Dynamic Random Access Memory Market Report Scope & Overview:

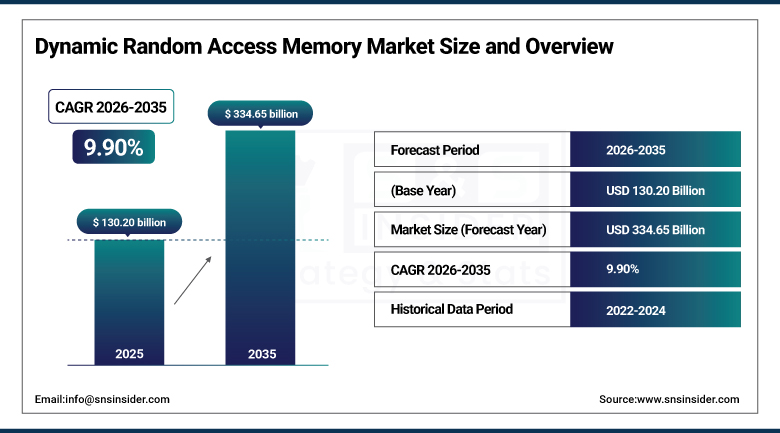

The Dynamic Random Access Memory Market size was valued at USD 130.20 Billion in 2025 and is expected to reach USD 334.65 Billion by 2035, growing at a CAGR of 9.90% from 2026 to 2035.

The Dynamic Random Access Memory (DRAM) market is growing due to the increased usage of data centers, cloud computing systems, and high performance computing which requires higher memory bandwidth. With an increase in demand for artificial intelligence, machine learning, and big data analytics, the consumption of DRAM is expected to rise. Apart from that, the increased adoption of smartphones, personal computers, and other consumer electronics is driving the growth of sophisticated memory technologies such as DDR5 and HBM. Innovation in semiconductors along with investment in advanced memory technology by leading manufacturers is aiding the growth of the market.

According to SK hynix, demand for High Bandwidth Memory (HBM) is expected to grow 2–3 times faster than conventional DRAM, driven by the rapid expansion of AI GPUs and AI computing infrastructure. Additionally, Micron Technology states that AI servers can consume approximately 8–12 times more DRAM per system than traditional cloud servers due to the intensive memory requirements of AI model training and inference workloads, further accelerating demand for advanced DRAM solutions.

DRAM Market Size and Forecast

-

Market Size in 2026E: USD 143.08 Billion

-

Market Size by 2035: USD 334.65 Billion

-

CAGR: 9.90% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Dynamic Random Access Memory Market - Request Free Sample Report

Dynamic Random Access Memory Market Trends

-

Rising demand for high-performance computing, AI workloads, and data center expansion driving strong consumption of DRAM chips

-

Growing penetration of smartphones, gaming devices, and consumer electronics increasing need for higher memory capacity and faster processing speeds

-

Increasing adoption of cloud computing and hyperscale data centers boosting large-scale deployment of advanced DRAM solutions

-

Expanding use of DDR5 and next-generation memory technologies improving bandwidth, energy efficiency, and overall system performance

-

Continuous advancements in semiconductor manufacturing processes enabling higher density, lower power consumption, and improved reliability of DRAM products

