Organic Substrate Packaging Materials Market Report Scope & Overview:

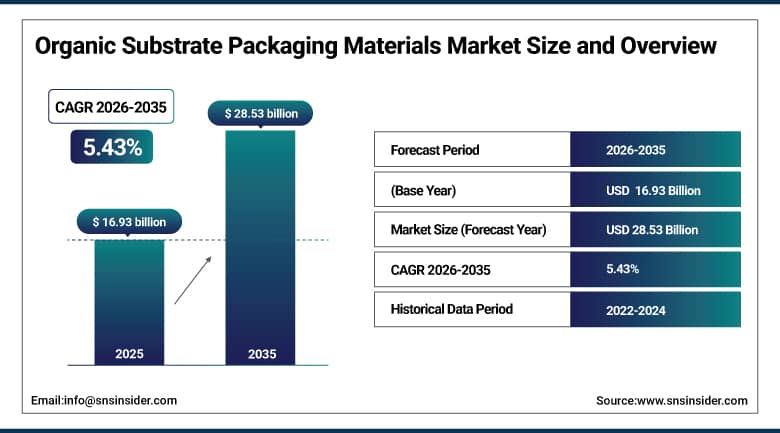

The Organic Substrate Packaging Materials Market size is valued at USD 16.93 Billion in 2025 and is projected to reach USD 28.53 Billion by 2035, growing at a CAGR of 5.43% during the forecast period 2026–2035.

The Organic Substrate Packaging Materials Market analysis report offers a comprehensive analysis of market dynamics, technology, and applications. The rising demand for miniature electronic devices, increased use in automotive electronics and electric vehicles, reliance on artificial intelligence and high-performance computing semiconductors, and development of Asian Pacific manufacturing bases are contributing to robust growth in the market from 2026-2035.

Demand for organic substrate packaging materials exceeded 1.2 million tons in 2025, fueled by the rise of sustainable electronics and eco-friendly semiconductor manufacturing practices.

Market Size and Forecast:

-

Market Size in 2025: USD 16.93 Billion

-

Market Size by 2035: USD 28.53 Billion

-

CAGR: 5.43% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Organic Substrate Packaging Materials Market - Request Free Sample Report

Organic Substrate Packaging Materials Market Trends:

-

EVs, ADAS, and infotainment systems are driving the fastest-growing application segment.

-

Polyimide substrates are gaining popularity due to flexibility and miniaturization requirements, and BT resin is the dominant material used.

-

Increased demand for eco-friendly, recyclable substrates that comply with global green regulations.

-

Expansion in GA and SO packages for AI, HPC, and 5G applications.

-

High dependence on Asian manufacturing, which is a geopolitical risk factor.

-

Increased demand for thinner, lighter substrates for wearable electronics and IoT devices.

-

Specialized substrates are needed for medical and defence electronics, which require high reliability.

U.S. Organic Substrate Packaging Materials Market Insights:

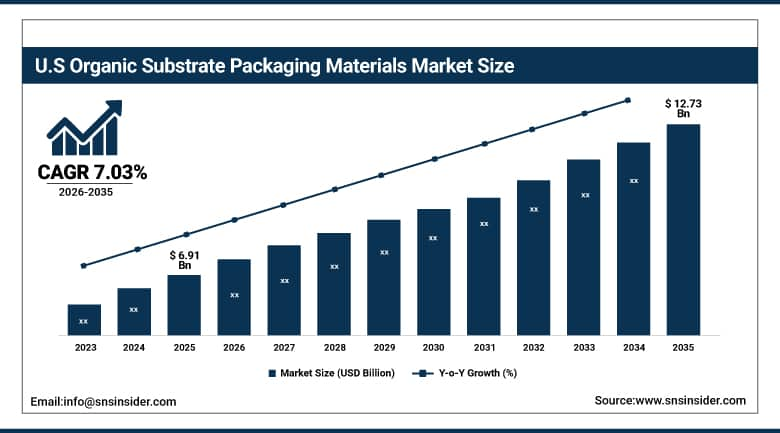

The US Organic Substrate Packaging Materials Market is expected to grow from USD 6.91 Billion in 2025 to USD 12.73 Billion by 2035 at a CAGR of 7.03%. The market growth is fueled by the increasing demand for advanced semiconductor packaging solutions, growing demand for organic substrate packaging solutions in the automotive segment and EVs, high penetration of organic substrate packaging solutions in AI, HPC, and 5G applications, and increasing investment in innovative organic substrate technologies.

