amazon SageMaker Studio and Amazon Bedrock, entered the discovery phase with production models expected in 2025. This development reflects the strategic direction of crop science companies toward AI powered agronomic advisory services that combine proprietary crop genetics knowledge, environmental sensor data, and generative AI language interfaces to deliver personalised field management recommendations at scale.

Market Size and Forecast

-

Market Size in 2026E: USD 3.46 Billion

-

Market Size by 2035: USD 24.55 Billion

-

CAGR: 24.34% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Artificial Intelligence In Agriculture Market - Request Free Sample Report

Artificial Intelligence in Agriculture Market Trends

-

Generative AI integration in farm management platforms is enabling natural language advisory tools that deliver personalized agronomic recommendations and simplify decision-making for farmers

-

Growing adoption of autonomous agricultural machinery, including self-driving tractors, robotic harvesters, and automated sprayers, is improving productivity and addressing labor shortages

-

Increasing use of AI-powered satellite imagery and remote sensing technologies is enhancing crop monitoring, disease detection, yield forecasting, and field-level farm management

-

AI-driven supply chain optimization is helping reduce food waste through improved harvest planning, inventory management, storage monitoring, and logistics coordination

-

Rising adoption of climate-smart agriculture solutions is enabling farmers to manage weather-related risks through predictive analytics, scenario modeling, and data-driven crop management strategies

U.S. Artificial Intelligence in Agriculture Market Outlook

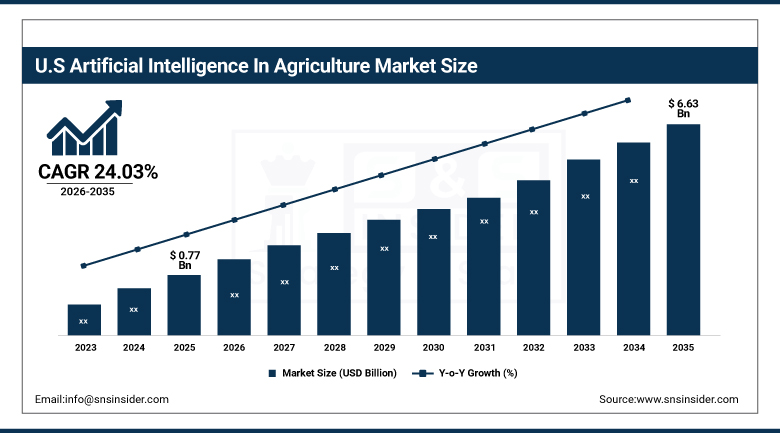

The U.S. Artificial Intelligence in Agriculture Market was valued at approximately USD 0.77 Billion in 2025 and is expected to reach approximately USD 6.63 Billion by 2035, growing at a CAGR of approximately 24.03%.

The U.S. is the world’s most commercially sophisticated AI in agriculture market, hosting the global headquarters of John Deere, The Climate Corporation (Bayer), Trimble Agriculture, Raven Industries, AG Leader Technology, and Corteva Agriscience, whose combined AI agriculture platform revenues define commercial technology standard setting. The USDA’s precision agriculture research programme, federal investment in agricultural technology through the Farm Bill, and land grant university agri tech development programmes create an institutional innovation ecosystem that sustains U.S. technology leadership. The extraordinary scale of U.S. commercial row crop farming, whose large average farm size creates strong economic justification for precision agriculture technology investment, sustains per farm AI adoption rates that substantially exceed global averages.

In May 2024, John Deere announced a strategic partnership with NVIDIA to develop real time AI analytics for its self driving tractor platforms. The partnership combines NVIDIA’s Jetson Orin computing platform’s edge AI processing capability with John Deere’s autonomous guidance and implement control systems to enable real time field condition adaptation that pre programmed autonomous systems cannot achieve. The partnership demonstrates the convergence of farm equipment, semiconductor, and AI platform technologies whose integration creates autonomous agricultural systems significantly more capable than either company’s independent technology development could produce.