U.S. Dynamic Random Access Memory Market Size Outlook

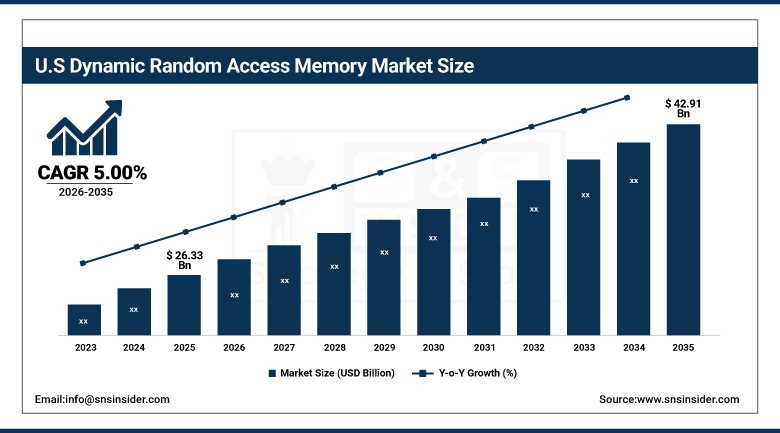

The U.S. Dynamic Random Access Memory (DRAM) Market was valued at approximately USD 26.33 Billion in 2025 and is expected to reach approximately USD 42.91 Billion by 2035, growing at a CAGR of approximately 5.00%.

The United States is the world's largest DRAM consuming market within the Americas region, driven by the domestic concentration of the world's largest hyperscale data centre operators including Amazon, Microsoft, Google, and Meta whose GPU-dense AI infrastructure requires massive DRAM content per server node, the U.S. headquarters of Apple, Dell, HP, and Qualcomm whose computing platform procurement creates large-volume DRAM demand, and the growing domestic semiconductor industry investment enabled by the CHIPS Act whose wafer fabrication and back-end assembly expansion includes DRAM-adjacent advanced packaging capability.

Micron Technology, the only U.S.-headquartered DRAM manufacturer, is expanding domestic DRAM production capacity at its Boise, Idaho headquarters campus and planning a new fab in Clay, New York enabled by CHIPS Act direct funding commitments, progressively increasing U.S.-origin DRAM supply capability that serves both national security supply chain objectives and commercial procurement.

Dynamic Random Access Memory Market Segment Analysis

-

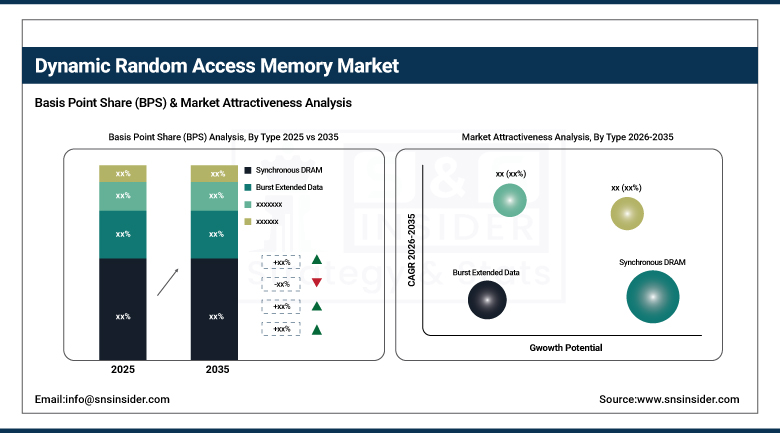

By Type, Synchronous DRAM segment dominated the Dynamic Random Access Memory (DRAM) Market in 2025 with 48% share; DDR5/GDDR5 segment is the fastest growing segment.

-

By Technology, DDR4 segment dominated the market in 2025 with 52% share; DDR5 segment is the fastest growing segment.

-

By End-Use, Consumer Electronics segment dominated the market in 2025 with 46% share; IT and Telecommunication segment is the fastest growing segment.

By Type, Synchronous DRAM segment dominates the DRAM Market, DDR5/GDDR5 segment expected to grow fastest

The Synchronous DRAM segment dominated the Dynamic Random Access Memory (DRAM) Market in 2025 owing to its widespread application in computing systems, consumer electronics, and enterprise applications. The technology is synchronized to the system clock, which ensures fast data transfer rates, better bandwidth, and processing performance. Its high degree of compatibility with PCs, laptops, and servers, along with a well-developed manufacturing infrastructure and cost-effectiveness, has contributed to its widespread acceptance. Constant demand for fast and dependable memory solutions has ensured its lead in the market.

