Naval Vessels Market Report Scope & Overview:

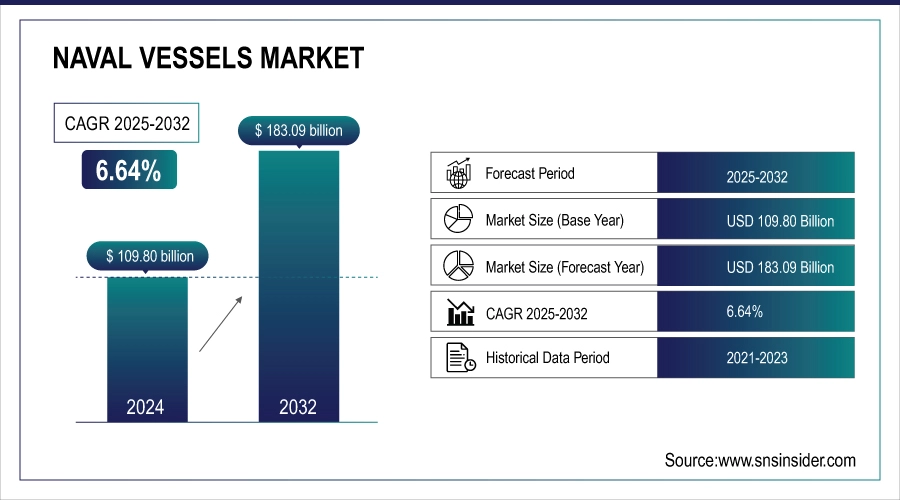

The Naval Vessels Market size was valued at USD 117.09 Billion in 2025 and is projected to reach USD 222.70 Billion by 2035, growing at a CAGR of 5.17% during 2026–2035.

The demand for naval vessels market is driven by global defense budgets, rising threats to maritime security, and the need to modernize the aging fleet with advanced technologies. Due to geopolitical tensions, many territorial disputes, and increase naval operations, demand for submarines, destroyers and frigates has been growing. Furthermore, nuclear propulsion, hybrid-electric systems and electronic warfare solutions are supporting naval capabilities, while the fast emergence of new economies is supported by heavy investment into indigenous shipbuilding programmes boosting maritime defence.

To Get more information On Naval Vessels Market - Request Free Sample Report

Key Naval Vessels Market Trends:

-

Rising defense spending and modernization of aging naval fleets with advanced submarines, aircraft carriers, and multi-role combat ships.

-

Increasing maritime security needs driven by territorial disputes and geopolitical tensions.

-

Technological advancements including nuclear propulsion, stealth features, and advanced weapons systems.

-

Transition toward hybrid and electric-powered vessels to support greener and more sustainable naval operations.

-

Growing demand for electronic warfare, cyber defense, AI-enabled command systems, and indigenous shipbuilding collaborations in emerging economies.

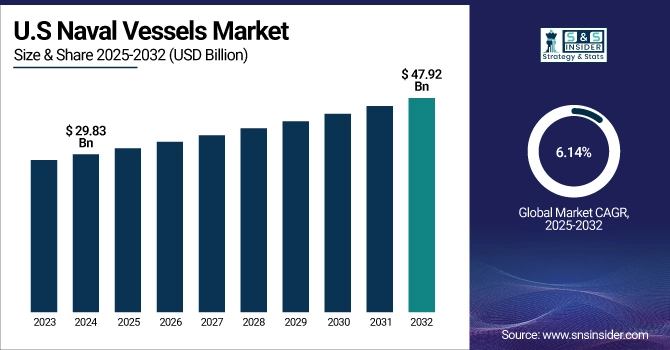

The U.S. Naval Vessels Market size was valued at USD 31.66 Billion in 2025 and is projected to reach USD 57.45 Billion by 2035, growing at a CAGR of 5.43% during 2026–2035. Fleet modernization programs, increased defense expenditure, advancements in nuclear propulsion, and rising demand for submarines, aircraft carriers, and multi-mission destroyers drive the U.S. naval vessels market.

Naval Vessels Market Driver:

-

Rising Defense Spending and Technological Innovations Drive Growth in Global Naval Vessels Market Amid Geopolitical Tensions

The Global Naval Vessels Market is driven by increasing expenditure on defense forces, rising geopolitical tensions and enhancement of ageing naval fleets. Countries are modernising with next generation submarines, aircraft carriers, sweetheart multi-role combat ships as a continued evolution of maritime ascendency and denial of access to its opponents. The increasing focus on maritime security and territorial disputes along with effective coastal defense systems are also driving the demand. Another factor boosting the market is technological innovations, such as nuclear propulsion as well as the development of stealth features and advanced weapons.

