Neuromorphic Computing Market Report Scope & Overview:

Get More Information on Neuromorphic Computing Market - Request Sample Report

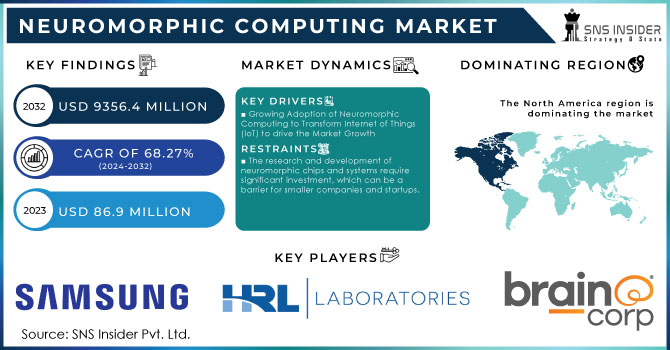

Neuromorphic Computing market size was valued at USD 86.9 Million in 2023. It is expected to Reach USD 9356.4 Million by 2032 and grow at a CAGR of 68.27% over the forecast period of 2024-2032.

The growth of the market is attributed to an increase in applications for neuromorphic technology such as deep learning, transistors and accelerators, next-generation semiconductors; autonomous systems including robotics drones, self-driving cars and artificial intelligence. For instance, in August 2023 a diverse consortium of researchers completed NeuRRAM - an all-new neuromorphic chip capable to simultaneously run various AI applications with greater precision and reduced energy consumption than equivalent possibilities. The integration of neuromorphic technology, along with AI and machine learning, has the potential to bolster the processing capabilities of defence systems and deliver rapid analytical insights to facilitate timely wartime decision-making. The technology is more energy saving, which can lead to better transportability (mobility, endurance and operation time) and portable for a soldier on field. Intel Corporation plans to install a Loihi chip to enable faster sensing by processing signals of biological nature from the camera, like neuromorphic technology in drone cameras. This means that complex algorithms running on robots can work efficiently using neuromorphic computing and so improve robotic systems efficiency both in terms of performance as well energy consumption. In September 2022, Intel Corporation, the Italian Institute of Technology, and the Technical University of Munich collaborated to unveil a novel approach to object learning utilizing neural networks. This joint effort aims to streamline and speed up robots acquiring knowledge about new objects upon deployment in various work environments.

Increasing use of machine learning, AI and higher I.P. is helps to drive the growth of Neuromorphic Computing Market. Enormous improvements are seen in neuromorphic computing technology. IBM's AI chip, launched in January 2023, uses 7nm technology for enhanced energy efficiency. This popular Swiss start-up's processors can cater for anywhere up to 1,000 frames per second - making SynSense a real-time solution. In October 2023, SiLC Technologies’ Launched Eyeonic Vision System delivers distance precision beyond 1,000 meters at the millimeter level. The chips from Eindhoven University that can detect cystic fibrosis with more than 90% accuracy. Working together with Lorser Industries, Brain Chip has achieved up to a >50% improvement in processing speed and energy efficiency on software defined radios — demonstrating the incredible transformative capabilities of neuromorphic computing across industries.

Drivers

-

Growing Adoption of Neuromorphic Computing to Transform Internet of Things (IoT) to drive the Market Growth

-

The ability of neuromorphic systems to process large amounts of data quickly and efficiently supports real-time applications in autonomous vehicles, robotics, and AI-driven systems.

-

The integration of neuromorphic computing with artificial intelligence and machine learning enhances the performance and capabilities of AI applications, driving demand across various sectors.

-

Neuromorphic computing's low-power and on-device processing capabilities make it well-suited for edge computing applications, reducing latency and improving performance in devices like smart sensors and autonomous systems.

-

Neuromorphic technology's potential in medical diagnostics and healthcare, such as biosensors for disease detection, propels market growth through improved diagnostic accuracy and speed.

The neuromorphic computing is having capability to pull data from many IoT devices, this technology is great for use in home automation applications as well as self-driving cars and health diagnostics. Neuromorphic computing allows AI algorithms to operate on effective network architectures and speedy data processing. Self-driving cars are one case that learns from other traffic to make faster decisions, and automated homes that adjust temperature and lighting based on the habits of people living in them. Furthermore, neuromorphic computing also reinforces IoT security by acting as an AI that help to identify any phishing or malicious activity. At CES 2024, Innatera introduced the Spiking Neural Processor T1 originating in neuromorphic microcontroller conceived for battery-operated AI running on a sensor-edge like smart homes accessories or wearables aiming energy efficiency IoT applications. For real-time processing algorithms with low power constraints, neuromorphic computing largely benefits AI and ML applications which they tend to be complementary such as autonomous systems, computer vision or natural language processing. Ideal use for this is IoT devices, robotics & autonomous vehicles. Areas are working towards full automation initiatives to drive efficiencies and improve quality. The ability of a neuromorphic chip can be employed in areas such as the military and cybersecurity for detecting anomalies, Image/object recognition e.g., by analyzing network traffic patterns. In September 2023, BrainChip Holdings Ltd worked with VVDN Technologies to help provide an Edge box that was powered by their very own Akida neuromorphic processors for it extend Edge AI capabilities.

