Sciatica Treatment Market Size & Trends:

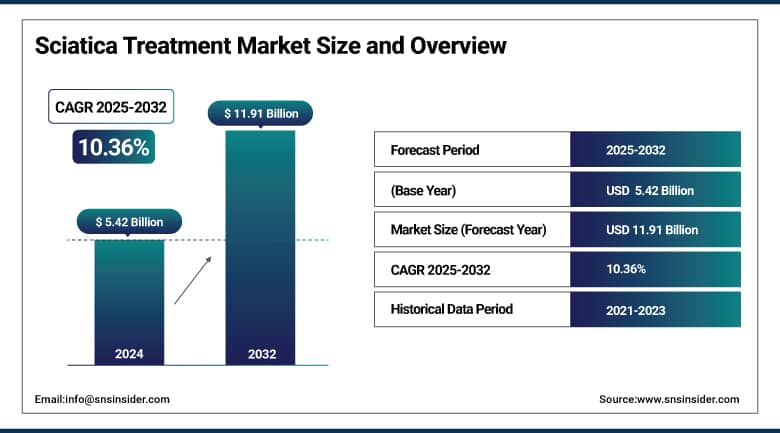

The Sciatica Treatment Market size was valued at USD 5.42 billion in 2024 and is expected to reach USD 11.91 billion by 2032, growing at a CAGR of 10.36% over 2025-2032.

The global sciatica treatment market is witnessing strong growth on the back of multiple factors, such as the increasing prevalence of the disease, inclination toward non-opioid treatments, and a surge in spending on alternative treatments. Additionally, utilization of complementary health approaches, including acupuncture and spinal manipulation, has increased dramatically from 2002 to 2022, according to reports from the CDC and NCCIH. In the meantime, the increased knowledge of the opioid epidemic has promoted the demand for non-opioid and integrative solutions for pain management, supporting the further expansion of the sciatica treatment market. A favorable healthcare reimbursement landscape and strong regulatory framework promoting the adoption of novel treatments drive the U.S. sciatica treatment industry.

The studies have shown a 50% lower likelihood of going in for an operation with the help of inversion. Increasing R&D outlays, clear from Naproxen testing and cutting-edge neurostimulation products, indicate an ongoing flow of new therapies. In addition, recent articles published in PubMed have highlighted a substantial increase in the number of reports on the treatment of sciatica with pharmacological and non-invasive therapies, demonstrating a dynamic academic and clinical research context.

Sciatica treatment market trend are rising preference for physical therapy and interventional pain procedures against surgical intervention and opioid therapy, and the development of personalized, multidisciplinary pain management strategies. Additional demand is generated by an ever-increasing sedentary lifestyle and aging population, both factors associated with an increased prevalence of disorders of the lumbar spine. There’s a trend of diversification in the sciatica treatment market share, with new sciatica treatment companies focusing on AI-based diagnostics and wearable tech for real-time monitoring and therapy adaptation.

Both supply-side enhancements (improved manufacture of NSAIDs and neuromodulation devices) and regulatory support (e.g., CDC guidelines on non-opioid pain treatments) in the world market for sciatica treatment will help to lay the groundwork for the advances of the future. Furthermore, the publications from the National Library of Medicine and the CDC report that various approaches – physical therapy, medication, and behavioral health, for instance– are emerging as first-line treatments, and are influencing the future of the sciatica treatment market analysis.

According to a recent study (2024), Naproxen is showing strong effectiveness in treating sciatica, potentially reducing dependency on more invasive methods.