Organic Substrate Packaging Materials Market Growth Drivers:

-

Rising demand for miniaturized and high-performance electronics is driving adoption of advanced organic substrate packaging materials.

The growing demand for AI-based semiconductors, 5G devices, and automotive electronic products is also driving the growth of the organic substrates market. Semiconductor material suppliers, consumer electronic device manufacturers, and automotive electronic system suppliers are using organic substrates such as BT resin, polyimide, and epoxy for high-density wiring, improved thermal management, and high-performance capabilities in compact electronic products.

More than 58% of semiconductor and electronic device manufacturers have adopted advanced organic substrate packaging materials for next-generation consumer electronic products, automotive electronic products, and AI-based electronic products in 2025.

Organic Substrate Packaging Materials Market Restraints:

-

High manufacturing costs and supply chain vulnerabilities are restraining the growth of organic substrate packaging materials.

Reliance on Asian production centers, combined with escalating raw material costs for BT Resin, PI, and Epoxy, are key issues that need to be addressed for market growth. Raw material costs for semiconductor and electronics manufacturers are a challenge, which also affects the overall scalability of the industry, depending on Asian sources. Competition from inorganic substrates, such as ceramics and metals, combined with the complexity of advanced packaging technologies, also requires substantial R&D investments, which slows market adoption for smaller industry players.

More than 42% of semiconductor and electronics manufacturers experienced production delays in 2025 due to raw material shortages, escalating raw material costs, and supply chain issues.

Organic Substrate Packaging Materials Opprtunities:

-

Expanding demand for advanced packaging in AI, HPC, and 5G applications is creating significant opportunities for organic substrate materials.

The rapid development of electric vehicles, autonomous driving systems, and wearable electronics is creating new opportunities for organic substrates such as polyimide and BT resin for miniaturization, wiring density, and thermal management. Semiconductor and electronics companies are investing in chiplet architectures, heterogeneous integration, and green substrate innovations. Organic substrates are becoming key enablers for next-generation semiconductor and electronics innovations.

More than 65% of leading semiconductor and electronics companies announced new investments in organic substrate packaging technologies in 2025.

Organic Substrate Packaging Materials Market Segmentation Analysis:

-

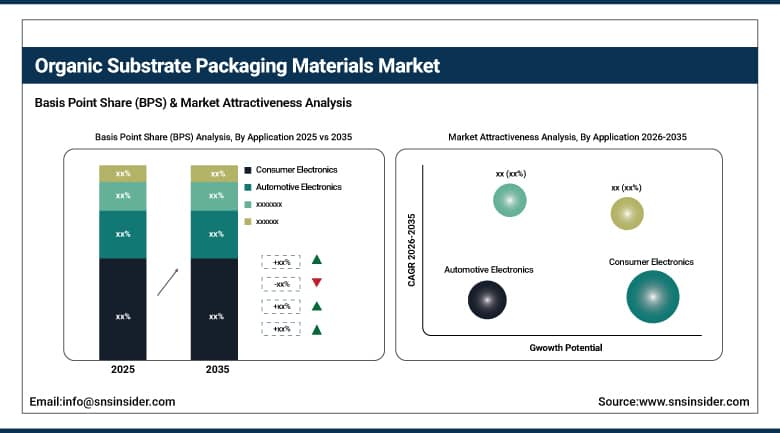

By Application, Consumer Electronics held the largest market share of 41.46% in 2025, while Automotive Electronics are expected to grow at the fastest CAGR of 6.64% during 2026–2035.

-

By Technology, SO Packages (Small Outline) dominated with 43.55% market share in 2025, whereas GA Packages (Grid Array) are projected to record the fastest CAGR of 5.56% through 2026–2035.

-

By Material Type, BT (Bismaleimide-Triazine) Resin Substrates accounted for the highest market share of 44.72% in 2025, while Polyimide Substrates are expected to grow at the fastest CAGR of 6.38% during the forecast period.

-

By End-User Industry, Semiconductors & Electronics Manufacturing held the largest share of 48.72% in 2025, while Automotive & Transportation are expected to grow at the fastest CAGR of 7.38% during the forecast period.

By Application Consumer Electronics Dominate While Automotive Electronics Grow Rapidly:

Consumer Electronics accounted for a dominant share in the organic substrate packaging materials market due to their increased usage in smartphones, laptops, tablets, and wearables. This segment also benefits from high-volume production, constant innovation in miniaturization, and the need for efficient packaging solutions that enable miniaturization.