Restraints

-

The research and development of neuromorphic chips and systems require significant investment, which can be a barrier for smaller companies and startups.

-

Designing neuromorphic systems that mimic the human brain's architecture and functionality is complex and challenging, slowing down widespread adoption.

-

The absence of industry standards for neuromorphic computing technologies can hinder interoperability and integration with existing systems and platforms.

The growing costs to design advanced chips and systems is the major restrain for growth of market. A new neuromorphic computer platform is a multimillion-dollar research and development (R&D) proposition globally. An entirely new neuromorphic chip, if developed from scratch by companies building it could cost just more than $50 million in advanced fabrication facilities and other operational expenses including material costs with specialized talent that a design would require. Much of the added cost comes from their complex nature, which often leads to new classes of materials and novel architectures. Moreover, the complex design and testing stages brings with it high costs and a time-suck. The high-cost barrier may discourage smaller companies and startups from entering the market, inhibiting competition/innovation in this area. Consequently, the rate of progress and adoption for neuromorphic computing could be slower than other more cost-effective technologies.

Segment Analysis

By Application

The image processing segment accounted for the largest market share of over 43% in 2023. This is because the computer vision has expanded across industries like automotive, healthcare and media & entertainment. A similar endpoint is the medical imaging which a significant facet of this sector. During the forecast period, image sensors and processing technologies are projected to support growth of revenue generation via Image Processing. Image processing is primarily about reducing visual information for the purpose of making it suitable for computer vision tasks, such as image recognition in this case to make subsequent steps much easier and more efficient. by being closer in operation to how the human brain works, it can give computers a much-needed boost in terms of understanding data and then converting that into an analysis. Artificial neural network models are also rising in popularity which aims at image processing and fast computation through the use of parallel architectures.

The signal-processing application segment held a market share of 26.5% in the year 2023 and is poised to register solid growth it generates revenue more efficiently during the forecast period Increasing need to process audio and acoustic signals is driving the signal-processing segment. The market is expected to grow during the forecast period with increasing adoption of Artificial Intelligence and Machine Learning across IT industry which in turn will favor the data processing segment. One of the top AI trends for organizations is autoML (automatic machine learning).

By End-Use

Consumer electronics was the leading segment in 2023, accounted for more than 56.5% share of revenue This is increasing the demand for neuromorphic chips in consumer electronics, where various electronic devices including laptops/PCs/tablets have gained popularity. Miniaturization of ICS stems from the demand for smaller and cheaper products according to consumer preferences, which subsequently drives growth in the global neuromorphic chip market.

Over the forecast frame, generating revenue from the automotive industry is projected to increase with significant growth rate. Many industries are using AI (Artificial Intelligence) and ML (Machine Learning) to automate the operations which help them in offering more efficient & quality products. Moreover, the growing adoption of AI and ML as a result faster speed, low power consumption, and efficient memory usage by these technologies is accelerating growth in automotive segment. This trend clearly shows how neuromorphic chips play a significant part in upgrading the function as well as capacity of automotive applications such as autonomous driving, and advanced driver-assistance systems (ADAS).

By Deployment

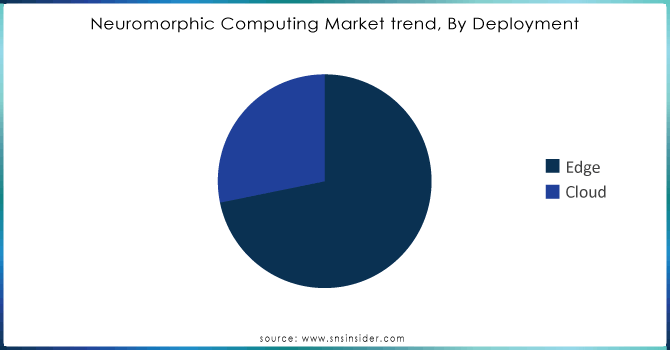

Edge segment led the market in 2023, accounted 71.8% of revenue share Growth of the segment is attributed to rise in adoption of edge computing for applications including touchless interfaces, voice-controlled cars and smart assistant robots. The increasing adoption of wireless networking will, in turn, raise interest towards the edge computing paradigm which is set to foster growth with respect to this vertical as more service providers look at hosting applications closer (or within) their end-user base. Edge computing is also being embraced at scale world over with the new generation of AI hardware supporting low-power applications and in-device adaptability fuelling broader market expansion beyond conventional micro data centres.

The cloud computing offers various technological benefits and expected to grow with fastest CAGR during the forecast period is expected in. These include a scalable data-managing platform for enterprise with secure one-click big-data storage and distribution. Cloud-based neuromorphic computing has the advantages of easy resource scaling, low initial hardware and software investment costs for users to share their workloads on demand with others around the world. Latency and security issues might serve as potential obstacles. The advancement in neuromorphic computing systems employ more powerful on-device processing capabilities mitigating the need for data canters and supporting expansion in cloud computing segment as well. The advantages of cloud computing, coupled with neuromorphic technology are appealing to the enterprise.

