Healthcare Transportation Services Market Report Scope & Overview:

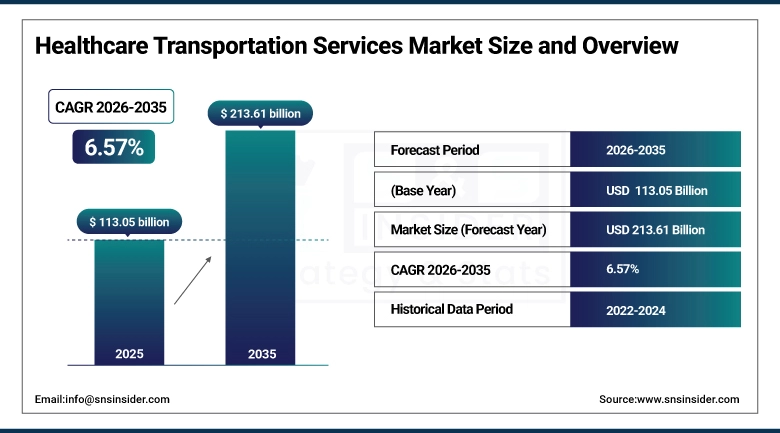

The Healthcare Transportation Services Market size was valued at USD 113.05 Billion in 2025 and is expected to reach USD 213.61 Billion by 2035, growing at a CAGR of 6.57% over the forecast period of 2026-2035.

The growth of the Global Healthcare Transportation Services Market includes the increasing need for timely patient mobility solutions, the increasing rate of chronic health conditions, and the increasing population of older adults with regular health visits. The transportation of patients, health practitioners, and health products between health facilities is a critical service in the health sector. The expansion of health facilities, the increasing health expenditure, and the need for accessible health transportation services are the major factors driving the growth of the global healthcare transportation services market. The increasing need for GPS tracking of ambulances, the integration of dispatch management services, and the incorporation of telemedicine services in transportation services are the major factors driving the growth of the global healthcare transportation services market. The increasing government support for non-emergency health transportation services and the partnership between health facilities and transportation services providers is also a major factor driving the growth of the global healthcare transportation services market.

In February 2025, several hospital networks across North America integrated AI-enabled fleet management systems for ambulance services, reducing emergency response times by nearly 22% and significantly improving patient transport efficiency.

Healthcare Transportation Services Market Size and Forecast:

-

Market Size in 2025: USD 113.05 Billion

-

Market Size by 2035: USD 213.61 Billion

-

CAGR: 6.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Healthcare Transportation Services Market - Request Free Sample Report

Healthcare Transportation Services Market Trends:

-

Increasing integration of digital dispatch platforms and GPS-enabled tracking systems to improve ambulance routing efficiency and emergency response time.

-

Growing adoption of non-emergency medical transportation (NEMT) services for elderly patients and individuals with mobility limitations requiring routine healthcare visits.

-

Rising demand for air ambulance services for long-distance emergency transfers and critical care patient transportation.

-

Expansion of partnerships between hospitals and private transport providers to ensure reliable patient mobility solutions.

-

Introduction of advanced life support ambulances equipped with modern monitoring devices, ventilators, and life-saving medical equipment.

-

Growing implementation of telemedicine integration in ambulance services enabling remote clinical guidance during patient transport.

-

Development of specialized transport services for organ transplantation logistics and critical medical product delivery.

