Network Management System Market Report Scope & Overview:

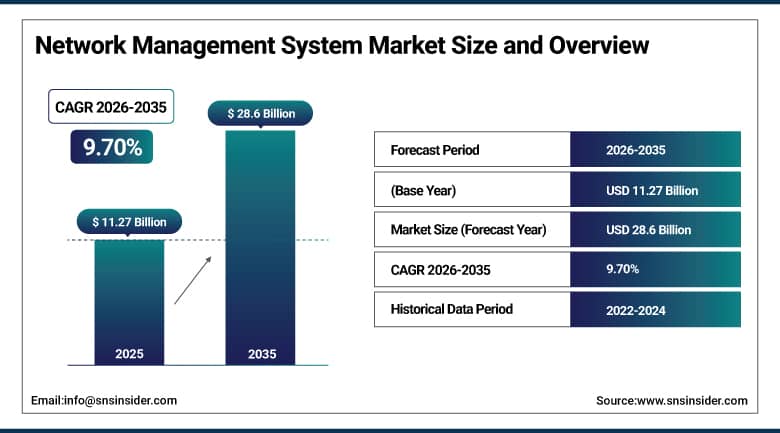

The Network Management System Market was valued at USD 11.27 Billion in 2025 and is expected to reach USD 28.6 Billion by 2035, growing at a CAGR of 9.70% from 2026–2035.

Network Management System refers to software-based platforms providing organizations with visibility, monitoring, configuration, and management of their IT network infrastructure. As organizations move from static networks to more complex network infrastructures, comprising data centers, cloud networks, edge computing infrastructures, mobile workforce networks, and IoT device networks, it becomes imperative for their NMS platform to be able to manage the complexities of such an ecosystem from a singular management perspective. With the rise of multi-cloud and hybrid networks, there is increasing pressure on organizations to migrate from legacy NMS solutions that cater to on-premises network infrastructures comprising of routers and switches to cloud-native NMS platforms that are capable of managing the performance and security of hybrid networks using artificial intelligence capabilities in near real time. There is a significant structural shift happening within the industry due to a few reasons. Firstly, the advent of 5G networking and its rollout in next-gen mobile devices would require organizations' NMS solutions to accommodate network slicing, virtualized radio access networks, and service orchestration due to the programmability of the 5G networks.

Over 70% of enterprise IT organizations in 2025 reported managing networks spanning at least two cloud providers alongside on-premise infrastructure. This multi-cloud complexity is the single most commercially significant driver of NMS platform investment as organizations require unified visibility and management across infrastructure environments whose native tools cannot communicate with each other.

Market Size and Forecast

- Market Size in 2026E: USD 12.37 Billion

- Market Size by 2035: USD 28.6 Billion

- CAGR: 9.70% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Network Management System Market - Request Free Sample Report

Network Management System Market Trends

- AI-powered network operations platforms are transforming traditional NMS tools by enabling automated anomaly detection, root cause analysis, and self-healing capabilities. This reduces manual monitoring efforts and improves network efficiency.

- Rapid 5G deployment is increasing demand for advanced NMS platforms capable of managing network slicing, Open RAN, and virtualized network architectures. Telecom operators require more flexible and programmable network management solutions.

- Adoption of software-defined networking (SDN) and network functions virtualization (NFV) is driving need for unified NMS platforms that manage both virtual and physical infrastructure. This enhances scalability and centralized network control.

- Growing implementation of zero-trust security models is boosting demand for NMS solutions that provide continuous monitoring, policy enforcement, and real-time traffic visibility. Organizations are prioritizing stronger network security and compliance management.

- SMEs are increasingly adopting cloud-based NMS subscriptions due to lower deployment costs and simplified management. Cloud-based platforms provide enterprise-grade network monitoring without requiring large in-house IT teams.

