Oxygen Concentrator Market Report Scope & Overview:

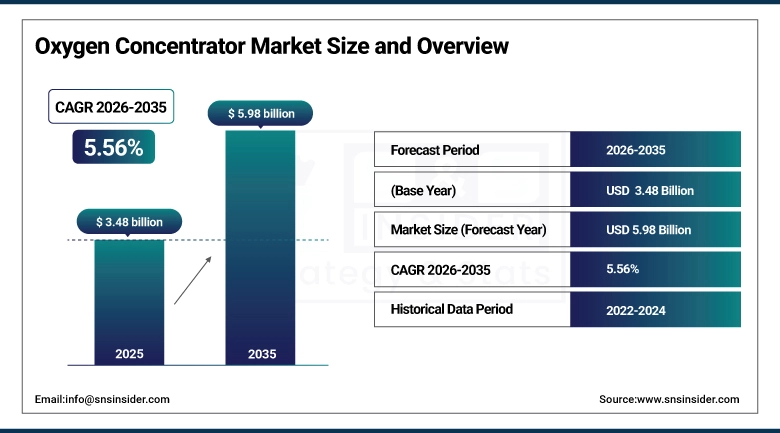

The Oxygen Concentrator Market was valued at USD 3.48 billion in 2025 and is expected to reach USD 5.98 billion by 2035, growing at a CAGR of 5.56% from 2026-2035.

Oxygen Concentrators market is predicted to witness high growth owing to increasing prevalence of chronic respiratory diseases including COPD and asthma, and surging demand for home oxygen therapy. The expanding market revenue is also driven by advancements in concentrator portability and the increasing aging global population. With an encouraging reimbursement trend and a favorable healthcare environment, particularly in emerging economies, adoption is on the rise. Continued focus on non-invasive respiratory support and rising levels of awareness are contributing to growth. Manufacturers are targeting residual flow, pulse flow, and continuous flow technology which enables maximization of the treatment amount given by a device using reduced levels of energy along with making it lightweight and user-friendly features for battery conservation.

According to industry data, the home care segment dominated the oxygen concentrator market with a 62.8% market share in 2025 due to the widespread preference to treat chronic respiratory diseases at home, driven by patient comfort, cost-effectiveness, and government initiatives promoting outpatient care.

Oxygen Concentrator Market Size and Forecast

-

Market Size in 2025: USD 3.48 Billion

-

Market Size by 2035: USD 5.98 Billion

-

CAGR: 5.56% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2032

-

Historical Data: 2022-2024

To Get more information on Oxygen Concentrator Market - Request Free Sample Report

Oxygen Concentrator Market Trends:

-

Rising adoption of portable oxygen concentrators (POCs) driven by patient preference for mobility, independence, and travel-friendly respiratory therapy without reliance on heavy oxygen cylinders.

-

Integration of smart connectivity features including Bluetooth, Wi-Fi, and remote monitoring capabilities enabling caregivers and clinicians to track patient oxygen levels and device performance in real-time.

-

Growing development of dual-mode oxygen concentrators that combine continuous flow and pulse flow delivery modes, offering broader prescription flexibility across diverse patient needs and activity levels.

-

Increasing focus on energy-efficient concentrator designs using advanced sieve bed materials and compressor technologies to reduce power consumption and improve device longevity in home care settings.

-

Expanding home oxygen therapy programs supported by Medicare and private insurance reimbursements, encouraging patients with COPD, asthma, and pulmonary fibrosis to choose home-based care over hospitalization.

-

Rising investment by manufacturers in AI-enabled respiratory monitoring platforms that integrate with oxygen concentrators to provide adaptive oxygen delivery based on real-time patient activity and SpO2 levels.

-

Growing adoption of oxygen concentrators in emerging economies driven by improving healthcare infrastructure, increasing awareness of respiratory conditions, and government-backed oxygen therapy programs.

