Naltrexone And Buprenorphine Market Report Scope & Overview:

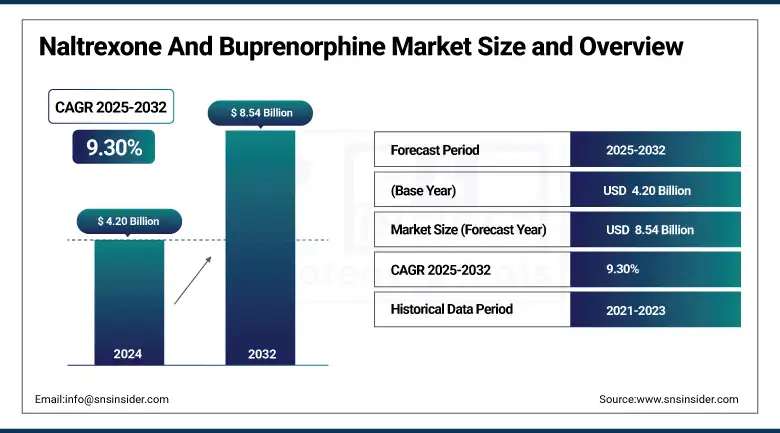

The naltrexone and buprenorphine market size was valued at USD 4.20 billion in 2024 and is expected to reach USD 8.54 billion by 2032, growing at a CAGR of 9.30% over 2025-2032.

Rising prevalence of opioid use disorders globally and higher acceptance of medication-assisted treatment (MAT) programs are driving the naltrexone and buprenorphine market. Increased awareness about opioid dependency, primarily in North America and some Western European countries, is likely to drive healthcare professionals to prescribe naltrexone and buprenorphine on a larger scale.

To Get more information On Naltrexone And Buprenorphine Market - Request Free Sample Report

In April 2024, Indivior rolled out a new digital support program that is connected to buprenorphine treatment, utilizing prescription AI-based adherence tracking, a significant step in the direction of integrating digital health with MAT.

With an estimated 296 million people globally using drugs in 2021 (UNODC), there is an increasing need for treatments for opioid dependence. Additionally, the naltrexone and buprenorphine market growth is being driven by the government initiatives, including wider insurance coverage of MAT (Medicaid in the U.S.) and payment schemes. Meanwhile, drug manufacturers are upping R&D spending, in part to develop long-acting injectables and combo products that improve compliance and effectiveness. For instance, Indivior and Alkermes are major naltrexone and buprenorphine manufacturers that emphasize innovation and availability.

For instance, regulatory backing, FDA authorizations for extended-release buprenorphine (Sublocade), and injectable naltrexone (Vivitrol), also contribute to the naltrexone buprenorphine market share by enhancing treatment adherence. On the supply side, expanded manufacturing facilities and funding by national drug control programs to reduce the treatment gap, coupled with a rise in spending on behavioral healthcare and telemedicine to improve patient access, have been driving naltrexone and buprenorphine market growth globally. This swirling mix of demand, regulatory push, and changing therapeutic modalities is projected to continue to capture naltrexone and buprenorphine market analysis results.

In 2023, Alkermes revealed expanded clinical studies for Vivitrol (naltrexone) in conjunction with cognitive behavioral therapy (CBT) in hopes of further boosting the recovery rates, and a key phenomenon in the integrated care models and the naltrexone and buprenorphine market trends.