The DDR5/GDDR5 segment is the fastest growing in the DRAM market owing to the increasing demand for higher bandwidths, higher energy efficiency, and improved performance in advanced applications. The segment finds increasing use in gaming systems, AI applications, data centers, and high performance computing applications. Technological advancements in memory technology and the trend towards next generation computing have contributed to its growth. Increasing demand for fast data processing and multitasking is further driving the growth of this segment.

By Technology, DDR4 segment dominates the DRAM Market, DDR5 segment expected to grow fastest

The DDR4 segment dominated the DRAM market in 2025 due to its extensive adoption in consumer electronics, computers, laptops, and server machines. It provides a good combination of performance, power efficiency, and economy and therefore it is very suitable for large-scale applications. Due to the fact that it has already established itself as a good memory solution with wide compatibility and large-scale production capabilities, its adoption will continue despite the emergence of new technologies. In mid-range computing devices and enterprises, DDR4 is very reliable and economic.

The DDR5 segment is the fastest growing in the DRAM market because of increasing demand for greater memory bandwidth, higher energy efficiency, and performance improvements. The DDR5 segment is being adopted quickly in advanced computing applications including AI processing, data centers, and future gaming systems. DDR5 has shown a higher adoption rate because of its ability to handle sophisticated workloads and fast processing capabilities, as companies shift towards high-performance computing and digital transformation.

By End-Use, Consumer Electronics segment dominates the DRAM Market, IT & Telecommunication segment expected to grow fastest

The Consumer Electronics segment dominated the DRAM market in 2025 because of its use in smartphones, laptops, tablets, gaming consoles, and other smart devices. Growth in digitalization, high requirements for speed and multitasking capabilities, and growing complexity of the devices have driven the increase in the DRAM consumption. Product innovations and growing numbers of connected devices also contribute to such leadership. Growing popularity of the smart technologies and high demands of everyday electronics ensure the continuing dominance of this segment in the DRAM market.

The IT and Telecommunication segment is the fastest growing in the DRAM market because of fast growth of data centers, cloud computing infrastructures, and 5G network infrastructure. High demand for powerful servers and applications and high demands for memory resources is contributing to such fast growth. Digital transformations and rising of internet traffic further drive the adoption. Growth of demands for memory solutions in communication networks drives such growth.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

South Korea |

32.84% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Dynamic Random Access Memory Market Insights

North America accounted for approximately 24.00% of global DRAM revenues in 2025, driven primarily by the domestic concentration of the world's largest data centre operators whose AI infrastructure investment creates the highest per-facility DRAM procurement value of any regional data centre market, and by the U.S. headquarters of Apple, Dell, HP, and Qualcomm whose computing platform DRAM procurement creates large-volume demand.

The CHIPS Act's support for Micron Technology's domestic DRAM production expansion is creating an incremental U.S.-based supply capability whose strategic importance to federal supply chain security is reflected in the USD 6.1 billion CHIPS Act direct funding commitment announced for Micron's Idaho and New York facilities.

Europe Dynamic Random Access Memory Market Insights

Europe held approximately 14.84% of global DRAM revenues in 2025. Germany accounts for approximately 28.47% of European revenues through its concentration of industrial computing, automotive electronics, and enterprise server procurement at major German corporations and public institutions. The EU Chips Act's investment in European semiconductor production and advanced packaging capability is creating long-term supply chain development whose second-tier effects include growing European DRAM system integration and design capability.

The United Kingdom, France, Netherlands, and Sweden contribute meaningful European demand through their enterprise computing, telecommunications, and automotive electronics sectors.