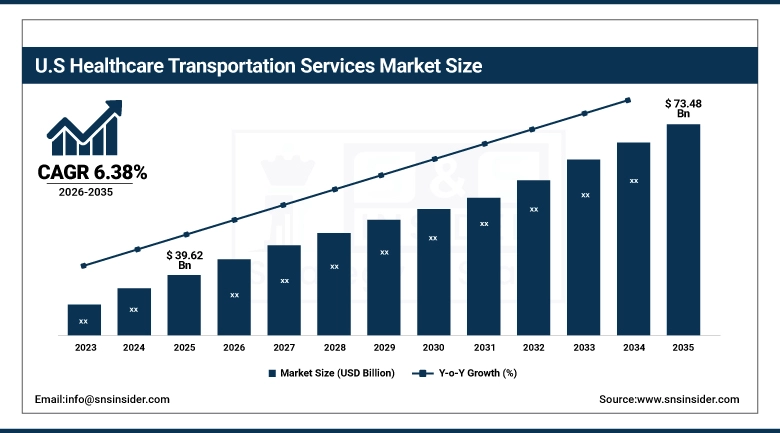

The U.S. Healthcare Transportation Services Market is estimated at USD 39.62 billion in 2025 and is expected to reach USD 73.48 billion by 2035, growing at a CAGR of 6.38% from 2026-2035. The market dominance in the United States is attributed to the significant market size, which is driven by the development of emergency medical services, healthcare spending, and the establishment of effective regulatory systems in patient transport services. The expansion of Medicaid-funded non-emergency patient transport services has increased the availability of patient transport services in the United States. The presence of private ambulance services, the adoption of advanced medical technology, and the expansion of healthcare facilities are factors driving the market in the United States.

Healthcare Transportation Services Market Growth Drivers:

-

Rising Demand for Efficient Emergency Medical Services Driving Market Growth

The increasing need for rapid response services is one of the major factors contributing to the growth of the healthcare transportation services market. Emergency response services play a major role in the survival of human lives by providing easy access to hospital facilities in the case of an accident, heart attack, trauma, and other critical health conditions. The increasing rate of road accidents, natural calamities, and health emergencies is creating a huge need for advanced ambulance services and the skills of the emergency response teams. The latest ambulances are equipped with advanced monitoring equipment, ventilators, cardiac defibrillators, and telecommunication facilities that enable the response teams to offer the best pre-hospital services. In addition, the government is investing in the infrastructure of emergency response services and the expansion of the ambulance network.

For instance, in April 2025, several European healthcare authorities expanded their advanced life support ambulance fleets by nearly 18%, improving emergency medical response coverage in rural and urban regions.

Healthcare Transportation Services Market Restraints:

-

High Operational Costs and Infrastructure Challenges Limiting Market Expansion

In spite of the strong demand for medical transportation services, the high costs of operating the ambulances, the equipment, and the personnel hired to operate them pose a major challenge in the growth of the market. Emergency transportation services require consistent and continuous investment in the maintenance of the vehicles, fuel, equipment, and training of the personnel to ensure the quality of service. In addition, the need to comply with the regulations and licensing of the services in different countries poses a challenge to the service providers. In many developing countries, the lack of health infrastructure and the availability of emergency transportation services may hinder the growth of the healthcare transportation services.

Healthcare Transportation Services Market Opportunities:

-

Expansion of Non-Emergency Medical Transportation Services Creating Market Opportunities

There are great opportunities in the healthcare transportation services market with the increased growth of non-emergency medical transportation services. Patients with chronic health conditions, physical disabilities, and old age are in need of transport services for attending routine medical check-ups, rehabilitation, and diagnostic tests. Non-emergency medical transport services offer cost-effective transport services for patients with chronic health conditions, physical disabilities, and old age. Governments are collaborating with transport companies specializing in healthcare transport services, thereby facilitating the access of underserved patients to healthcare services. The use of ride-sharing services, along with mobile apps, for transporting patients is enhancing the serviceability of non-emergency medical transport services.

For example, in January 2025, a major healthcare transportation provider introduced an app-based non-emergency transport platform that improved patient scheduling efficiency and reduced missed hospital appointments by nearly 30%.

Healthcare Transportation Services Market Segment Analysis:

-

By type, emergency medical transportation accounted for the largest share of 61.42% in 2025, while the non-emergency medical transportation segment is anticipated to grow at the fastest CAGR of 7.21% during the forecast period.

-

By provider type, the private segment held the highest market share of approximately 64.18% in 2025 and is expected to continue dominating the market due to increasing outsourcing of transportation services by hospitals.

-

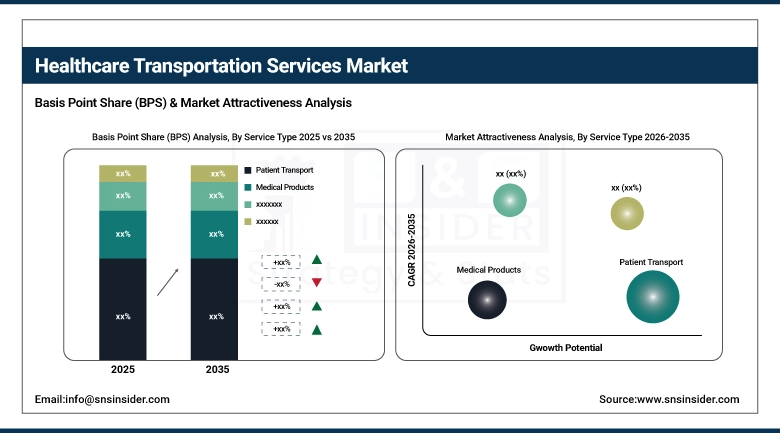

By service type, patient transport services accounted for the largest share of around 56.74% in 2025 owing to rising patient mobility requirements.