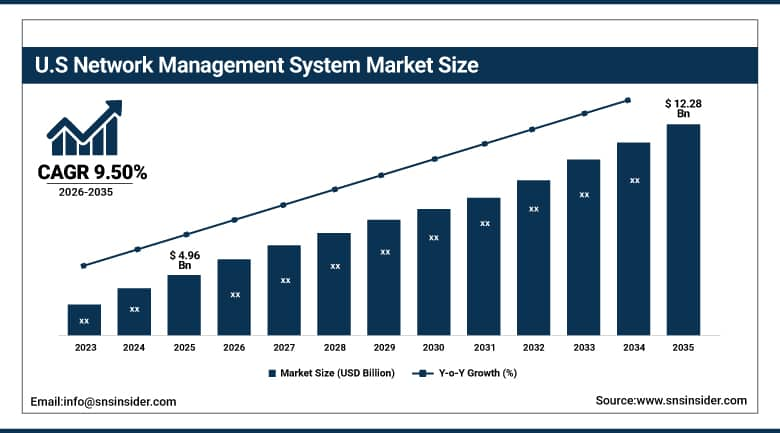

The U.S. Network Management System Market Outlook

The U.S. Network Management System Market was valued at approximately USD 4.96 Billion in 2025 and is expected to reach approximately USD 12.28 Billion by 2035, growing at a CAGR of 9.50%.

The largest market for national network management system solutions is America because of the sheer scale of the IT infrastructure for enterprises within the nation, the number of global technology companies that serve as clients to NMS providers, and the compliance regulations that exist within sectors such as health care, financial services, and governments which mandate the use of NMS platforms for documenting network monitoring and audits. Telecom firms like AT&T, Verizon, and T-Mobile are developing NMS platforms able to manage their next generation 5G network solutions spanning millions of devices across many million sites. Major cloud operators in America such as those operating at hyperscale levels have built proprietary NMS solutions based upon their internal needs for network management. Enterprise NMS solutions are being sought by organizations in all key industry segments within the nation. Health care entities operating HIPAA-compliant network environments must utilize NMS solutions to not only provide optimal operations, but also to comply with the required documentation and compliance mandates. Financial services firms using real-time trading infrastructures, payment processing systems, and other banking applications must deploy NMS platforms to monitor their network performance at the sub-second level of precision.

Cisco Systems reported that over 60% of its U.S. enterprise customers evaluated or deployed AI-enabled network management capabilities in 2025. This adoption rate reflects the commercial maturity of AI-powered NMS and the broad enterprise awareness of the operational benefits that automated anomaly detection and intelligent remediation deliver relative to manual monitoring approaches.

Network Management System Market Segment Analysis

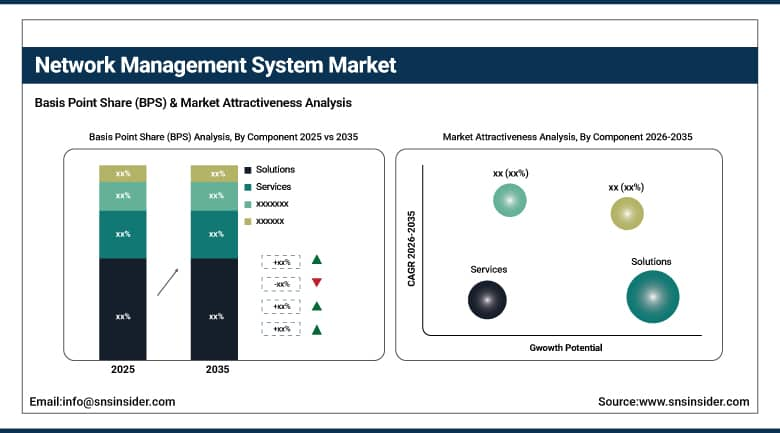

- By Component, Solutions held the largest share in 2025; Services are the fastest-growing component at a CAGR of 11.47% through growing demand for managed NMS services, integration support, and ongoing platform administration.

- By Deployment, On-Premises dominated with approximately 69% share in 2025; Cloud-Based is the fastest-growing deployment model at a CAGR of 10.95% through enterprise demand for scalable, remotely accessible, cost-effective NMS solutions.

- By Organization Size, Large Enterprises dominated the market with the largest share in 2025; SMEs are the fastest-growing segment at a CAGR of 15.65% through rising digitalization, cloud adoption, and demand for affordable cloud-based NMS solutions.