Market Segment Analysis

-

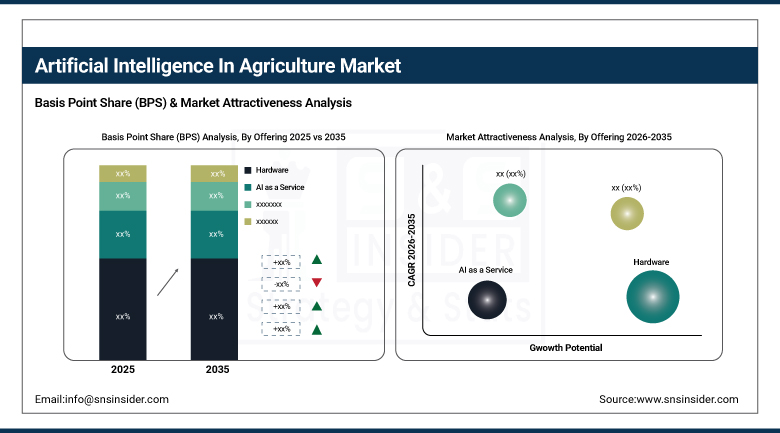

By Offering, the Software segment dominated the Artificial Intelligence in Agriculture Market with approximately 55% share in 2025, while the Hardware segment is the fastest growing.

-

By Technology, the Machine Learning & Deep Learning segment dominated the Artificial Intelligence in Agriculture Market with approximately 47% share in 2025, while the Computer Vision segment is the fastest growing.

-

By Application, the Precision Farming segment dominated the Artificial Intelligence in Agriculture Market in 2025, while the Agriculture Robots segment is the fastest growing.

By Offering, software dominates, hardware grows fastest

Software retained the dominant offering position with approximately 55% of the AI in agriculture market in 2025. The commercial primacy of software reflects AI’s fundamental value delivery mechanism in agriculture, where the interpretation of raw sensor, satellite, and environmental data into actionable farm management insights requires sophisticated software platforms whose machine learning models, data fusion algorithms, and user interface design collectively create the farmer facing product that drives adoption decisions. Farm management information systems that integrate AI analytics with field mapping, financial tracking, and compliance documentation create software platforms whose comprehensive farm management utility sustains subscription relationships beyond initial AI feature adoption. The Climate Corporation’s Climate FieldView platform, Trimble Agriculture’s Connected Farm system, and AG Leader’s AgFiniti platform collectively demonstrate the commercial scale of AI agriculture software procurement from large commercial farm operators.

Hardware is the fastest growing offering because the progressive commoditisation of AI capable edge computing components, drone platforms, and IoT agricultural sensors is reducing the capital cost barrier that previously limited hardware adoption to the largest farm operations. Each agricultural drone whose camera and onboard AI processing can substitute for multiple field scouting labour hours creates hardware procurement whose ROI calculation improves proportionally with farm size and labour cost. Autonomous tractor guidance systems, variable rate application hardware, and soil moisture sensor networks whose data feeds AI optimisation platforms create hardware procurement that grows proportionally with software platform adoption.

By Technology, machine learning dominates, computer vision grows fastest

Machine learning and deep learning retained the dominant technology position with approximately 47% of the AI in agriculture market in 2025. The technology’s commercial primacy reflects its proven effectiveness across the most commercially significant agricultural AI applications, encompassing yield prediction from historical weather and management data, disease risk forecasting from environmental condition patterns, soil nutrient response modelling from field trial data, and precision irrigation scheduling from soil moisture and evapotranspiration models. Each growing season’s data accumulation creates training data that improves model performance, creating compounding accuracy improvements that sustain machine learning’s commercial advantage over alternative AI approaches requiring less training data. John Deere’s See and Spray system, The Climate Corporation’s yield prediction models, and Trimble’s prescription map generation collectively demonstrate machine learning’s commercial deployment at scale in precision agriculture.

