Olive Oil Market Report Scope & Overview:

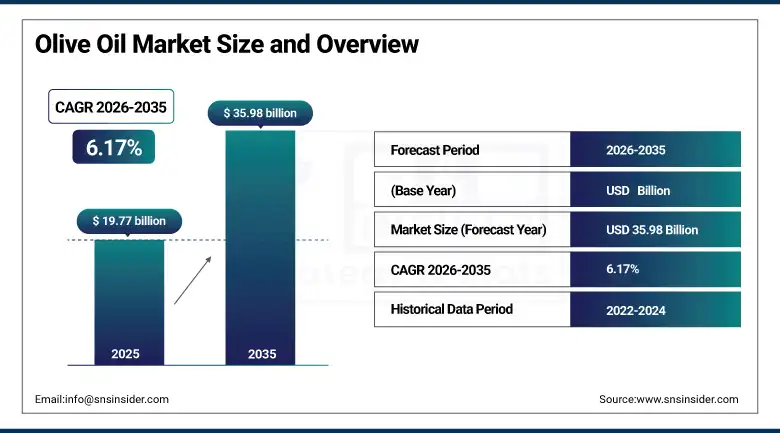

The Olive Oil market was valued at USD 19.77 billion in 2025 and is expected to reach USD 35.98 billion by 2035, growing at a CAGR of 6.17% from 2026–2035.

The global olive oil market encompasses production concentrated almost entirely in the Mediterranean basin, where Spain, Italy, Greece, Tunisia, Morocco, and Turkey collectively account for approximately 95% of world production through climatic and agronomic conditions that the olive tree requires for productive fruit-bearing cultivation, with consumption spreading across all continents as health-conscious dietary trends, Mediterranean cuisine popularisation, and food industry adoption of olive oil as a premium cooking and finishing oil ingredient drive demand far beyond the traditional producing and consuming regions. The market is structured across a quality hierarchy from extra virgin olive oil at the premium tier through virgin olive oil, ordinary virgin olive oil, and refined olive oil to olive pomace oil at the commodity tier, with each grade defined by free acidity levels, sensory characteristics, and extraction process compliance standards enforced by the International Olive Council and reflected in national import and labelling regulations across major consuming markets.

Over 45% of global consumers across surveyed markets report preferring extra virgin olive oil for daily cooking and salad dressing applications, a finding that reflects both the health-driven premiumisation trend reshaping the edible oils category globally and the flavour quality differential that top-quality EVOO provides in culinary applications where the oil's taste contribution is part of the dish's final character.

Olive Oil Market Size and Forecast

-

Market Size in 2026E: USD 20.99 Billion

-

Market Size by 2035: USD 35.98 Billion

-

CAGR: 6.17% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

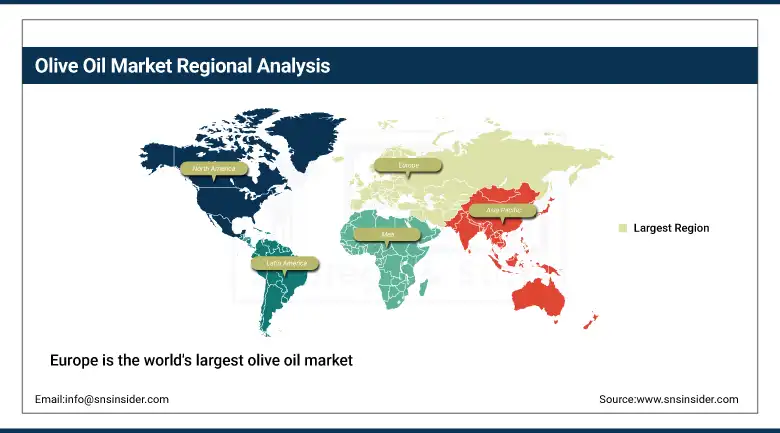

Largest Region: Europe

To Get more information On Olive Oil Market - Request Free Sample Report

Olive Oil Market Trends

-

Rising consumer preference for certified organic and single-origin extra virgin olive oils that can demonstrate provenance, harvest date, polyphenol content, and extraction methodology through digital traceability systems and third-party certification, supporting premium pricing differentiation in a commodity-adjacent category where brand trust and authenticity are key purchase drivers.