To Get More Information On Sciatica Treatment Market - Request Free Sample Report

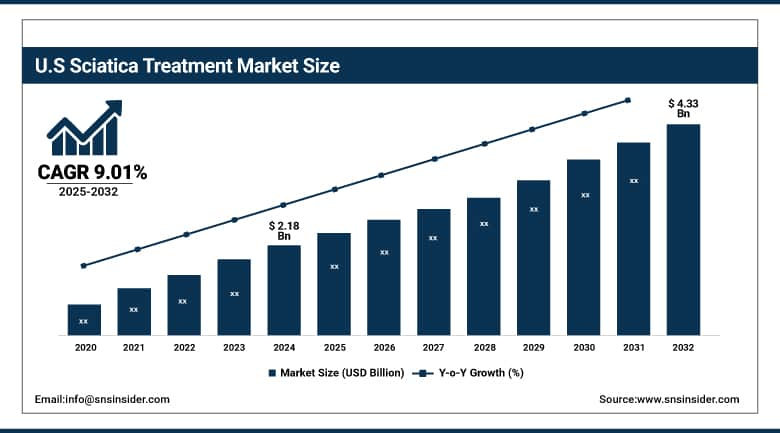

The U.S. Sciatica Treatment Market size was valued at USD 2.18 billion in 2024 and is expected to reach USD 4.33 billion by 2032, growing at a CAGR of 9.01% over 2025-2032.

Sciatica Treatment Market Dynamics:

Drivers:

-

Technological Advancements, Shifting Pain Management Paradigms, and Investment Surge Fuel the Market Expansion

The sciatica treatment market is fueled by increasing interest in non-surgical, customized treatment modalities and innovative approaches in neuromodulation technologies, pharmacotherapy, and regenerative medicine. Substantial improvements, such as targeted nerve ablation and minimally invasive decompression procedures, have resulted in better patient outcomes, which has expanded the user base. AAMG notes greater dependence on integrative strategies (e.g., TENS units, epidural steroid injections, cognitive-behavioral approaches), consistent with CDC-approved non-opioid treatments.

According to The National Center for Complementary and Integrative Health, adult use of yoga and chiropractic care increased by 40% from 2012 to 2022, and is expected to drive sciatica therapy demand.

From the supply side, local producers are increasing production capacities for sciatica-diagnosing devices, and diversified companies in the pharmaceutical industry are broadening their product portfolios through trials, with NSADs, corticosteroids, and muscle relaxants. Substantial R&D commitments, like the NIH’s annual USD 47 million grant pool to musculoskeletal pain research, further fuel this trend. Regulatory assistance, such as the FDA’s breakthrough device designation for next-generation spinal cord stimulation technology, is helping bring new therapies to market quicker. On the whole, this advent of innovation, patient preference alteration, and policy support is generating the fertile soil for the growth of the sciatica treatment market.

Restraints:

-

Fragmented Treatment Outcomes, High Procedure Costs, and Limited Insurance Coverage Hinder Market Expansion

Despite the achievements, a number of obstacles persist that are impeding the complete development of the global sciatica treatment market. Primary among them is the notion that the effect of treatment is partial—one treatment, such as surgical discectomy or epidural steroid injections, works better while another treatment does not work as well, especially regarding the severity (and chronicity) of symptoms, as indicated in several NASS Open Access publications.

In addition, some advanced treatments, such as spinal decompression, neuroablation, and biological treatments, such as platelet-rich plasma (PRP), are so expensive that very few patients can afford them. According to the Journal of Neurosurgery: Spine, it goes by the wayside with the average cost of a minimally invasive lumbar spine surgery exceeding USD 20,000 per level with sporadic insurance reimbursement, particularly in resource-constrained growth markets. In the U.S., private health insurers often don’t cover alternative treatments like acupuncture or inversion therapy, even though the data supporting them is expanding. Furthermore, there is no homogeneity of clear rules and guidelines among pain management practitioners, which makes standardized therapeutic procedures infrequent.