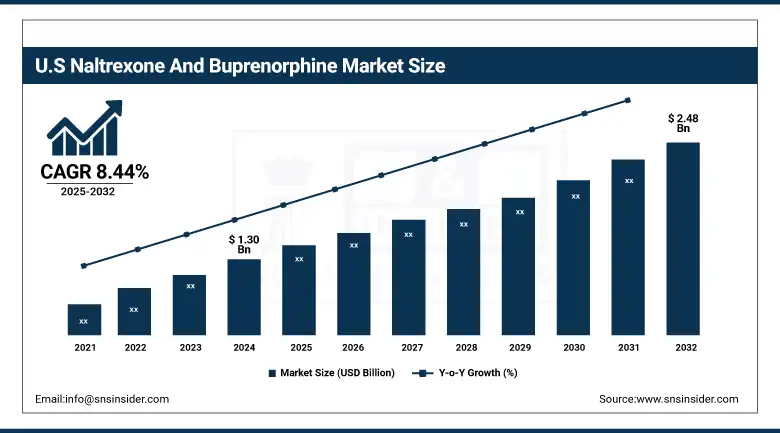

The U.S. naltrexone and buprenorphine market size was valued at USD 1.30 billion in 2024 and is expected to reach USD 2.48 billion by 2032, growing at a CAGR of 8.44% over 2025-2032. In the U.S., the regional market is handled primarily by the U.S. market, which is mainly dominated by well-established reimbursement support, treatment protocols, and changes in policy, such as the removal of the X-waiver to prescribe buprenorphine.

Market Dynamics:

Drivers:

-

Expanding Access to Treatment and Technological Advancements Boosting Adoption for Naltrexone and Buprenorphine Market

Growing access to naltrexone and buprenorphine globally, heightened government support, and advancements in drug delivery devices are factors driving the naltrexone and buprenorphine markets. The number of people with opioid use disorder (OUD), totaling >60 million globally, is one main driving force behind the increase in demand for medication-assisted therapies.

Government commitments to address the opioid crisis are significant. For instance, in 2023, Congress appropriated USD 4.8 billion to support treatment programs and increased MAT access through SAMHSA. Furthermore, the development of technologies, such as long-acting depot injections and subdermal implants, has led to enhanced patient compliance with a low risk of relapse, in turn stimulating the growth of the naltrexone and buprenorphine market.

Braeburn Pharmaceuticals and others are developing long-acting formulations for buprenorphine, including Brixadi, currently approved for weekly and monthly dosing by the FDA in 2023. Furthermore, simplified regulatory routes and revised standards, including the elimination of the X-waiver requirement for buprenorphine prescribing in the U.S., are expanding the pool of licensed prescribers. Integration of telehealth after COVID-19 has increased access to MAT, particularly in rural areas with limited resources, thereby enhancing overall global naltrexone and buprenorphine market analysis.

Restraints:

-

Stigma, Regulatory Barriers, and Limited Access Hamper Market Expansion

Several restraints are still impacting the naltrexone and buprenorphine market, despite an increasing demand. One significant barrier is MAT (medication-assisted treatment) related stigma, which restricts reach, even among individuals who have been diagnosed. Even if the 1.0:2.41 ratio is sufficient, only 11% of individuals in need of MAT received it in 2022, based on the National Survey on Drug Use and Health (NSDUH), indicating a substantial treatment penetration deficit. Further, limited provider infrastructure and shortage of MAT-trained physicians in low- and middle-income countries (LMICs) limit global scalability of treatment. Regulatory limitations, particularly in areas with rigid narcotic regulating laws, are dampening the market analysis of Maltrexone and Buprenorphine.

In many European countries, for instance, restrictive buprenorphine prescription practices keep access extremely low despite increasing demand. Furthermore, supply-side issues, such as the manufacture of depot or implantable formulations, are expensive and could delay the deployment. LMICs have a low level of spending on R&D, and the markets in such countries are imbalanced. Pharmaceutical companies are also under legal scrutiny, and for instance, Indivior paid more than USD 600 million in 2020 to settle charges related to marketing, which raised red flags with regulators. Finally, attitudes of people with substance use disorder regarding side effects, withdrawal treatment, and the stigmatization of MAT as “replacing one drug with another” further obstruct treatment acceptance, despite the unambiguous clinical advantages, which, in turn, limits the market share potential for naltrexone and buprenorphine in some areas and with some populations.

Segmentation Analysis:

By Product

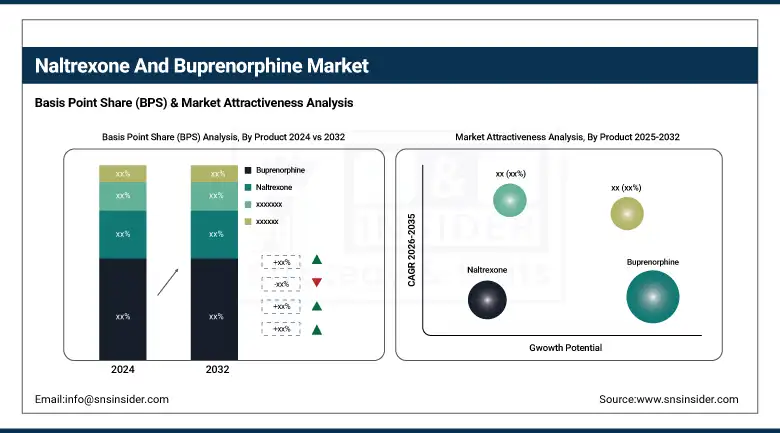

Buprenorphine accounted for 73.53% revenue share in the global market in 2024. This dominance is largely attributable to its superior effectiveness for the treatment of opioid use disorder (OUD), its reduced abuse potential owing to partial agonism, and multiple available formulations. Buprenorphine’s diverse route of administration, including oral, injectable, and implantable formulations, renders it well suited for treatment in clinical and outpatient contexts.

Meanwhile, the naltrexone segment is expected to be the fastest expanding, fueled by growing penetration for the treatment of alcohol use disorder (AUD) and increasing demand for long-acting injectable format, which can enhance patient adherence.

By Route of Administration

Based on the route of administration, the injectable buprenorphine segment dominated the market with a share of 68.14% in 2024. Rising preference for depot injections that decrease dosage frequency and increase compliance, particularly amongst the high-risk pool, has enhanced the growth of this segment.

The oral naltrexone segment, on its part, is estimated to register the highest CAGR since it is largely prescribed as compared to the implants on account of convenience and price, and will capture 55.14% of the naltrexone market share by 2024.

By Application

Concerning the application, OUD was the major indication in both drug segments, with OUD contributing 69.52% revenue share in the naltrexone segment in 2024. The increase in opioid addiction and the initiation of national support programs for medication-assisted treatment (MAT) have increased its application.

Alcohol use disorder in the naltrexone space is also set to grow rapidly in the future, with heightened disease diagnosis and treatment guidelines changing to reflect the efficacy of naltrexone to reduce alcohol relapse.

By Distribution Channel

In terms of distribution channels, hospital pharmacies contributed to the largest market share of 47.93% in 2024, owing to controlled treatment protocols and easy access to monitored care for high-risk OUD patients.

Retail pharmacies are likely to have the fastest growth, driven by regulatory changes expanding access to outpatient MAT and greater prescribing of oral agents for chronic relapse prevention.

Regional Analysis:

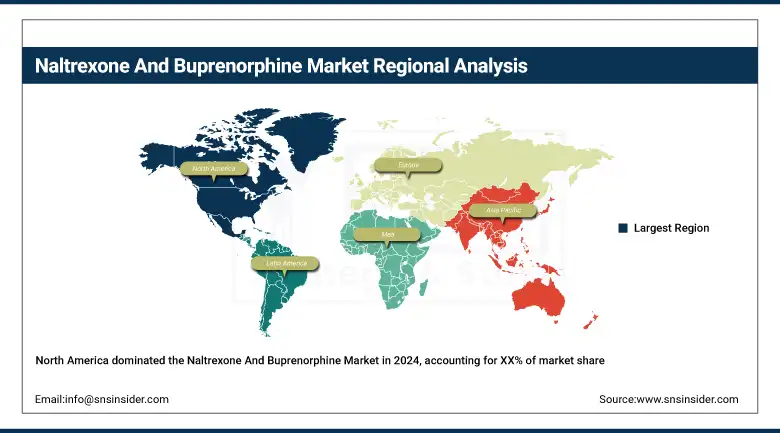

The North American naltrexone and buprenorphine market led the market in 2024, due to the high prevalence of opioid use disorder (OUD), large numbers of government initiatives, and easy availability of medication-assisted treatments (MAT).

Get Customized Report as per Your Business Requirement - Enquiry Now

By 2023, more than 2.1 million U.S. residents were diagnosed with OUD, indicating substantial demand for treatment. Combine this with strategic investments made in harm-reduction programmes, and the market uptake of long-acting injectable drugs like Sublocade and Brixadi increased. Canada is the fastest-growing country in the region due to MAT implementation and favorable country policies for opioid agony therapy (OAT). The proliferation of telehealth delivery models for addiction care is also making treatment more available in rural and underserved populations, in both the U.S. and Canada.