-

Growing e-commerce penetration of olive oil retail, where direct-to-consumer sales from Mediterranean producers and olive oil subscription services curating seasonal harvests from small estates are bypassing traditional import and retail distribution to deliver premium fresh-harvest oils to health-conscious consumers across North America, Northern Europe, and Asia Pacific.

-

Expanding culinary adoption of extra virgin olive oil as a finishing oil, dipping condiment, and premium flavour ingredient in food service and home cooking beyond its Mediterranean heritage markets, driven by cooking media, chef endorsement, and food culture programming that has elevated olive oil's status from functional cooking fat to taste ingredient in global premium culinary culture.

-

Increasing integration of olive oil into cosmetic and personal care formulations including premium facial moisturisers, hair treatment masks, skin care serums, and body care products where its oleic acid content and polyphenolic antioxidant composition are marketed as anti-ageing, moisturising, and protective skin wellness benefits that justify premium positioning.

-

Growing production and market development of olive oil varieties outside the traditional Mediterranean production zone, including from California, Australia, Argentina, Chile, and South Africa, where favourable climate regions and quality-oriented producers are establishing internationally recognised premium EVOO brands that diversify the global supply base and create new origin stories for marketing to quality-conscious global consumers.

U.S. Olive Oil Market Outlook

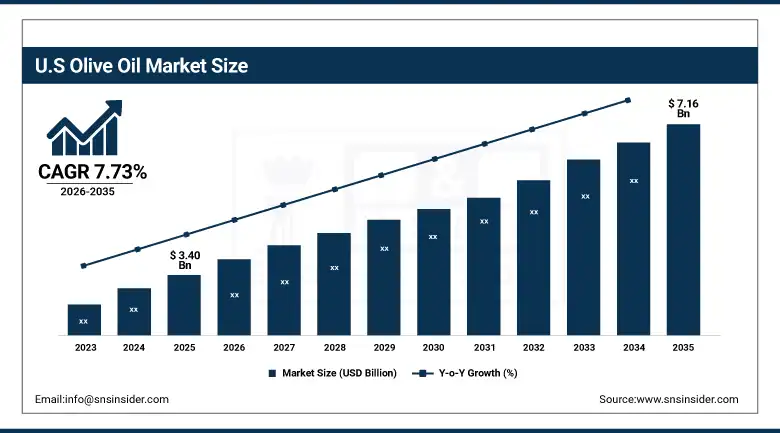

The U.S. Olive Oil Market was valued at approximately USD 3.40 billion in 2025 and is expected to reach approximately USD 7.16 billion by 2035, growing at a CAGR of 7.73%, driven by rising health-conscious consumption patterns, increasing adoption of Mediterranean dietary principles endorsed by cardiovascular medical organisations, premiumisation toward extra virgin varieties among quality-aware consumers, and expanding specialty retail and online channels bringing a wider range of high-quality imported and domestic olive oils to engaged consumers.

The United States has emerged as one of the world's leading olive oil consumer markets, having surpassed Spain as the second-largest consumer globally in 2023 as the combination of Italian-American culinary tradition, Mediterranean diet health marketing, chef-driven EVOO advocacy in food media, and expanding health-food retail distribution collectively drove American per-capita consumption to levels that reflect genuine dietary integration rather than occasional specialty use. The domestic California olive oil industry, anchored by producers in the San Joaquin Valley and Mission olive heritage estates in the coastal foothills, has developed a quality-oriented segment that commands premium pricing based on freshness, polyphenol content transparency, and California agricultural certification that differentiates domestic producers from imported commodity oils whose labelling compliance with EVOO quality standards has faced persistent scrutiny and regulatory attention. USDA voluntary olive oil quality standards and increasing state-level labelling enforcement are improving market transparency and supporting consumer confidence in premium domestic and imported olive oil purchases.