- By End User, IT & Telecom held approximately 22% share in 2025; Healthcare is the fastest-growing end user at a CAGR of 13.84% through digitalization, telemedicine adoption, and network security requirements for medical data privacy.

By Component, Solutions dominates, Services grows fastest

By Component, Solutions held the largest share in 2025, driven by strong enterprise adoption of integrated network management platforms, real-time monitoring tools, and advanced automation capabilities that enhance visibility, control, and operational efficiency across complex IT infrastructures. Solutions continue to dominate due to increasing demand for end-to-end Network Management Systems (NMS) that support multi-vendor environments and hybrid network architectures.

Meanwhile, Services is the fastest-growing component segment, expected to register a CAGR of 11.47% during the forecast period, fueled by rising reliance on managed NMS services, system integration support, consulting, and ongoing platform administration. Enterprises are increasingly outsourcing network management functions to specialized service providers to reduce operational complexity, ensure 24/7 network uptime, and access advanced expertise in cybersecurity, cloud networking, and performance optimization.

By Deployment, on-premises dominates, cloud grows fastest

Deployment in-premise comprised nearly 69% of the network management system market share in 2025. Such market positioning owes itself to the strong inclination of big corporations towards having complete autonomy over their network management systems, especially considering industries in which regulatory restrictions, concerns around network performance and latency, and specific security policies make deployment in the public cloud problematic. Health care institutions handling protected health information (PHI), financial firms with strong compliance demands, and government institutions with classified network segments utilize in-premise NMS systems capable of imposing access control policies that cannot be implemented by cloud-based solutions.

The fastest-growing deployment type is that of cloud delivery with a compound annual growth rate of 10.95%. Cloud NMS proves more convenient for organizations lacking network operation centers. While on-premise NMS takes weeks to deploy since it involves the process of downloading and configuring software, cloud NMS is up and running in just a few hours. It scales dynamically according to increases in devices and data volume. Updates are performed centrally and do not involve intervention from the IT department.

By End User, IT & telecom dominates, healthcare grows fastest

The market share of IT and telecoms in 2025 was estimated to be around 22%. This can be explained by the fact that this industry is both the main consumer and a significant contributor to the development of the NMS market. Telecom companies working with national networks covering millions of network points are among the most complex customers when it comes to network management services. Their requests for immediate performance tracking, prediction, and automatic fault correction have contributed to increased innovation efforts in NMS.

Healthcare is now the fastest-growing NMS end-user segment with a CAGR of 13.84% until 2035. The requirements for network management technologies imposed by the healthcare industry continue to rise in terms of speed and complexity. Modern hospitals require their networks to provide high-speed connectivity to various connected medical equipment, EHR and patient monitoring systems, and telemedicine portals. Healthcare industry cybersecurity threats such as ransomware attacks aimed specifically at hospital network systems make network security monitoring more important than ever.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.2% |