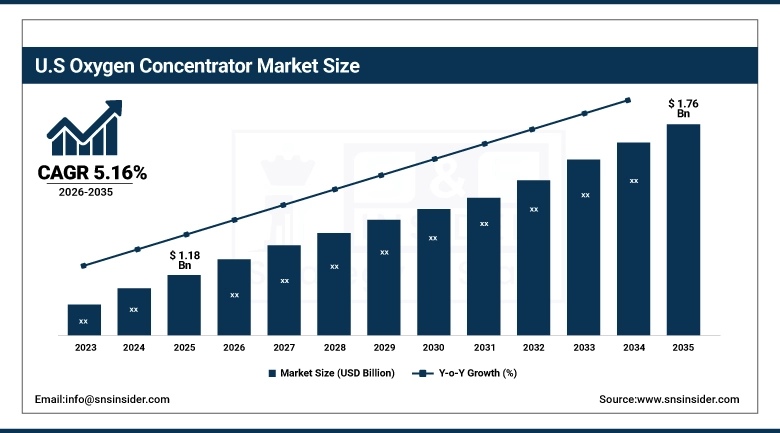

The U.S. Oxygen Concentrator Market was valued at USD 1.18 billion in 2025 and is expected to reach USD 1.76 billion by 2035, registering a CAGR of 5.16% during 2026-2035.

North America Oxygen Concentrator Market Analysis By Country The leading share of the North America oxygen concentrator market is held by the United States market due to the existence of a high standard healthcare system and increased awareness levels regarding respiratory disorders and demand for home use oxygen therapy. The high prevalence of chronic respiratory diseases such as COPD and asthma in the elderly population, availability of large manufacturers providing medical devices, strong reimbursement policies and rapid technological advancements are some factors allowing a high adoption of portable oxygen concentrators, and fixed oxygen concentrators.

In October 2024, Inogen released its Rove 4 Portable Oxygen Concentrator, delivering the highest oxygen output in the lightest weight 4-setting POC available in the U.S.

The U.S. Federal Aviation Administration and Department of Transportation continue to relax regulations on in-flight use of portable oxygen concentrators, opening new travel-related demand segments and reinforcing POC adoption among active and ambulatory patients through 2035.

Oxygen Concentrator Market Segment Insights

-

Based on Product, Fixed Medical Oxygen Concentrators accounted for the largest market share (58.14%) in 2025; Portable Medical Oxygen Concentrators expected to be the fastest-growing segment.

-

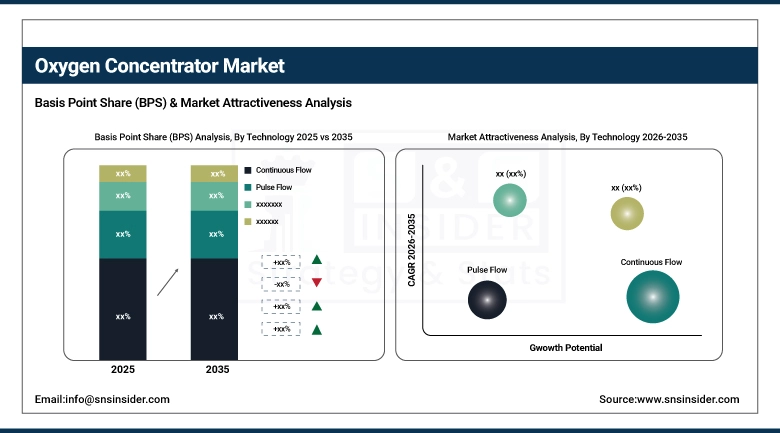

Based on Technology, Continuous Flow accounted for the largest market share (57.16%) in 2025; Pulse Flow expected to be the fastest-growing segment (CAGR of 5.86%).

-

Based on End-Use, Home Care accounted for the largest market share (62.8%) in 2025; Non-Home Care expected to be the fastest-growing segment.

By Technology, Continuous Flow dominates, Pulse Flow expected to grow fastest

The continuous flow segment dominated with approximately 57.16% revenue share in 2025, due to its potential for use in patients who require a constant delivery of oxygen. Continuous flow concentrators are particularly useful in rudimentary ICUs, hospitals and among patients with severe respiratory diseases so that oxygen can be delivered without consideration of breathing patterns. The versatility of their compatibility with CPAP, the supplemental oxygen and other respiratory therapy machines brackets them in a broader spectrum.

The pulse flow segment is expected to grow at the fastest CAGR of 5.86% during 2026-2035. Pulse flow concentrators only provide oxygen during inhalation, greatly improving energy conservation, while the devices themselves are used in ambulatory (moving), active patients with low to moderate respiratory demand. Due to their smaller dimensions and greater battery capacity, they are perfectly adapted for use in motion, on the road or at home in mobile conditions.

By Product, Fixed Medical Oxygen Concentrators dominate, Portable expected to grow fastest

Fixed medical oxygen concentrators accounted for the largest revenue share of approximately 58.14% in 2025. This dominance can be attributed to their widespread use in both clinical and homecare settings for patients needing long-term oxygen therapy. Concentrators are fixed items, and they are common place in hospitals, chronic care residences [1], as well as home care settings, particularly for patients with severe or complicated pulmonary illness. They also provide constant and high-volume oxygen irrespective of the patient's breathing pattern, making them an important component in intensive care readiness alongside Pulmonary rehabilitation centres.

