Opto Semiconductors Market Size & Overview

Get More Information on Opto Semiconductors Market - Request Sample Report

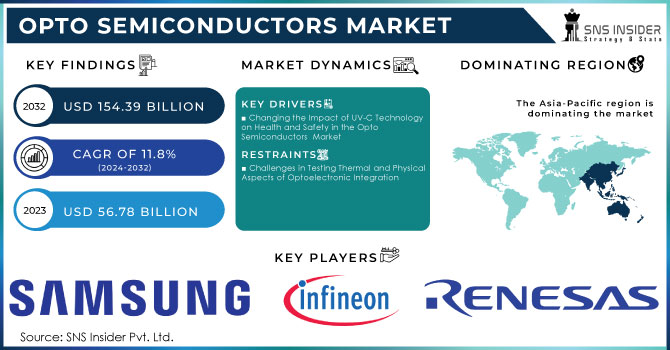

The Opto Semiconductors Market Size was valued at USD 56.78 Billion in 2023 and is expected to reach USD 154.39 Billion by 2032 and grow at a CAGR of 11.8% over the forecast period 2024-2032.

The Opto semiconductors market is set to experience substantial expansion, fueled by rising needs for sophisticated lighting options, communication advancements, and health-related uses. Important reasons for this growth include the increasing use of UV-C LEDs for disinfection in healthcare, consumer electronics, public areas, and household devices. The increasing adoption of contactless technology, such as touch-free payment systems and robotic disinfection devices, is continuing to drive the need for Opto Semiconductors s. Advances in Optoelectronic materials and progress in miniaturization allow for the creation of improved and adaptable solutions. Moreover, the increasing emphasis on energy efficiency and sustainability is driving the use of LED lighting technologies. As per the U.S. Department of Energy, LED lighting is forecasted to decrease energy usage by 50% to 75% in comparison with traditional incandescent bulbs. With a focus on cleanliness and safety, the Opto Semiconductors market is expected to be a vital player in meeting these changing demands, presenting an appealing investment prospect for technology industry stakeholders. The intersection of these developments emphasizes the significance of Opto semiconductors in creating a greener, more effective future.

The Opto Semiconductors market is growing strongly due to rising demand in sectors like telecommunications, automotive, and medical devices. The latest events, like Polymatech Electronics' USD 16.2 million investment in creating a semiconductor manufacturing site in Bahrain, highlight this pattern. The company plans to broaden its focus on Opto-semiconductors, such as LEDs, lasers, and photodetectors, through its new facility, targeting markets in West Asia and North Africa. This tactical decision also indicates a wider trend in the industry towards power semiconductors and advanced data transmission technologies, especially with the introduction of 5G and upcoming 6G networks. Moreover, the worldwide demand for energy efficiency and sustainability is driving the growth of Optoelectronic devices, which are essential for improving the effectiveness and efficiency of different applications. Polymatech aims to boost its annual chip production from 2 billion to 5 billion by the end of 2024, positioning the Opto Semiconductors market for continued growth in line with the demand for smaller devices and cutting-edge solutions in an increasingly interconnected society.

Opto Semiconductors Market Dynamics

Drivers

-

Changing the Impact of UV-C Technology on Health and Safety in the Opto Semiconductors Market

Innovations in UV-C technology are revolutionizing disinfection applications, presenting significant growth opportunities for the Opto Semiconductors market. UV-C light, characterized by its short wavelength, possesses germicidal properties that effectively inactivate viruses, bacteria, and other pathogens. This functionality has become increasingly crucial across various sectors, particularly healthcare, hospitality, and public spaces, as businesses and consumers emphasize cleanliness and safety. In healthcare settings, for example, UV-C LEDs are being integrated into devices designed for disinfecting surfaces, medical equipment, and air. Hospitals are adopting UV-C systems to sanitize operating rooms and patient areas, achieving a remarkable reduction in healthcare-associated infections (HAIs). According to a study published in the American Journal of Infection Control, UV-C disinfection has been shown to lower microbial counts by over 90% in hospital environments. Additionally, UV-C technology is being implemented in public transportation systems and facilities to promote cleaner conditions; high-touch surfaces in trains, buses, airports, and shopping malls are regularly disinfected using UV-C light systems. The U.S. Environmental Protection Agency (EPA) has also recognized the efficacy of UV-C technology in disinfecting both air and surfaces, highlighting its potential as a public health solution. The growing interest in personal hygiene has led to the creation of consumer products featuring UV-C technology, such as sanitizing wands and phone sanitizers, further driving the demand for UV-C Optoelectronics. Moreover, the transition toward UV-C LEDs over traditional mercury-based lamps is significant; LEDs offer longer lifespans, reduced energy consumption, and lower environmental impacts.