In 2024, Houthi militants conducted 90 maritime attacks in the Red Sea and disrupted shipping lanes, triggering a 56% drop in vessel transits in the area. This has spurred demand for naval assets to ensure maritime safety.

Naval Vessels Market Restraint:

-

Regulatory Barriers and Technology Integration Challenges Slow Growth and Deployment in Global Naval Vessels Market

Challenges such as a complex regulatory framework, long procurement cycles, and technology integration challenges across legacy vessels, act as restraints for the Naval Vessels Market. International collaborations are often delayed by geopolitical sensitivities, and expediting such partnerships is further complicated by export restrictions on advanced naval technologies. Production timelines are further delayed by shortages in skill-specific shipbuilding and skilled engineering labor. Many of these vessel options are subjected to layers of technical complexity imposed by environmental compliance and sustainability standards, significantly slowing the pace of vessel development and deployment.

Naval Vessels Market Opportunity:

-

Hybrid Electric Vessels and Advanced Technologies Transform Naval Market with Emerging Economies Driving Collaborative Growth

The development of hybrid and electric-powered vessels is a response to the transition of naval forces towards greener energy systems for better practicability and sustainability. And there is also growing demand for electronic warfare/electronic jamming, cyber defense, and artificial intelligence-enhanced command and control systems. Increasing indigenous shipbuilding programs in the emerging economies is opening doors for global shipbuilders and technology providers to collaborate, transfer capability, and expand their footprint.

The European Defence Agency (EDA), responding to rising tensions and defense needs, announced in late 2024 a collaborative program among 18 EU countries for the joint development of electronic warfare and air/missile defense systems.

Naval Vessels Market Segment Analysis

-

By Vessel Type, Submarines dominated the market with 31.97% in 2025, while frigates are expected to grow at the fastest CAGR of 7.93% from 2026 to 2035.

-

By System, Weapon systems dominated the market with 33.76% in 2025, while others (electronic warfare systems, command & control systems, and navigation systems) are expected to grow at the fastest CAGR of 7.39% from 2026 to 2035.

-

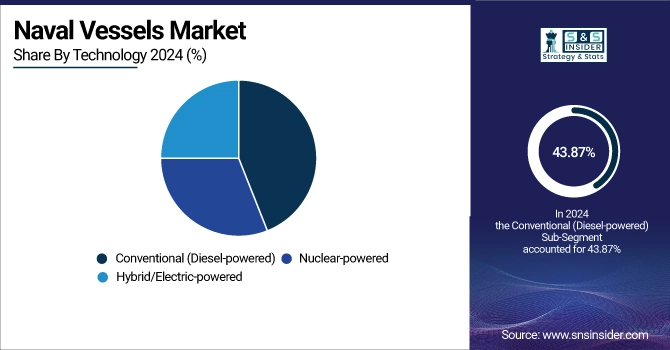

By Technology, Conventional (diesel-powered) vessels dominated the market with 43.87% in 2025, while hybrid/electric-powered vessels are expected to grow at the fastest CAGR of 7.31% from 2026 to 2035.

-

By Application, Combat operations dominated the market with 41.56% in 2025, while coastal defense is expected to grow at the fastest CAGR of 7.79% from 2026 to 2035.

By Vessel Type: Submarines Drive Naval Market Leadership as Frigates Emerge as Fastest Growing Multi Role Defense Segment Globally

The submarines segment has been projected to continue leading the global naval vessels market from 2024 as they play an essential part in underwater warfare, strategic deterrence, and intelligence-gathering. Nuclear and conventional submarines continue to be critical pillars of naval modernization programs among great powers, including but not limited to the U.S., China, Russia, and India. On the other hand, with a limited budget frigates will witness fastest growth with highest CAGR from 2026 to 2035, as it provides multi-role capabilities in terms of high value for money on surveillance, anti-submarine warfare and coastal defense attractiveness for a larger portion of the emerging naval forces worldwide.