|

Europe |

Germany |

27.4% |

|

Asia Pacific |

China |

41.8% |

|

Middle East & Africa |

UAE |

28.3% |

|

Latin America |

Brazil |

42.6% |

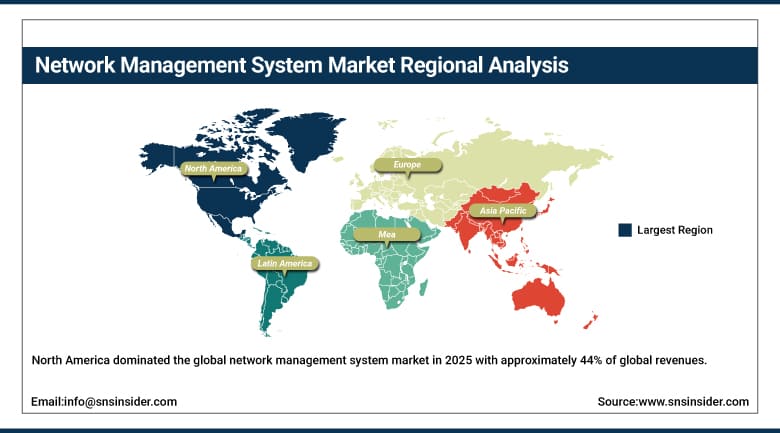

North America Network Management System Market Insights

North America dominated the global network management system market in 2025 with approximately 44% of global revenues. The United States accounts for approximately 79.2% of North American revenues as the world's most commercially developed enterprise IT market with the highest concentration of global technology vendors, the largest scale of enterprise network infrastructure, and the most complex regulatory compliance environment for network documentation and monitoring. U.S. telecommunications operators are among the most active 5G NMS platform adopters globally as they manage network slicing and Open RAN architecture deployment at national scale. Cisco, IBM, SolarWinds, and ManageEngine are among the most commercially significant NMS vendors operating primarily from U.S. bases. Canada is a growing NMS market driven by enterprise digital transformation, 5G network deployment by Bell, Rogers, and TELUS, and government digital services modernization investment. Canadian financial institutions under OSFI network security guidance and healthcare organizations under provincial privacy regulations are active NMS procurement drivers.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Network Management System Market Insights

Europe is a large and regulation-driven network management system market where GDPR network data processing requirements, NIS2 Directive mandatory network security monitoring obligations, and DORA financial sector resilience requirements are creating regulatory compliance-driven NMS demand. Germany accounts for approximately 27.4% of European revenues through its position as the EU's largest enterprise IT market and the center of Industry 4.0 network management investment in manufacturing and industrial automation. European NMS procurement is shaped by data sovereignty requirements that favor solutions with EU-based data processing and certified security compliance frameworks. The United Kingdom, France, the Netherlands, and Scandinavia each represent significant national NMS markets. UK financial institutions managing critical payment infrastructure, French telecommunications operators deploying 5G, and Dutch logistics and e-commerce operators managing complex warehouse network environments are among the most active European NMS investment drivers.

Asia Pacific Network Management System Market Insights

Asia Pacific is the fastest-growing network management system market at a CAGR of 11.41% through 2035. China accounts for approximately 41.8% of Asia Pacific revenues through its combination of the world's most extensive 5G deployment programme, rapid enterprise digital transformation across manufacturing, finance, and retail, and significant government smart city and digital infrastructure investment. India, Japan, South Korea, and Southeast Asia are all significant and growing NMS markets where telecommunications operator investment, enterprise IT modernization, and government digital services development are creating sustained platform procurement demand.

MEA & Latin America Network Management System Market Insights

The Middle East and Africa and Latin America are growing network management system market where telecommunications infrastructure investment, enterprise digital transformation, and smart city programme deployment are expanding the demand for network management platforms. The UAE leads MEA revenues at approximately 28.3% of the regional share through its advanced digital economy, active 5G deployment, and government smart city initiatives that create sophisticated NMS requirements across public and private sector operators. Brazil leads Latin American revenues at approximately 42.6% through its large enterprise technology market and telecommunications network expansion investments by Claro, TIM, and Vivo that create active NMS procurement demand.

Market Dynamics

Growth Drivers: Rapid 5G deployment, rising multi-cloud adoption, and increasing use of AI-powered automation for network monitoring and management are driving the network management system market growth.

5G network deployment is creating demand for NMS platforms with capabilities that no previous generation of network management technology required. Network slicing requires NMS platforms to manage multiple virtual network instances on shared physical infrastructure, each with distinct performance and security policy requirements. Open RAN architecture allows different vendors' radio, distributed unit, and centralized unit equipment to be combined in single deployments, requiring NMS platforms that can manage multi-vendor 5G components through standardized interfaces. The virtualized 5G core requires cloud-native NMS platforms that can orchestrate virtual network functions dynamically as traffic loads and service demands shift. AI and machine learning are fundamentally changing what network management systems can do. Traditional NMS platforms monitor and report network performance metrics, alerting operators when thresholds are exceeded. AI-powered NMS platforms analyses traffic patterns, device behaviour, and historical performance data to predict degradation before it affects user experience, identify the root cause of complex multi-layer faults faster than manual investigation, and autonomously implement corrective actions without operator intervention.

Restraints: Legacy infrastructure integration challenges, cloud data privacy concerns, and shortage of skilled network management professionals are restraining network management system market growth.