Asia Pacific Dynamic Random Access Memory Market Insights

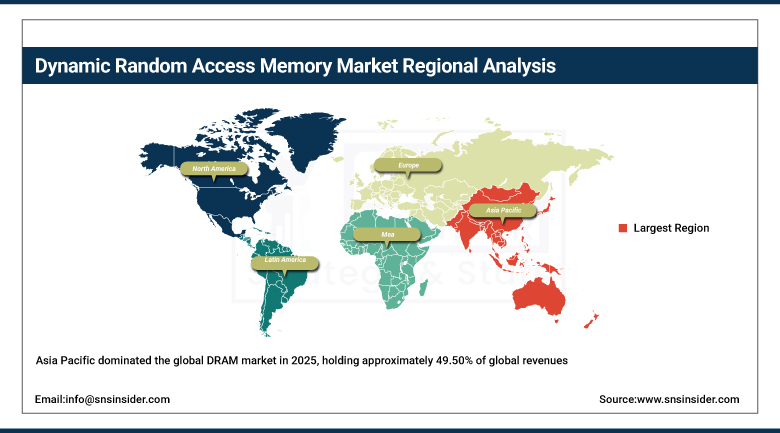

Asia Pacific dominated the global DRAM market in 2025, holding approximately 49.50% of global revenues, anchored by the geographic concentration of the three companies that collectively produce over 90 percent of the world's DRAM: Samsung Electronics in South Korea, SK Hynix in South Korea, and Micron's assembly operations in Japan and Taiwan.

South Korea accounts for approximately 32.84% of Asia Pacific revenues through Samsung Electronics' and SK Hynix's combined DRAM production and domestic Korean electronics industry consumption. China, Japan, Taiwan, and India each contribute meaningful Asia Pacific demand through their electronics manufacturing, consumer devices production, and growing data centre infrastructure investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Dynamic Random Access Memory Market Insights

Middle East and Latin America are growing DRAM markets where data centre investment, consumer electronics adoption, and automotive electronics expansion are creating increasing memory component demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its concentration of cloud service provider regional data centre investment, growing consumer electronics market, and increasing 5G infrastructure deployment.

Saudi Arabia's NEOM and Vision 2030 digital infrastructure programmes contribute secondary MEA DRAM demand. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large consumer electronics market, growing domestic IT infrastructure investment, and automotive electronics sector serving both domestic vehicle production and export markets.

Market Dynamics

Growth Drivers: AI training requires high DRAM density while mobile AI increases LPDDR content per device

The AI infrastructure investment cycle that has created unprecedented GPU cluster deployment at hyperscalers globally is simultaneously creating DRAM demand at the highest per-server content levels in computing history. An AI training server equipped with eight NVIDIA H100 GPUs contains 640 gigabytes of HBM3 memory soldered onto the GPUs, plus 1,000 to 2,000 gigabytes of DDR5 DIMM memory in the host server, creating a per-node DRAM content that is 10 to 20 times the memory content of a standard enterprise server.

The aggregate effect across hundreds of thousands of AI training servers deployed in hyperscaler facilities is a DRAM demand increment from this single application category that represents a material fraction of total global DRAM production capacity, creating sustained upward pressure on DRAM pricing and supply allocation that benefits all three major DRAM producers simultaneously.

Restraints: DRAM cyclicality creates price volatility and oversupply risk due to capital intensive manufacturing

The DRAM market's historical cyclicality, in which commodity pricing collapses of 30 to 40 percent occur during supply surplus periods when capacity additions outpace demand growth, creates revenue and margin volatility that complicates long-term capital planning for both producers and buyers. The period from late 2022 through mid-2023 saw DRAM spot prices decline 60 to 70 percent from cycle peaks as COVID-era demand acceleration reversed and inventory corrections at PC and smartphone OEMs reduced procurement volumes, creating producer revenue declines of 20 to 40 percent and material operating losses at Micron and SK Hynix despite their production capacity and technology leadership positions.

The AI demand surge has moderated this cyclicality somewhat by adding a demand floor from data centre procurement that is less sensitive to consumer electronics cycles, but consumer segment cyclicality remains a structural feature of DRAM market dynamics that creates forecast uncertainty across the cycle.

Opportunities: HBM expansion and compute in memory DRAM enable high value AI edge premium pricing

High bandwidth memory product expansion beyond GPU integration into AI inference accelerators, network processors, and AI-capable mobile devices represents a growing premium DRAM market segment whose per-gigabyte revenue substantially exceeds standard DIMM or LPDDR products. As AI inference scales from centralised data centre deployment toward edge computing and device-level operation, the bandwidth requirements of on-device AI workloads will progressively push mobile and edge platform memory specifications toward LPDDR5X and beyond in the consumer segment, and toward custom memory architectures combining HBM-style bandwidth with mobile-appropriate packaging formats in the premium edge AI segment.