Computer vision is the fastest growing technology because the proliferation of high resolution drone cameras, robotic platform vision systems, and fixed greenhouse imaging sensors creates an expanding application base whose visual inspection, disease detection, and automated harvesting guidance requirements create structured commercial adoption growth. Each robotic weeding system whose computer vision discriminates crop plants from weeds at field working speed, each drone scouting programme whose imagery analysis identifies disease infection boundaries at field resolution, and each automated sorting line whose visual inspection replaces manual grading creates computer vision agricultural AI procurement that compounds with precision agriculture technology adoption.

By Application, precision farming dominates, agriculture robots grow fastest

Precision farming retained the dominant application position in 2025. The application’s commercial dominance reflects its status as the foundational AI agriculture use case whose variable rate fertiliser, seed, and pesticide application technology creates the most proven and widely adopted AI agriculture return on investment calculation. Each farm that adopts AI powered prescription maps for input application creates measurable cost reduction from input optimisation and yield improvement from site specific management that conventional uniform rate application approaches cannot achieve. The application’s commercial maturity, evidenced by multi year adoption across North American and European commercial farming operations, sustains revenue leadership as the established AI agriculture investment category.

Agriculture robots are the fastest growing application because the intersection of agricultural labour shortage severity, minimum wage legislation increases, and declining robotic hardware costs is creating economic crossover points where autonomous harvesting, weeding, and planting systems achieve payback periods that motivate commercial farm investment. Each fresh produce operation where hand harvest labour cost represents 40 to 60 percent of total production cost creates economic motivation for robotic harvesting system investment whose economics improve with each hardware generation. Companies including Agrobot, Harvest CROO Robotics, Carbon Robotics, and Iron Ox collectively demonstrate the commercial investment scale in agricultural robotics that sustains the application’s fastest growing designation.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Artificial Intelligence in Agriculture Market Insights

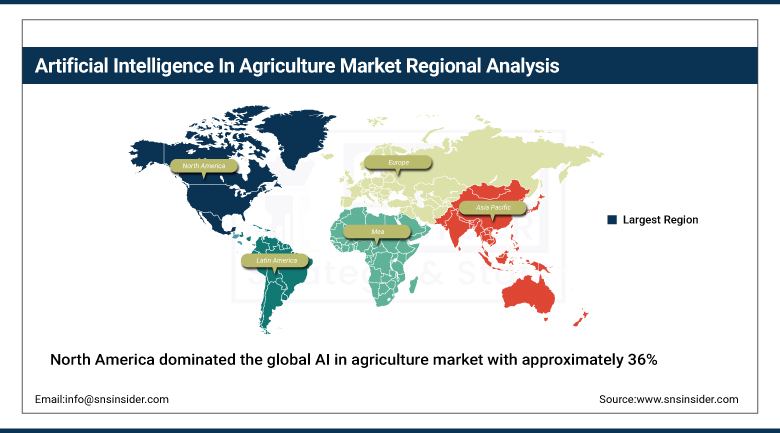

North America dominated the global AI in agriculture market with approximately 36% of revenues in 2025, driven by strong technological innovation, early adoption of precision farming solutions, advanced agri tech infrastructure, and supportive government policies. The United States accounts for approximately 87.4% of North American revenues through John Deere, The Climate Corporation, Trimble Agriculture, AG Leader Technology, and Corteva Agriscience’s commercial operations.

Canada contributes approximately 12.6% of North American revenues through the Protein Industries Canada’s AI agriculture investment programme, the western Canadian grain farming sector’s precision agriculture adoption, and the growing agri tech startup ecosystem in Guelph, Saskatoon, and Vancouver that creates innovation above the installed base procurement trend.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Artificial Intelligence in Agriculture Market Insights

Europe is a sophisticated AI in agriculture market where the European Green Deal’s Farm to Fork strategy, the Common Agricultural Policy’s digital farming support programmes, and strong sustainability mandates create structured institutional adoption. Germany accounts for approximately 22.3% of European revenues through its large commercial farm sector’s precision agriculture investment, John Deere’s European operations, and the agri tech startup ecosystem centred around Berlin and Munich.

The Netherlands, France, and the United Kingdom are significant secondary markets where Dutch greenhouse technology leadership, French wine and cereal precision farming adoption, and UK Research and Innovation’s agricultural AI funding programmes create consistent AI agriculture procurement. BASF’s xarvio digital farming platform and Bayer’s European precision agriculture operations sustain commercial supply.