The American Heart Association's dietary guidance endorsing olive oil as the preferred cooking and finishing fat for heart-healthy dietary patterns, combined with the FDA's qualified health claim permitting olive oil manufacturers to reference its monounsaturated fat content in relation to reduced cardiovascular disease risk on product labels, provides an institutional endorsement infrastructure that supports premium olive oil's positioning as a health investment rather than merely a culinary ingredient.

Olive Oil Market Segment Analysis

-

By Type, Extra Virgin Olive Oil dominated with the largest market share in 2025, driven by premium health positioning, superior flavour quality, and consumer preference for minimally processed natural products; Organic olive oil is the fastest-growing type sub-segment as sustainability and clean-label purchasing motivations drive premiumisation at the top of the EVOO quality tier.

-

By Application, Food & Beverages dominated as the primary use category encompassing household cooking, food service, and food manufacturing applications that collectively account for the overwhelming majority of global olive oil consumption; Cosmetics & Personal Care is the fastest-growing application as formulators increase olive oil and olive-derived ingredient integration in premium skin care and hair care products.

-

By Distribution Channel, Supermarkets & Hypermarkets held approximately 54.20% of revenues in 2025 as the primary access point for mass-market olive oil purchases across all quality tiers; Online retail is the fastest-growing channel at a CAGR of 9.10% driven by direct-to-consumer premium olive oil sales, subscription services, and specialty imported variety access unavailable in physical retail assortments.

-

By Packaging, Bottles led the market through their versatility, visual merchandising advantages, and consumer preference for glass bottles in premium EVOO segments where the packaging quality signals product quality; tins maintain importance in food service and institutional markets where larger format packaging reduces per-unit cost.

By Type, Extra Virgin Olive Oil dominates, Organic is expected to grow fastest

Extra Virgin Olive Oil retained the dominant type position in the Olive Oil Market in 2025, reflecting the convergence of health-driven consumer motivation and culinary quality preference that positions EVOO as the default choice for health-aware consumers who have made olive oil their primary dietary fat. EVOO's strict quality standard requirements including free acidity below 0.8%, absence of defects in sensory panel evaluation, and prohibition of any processing beyond mechanical extraction establish a meaningful quality threshold above commodity oils that allows producers and retailers to command sustained price premiums in consumer markets where health and quality consciousness supports premium edible oil spending. The extra virgin category's growth is being further supported by the expansion of the gourmet and artisan food retail channel in major consuming markets, where specialty shops, farmers markets, and premium grocery chains dedicate significant shelf space and buyer expertise to curating premium-quality extra virgin olive oils from specific Mediterranean origin regions, harvest years, and variety types that engage connoisseur consumers willing to pay exceptional prices for demonstrably superior quality.

Refined olive oil holds a substantial market share as the affordable cooking-grade alternative for price-sensitive consumers who value olive oil's cooking properties and health reputation relative to other refined vegetable oils but cannot or do not prioritise the premium pricing associated with extra virgin quality. The refined segment serves important volume in food manufacturing applications where olive oil's flavour and functional properties are valued in products including mayonnaise, salad dressings, marinades, canned fish, and baked goods without the additional cost of extra virgin quality being commercially justified for the application.

By Distribution Channel, Supermarkets & Hypermarkets dominate, Online is expected to grow fastest

Supermarkets and Hypermarkets retained the dominant distribution position with approximately 54.20% of Olive Oil Market revenues in 2025, reflecting their role as the primary food retail environment in virtually every major consuming market where both commodity-grade and premium EVOO products are accessible to consumers during regular grocery shopping trips that represent the majority of olive oil purchase occasions. Large format food retailers including Carrefour, Walmart, Tesco, Aldi, Kroger, and their regional equivalents provide multi-brand, multi-price-tier olive oil assortments that allow consumers to trade up from basic refined grades to premium extra virgin varieties as health awareness and quality appreciation develop, supporting the premiumisation dynamic that is the primary growth driver for the global olive oil market's value expansion. Premium supermarket chains and specialty food retailers within the supermarket channel are increasingly dedicating dedicated olive oil sections with expanded premium assortments, educational signage, and tasting station amenities that create an in-store experience appropriate for a product category where flavour education drives repeat purchase of premium varieties.