-

The Increasing Popularity of Optoelectronics Manufacturing Services Outsourcing

The Optoelectronics market is experiencing growth due to the rising popularity of outsourcing Electronics Manufacturing Services (EMS). Different industries, such as automotive and consumer electronics, are looking towards EMS providers to produce top-notch Optoelectronic components like LEDs, optical sensors, Optocouplers, and photonic cells. This trend gives manufacturers a competitive advantage as they can concentrate on their main strengths, while also benefiting from the specialized skills and efficiencies of EMS providers. Outsourcing leads to lower production costs and improved product quality by working with certified organizations dedicated to high standards due to the growing complexity of electronic components and the need for specialized manufacturing skills. Additionally, the U.S. Department of Commerce underlines the significance of dependable manufacturing procedures, affirming that certified manufacturers have the capability to create components that adhere to strict quality standards, especially for industries that heavily rely on Optoelectronic applications.

Outsourcing companies demonstrate their dedication to top-notch manufacturing by meeting the needs of multiple industries, leading to a rise in the worldwide need for Optoelectronics. This trend emphasizes how crucial outsourcing is for improving production efficiency and product innovation, which in turn enhances growth in the Optoelectronics market. The demand for Optoelectronic components is projected to increase significantly in the forecast period due to manufacturers' growing preference for outsourcing their production needs.

Restraints

-

Challenges in Testing Thermal and Physical Aspects of Optoelectronic Integration

Thermal and physical testing challenges pose significant restraints for the growth of the Opto Semiconductors market, which are linked to the integration of Optoelectronic devices. These modern gadgets are frequently crafted from semiconductor materials, whether organic or inorganic, that commonly undergo energy loss and heating while in use. The generation of heat can lead to variations in performance and the creation of defect centers in the semiconductor, impacting its functionality negatively. One significant challenge is the effective control of heat in these devices, as achieving precise temperature measurements can be very challenging. Due to their poor thermal conductivity, Optoelectronic devices may face challenges when placed on temperature-sensing platforms, making the thermal testing process more complex.In order to address these problems, researchers are turning more and more to infrared (IR) thermography as a workable solution. This technology allows for non-invasive temperature measurements and monitoring, greatly improving the assessment of thermal performance in Optoelectronic devices.

Opto Semiconductors Market - Segment Analysis

by Type

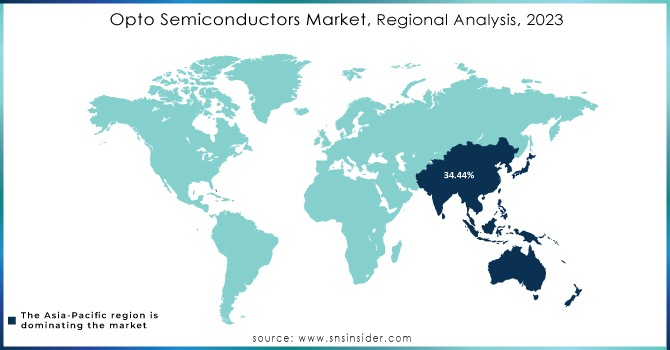

The Opto Semiconductors market in 2023 was dominated by LED and Li-Fi equipment, which together accounted for a significant 34.44% of revenue share. The increase is due to the wide use of LED technology in different areas like general lighting, automotive lighting, and consumer electronics. Philips Lighting and other companies have introduced cutting-edge LED products that prioritize energy efficiency and intelligent lighting options. Additionally, progress in Li-Fi technology, which uses light for fast data transfer, is increasing in industries like telecommunications and healthcare. An example of this is pureLiFi, a leading company in Li-Fi technology, which recently introduced new Li-Fi solutions that offer quicker and more secure wireless communication, ultimately boosting market expansion. The demand in this segment is anticipated to surge due to the incorporation of Li-Fi into smart environments and IoT applications. Furthermore, there is a growing trend among manufacturers to dedicate more resources to research and development in order to improve the effectiveness of LED technologies and to discover new uses, such as horticultural lighting and Li-Fi for augmented reality environments. This emphasis on creativity, combined with the move towards energy-saving lighting options, is predicted to maintain the growth trend of the LED and Li-Fi equipment sector in the Opto Semiconductors market.