Europe is the second biggest and ever-changing market with increasing opioid dependence and the unification of MAT in the public healthcare system, and harm-reduction policies. The U.K. is the first-ranking state owing to its advanced drug policies, wide free availability of drug treatment in the form of the NHS, and widespread use of buprenorphine treatment. Opioid related deaths represented just under 49% of drug misuse deaths as of 2023, which serves to highlight the importance of effective treatments. Germany is the fastest-growing MAT market in Europe, owing to its recent regulatory changes leading to ease of access to MAT and a rapidly increasing number of opioid addicted patients. Moreover, countries such as France and Spain are increasing the government-sponsored addiction centers, which are likely to support regional growth. An increasing number of pharmaceutical R&D activities into extended-release naltrexone across Europe are also one of the factors that are driving the growth of the naltrexone and buprenorphine market in the region.

The Asia Pacific market is poised for the fastest growth, with a rising number of opioid abuse incidences, government-led awareness programs, and investment in mental health infrastructure. This region is made up of India, which averages the highest utilization, driven by a large population of people with opioid dependence, which numbers more than 2 million, as per the Ministry of Social Justice & Empowerment. The naltrexone and buprenorphine market growth has been driven by an increasing number of de-addiction centers, government initiatives funded through programs, such as Nasha Mukt Bharat Abhiyaan, and the low price of generic buprenorphine.

China and Australia have also played a significant role, with China using OAT programmes and Australia using its extensive health infrastructure to introduce more recent MAT methods. Japan is growing at a steady pace owing to the rise of clinical research and government support for new formulations. Telemedicine-based addiction care and public–private partnerships, in addition to ethnic vendors, will continue enhancing treatment accessibility in APAC, thereby continuing to fuel the naltrexone and buprenorphine market growth.

Key Players:

Leading naltrexone and buprenorphine companies operating in the market include Indivior PLC, Collegium Pharmaceutical (BioDelivery Sciences International, Inc.), Alkermes, Inc., Orexo US, Inc., Titan Pharmaceuticals, Omeros Corporation, Camurus, Sun Pharmaceutical Industries Ltd., Teva Pharmaceuticals, and Dr. Reddy’s Laboratories.

Recent Developments:

In February 2025, the FDA approved crucial label updates for SUBLOCADE (buprenorphine extended-release), including a rapid initiation protocol (treatment can begin just one hour after transmucosal buprenorphine) and authorization for additional injection sites (thigh, buttock, arm), enhancing flexibility, convenience, and patient adherence.

In January 2025, Delpor Inc. progressed into Phase 3 near-ready design for a titanium-based implant capable of delivering naltrexone for up to one year. Backed by NIH HEAL funding, this long-duration implant promises enhanced compliance and reversibility, ideal for both opioid and alcohol use disorders.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.20 billion |

| Market Size by 2032 | USD 8.54 billion |

| CAGR | CAGR of 9.30% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Naltrexone, Buprenorphine (BELBUCA, Sublocade, Suboxone, Zubsolv, and Others) • By Route of Administration (Naltrexone, (Oral Administration, Injectable Administration, and Implantable Administration), Buprenorphine (Oral Administration, Injectable Administration, and Implantable Administration) • By Application (Naltrexone, (Opioid use disorder (OUD), Alcohol use disorder (AUD))), Buprenorphine (Opioid use disorder (OUD)) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Indivior PLC, Collegium Pharmaceutical (BioDelivery Sciences International, Inc.), Alkermes, Inc., Orexo US, Inc., Titan Pharmaceuticals, Omeros Corporation, Camurus, Sun Pharmaceutical Industries Ltd., Teva Pharmaceuticals, and Dr. Reddy’s Laboratories. |

Frequently Asked Questions

North America dominated the Naltrexone and Buprenorphine market.

One significant barrier is MAT (medication-assisted treatment) related stigma, which restricts reach, even among individuals who have been diagnosed.

Growing access to naltrexone and buprenorphine globally, heightened government support, and advancements in drug delivery devices are factors driving the naltrexone and buprenorphine market.

The market is expected to reach USD 8.54 billion by 2032, increasing from USD 4.20 billion in 2024.

The Naltrexone and Buprenorphine market is anticipated to grow at a CAGR of 9.30% from 2025 to 2032.

Get in Touch