Need any customization research on Neuromorphic Computing market - Enquiry Now

Regional analysis

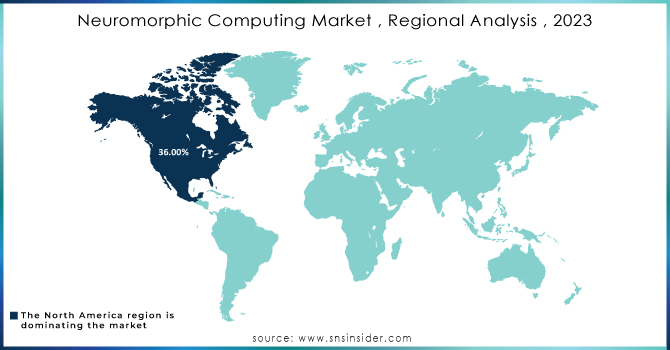

North America dominated the market with revenue a share of more than 36% in the market during 2023 This is because, the US and Canada have deployed a significant number of neuromorphic computing applications earlier than other regions that puts them in leading position to drive change. One of the significant trends in North America is the movement toward AI-powered voice and speech recognition which has improved quality of various of speech engines for better user experience. During the forecast period, Europe is anticipated to witness substantial growth. The sector is home to several programmes and institutions oriented towards neuromorphic computing. Moreover, increasing adoption of biometric systems across various European countries is creating potential growth opportunities for the application areas in image processing utilizing neuromorphic computing. Europe's commitment to neuromorphic computing positions it as a key player in the field, provide many opportunities for companies and academics ready to innovate around this rapidly evolving technology

Key Players

The major players are General Vision, Inc., Samsung Electronics Co., Ltd, Brain Corporation, HRL Laboratories LLC, Knowm Inc., BrainChip Holdings Ltd., International Business Machines Corporation, Hewlett Packard Company, Intel Corporation, CEA-Leti, Qualcomm Technologies, Inc, Vicarious FPC, Inc., Applied Brain Research Inc., and others in the final report.

Recent Developments

-

IBM came up with an AI Chip built using 7nm technology that was so power efficient at, back in January,2023. The AI hardware accelerator chip offers state-of-the-art power efficiency and supports a wide range of model types. It is scalable from training large scale models in the cloud all the way down to enhancing security and privacy by bringing training closer to edge devices, allowing data almost never touching it's source.

-

In February SynSense combined forces with iniVation to address the rising demand for intelligent vision in high-performance consumer and industrial markets. Collaboration to develop neuromorphic technology for standalone processors, vision sensors and systems with integrated compute in sensor offering use cases across robotics, automotive consumer devices powered by the company’s edge AI product gallery.

-

SiLC Technologies October 2023, Eyeonic Vision System FMCW LiDAR Machine Vision The system supports rapid and accurate object identification, as well as the detection of polarization intensities and 3D distance to an accuracy of millimeters in distances greater than one kilometer.

-

The method for training neuromorphic chips to recognise cystic fibrosis using a biosensor was created by Dutch research scientists from Eindhoven University of Technology in September 2023. The "smart biosensor" has the potential for many point-of-care healthcare applications and could also be useful in enabling chips to automatically adjust themselves to their environments.

-

BrainChip Holdings Ltd. entered a collaboration with one of its technology partners, Lorser Industries Inc., for Neuromorphic computing arrangements in June 2023. In addition, the partnership gives BrainChip its first development deal for Akida in software-defined radio (SDR).

| Report Attributes | Details |

| Market Size in 2023 | USD 23.16 Bn |

| Market Size by 2032 | USD 81.12 Bn |

| CAGR | CAGR of 90% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software) • By Application (Signal Processing, Image Processing, Data Processing, Object Detection, Others) • By Deployment (Edge, Cloud) • By End-Use (Consumer Electronics, Automotive, Healthcare, Military & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | General Vision, Inc., Samsung Electronics Co., Ltd, Brain Corporation, HRL Laboratories LLC, Knowm Inc., BrainChip Holdings Ltd., International Business Machines Corporation, Hewlett Packard Company, Intel Corporation, CEA-Leti, Qualcomm Technologies, Inc, Vicarious FPC, Inc., Applied Brain Research Inc. |

| Key Drivers | • Growing Adoption of Neuromorphic Computing to Transform Internet of Things (IoT) to drive the Market Growth • The ability of neuromorphic systems to process large amounts of data quickly and efficiently supports real-time applications in autonomous vehicles, robotics, and AI-driven systems. |

| Market Restraints | • The research and development of neuromorphic chips and systems require significant investment, which can be a barrier for smaller companies and startups. |

Frequently Asked Questions

Ans. There are four segments cover in this report, By Component, By Application, By Deployment, By End-Use.

Ans. The forecast period for the Neuromorphic Computing Market is 2024-2032.

Ans: The Neuromorphic Computing Market size was valued at USD 86.9 Mn in 2023

Ans: The Neuromorphic Computing Market is to grow at a CAGR of 86.27% Over the forecast period of 2024-2032.

Ans: The North American region is dominating the Neuromorphic Computing Market.

Get in Touch