Online retail is the fastest-growing distribution channel at a CAGR of 9.10% through 2035, driven by the structural advantages that e-commerce provides for premium olive oil as a high-interest, research-intensive specialty food product where consumers seek detailed information about origin, harvest date, producer, polyphenol content, and independent quality certifications that physical retail shelf space cannot accommodate but digital product pages can convey comprehensively. Direct-to-consumer sales by Mediterranean producers shipping freshly harvested oils directly to consumers across North America, Northern Europe, and Asia Pacific through brand websites and subscription services are bypassing traditional import distribution to deliver demonstrably fresher oils at prices that reflect the producer's capture of distribution margin, creating a growing premium e-commerce segment that is establishing loyal customer relationships around harvest-season purchasing cycles.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.3% |

|

Europe |

Spain |

27.4% |

|

Asia Pacific |

China |

40.1% |

|

Middle East & Africa |

UAE |

29.3% |

|

Latin America |

Brazil |

41.5% |

North America Olive Oil Market Insights

North America holds a substantial share of global Olive Oil Market revenues with the United States accounting for approximately 86.3% of North American revenues and representing one of the world's most strategically important olive oil importing and consuming markets. The United States' rise to its position as the second-largest global olive oil consumer reflects sustained marketing investment by Italian, Spanish, and Greek export organisations promoting Mediterranean diet health benefits, the expansion of Italian and Mediterranean cuisine into mainstream American dining culture, and the influence of culinary media including cooking programmes, food journalism, and chef culture that has elevated extra virgin olive oil's status in American kitchen culture from specialty ingredient to pantry essential. California's emerging domestic olive oil industry, producing roughly 3 to 4% of domestic consumption from approximately 50,000 acres of olive cultivation, adds a local production narrative that premium retailers and food service operators use to support domestic origin marketing and supply chain transparency positioning.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Olive Oil Market Insights

Europe is the world's largest olive oil market by both production and consumption, with Spain, Italy, and Greece collectively accounting for the majority of global production and European consumers maintaining the highest per-capita olive oil consumption levels globally across the traditional Mediterranean diet countries. Spain leads European olive oil production and export with approximately 27.4% of European olive oil market revenues concentrated in the Spanish domestic market alongside exports to the rest of Europe and the world, anchored by the Andalusian olive growing region that produces more olive oil than any other country or region globally. European market dynamics are shaped by the tension between record retail price increases following drought-related harvest failures in 2023 and 2024 that temporarily elevated olive oil consumer prices to levels that induced trade-down behaviour toward other edible oils, and the underlying long-term structural demand growth driven by Mediterranean diet adoption in Northern European markets and the health positioning that sustains premium EVOO demand even as prices fluctuate.

Asia Pacific Olive Oil Market Insights

Asia Pacific is the fastest-growing regional olive oil market, driven by rapidly rising health awareness and Mediterranean diet interest among affluent urban consumers in China, Japan, South Korea, and India, combined with the expansion of premium grocery retail and online specialty food channels that make high-quality imported olive oils accessible to growing middle-class consumer segments whose disposable income supports premium edible oil spending. China accounts for approximately 40.1% of Asia Pacific olive oil revenues as the region's largest national market, where olive oil imports have grown substantially over the past decade as Chinese consumers associate the product with European culinary sophistication, natural health benefits, and premium food culture that resonates with the aspirational consumption patterns of China's urban upper-middle class. Australia contributes both as a producing and consuming market, with a developed domestic olive oil industry whose quality-oriented producers compete credibly with Mediterranean imports in the premium segment while benefiting from proximity and preferential trade arrangements within the Asia Pacific regional market.