Sciatica Treatment Market Segmentation Analysis:

By Type

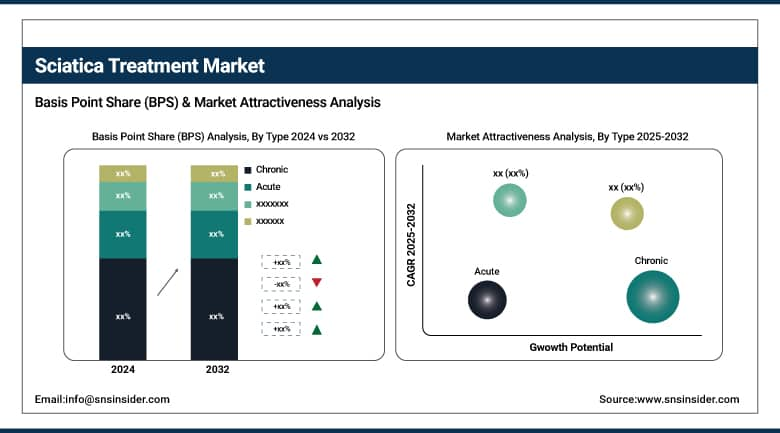

The chronic sciatica segment was the highest contributor to the global sciatica treatment market in 2024, accounting for 58% of the total market share. This is due to the high rate of recurrence and chronic nature of sciatica, which often results in long-term use of pharmacological and non-pharmacological treatments. The long-lasting condition usually requires regular support, including NSAIDs, exercise routines, and in some cases even surgery.

On the contrary, the acute segment is anticipated to be the fastest-growing over the forecast period, on account of high early diagnosis rates and an increasing inclination towards immediate, short-term duration treatment to avoid the onset of chronic sciatica. Growing utilization of the fast-acting drugs and the early stage of physiotherapeutic intervention are anticipated to propel demand for the segment.

By Drug Class

The NSAIDs market segment dominated the overall sciatica treatment market in 2024, contributing about 46% share of the total revenue. NSAIDs are commonly advised first-line treatment due to their efficacy in reducing inflammation and controlling pain without the risk of danger from opioid usage. The fact that they are available over the counter, as well as having a good safety profile, also makes them good candidates for widespread use.

Nevertheless, the corticosteroids category is projected to be the fastest growing, as they offer strong anti-inflammatory activity, especially in patients with severe or refractory disease. Growing adoption in the class due to growing utilization of epidural steroid injections and oral corticosteroids in clinical practice is driven by supportive clinical data.

By Distribution Channel

In 2024, the retail & online pharmacies segment held the largest share of the global sciatica treatment market, by distribution channel, accounting for 61% of the overall market. Rising preference for in-home care, increasing e-commerce penetration, and the convenience of over-the-counter purchases, particularly given the adoption of digital health, are driving this dominance. Furthermore, the rising level of awareness among consumers and inclination towards self-medication will drive the sales of the market through the retail and online channels.

The hospital pharmacy segment is anticipated to expand at a substantial CAGR due to the rising number of patients receiving in-hospital dispensing of prescription drugs (particularly controlled substances such as corticosteroids and opioids) as part of surgery and interventional procedures.

Sciatica Treatment Market Regional Insights:

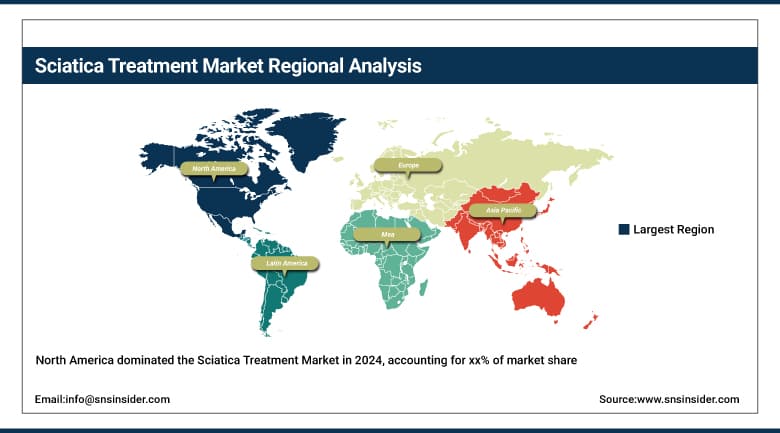

North America was the leading region in the global sciatic treatment market in 2024 and was the largest revenue-generating region, due to well-developed healthcare infrastructure, greater awareness of early diagnosis, and favourable reimbursement policies. This is also a shared problem for regional pain practitioners; in the U.S., sciatica and chronic back pain are quite common, and the studies have indicated that almost 40% of adults have suffered from sciatica at some time. Robust regulation support for non-opioid therapies, sizeable R&D funding (e.g., the NIH musculoskeletal pain research grants), and expedited FDA approvals for innovative devices such as spinal stimulators also contribute to growth. Canada is finding greater utilization of physiotherapy and integrative medicine, and in Mexico, the use of pharmacologic treatment and surgeries is slowly widening access. The existence market market-leading sciatica treatment companies and robust distribution networks also contributes to regional dominance.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe is a key market, and demand remains solid, buoyed by an aging population and increasing levels of inactivity. Countries such as Germany and the UK are significant contributors based on mature pain-management programs and the high prevalence of chronic lower back disorders. There is access to both pharmacological and non-pharmacological treatments within Germany, while in the UK, increasing provision of physiotherapy and multidisciplinary pain clinics within the public sector has occurred through NHS reforms. Public health care spending has increased in France and Italy. Emerging Eastern European countries like Poland and Turkey are focused on increased healthcare accessibility and higher adoption of non-opioid sciatica therapeutics.

The sciatica treatment market in Asia Pacific is expected to grow at the highest CAGR during the forecast period, owing to the rising healthcare spending, rising awareness about musculoskeletal disorders, and an increase in minimally invasive procedures. India is anticipated to have the maximum growth, driven by an increase in urbanization, expanding insurance penetration, and rising spending on telehealth and physiotherapy facilities. The growing geriatric population and prevalence of work-related back pain are the other contributors to demand.

Key Players in the Sciatica Treatment Market:

Leading sciatica treatment companies in the market are Pfizer, Abbott, Bayer, Endo International, Johnson & Johnson, GSK, Novartis, Bristol Myers Squibb, Amneal Pharmaceuticals, and Sorrento Therapeutics.

Recent Developments in the Sciatica Treatment Market:

-

In May 2025, Dr. DeCarlo introduced advanced spinal decompression therapy in New City, NY, offering a non-invasive solution for sciatica and disc-related pain, reflecting a growing trend in alternative treatment options.

-

In November 2024, Vertex Pharmaceuticals announced promising pivotal clinical trial results for its non-opioid treatment for chronic sciatica pain, marking a significant step toward FDA approval and potentially reshaping the chronic pain landscape.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.42 billion |

| Market Size by 2032 | USD 11.91 billion |

| CAGR | CAGR of 10.36% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Acute, Chronic) • By Drug Class (Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Corticosteroids, Antidepressants, and Others) • By Distribution Channel (Hospital Pharmacies, Retail & Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Pfizer, Abbott, Bayer, Endo International, Johnson & Johnson, GSK, Novartis, Bristol Myers Squibb, Amneal Pharmaceuticals, and Sorrento Therapeutics. |

Frequently Asked Questions

North America dominated the Sciatica Treatment market.

Fragmented treatment outcomes, high procedure costs, and limited insurance coverage hinder market expansion.

The sciatica treatment market is fueled by increasing interest in non-surgical, customized treatment modalities and innovative approaches in neuromodulation technologies, pharmacotherapy, and regenerative medicine.

The market is expected to reach USD 11.91 billion by 2032, increasing from USD 5.42 billion in 2024.

The Sciatica Treatment market is anticipated to grow at a CAGR of 10.36% from 2025 to 2032.

Get in Touch