Automotive Electronics is another segment that is growing at a fast pace due to the increased demand for electric vehicles, ADAS systems, and infotainment systems in cars. The need for efficient packaging solutions for automotive products is driving the growth of this segment, which is likely to become a growth engine for the future.

By Technology, SO Packages (Small Outline) Dominate While GA Packages (Grid Array) Grow Rapidly:

SO Packages (Small Outline) had the dominant share in the organic substrate packaging materials market mainly due to their cost-effectiveness and suitability for smaller consumer devices such as smartphones, tablets, and laptops. Their reliability and scalability for high-volume production lines have been well established for manufacturers seeking a balance between performance and cost-effectiveness.

GA Packages (Grid Array) are the fastest-growing segment of the organic substrate packaging materials market due to the increasing need for AI, HPC, and 5G applications. Their capacity for handling increased input/output density and high-performance requirements is fueling their growth, especially for next-generation semiconductor packaging.

By Material Type, BT (Bismaleimide-Triazine) Resin Substrates Dominate While Polyimide Substrates Grow Rapidly:

BT (Bismaleimide-Triazine) Resin Substrates were the most dominantly used organic substrate packaging materials, and the reason for this was the excellent thermal, mechanical, and reliability properties of these substrates, especially for integrated circuit packages. The excellent high-temperature properties of BT Resin Substrates, along with their dimensional stability, have made these materials the preferred choice for the development of high-performance electronics, including consumer electronics, AI chips, and computing systems.

Polyimide Substrates are the fastest-growing type of substrate materials, and the reason for this is the flexible and lightweight properties of these materials, which are ideal for the development of miniaturized and wearable electronics. The growing trend of consumers preferring to use lighter and thinner electronics has helped these substrates to emerge as the preferred choice for the development of innovative electronics.

By End User, Semiconductors & Electronics Manufacturing Dominate While Automotive & Transportation Grow Rapidly:

Semiconductors & Electronics Manufacturing held the diminant share in the market due to the high adoption rate of organic substrates in IC packaging, AI chips, and consumer products. This segment is considered the backbone of the industry.

Automotive & Transportation is the fastest-growing segment in the market due to the increased rate of electric vehicles and the development of autonomous driving solutions. The increased demand for automotive electronic packaging solutions is driving growth in the industry.

Organic Substrate Packaging Materials Market Regional Analysis:

Asia-Pacific Organic Substrate Packaging Materials Market Insights:

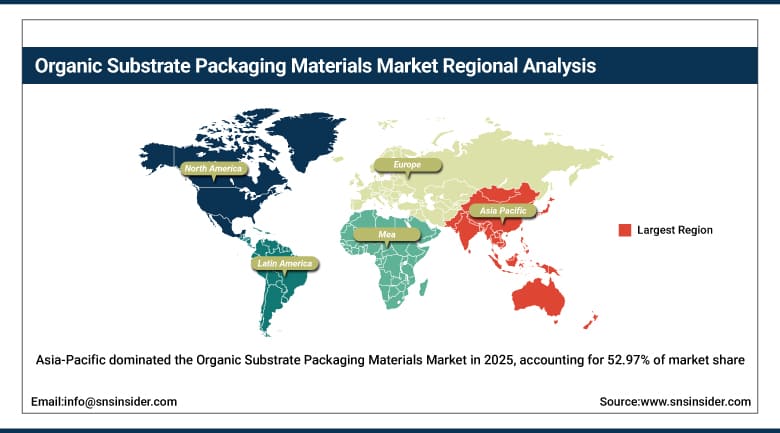

Asia-Pacific holds the largest share in the organic substrate packaging materials market with a share of 52.97%, followed by the fastest growth rate of 6.08%. Countries such as Taiwan, South Korea, Japan, and China have become a hub for semiconductor packaging with high demand for consumer electronic products, rapid industrialization, and government initiatives to strengthen local supply chains. The Asia-Pacific region has access to large-scale manufacturing capabilities, high-end research and development capabilities, and industry players such as ASE Group, Kyocera, and Samsung Electro-Mechanics.