Asia Pacific Artificial Intelligence in Agriculture Market Insights

Asia Pacific is the fastest growing regional AI in agriculture market, driven by food security concerns across densely populated nations, population growth creating above average food demand pressure, rising agri tech startup activity, and government backed digital farming programmes in China, India, Japan, South Korea, and Southeast Asia. China accounts for approximately 44.8% of Asia Pacific revenues through government smart agriculture investment, the large domestic agri tech company ecosystem, and the extraordinary scale of Chinese agricultural production that creates proportional precision farming technology demand.

India represents the most commercially dynamic emerging market within Asia Pacific where the government’s Digital Agriculture Mission, the extraordinary smallholder farmer population whose aggregate AI advisory service adoption creates substantial market scale despite low per farm investment, and the rapidly growing agri tech startup ecosystem in Bengaluru and Pune create above average AI agriculture market growth.

MEA & Latin America Artificial Intelligence in Agriculture Market Insights

Israel leads MEA revenues at approximately 31.2% through its globally recognised precision agriculture technology leadership, drip irrigation AI integration, and CropX, Taranis, and Prospera Technologies’ commercial operations creating above average per hectare AI agriculture investment. UAE’s smart greenhouse and vertical farming investment adds complementary demand. Brazil leads Latin American revenues at approximately 44.2% through its large scale soybean and sugarcane precision farming adoption, the government’s Embrapa digital agriculture programme, and the extraordinary commercial farm scale that sustains premium precision technology investment. Argentina’s soy and corn precision farming collectively sustain regional growth through 2035.

Growth Drivers: Agricultural labour shortage and food security pressure creating structural AI adoption motivation across farm sizes

Persistent and worsening agricultural labour shortage is the AI in agriculture market’s most commercially compelling structural growth driver across both developed and developing economies. Each year of minimum wage increase, each seasonal agricultural visa programme that fails to fill harvest labour requirements, and each farm operation that cannot recruit adequate permanent staff creates economic motivation for AI powered automation investment whose ROI calculation improves proportionally with avoided labour cost. The U.S. agricultural labour shortage, estimated at hundreds of thousands of unfilled seasonal positions annually, creates investment motivation for robotic harvesting, autonomous weeding, and AI guided crop management that sustains above average technology adoption spending among large commercial farm operators.

Global food security pressure from population growth projected to reach 9.7 billion by 2050, climate variability that creates yield uncertainty, and arable land constraints that limit area expansion collectively create structural demand for AI tools that improve yield per hectare from the existing agricultural land base. Each percentage point improvement in crop yield efficiency that AI precision management enables creates food security value whose importance to national agricultural policy creates government programme investment that sustains AI agriculture adoption beyond purely commercial farm operator procurement motivation.

Restraints: High upfront cost and digital literacy barriers for smallholder farmers

High upfront cost of AI agriculture technology creates adoption barriers for small and smallholder farm operations whose capital budget constraints prevent investment in precision agriculture hardware, software subscriptions, and connectivity infrastructure whose combined cost exceeds short term production economics payback for low acreage operations. Each developing country farm whose average holding size of 1 to 2 hectares creates a total addressable technology investment that commercial precision agriculture platforms’ pricing models cannot profitably serve without significant subsidy or cooperative aggregation.

Digital literacy barriers among traditional farm operator populations, particularly in developing economies where educational access and technology familiarity create adoption resistance, moderate the pace at which AI agriculture technology penetrates beyond the early adopter commercial farming segment. Each farm operator whose technology adoption confidence requires hands on training, local language interface, and ongoing technical support creates customer acquisition cost that slows adoption curve progression.

Opportunities: Generative AI farm advisory integration and carbon credit programme AI verification

Generative AI farm advisory platform development represents the most commercially accessible near-term market expansion opportunity whose natural language farmer interface eliminates the digital literacy barrier that conventional precision agriculture software’s complex data interpretation requires. Each generative AI system that can answer a farmer’s crop management question in local language from real time field sensor data creates adoption accessibility that expert system and dashboard-based AI agriculture platforms cannot achieve among technology hesitant farm operator populations.