By System: Weapon Systems Lead Naval Market as Electronic Warfare and AI Driven Technologies Propel Future Growth

Weapon systems topped the naval vessels market in 2024, with growing spending on advanced missile launchers, naval guns, and torpedo systems enhancing the combat capabilities of naval forces. Nations are tending towards highly armed vessels to enhance deterrence and readiness in areas that are conflict-prone. On the other hand, the “Others” segment, which includes electronic warfare, command and control, and navigation systems, is poised to record the fastest growth from 2026 to 2035, due to the rising need for electronic jamming, AI-based control, and enhanced situational awareness solutions.

By Technology: Conventional Vessels Dominate Naval Market as Hybrid Electric Ships Drive Future Growth and Sustainability

Conventional (diesel-powered) vessels dominated the naval vessels market in 2024, as they continue to be widely deployed for corvettes, frigates, and patrol vessels due to their cost-effectiveness, proven reliability, and simpler maintenance compared to nuclear-powered alternatives. They remain the backbone of many naval fleets, especially in developing countries. However, hybrid/electric-powered vessels are expected to grow at the fastest CAGR from 2026 to 2035, driven by the global shift toward greener propulsion technologies, reduced acoustic signatures, and enhanced operational sustainability.

By Application: Combat Operations Lead Naval Vessels Market While Coastal Defense Emerges as Fastest Growing Segment Globally

In 2024, combat requirements drove the naval vessels market, with submarines, destroyers, and aircraft carriers, all equipped with advanced weaponry, being in high demand. The major nations have been focusing on developing blue-water navies to secure maritime routes and counter their adversaries. However, coastal defense is expected to grow at the fastest CAGR from 2026 to 2035, supported by rising maritime security concerns, territorial disputes, and the need for cost-effective vessels to protect littoral waters.

Naval Vessels Market Regional Analysis:

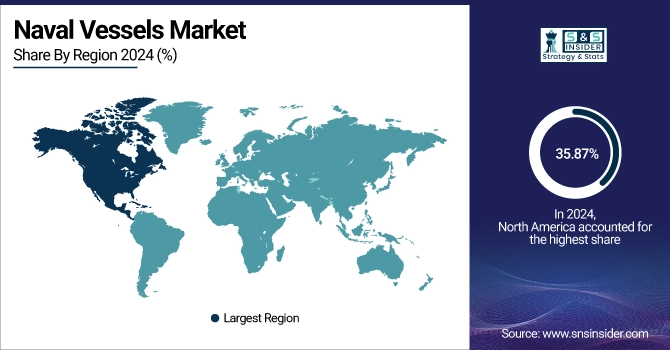

North America Dominates the Naval Vessels Market in 2025

In 2025, for naval vessels market, North America emerged as the largest during the forecast period with a revenue share of 35.87% because of the previous spending on defense, developed shipbuilding infrastructure and modernization programs. This has allowed for high levels of investment in nuclear-powered submarines, aircraft carriers and destroyers across the region, as well as electronic warfare and AI-based command systems. North America solidifies this leadership by prioritizing maritime security, fleet readiness, and power projection, along with high levels of R&D investment, and a strategic defense-industrial base.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Leads Naval Vessels Market in North America

In 2025, the North American naval vessels market was fully driven by the unparalleled defence budget of U.S. with a high level of fleet modernization programs and has nuclear-powered submarines and aircraft carriers.

Asia Pacific is the Fastest-Growing Region in Naval Vessels Market in 2025

Asia Pacific is expected to record the fastest CAGR in the naval vessels market from 2026 to 2035, driven by rising geopolitical tensions, territorial disputes, and increased focus on maritime security. Countries across the region are investing heavily in submarines, destroyers, and advanced coastal defense vessels to strengthen naval capabilities. Expanding indigenous shipbuilding programs, technological collaborations, and defense modernization initiatives are further fueling demand, making Asia Pacific a critical growth hub for the global naval market.

China Leads Naval Vessels Market Growth in Asia Pacific

China dominated the Asia Pacific naval vessels market in 2024, supported by its aggressive naval expansion, indigenous shipbuilding capacity, and large-scale investments in aircraft carriers, nuclear submarines, and advanced destroyers.

Europe Naval Vessels Market Insights

In 2025, the European naval market progressed because of large investments in the modernization of fleets, shipbuilding programs, and rising concerns about maritime security in the face of regional and international tensions. The emphasis was on developing advanced frigates, submarines, and auxiliary ships with characteristics such as stealth, artificial intelligence, and electronic warfare capabilities. Collaboration and cross-border shipbuilding programs led by NATO supported the European naval sector, with consistent demand for modern ships to secure strategic waters and allied interests.