-

By end-user, hospitals & ASCs held the largest revenue share of nearly 49.63% in 2025 due to high demand for emergency and interfacility patient transportation.

By Service Type, Patient Transport Services Hold the Largest Market Share

However, patient transportation services were the dominant services in the market, with a revenue share of about 56.74% in 2025. Hospitals and healthcare centers require transport services for the movement of patients from one department to another, diagnostic centers, rehabilitation centers, and specialized treatment centers, among others. The movement of patients in healthcare centers is important in the delivery of healthcare services, as it helps in the efficient execution of treatment procedures.

By Type, Emergency Medical Transportation Dominates While Non-Emergency Medical Transportation Expands Rapidly

The segment of emergency medical transportation services accounted for the highest market share of around 61.42% in the healthcare transportation services market in 2025. This is because ambulances and air ambulance services play a vital role in providing timely medical response services during emergencies. The increasing number of cases of cardiovascular diseases, trauma injuries, and accidents has always fueled the demand for advanced emergency medical transportation services. Basic life support and advanced life support ambulances are commonly used by hospitals and other emergency medical services for the transportation of patients to healthcare centers for timely medical care and treatment.

Non-emergency medical transportation services are expected to grow at the highest CAGR of 7.21% during the forecast period. This segment is fueled by the increasing number of patients with limited mobility and the requirement for regular medical check-ups and treatment. Wheelchair transportation services and stretcher services are also becoming popular among patients with limited mobility.

By Provider Type, Private Service Providers Lead the Market

The private sector segment dominated with a significant share of around 64.18% in 2025 due to a rise in hospital and healthcare establishments that increasingly opt for outsourcing patient transportation services to specialized companies. Private healthcare transportation companies provide better fleet management systems, medical staff, and vehicles that provide safe patient transportation. Also, private sector companies provide better flexible models and faster response times compared to public transportation networks.

By End-User, Hospitals & ASCs Lead the Market

Hospitals and ambulatory surgical centers have shown a high market share in revenue generation, which is nearly 49.63% in 2025, owing to the high demand for emergency patient transport, interfacility transfers, and specialized medical transport services. Patient admissions and expansions in healthcare facilities are some of the major factors that contribute to the adoption of healthcare transportation services in hospitals.

Healthcare Transportation Services Market Regional Highlights:

North America Healthcare Transportation Services Market Insights:

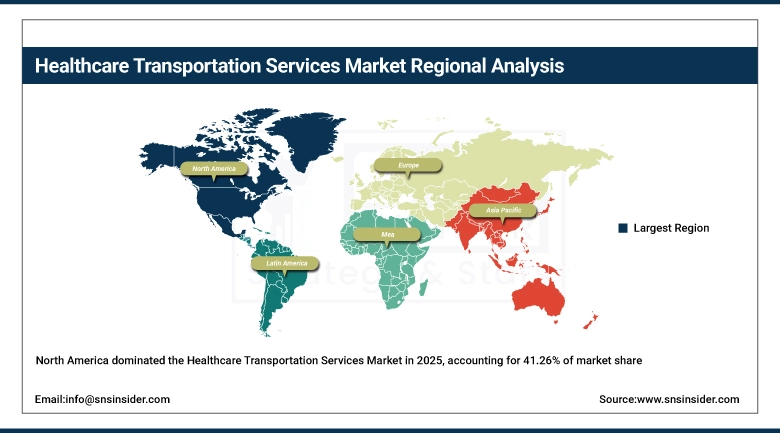

North America has the highest revenue share of approximately 41.26% in 2025 due to the presence of a well-established emergency medical services infrastructure, as well as government support for medical transportation programs. Additionally, there is access to advanced ambulance technology, trained paramedic staff, and adequate insurance coverage for emergency as well as non-emergency medical transportation services.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Healthcare Transportation Services Market Insights:

The Asia Pacific region is expected to witness the highest growth rate, i.e., 7.18%, during the forecast period. This is due to increasing healthcare infrastructure, urbanization, and awareness about healthcare services. Countries such as China and India are investing heavily in emergency medical services, such as ambulances, to enhance access to healthcare services. Increasing expenditure on healthcare services, hospitals, etc., is also driving the market growth in this region.