As for the product type, portable medical oxygen concentrators are expected to regret the largest C.A.G.R over the forecast period. Growth in patient demand motion, independence and travel-friendly respiratory home care solutions are rapidly driving United States of America adoption. Devices like the Inogen Rove 4 and Caire IntenOxy 5 represent innovations that, through miniaturization, improved battery technology, and pulse dose delivery capabilities, help ensure patients live active lifestyles while successfully managing their chronic respiratory conditions.

By End-Use, Home Care dominates, Non-Home Care expected to grow fastest

Home care dominated the oxygen concentrator market with approximately 62.8% market share in 2025, owing to the widespread preference for treating chronic respiratory diseases in the comfort of one's home. Strong reimbursement support from Medicare and private insurers, combined with patient preferences for improved quality of life and reduced hospitalization costs, drives home oxygen therapy adoption.

The non-home care segment is projected to be the fastest-growing during the forecast period owing to increasing demand for oxygen therapy in clinical, ambulatory and emergency settings. The growth of this segment is driven by growing hospital admissions for respiratory emergencies, developing healthcare markets in the U.S., and increasing need for ambulatory surgical centers are driving revenue growth.

Oxygen Concentrator Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

39% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

Saudi Arabia |

32% |

|

Latin America |

Brazil |

45% |

North America Oxygen Concentrator Market Insights:

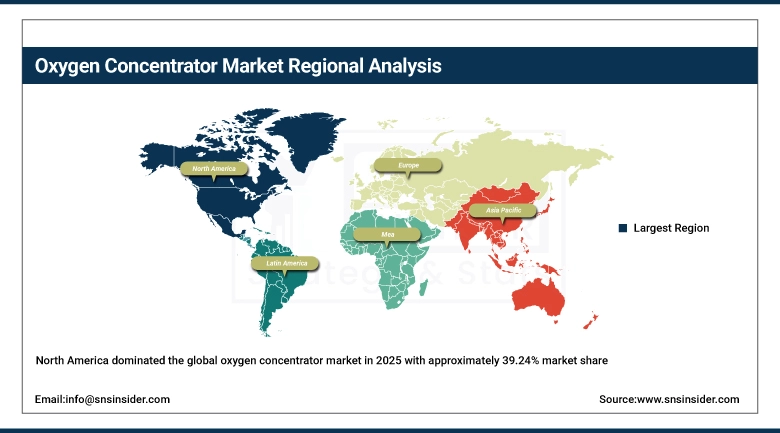

North America dominated the global oxygen concentrator market in 2025 with approximately 39.24% market share attributed to its developed healthcare infrastructure coupled with high awareness levels regarding respiratory disorders and significant demand for home oxygen therapy. The United States, backed by high prevalence of chronic respiratory diseases, advanced Medicare reimbursement frameworks and presence of major medical device manufacturers including Inogen, Philips Respironics and CAIRE Inc.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Oxygen Concentrator Market Insights:

Asia Pacific is the fastest-growing region in the oxygen concentrator market with a 6.20% CAGR over the forecast period, during the forecast period driven by growing healthcare spending, rising awareness towards respiratory care and a large patient pool with significant unmet medical needs. China, India and Japan are growth markets where governments are working towards improving respiratory disease management by investing in home oxygen therapy programs as well as updating their healthcare infrastructures.

Europe Oxygen Concentrator Market Insights:

The global oxygen concentrator market in Europe is primarily dominated by high-income nations with an aging demographic, well-established healthcare facilities, a significant proportion of patients suffering from chronic obstructive pulmonary disease (COPD) and other respiratory disorders; favorable reimbursement policies encourage the purchase of portable/ home devices. European players are also preparing connected oxygen therapy platforms interfacing with the digital health ecosystem.

Middle East & Africa and Latin America Oxygen Concentrator Market Insights:

The Middle East and Africa oxygen concentrator market is experiencing growth due to better healthcare infrastructure, more government programs through which oxygen therapy is being made available in this region along with the rising number of urban populations who are suffering from respiratory diseases like Chronic Obstructive Pulmonary Disease (COPD). In Latin America, Brazil and Mexico spearheaded accelerated prospects for oxygen concentrators during the pandemic era-driven initiatives as strong demand growth for this unit type continues through 2035.