The problem of integration complexity is the most frequently mentioned issue when implementing an NMS. Companies invest in various hardware manufactured by different vendors for years. Connecting these devices to the common NMS software will involve complex integrations, which take significant time and money to achieve. Many businesses that operate their networks face the problem of higher costs associated with deploying their NMS solutions due to the complexity of the implementation process compared to what was initially anticipated by businesses during budgeting. Data privacy concerns limit cloud NMS adoption in regulated industries. Network management data includes traffic flows, device access logs, security event records, and user activity metadata whose processing in cloud environments creates regulatory compliance complexity under GDPR, HIPAA, and sector-specific financial data protection requirements.

Opportunities: AI-driven network automation, expansion of managed NMS services for SMEs, and growth of intent-based networking platforms are creating strong opportunities in the network management system market.

Management of intent-based networking is the next level of NMS capabilities. Instead of defining the required configuration of networks, intent-based networks enable administrators to define their intentions in a more abstract way, such as the requirement to route all traffic coming from the finance department through a compliant pathway, encrypt it, and then distribute it accordingly, and the NMS system would translate those intentions into the required configuration settings of all devices. Intent-based networks would significantly reduce configuration complexities and the risks associated with errors in the process – which are among the key causes of network failures. Cisco DNA Centre and Juniper Apstra are the two commercial leaders in providing NMS solutions for intent-based networks, and it is reasonable to assume that the number of such solutions will only grow in the future. Managed NMS services in SMEs are another significant area of development in the field. As smaller businesses often cannot afford to build their own network operations centers, they have become one of the most important yet commercially underserved markets for NMS services.

Recent Developments:

- 2025: Cisco Systems launched Cisco AI Defense, an AI-powered network security and management platform integrating threat detection, policy enforcement, and anomaly analysis across multi-cloud and hybrid enterprise network environments through its existing management infrastructure.

- 2025: IBM Instana expanded its network observability capabilities with new AI-powered root cause analysis features that reduce mean time to resolution for complex multi-layer network faults by automatically correlating events across infrastructure tiers.

- 2025: SolarWinds completed its go-private restructuring and launched a major NMS product update focused on hybrid and multi-cloud network observability, addressing enterprise demand for unified management across on-premise and public cloud infrastructure.

Network Management System Market Key Players are:

- Cisco Systems Inc.

- IBM Corporation

- SolarWinds Inc.

- Juniper Networks Inc.

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Ericsson AB

- Broadcom Inc. (CA Technologies)

- ManageEngine (Zoho Corporation)

- NetScout Systems Inc.

- Paessler AG (PRTG Network Monitor)

- Nagios Enterprises LLC

- Zabbix LLC

- ScienceLogic Inc.

- BMC Software Inc.

- Micro Focus International plc

- Datadog Inc.

- Dynatrace Inc.

- New Relic Inc.

- LiveAction Inc.

Network Management System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.27 Billion |

| Market Size by 2035 | USD 28.6 Billion |

| CAGR | CAGR of 9.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (On-Premises, Cloud-Based) • By Organization Size (Large Enterprises, Small & Medium Enterprises) • By End User (IT & Telecom, BFSI, Healthcare, Retail, Government & Public Sector, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cisco Systems Inc., IBM Corporation, SolarWinds Inc., Juniper Networks Inc., Huawei Technologies Co. Ltd., Nokia Corporation, Ericsson AB, Broadcom Inc. (CA Technologies), ManageEngine (Zoho Corporation), NetScout Systems Inc., Paessler AG (PRTG Network Monitor), Nagios Enterprises LLC, Zabbix LLC, ScienceLogic Inc., BMC Software Inc., Micro Focus International plc, Datadog Inc., Dynatrace Inc., New Relic Inc., LiveAction Inc. |

Frequently Asked Questions

North America dominated the Network Management System Market in 2025 with approximately 44% of global revenues.

On-Premises deployment dominated with approximately 69% of revenues in 2025.

5G network deployment complexity and multi-cloud enterprise adoption creating network visibility gaps are the primary drivers.

The Network Management System Market was valued at USD 11.27 Billion in 2025.

The Network Management System Market is expected to grow at a CAGR of 9.70% from 2026 to 2035.

Get in Touch