Get Customized Report as Per Your Business Requirement - Enquiry Now

China Organic Substrate Packaging Materials Market Insights:

China is a key player in the Asia-Pacific region, driven by its large consumer electronics market, growing automotive space, and strategic investments in semiconductor packaging. The country is growing its domestic production capacity to decrease its reliance on imports while promoting innovation around advanced packaging technologies including chiplet integration and high-density wiring boards. With high government support and growing demand for AI chipsets, EV components, and 5G devices, China is both a major contributor and a growth engine for the Asia-Pacific region.

North America Organic Substrate Packaging Materials Market Insights:

The North America Organic Substrate Packaging Materials Market is a dominant market, backed by strong semiconductor manufacturing capabilities and electronics industry requirements in the US and Canada. Organic substrate packaging material market growth is driven by the widespread use of organic substrate packaging materials in consumer electronics, automotive electronics, and AI devices. The region has a strong industry base, continuous R&D activities, and government initiatives supporting domestic semiconductor manufacturing, which keeps this market in a dominant position. This region has strong associations between tech companies and OEMs, which keeps the market for organic substrate packaging materials strong.

U.S. Organic Substrate Packaging Materials Market Insights

The U.S. Organic Substrate Packaging Materials Market is influenced by the presence of a strong semiconductor industry, high demand for consumer electronics, and the increasing adoption of advanced packaging technologies. Organic substrate packaging material market growth is driven by the widespread use of organic substrate packaging materials in consumer electronics, automotive electronics, and AI devices. The increasing rate of innovation in chiplet integration, heterogeneous packaging, and eco-friendly substrate materials has also helped the U.S. Organic Substrate Packaging Materials Market to thrive.

Europe Organic Substrate Packaging Materials Market Insights:

Europe’s organic substrate packaging market is driven by strong market opportunities in automotive electronics, industrial automation, and aerospace segments. Countries such as Germany, France, and the UK are investing considerably in semiconductor packaging technologies to fuel EV markets and advanced manufacturing capabilities. Sustainability is a key factor for the region, with a focus on “green” materials that align with stringent environmental regulations. R&D collaborations, semiconductor independence initiatives, and associations between tech industry players and OEMs in the auto sector contribute to Europe’s position as a key market, albeit a smaller market compared to the APAC and North American markets.

Germany Organic Substrate Packaging Materials Market Insights:

Germany is the largest market in Europe, driven by the leadership of the automotive industry and its focus on integrating advanced electronics. Investments in EVs, autonomous driving technologies, and industrial automation are boosting the market for advanced organic substrates in Germany. Investments in EVs, autonomous driving technologies, and industrial automation are boosting the market for advanced organic substrates in Germany. The presence of strong R&D capabilities, semiconductor industry collaborations with the automotive industry, and government initiatives for innovation make Germany a critical market for shaping the competitiveness of Europe in the organic substrate packaging materials market.

Latin America Organic Substrate Packaging Materials Market Insights:

The Latin America organic substrate packaging materials market is in the developing phase, driven by the increasing rate of adoption of consumer electronics, the growing automotive sector, and the increasing rate of investment in semiconductor packaging materials. The countries that are contributing to the growth of the Latin America organic substrate packaging materials market are Brazil and Mexico, where the increasing rate of smartphone adoption, industrial automation, and the increasing rate of adoption of electric vehicles are key factors contributing to the growth of the market.

Middle East & Africa Organic Substrate Packaging Materials Market Insights:

The Middle East & Africa Organic Substrate Packaging Materials Market is a developing market, driven by the growing consumer electronics industry, increased automotive market needs, and steady investments in semiconductor packaging technologies. The UAE, Saudi Arabia, and South Africa are some of the key markets for the Middle East & Africa Organic Substrate Packaging Materials Market, driven by factors such as increased smartphone penetrations, industrial automation, and government initiatives for economic diversification through technological advancements.

Organic Substrate Packaging Materials Market Competitive Landscape:

Amkor Technology Inc. is a US-based company specializing in semiconductor packaging and test services. The company boasts a vast selection, exceeding 3,000 packaging formats. These encompass flip chip, wafer-level packaging, and 3D packaging technologies. The company prides itself on its high-volume manufacturing excellence and cutting-edge technologies such as its S-SWIFT chiplet integration solution and its S-Connect solution for enhanced signal integrity. Amkor's reach spans the globe, with facilities in Asia, EMEA, and the United States, bolstering the semiconductor industry as a whole. Amkor's strategy on laminate and organic substrates makes it a key enabler for consumer electronics, automotive, and AI chip suppliers.