MEA & Latin America Olive Oil Market Insights

The Middle East and Africa and Latin America represent growing olive oil markets with distinct structural characteristics. MEA is unique in including both major producing and major consuming markets within the same regional grouping, with Tunisia, Morocco, and Turkey contributing substantially to global production while UAE, Saudi Arabia, and other Gulf Cooperation Council countries represent premium-consuming import markets where olive oil's Mediterranean culinary associations and health positioning align with the premium food culture of affluent Gulf consumers. UAE leads MEA consuming market revenues at approximately 29.3% of the regional total through its role as a regional trade hub, high per-capita income supporting premium edible oil purchasing, and cosmopolitan food culture incorporating Mediterranean dietary elements. Latin America is developing as a market where Brazil and Argentina lead consumption growth at approximately 41.5% and growing shares of regional revenues respectively, with Brazil's large urban population increasingly incorporating olive oil into cooking routines as health awareness rises and retail distribution improves.

Market Dynamics

Growth Drivers: Mediterranean diet global adoption driven by scientific health evidence combined with premiumisation trends in edible oils rewarding EVOO's quality differentiation with sustained price premium acceptance

The primary structural growth drivers for the Olive Oil Market are the scientifically documented and institutionally endorsed health benefits of olive oil consumption that create a health investment motivation for purchase that insulates premium EVOO demand from purely price-driven commodity switching behaviour, combined with the global spread of Mediterranean culinary culture through restaurants, food media, culinary tourism, and diaspora food culture that is expanding olive oil consumption beyond its traditional European and Middle Eastern base into the massive consumer populations of Asia, North America, and Latin America. The growing evidence base linking regular extra virgin olive oil consumption to reduced mortality from cardiovascular disease, reduced risk of metabolic syndrome, anti-inflammatory effects documented in clinical interventions, and potential protection against cognitive decline in ageing populations provides a uniquely powerful health narrative that physicians, dietitians, and public health authorities are increasingly comfortable endorsing, creating a healthcare professional recommendation channel that drives premium edible oil purchasing in health-prioritising consumer segments. Climate change's impact on Mediterranean olive production, while creating short-term price volatility and harvest uncertainty, is accelerating investment in irrigation technology, drought-resistant olive variety development, and geographic diversification of production to new regions that collectively support the market's long-term supply security.

Restraints: Supply concentration in climate-vulnerable Mediterranean production regions creating price volatility, widespread olive oil adulteration and mislabelling undermining consumer trust, and price premium limiting mass-market penetration in cost-sensitive demographics

A significant restraint on the Olive Oil Market is the extraordinary geographic concentration of global production in a small number of Mediterranean countries that creates systematic vulnerability to regional drought, frost, olive fruit fly infestation, and other agricultural disruption events that can reduce global supply by 20 to 40% in affected years, triggering retail price spikes that disrupt consumer purchasing patterns and accelerate trade-down to competing edible oils whose supply chains are distributed across more geographically diverse production bases. The 2023 and 2024 Mediterranean drought conditions that severely reduced olive harvests in Spain, Italy, and Greece drove global EVOO retail prices to historic highs in many markets, providing a stress test of the premium segment's demand resilience that demonstrated both the loyalty of health-motivated premium consumers and the price sensitivity thresholds that cause even committed olive oil users to reduce purchase frequency or trade down to lower quality grades. The long-standing problem of olive oil adulteration and mislabelling, where lower-quality refined oils or non-olive vegetable oils have historically been fraudulently labelled as extra virgin olive oil in international trade, continues to undermine consumer trust and compress the price premium that genuine premium EVOO can sustain in retail markets where certification and verification infrastructure is underdeveloped.

Opportunities: Digital traceability technology enabling provenance verification and premium authentication, new production geography development diversifying supply, and functional food and cosmetic industry application expansion

Blockchain and digital traceability technology applications in olive oil supply chain verification represent a commercial opportunity for premium producers to substantiate the quality claims that support their price premiums through immutable records of harvest date, grove location, chemical analysis, and chain of custody that consumers can access through QR codes on product packaging. Several Italian, Spanish, and Greek premium olive oil producers have deployed blockchain traceability systems that enable retail consumers to verify the complete provenance of the oil in their bottle from grove through pressing to bottling, a transparency capability that meaningfully differentiates premium products from commodity imports and supports the price premiums that make premium olive oil production economically sustainable. The cosmetic and personal care industry's growing use of olive-derived ingredients including squalene, hydroxytyrosol, olive polyphenols, and olive wax in premium skin care formulations creates an additional demand channel that generates value from the full spectrum of olive oil processing outputs beyond the food-grade oil itself, improving the economics of premium olive processing operations.