Compute-in-memory architectures that process neural network matrix operations within the DRAM array itself eliminate memory bandwidth as the primary AI inference bottleneck, creating potential for qualitative performance improvements in AI-capable devices that motivates significant industry R&D investment.

Recent Developments:

-

2025: Samsung Electronics commenced mass production of 12-nanometre class LPDDR5X mobile DRAM at Pyeongtaek P4 achieving 7,500 megabits per second at 1.01 volts, delivering 25 percent bandwidth and 25 percent power efficiency improvements over prior-generation LPDDR5 for AI-capable flagship smartphone platforms.

-

2025: Micron Technology secured a major HBM3E supply contract with a leading AI server manufacturer, validating Micron's competitive HBM position against Korean suppliers and establishing U.S.-site HBM commercial production for the first time, aligning with CHIPS Act domestic advanced semiconductor production objectives.

-

2024: SK Hynix commenced HBM3E production at its M15X Cheongju fab with a 36-gigabyte per second per pin bandwidth achieving 36 percent improvement over HBM3, qualifying with NVIDIA for incorporation into Blackwell B200 AI accelerator GPU packages whose AI training performance depends directly on HBM memory bandwidth per die stack.

Key DRAM Companies are:

-

Samsung Electronics

-

Micron Technology Inc

-

Nanya Technology Corporation

-

Winbond Electronics Corporation

-

Powerchip Semiconductor Manufacturing Corp (PSMC)

-

ChangXin Memory Technologies (CXMT)

-

Elite Semiconductor Memory Technology Inc. (ESMT)

-

Macronix International Co. Ltd.

-

Vanguard International Semiconductor Corporation

-

Kioxia Holdings Corporation

-

Renesas Electronics Corporation

-

Texas Instruments Incorporated

-

Intel Corporation

-

IBM Corporation

-

Fujitsu Limited

-

Toshiba Corporation

-

ADATA Technology Co. Ltd.

-

Apacer Technology Inc.

Dynamic Random Access Memory Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 130.20 Billion |

| Market Size by 2035 | USD 334.65 Billion |

| CAGR | CAGR of 9.90% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Synchronous DRAM, Burst Extended Data, Output Extended Data, Output Asynchronous DRAM, Fast Page Mode) • By Technology (DDR4, DDR3, DDR5/GDDR5, DDR2) • By End-Use (IT and Telecommunication, Defense and Aerospace, Media and Entertainment, Medical and Healthcare, Consumer Electronics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Samsung Electronics, SK Hynix Inc., Micron Technology Inc., Nanya Technology Corporation, Winbond Electronics Corporation, Powerchip Semiconductor Manufacturing Corp (PSMC), ChangXin Memory Technologies (CXMT), Integrated Silicon Solution Inc. (ISSI), Elite Semiconductor Memory Technology Inc. (ESMT), Macronix International Co. Ltd., Vanguard International Semiconductor Corporation, Kioxia Holdings Corporation, Renesas Electronics Corporation, Texas Instruments Incorporated, Intel Corporation, IBM Corporation, Fujitsu Limited, Toshiba Corporation, ADATA Technology Co. Ltd., Apacer Technology Inc. |

Frequently Asked Questions

The DDR4 segment dominated the Dynamic Random Access Memory Market.

AI infrastructure, HBM demand, mobile AI, DDR5 adoption, and expanding 5G and IoT devices drive DRAM market growth.

Asia Pacific dominated the Dynamic Random Access Memory Market in 2025.

The Dynamic Random Access Memory Market is expected to grow at a CAGR of 9.90% from 2026 to 2035.

The Dynamic Random Access Memory Market was valued at USD 130.20 Billion in 2025.

Get in Touch