Europe Healthcare Transportation Services Market Insights:

Europe represents the second-largest regional market due to the high standards of healthcare facilities in Europe, well-developed emergency healthcare facilities, and increased investments by European governments in healthcare infrastructure. Countries such as Germany, France, and the UK have well-developed ambulance and healthcare transport facilities that provide efficient healthcare services.

Latin America (LATAM) and Middle East & Africa (MEA) Healthcare Transportation Services Market Insights:

Healthcare transportation services markets in Latin America and the Middle East & Africa are expanding steadily due to improving healthcare infrastructure, rising emergency response initiatives, and increasing private sector participation in medical transport services. Governments in these regions are focusing on expanding ambulance networks and improving healthcare accessibility in rural and underserved communities.

Healthcare Transportation Services Market Competitive Landscape:

Falck A/S (founded in 1906) is a leading provider of emergency response and healthcare transportation services globally, offering ambulance services, patient transport, and medical emergency response solutions through a large international fleet.

-

In March 2025, Falck expanded its advanced life support ambulance fleet in Europe to strengthen emergency medical service coverage across several urban regions.

Global Medical Response (founded in 2015) provides emergency and non-emergency medical transportation services across the United States, operating one of the largest ambulance networks in the country.

-

In January 2025, the company integrated advanced digital dispatch technology across its ambulance network to improve response time and operational efficiency.

Acadian Ambulance Service (founded in 1971) offers emergency medical services, air ambulance operations, and non-emergency patient transportation services across multiple regions.

-

In February 2025, the company launched new air ambulance units equipped with advanced telemedicine systems for critical patient monitoring during transport.

Healthcare Transportation Services Market Key Players:

-

Falck A/S

-

Global Medical Response

-

Acadian Ambulance Service

-

American Medical Response

-

Air Methods Corporation

-

REVA Air Ambulance

-

Medivic Aviation

-

Ziqitza Healthcare

-

BVG India Limited

-

London Ambulance Service

-

Rural/Metro Corporation

-

Envision Healthcare

-

ProTransport-1

-

Lifeguard Ambulance Service

-

First Care Ambulance

-

AirMed International

-

Metro Aviation

-

IAS Medical

-

Response Plus Medical

-

Falcon Emergency Air Rescue

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 113.05 Billion |

| Market Size by 2035 | USD 213.61 Billion |

| CAGR | CAGR of 6.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Emergency Medical Transportation (Basic Life Support Ambulances, Advanced Life Support Ambulances, Air Ambulances, Others), Non-Emergency Medical Transportation (Ambulatory Transportations, Stretchers, Wheelchairs, Others) • By Provider Type (Private, Public) • By Service Type (Patient Transport, Medical Products, and Others) • By End-User (Hospitals & ASCs, Specialty Clinics, Nursing Care Facilities, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Falck A/S, Global Medical Response, Acadian Ambulance Service, American Medical Response, Air Methods Corporation, REVA Air Ambulance, Medivic Aviation, Ziqitza Healthcare, BVG India Limited, London Ambulance Service, Rural/Metro Corporation, Envision Healthcare, ProTransport-1, Lifeguard Ambulance Service, First Care Ambulance, AirMed International, Metro Aviation, IAS Medical, Response Plus Medical, Falcon Emergency Air Rescue |

Frequently Asked Questions

Market growth is driven by the rising demand for emergency medical services, increasing prevalence of chronic diseases, growing elderly population, and expanding healthcare infrastructure worldwide.

The Healthcare Transportation Services Market is expected to reach USD 213.61 billion by 2035, growing from USD 113.05 billion in 2025 at a CAGR of 6.57% during 2026–2035.

Emergency medical transportation dominates the market, accounting for 61.42% of the total market share in 2025 due to the increasing demand for rapid emergency response and advanced ambulance services.

North America holds the largest market share with 41.26% revenue share in 2025, supported by advanced emergency medical services infrastructure and strong government-backed medical transportation programs.

Significant opportunities exist in the expansion of non-emergency medical transportation (NEMT), integration of digital dispatch platforms, telemedicine-enabled ambulance services, and app-based medical transport booking systems.

Get in Touch