Recent Developments:

-

September 2025: Corto launched its Agrumato-Method Olive Oil Gift Set, incorporating two limited-edition oils produced by cold-extracting freshly picked California olives simultaneously with fresh seasonal botanicals including Calabrian chili and Lemon Verbena, demonstrating the premium flavour innovation that is expanding olive oil's appeal beyond functional cooking fat into artisan culinary gift and specialty food retail categories.

-

2025: The California Olive Ranch expanded its domestic production capacity and retail distribution across the United States, marketing its freshness-dated 100% California-origin extra virgin olive oil as a superior alternative to imported oils whose transit time compromises polyphenol content and sensory quality by the time they reach American retail shelves.

-

2025: Deoleo, the world's largest olive oil company operating the Bertolli, Carapelli, and Carbonell brands, advanced its sustainability strategy with expanded organic certified production and invested in traceability technology connecting retail consumers to producer grove origins across its multi-country supply base.

-

2025: Australia's Western Australian olive oil producers collectively invested in coordinated export marketing to Asia Pacific markets, building on the region's quality reputation and geographic proximity advantage to compete with Mediterranean exports in Chinese and Japanese premium EVOO retail channels.

-

July 2025: Wikifarmer, the Athens and Seville-based online agricultural marketplace, initiated operations in the United Kingdom, expanding its direct producer-to-buyer olive oil trading platform that connects Mediterranean olive producers with food businesses and specialist retailers across European markets seeking traceable, competitively priced premium olive oil sourcing.

Olive Oil Market Key Players

-

Deoleo S.A. (Bertolli, Carapelli, Carbonell)

-

Filippo Berio & C. S.p.A.

-

Borges International Group

-

Salov Group (Filippo Berio)

-

Cargill Incorporated

-

California Olive Ranch

-

Ybarra Alimentacion S.L.

-

Gallo Worldwide

-

DCOOP (Oleoestepa)

-

SOVENA Group

-

Minerva SA

-

Colavita USA LLC

-

Pompeian Inc.

-

Alovitox Superfoods

-

Corto Olive

-

McEvoy Ranch

-

Kirkland Signature (Costco Wholesale)

-

Lucini Italia Company

-

Spectrum Organics (Hain Celestial Group)

-

Roland Foods LLC

Olive Oil Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.77 Billion |

| Market Size by 2035 | USD 35.98 Billion |

| CAGR | CAGR of 6.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Extra Virgin Olive Oil, Virgin Olive Oil, Refined Olive Oil, Pomace Olive Oil, Others) • By Application (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Others) • By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Food Service, Others) • By Packaging (Bottles, Tins/Cans, Pouches, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Deoleo S.A. (Bertolli, Carapelli, Carbonell), Filippo Berio & C. S.p.A., Borges International Group, Salov Group (Filippo Berio), Cargill Incorporated, California Olive Ranch, Ybarra Alimentacion S.L., Gallo Worldwide, DCOOP (Oleoestepa), SOVENA Group, Minerva SA, Colavita USA LLC, Pompeian Inc., Alovitox Superfoods, Corto Olive, McEvoy Ranch, Kirkland Signature (Costco Wholesale), Lucini Italia Company, Spectrum Organics (Hain Celestial Group), Roland Foods LLC |

Frequently Asked Questions

Europe dominated the Olive Oil Market in 2025 as the world's leading olive oil producing and consuming region.

Extra Virgin Olive Oil dominated the Olive Oil Market in 2025 through its premium health positioning and superior culinary quality.

The global spread of Mediterranean diet adoption driven by extensive scientific evidence of cardiovascular and anti-inflammatory health benefits, combined with premiumisation trends in edible oils that reward extra virgin olive oil's quality differentiation with sustained consumer price premium acceptance.

The Olive Oil Market was valued at USD 19.77 billion in 2025.

The Olive Oil Market is expected to grow at a CAGR of 6.17% from 2026 to 2035.

Get in Touch