Middle East & Africa and Latin America Market Insights

In the Middle East and Africa, increased military expenditure and the need to enhance maritime security are driving the demand for naval vessels in Saudi Arabia, the UAE, and South Africa. In Latin America, Brazil, Mexico, and Argentina are focusing on improving their naval capabilities, monitoring their coastlines, and enforcing anti-smuggling activities.

Naval Vessels Market Competitive Landscape:

Lockheed Martin

Lockheed Martin plays a pivotal role in the naval vessels market, delivering advanced combat systems, Aegis-equipped destroyers, radar solutions, and electronic warfare technologies. Its innovations enhance naval capabilities, supporting fleet modernization, missile defense, and multinational maritime security initiatives worldwide.

-

In July 2025, Lockheed Martin delivered SPY-7 radar components for Japan’s ASEV, Canada’s River-Class destroyers, Spain’s F-110 frigates, and the U.S. TPY-6 system, demonstrated successful mid-range missile interception.

BAE System

BAE Systems is a leading player in the naval vessels market, specializing in shipbuilding, modernization, and repair. It delivers advanced frigates, submarines, and combat systems, while integrating electronic warfare, propulsion, and sustainability technologies to strengthen global maritime defense capabilities.

-

In November 2024, BAE Systems Unveiled its new Littoral Strike Craft (LSC) concept at Euronaval 2024, showcasing innovative ship-to-shore deployment modes with unmanned surface vessel integration.

Naval Vessels Market Key Players:

Some of the Naval Vessels Market Companies

-

BAE Systems

-

Huntington Ingalls Industries

-

Lockheed Martin

-

Northrop Grumman

-

Naval Group

-

Saab AB

-

Thyssenkrupp Marine Systems (TKMS)

-

Fincantieri S.p.A.

-

Mitsubishi Heavy Industries

-

Daewoo Shipbuilding & Marine Engineering (DSME)

-

Hyundai Heavy Industries (HHI)

-

Hanwha Ocean (formerly DSME)

-

Larsen & Toubro (L&T)

-

Garden Reach Shipbuilders & Engineers (GRSE)

-

Mazagon Dock Shipbuilders Limited (MDL)

-

Navantia

-

Austal Limited

-

Damen Shipyards Group

| Report Attributes | Details |

| Market Size in 2025 | USD 117.09 Billion |

| Market Size by 2035 | USD 222.70 Billion |

| CAGR | CAGR of 6.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vessel Type (Submarines, Aircraft Carriers, Destroyers, Frigates, and Others (Corvettes, Amphibious Ships, Support & Auxiliary Vessels)) • By System (Weapon Systems, Communication Systems, Propulsion Systems, and Others (Electronic Warfare Systems, Command & Control Systems, Navigation Systems)) • By Technology (Conventional (Diesel-powered), Nuclear-powered, and Hybrid/Electric-powered) • By Application (Combat Operations, Surveillance & Reconnaissance, Logistics & Support, Coastal Defense, and Search & Rescue) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BAE Systems, General Dynamics, Huntington Ingalls Industries, Lockheed Martin, Northrop Grumman, Naval Group, Saab AB, thyssenkrupp Marine Systems (TKMS), Fincantieri S.p.A., Mitsubishi Heavy Industries, Kawasaki Heavy Industries, Daewoo Shipbuilding & Marine Engineering (DSME), Hyundai Heavy Industries (HHI), Hanwha Ocean, Larsen & Toubro (L&T), Garden Reach Shipbuilders & Engineers (GRSE), Mazagon Dock Shipbuilders Limited (MDL), Navantia, Austal Limited, Damen Shipyards Group. |

Frequently Asked Questions

North America dominated the Naval Vessels Market in 2025.

Submarines segment dominated the Naval Vessels Market.

The key drivers of the naval vessels market are rising defense spending, geopolitical tensions, fleet modernization, and advancements in shipbuilding technologies such as stealth, nuclear propulsion, and electronic warfare systems.

The Naval Vessels Market size was valued at USD 117.09 Billion in 2025 and is projected to reach USD 222.70 Billion by 2035, growing at a CAGR of 5.17% during 2026–2035.

The Naval Vessels Market is expected to grow at a CAGR of 6.64% from 2026-2035.

Get in Touch