by Application

In 2023, the consumer electronics sector played a major role in driving the Opto Semiconductors market, securing a dominant revenue share of 39.44%. The increasing popularity of high-tech electronic gadgets like smartphones, tablets, and smart home devices is the main reason for this dominance, as these products rely more and more on Optoelectronic components for their features and efficiency. Prominent companies like Samsung and Apple have played a crucial role in this expansion by releasing groundbreaking products that showcase advanced Optoelectronic technology. An example of this is the Galaxy S23 series released by Samsung, which incorporates cutting-edge OLED screens that use Optoelectronic materials to improve both visual clarity and energy consumption. In the same way, Apple has integrated LiDAR technology into the iPhone 15 to enhance augmented reality capabilities and camera features by accurately measuring distances. Moreover, the increasing popularity of smart home gadgets such as Amazon Echo and Google Nest, equipped with Optoelectronic sensors for enhanced interaction and automation, is also driving market expansion. The rapid advancement of consumer electronics towards more complex and interlinked devices is projected to keep boosting the Opto Semiconductors market, encouraging more innovation and product enhancements to meet consumer demands for better performance and features.

Opto Semiconductors Market - Regional Outlook

In 2023, the Asia-Pacific region emerged as a leader in the Opto Semiconductors market, capturing a substantial revenue share of 34.44%. This dominance is primarily driven by the region's robust electronics manufacturing base, rapid technological advancements, and increasing demand for consumer electronics. Notably, companies such as Sony and Panasonic are at the forefront of innovation in this sector. Sony recently launched a series of advanced image sensors that utilize Optoelectronic technology, enhancing image quality in both consumer and professional cameras. Meanwhile, Panasonic unveiled its next-generation OLED display technology, which leverages Optoelectronic components to deliver superior energy efficiency and vibrant color reproduction. Additionally, the growing adoption of smart devices and the Internet of Things (IoT) in countries like China, Japan, and South Korea further fuels market expansion. The demand for high-performance Optoelectronic components is also driven by significant investments in 5G infrastructure, with companies like Huawei and ZTE integrating Optoelectronics in their telecom solutions. As Asia-Pacific continues to lead in technological innovation and manufacturing capabilities, the region is well-positioned to maintain its dominance in the Opto Semiconductors market, fostering further developments and investments in the coming years.

In 2023, North America emerged as the fastest-growing region in the Opto Semiconductors market, driven by robust technological innovation, a strong demand for advanced Optoelectronic solutions, and significant investments in research and development. Leading companies such as Intel and Broadcom are at the forefront of this growth. Intel recently unveiled its new line of photonic integrated circuits designed to enhance data transfer speeds and reduce power consumption in data centers, aligning with the increasing demand for high-performance computing and cloud services. Additionally, Broadcom launched a range of optical transceivers that cater to the burgeoning 5G infrastructure and high-speed networking needs, showcasing its commitment to advancing communication technologies. Furthermore, the automotive sector in North America is witnessing a surge in demand for Optoelectronic components, particularly in the development of advanced driver-assistance systems (ADAS) and autonomous vehicles. Companies like Tesla and General Motors are integrating sophisticated Optoelectronic sensors to improve vehicle safety and performance. This combination of technological advancements, strategic product launches, and a focus on next-generation applications positions North America as a dynamic hub for Opto Semiconductors growth, signaling a promising outlook for the industry in the region.

Need Any Customization Research On Opto Semiconductors Market - Inquiry Now

Key Players

Some of the major key players in Opto Semiconductors Market who offering their product:

-

Samsung Electronics Co., Ltd. (LEDs, Optical Sensors)

-

Sony Corporation (Image Sensors, Optical Devices)

-

Osram Licht AG (LEDs, Laser Diodes)

-

Broadcom Inc. (Optical Transceivers, Infrared Emitters)

-

ON Semiconductor Corporation (Photodiodes, LED Drivers)

-

Vishay Intertechnology, Inc. (Optocouplers, Infrared Emitters)

-

ROHM Semiconductor (Laser Diodes, LEDs)

-

Cree, Inc. (Wolfspeed) (Silicon Carbide (SiC) LEDs, Power Semiconductors)