Carbon credit programme AI verification represents a growing commercial opportunity as agricultural carbon markets’ need for verifiable soil carbon sequestration measurement creates demand for AI soil monitoring platforms whose remote sensing and machine learning analysis provides measurement, reporting, and verification capability at farm scale economics that physical soil sampling cannot match. Each carbon credit programme that adopts AI based MRV creates sustained recurring revenue for AI agriculture monitoring platforms whose value grows with carbon credit programme adoption.

Recent Developments:

-

2024: Bayer Crop Science began developing a new AWS based data science platform in August 2024 with generative AI capabilities built with Amazon SageMaker Studio and Bedrock, targeting innovative agricultural advisory solutions with production models expected by 2025.

-

2024: John Deere announced a strategic partnership with NVIDIA in May 2024 to develop real time AI analytics for self-driving tractor platforms, combining NVIDIA Jetson Orin edge computing with John Deere’s autonomous guidance systems for real time field condition adaptation.

-

2024: IBM launched a new AI based weather forecasting tool in June 2024 tailored specifically for small scale farmers in Africa and South Asia, providing localised weather prediction and crop advisory services through mobile interfaces accessible without advanced connectivity infrastructure.

-

2024: Bayer Crop Science unveiled its AI powered disease detection platform for wheat and corn crops in April 2024, using satellite imagery analysis and machine learning models to identify foliar disease infection at early stages before visible symptoms cause economically significant yield loss.

-

2023: Protein Industries Canada opened an expanded call for projects in November 2023 under the Pan Canadian Artificial Intelligence Strategy, considering projects spanning the entire agriculture and food value chain from seed genetics to on farm production, ingredient manufacturing, food processing, and logistics.

Artificial Intelligence in Agriculture Market Key Players

-

John Deere

-

The Climate Corporation

-

Trimble Inc.

-

AG Leader Technology

-

IBM Corporation

-

Microsoft Corporation

-

NVIDIA Corporation

-

Raven Industries

-

DJI Innovations

-

Taranis

-

Prospera Technologies

-

Aerobotics

-

Iron Ox

-

Carbon Robotics

-

Harvest CROO Robotics

-

BASF SE

-

Kubota Corporation

-

AgriForce Growing Systems

Artificial Intelligence in Agriculture Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.78 Billion |

| Market Size by 2035 | USD 24.55 Billion |

| CAGR | CAGR of 24.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Offering (Software, Hardware, AI as a Service) • by Technology (Machine Learning & Deep Learning, Computer Vision, Predictive Analytics, Natural Language Processing, Others) • by Application (Precision Farming, Agriculture Robots, Drone Analytics, Livestock Monitoring, Smart Greenhouse Management, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | John Deere, The Climate Corporation, Trimble Inc., AG Leader Technology, Corteva Agriscience, IBM Corporation, Microsoft Corporation, NVIDIA Corporation, Raven Industrie, DJI Innovation, Taranis, CropX Technologies, Prospera Technologies, Aerobotics, Iron Ox, Carbon Robotics, Harvest CROO Robotics, BASF SE , Kubota Corporation, AgriForce Growing Systems |

Frequently Asked Questions

The Artificial Intelligence in Agriculture Market is expected to grow at a CAGR of 24.34% from 2026 to 2035.

Persistent agricultural labour shortage creating economic motivation for AI powered automation investment, and global food security pressure from population growth requiring above average yield improvement per hectare that AI precision farming tools enable through optimised input application, disease detection, and harvest timing.

The Artificial Intelligence in Agriculture Market was valued at USD 2.78 Billion in 2025.

Software dominated the Artificial Intelligence in Agriculture Market with approximately 55% share in 2025, while the Hardware segment is the fastest growing.

North America dominated the Artificial Intelligence in Agriculture Market with approximately 36% of revenues in 2025, while Asia Pacific is the fastest growing region driven by food security pressure, population growth, and government backed digital farming programmes.

Get in Touch