-

In June 2025, Amkor opened a new advanced packaging and test facility in the U.S., strengthening domestic semiconductor supply chain resilience.

ASE Group, based in Taiwan, is the world’s largest semiconductor packaging and test service provider. ASE is a pioneer in heterogeneous integration (HI) and system-in-package (SiP) technologies, which are required for increased functionality, performance, and connectivity in modern electronic systems. ASE helps in accelerating AI innovation through heterogeneous integration of several ASICs and silicon bridges, making it a significant player in AI, HPC, and 5G. ASE is ASE, SPIL, and USI under ASE Technology Holding, providing unparalleled expertise in advanced packaging.

-

In March 2025, ASE broke ground on a new high-tech facility in Kaohsiung, investing NT$17.8 billion to meet growing AI chip demand.

Kyocera Corporation, a Japan-based company, is a leader in organic packages and printed wiring boards. The company provides total solutions from design, manufacturing, and quality assurance. The company's product portfolio consists of FC-BGA, FC-CSP substrates, and thin-type module substrates. The company utilizes its expertise in high-density wiring board technology, which provides cost performance and reliability. The company also focuses on sustainability, which helps build a decarbonized society through eco-friendly packaging.

-

In November 2025, Kyocera expanded its organic package product line to support next-generation automotive and communication technologies.

Organic Substrate Packaging Materials Market Key Players:

-

Amkor Technology Inc.

-

ASE Group (Advanced Semiconductor Engineering)

-

Kyocera Corporation

-

Shinko Electric Industries Co., Ltd.

-

Ibiden Co., Ltd.

-

Unimicron Technology Corp.

-

Nan Ya Printed Circuit Board Corp.

-

Daeduck Electronics Co., Ltd.

-

Kinsus Interconnect Technology Corp.

-

Samsung Electro-Mechanics Co., Ltd.

-

LG Innotek Co., Ltd.

-

Toppan Printing Co., Ltd.

-

Simmtech Co., Ltd.

-

Shennan Circuits Co., Ltd.

-

WUS Printed Circuit Co., Ltd.

-

Fujitsu Interconnect Technologies Ltd.

-

Nitto Denko Corporation

-

Microchip Technology Inc.

-

Texas Instruments Incorporated

-

Murata Manufacturing Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.93 Billion |

| Market Size by 2035 | USD 28.53 Billion |

| CAGR | CAGR of 5.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Consumer Electronics, Automotive Electronics, Industrial Electronics, Others) • By Technology (SO Packages (Small Outline), GA Packages (Grid Array), Flat No-Leads Packages, Others) • By Material Type (BT (Bismaleimide-Triazine) Resin Substrates, Polyimide Substrates, Epoxy Resin Substrates, Others) • By End-User Industry (Semiconductors & Electronics Manufacturing, Automotive & Transportation, Industrial & Automation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amkor Technology, ASE Group, Kyocera Corporation, Samsung Electro-Mechanics, Shinko Electric Industries, Ibiden Co. Ltd., Sumitomo Bakelite Co. Ltd., Mitsui Chemicals, Nitto Denko Corporation, Panasonic Holdings Corporation, Toppan Printing Co. Ltd., Unimicron Technology Corp., Nan Ya Printed Circuit Board Corp., Kinsus Interconnect Technology Corp., Daeduck Electronics Co. Ltd., LG Innotek, Simmtech Co. Ltd., Shennan Circuits Co. Ltd., WUS Printed Circuit Co. Ltd., Zhen Ding Technology Holding Limited. |

Frequently Asked Questions

The main challenges include high manufacturing costs, competition from inorganic substrates (ceramics), and supply chain vulnerabilities due to heavy reliance on Asia-Pacific production hubs.

Automotive electronics is the fastest-growing application segment, with a CAGR of 6.64%, fuelled by electric vehicles, autonomous driving, and infotainment systems.

Asia-Pacific leads the market with 52.97% share, driven by strong semiconductor packaging industries in China, Taiwan, South Korea, and Japan. It is also the fastest-growing region with a CAGR of 6.08%.

The largest demand comes from consumer electronics (smartphones, laptops, wearables), followed by automotive electronics (EVs, ADAS systems), and semiconductors for AI/HPC applications.

Organic substrate packaging materials are resin-based substrates (such as BT resin, polyimide, and epoxy) used in semiconductor packaging to provide mechanical support, electrical connections, and thermal management for integrated circuits.

Get in Touch