-

Lumentum Holdings Inc. (Laser Diodes, Optical Communication Components)

-

AMS AG (Ambient Light Sensors, Proximity Sensors)

-

Nichia Corporation (High-Intensity LEDs, Laser Diodes)

-

Infineon Technologies AG (Optical Sensors, LED Drivers)

-

Toshiba Corporation (Optoelectronic Devices, Laser Diodes)

-

Renesas Electronics Corporation (LED Drivers, Optical Sensors)

-

II-VI Incorporated (Laser Diodes, Photonic Devices)

-

Lite-On Technology Corporation (LEDs, Optocouplers)

-

Panasonic Corporation (LEDs, Phototransistors)

-

Acuity Brands, Inc. (LED Lighting Solutions, Intelligent Lighting Controls)

-

Sharp Corporation (Optical Sensors, LEDs)

-

Fujitsu Limited (Optoelectronic Components, Laser Diodes)

-

Others

Recent Development

-

(August 12, 2024): Indian Opto-semiconductor maker Polymatech has acquired a US-based semiconductor equipment provider specializing in packaging and testing. This strategic acquisition is aimed at establishing an integrated chipmaking business that encompasses various sectors. Additionally, Tata has commenced the construction of its first integrated circuit (IC) backend facility in Assam, marking a significant step in India's semiconductor manufacturing capabilities.

-

(September 16, 2024): Polymatech, based in Chennai, is set to establish a semiconductor unit in Bahrain, expanding its Opto-semiconductor footprint. Specializing in Opto-semiconductor chips for LEDs, lasers, and photodetectors, the company is now shifting its focus to power semiconductors and data transmission technologies, including 5G and 6G chips, following its recent acquisition of a California-based firm.

-

Recent Development (August 12, 2024): Intel's telecommunications division faces significant cost cuts following disappointing financial results, as its telecom networks business was largely overlooked in the earnings report. Analysts are concerned that many telecom operators doubt Intel's General Purpose Processing (GPP) approach, which may lead to substantial impacts from these reductions.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 56.78 Billion |

| Market Size by 2032 | USD 154.39 Billion |

| CAGR | CAGR of 11.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (LED and Li-Fi Equipment, Image Sensors, Infrared Component, Optocouplers, Laser Diode, Optical down converters, Laser Levelling and Gyroscopes, Others) • By Application (Consumer Electronics, Information Processing and Telecommunications, Automotive Applications, Industrial, Medical Application, Aerospace & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Samsung Electronics Co., Ltd., Sony Corporation, Osram Licht AG, Broadcom Inc., ON Semiconductor Corporation, Vishay Intertechnology, Inc., ROHM Semiconductor, Cree, Inc. (Wolfspeed), Lumentum Holdings Inc., AMS AG, Nichia Corporation, Infineon Technologies AG, Toshiba Corporation, Renesas Electronics Corporation, II-VI Incorporated, Lite-On Technology Corporation, Panasonic Corporation, Acuity Brands, Inc., Sharp Corporation, and Fujitsu Limited,& others. |

| Key Drivers | • Changing the Impact of UV-C Technology on Health and Safety in the Opto Semiconductors Market • The Increasing Popularity of Optoelectronics Manufacturing Services Outsourcing |

| RESTRAINTS | • Challenges in Testing Thermal and Physical Aspects of Optoelectronic Integration |

Frequently Asked Questions

Major players in the opto semiconductors market include OSRAM Opto Semiconductors, Cree, Broadcom, ON Semiconductor, Vishay Intertechnology, Samsung Electronics, Nichia Corporation, Sony, Sharp Corporation, and Toshiba, driving innovations in optoelectronics.

Major types of opto semiconductors include Light-Emitting Diodes (LEDs), laser diodes, infrared sensors, photodiodes, and optical communication devices, all of which play critical roles in modern electronics and telecommunications.

Key industries include automotive (for lighting and sensing applications), telecommunications (fiber optics and data transmission), consumer electronics (LEDs and sensors), and healthcare (medical imaging and diagnostic devices).

Ans: The Opto Semiconductors Market Size to grow at a CAGR of 11.8% over the forecast period 2024-2032.

Ans: The Opto Semiconductors Market Size was valued at USD 56.78 billion in 2023 and is expected to reach USD 154.39 billion by 2032.

Get in Touch