Oxygen Concentrator Market Growth Drivers:

-

Rising Respiratory Disease Burden and Advancements in Smart Oxygen Therapy Accelerating Market Expansion

Growing incidence of chronic respiratory diseases including Chronic Obstructive Pulmonary Disease (COPD), asthma, sleep apnea, and pulmonary fibrosis along with the rapidly growing geriatric population is primarily advocating for oxygen concentrators globally. Long-term oxygen therapy market has witnessed a robust growth due to increasing understanding of air pollution, smoking-related illnesses, occupational respiratory disorders, and post-viral respiratory complications. Concentrators with portability and home use will witness high demand due to a shift in healthcare systems focusing on driving down costs associated with hospital admissions and more focus on the comfort of the patient at home. Next-gen portable concentrator Importantly, the quality of these technologies including AI-enabled adaptive oxygen delivery systems and IoT-connected remote patient monitoring with mobile brand app integration, quieter operation, lightweight designs, and longer battery life is what is transforming next-generation portable oxygen concentrators into both high performers in providing therapy as well as great companions for patients. Such innovations enable patients to better manage chronic respiratory diseases while remaining mobile and independent, and will underpin organic market expansion through 2035.

Oxygen Concentrator Market Restraints

-

High Device Costs and Limited Accessibility in Developing Regions Hindering Wider Adoption

Despite strong market growth potential, the oxygen concentrator market faces several restraints related to high equipment costs, accessibility limitations, and operational challenges. Advanced battery systems, artificial intelligence monitoring capabilities, and compact lightweight designs of the premium portable oxygen concentrators make them a costly affair for patients in low-income as well as price-sensitive regions. But the widespread adoption of LTOT is prevented by inadequate healthcare infrastructure, limited reimbursement, frequent electricity cuts and lack of awareness regarding important features of LTOT in many developing countries and rural set up. Furthermore, the necessity for maintenance, regular filter replacements, and servicing add to the overall cost burden on patients and healthcare providers. These include product recalls, reliability issues with devices, oxygen purity variation, and regulatory compliance challenges which also adversely affect consumer confidence thereby increasing the overall purchasing time. All of these factors together pose obstacles for the widespread adoption of sophisticated oxygen concentrators, especially in low- to middle-income countries with limited budgets for healthcare.

Oxygen Concentrator Market Opportunities

-

Expansion of Home Healthcare and AI-Connected Respiratory Monitoring Creating Future Growth Potential

The oxygen concentrator market will experience significant growth opportunities due to factors such as growing reach of home healthcare services, increased telemedicine adoption, and rising investments in establishing digital respiratory care infrastructure across emerging economies. The government and healthcare organizations are promoting home oxygen therapy programs to reduce hospital over-crowding, lower long-term treatment costs further supporting the adoption of portable and stationary oxygen concentrators. Increasing use of telehealth platforms integrated with connected oxygen concentrators allows physicians and caregivers to significantly come through the remote monitoring of real-time vitals such as oxygen saturation level, therapy adherence and device performance so that improved patient care can be delivered avoiding emergency hospital visits. Additionally, some growth areas for manufacturers are propelled by improvements in algorithms related to AI-enabled oxygen flow optimization systems the advent of compact wearable concentrator technologies; energy-efficient design and cloud-based respiratory data analytic solutions.

Recent Developments:

-

2025 (June): Inogen, Inc. introduced the Voxi 5 Stationary Oxygen Concentrator, offering an affordable, durable, and quiet continuous flow oxygen therapy solution for long-term care patients in the U.S., with a 3-year sieve bed warranty.

-

2025 (January): CAIRE Inc. launched the IntenOxy 5 stationary oxygen concentrator in the U.S. and Puerto Rico, delivering approximately 95.5% oxygen concentration with flow settings from 0.5 to 5 LPM and low power consumption.

-

2024 (October): Inogen, Inc. released the Rove 4 Portable Oxygen Concentrator, delivering the highest oxygen output in the lightest weight 4-setting POC using Inogen's patented pulse-dose Intelligent Delivery Technology.

-

2024 (March): Drive DeVilbiss Healthcare, in collaboration with Sanrai International, unveiled the PulmO2 10 L Oxygen Concentrator for underpenetrated healthcare markets, emphasizing durability and long-duration oxygen delivery.

-

2023 (January): Inogen, Inc. received European Medical Device Regulation (EU MDR) approval from BSI for the Inogen One G4 and Inogen One G5 portable oxygen concentrators, expanding European market access.

Oxygen Concentrator Market Key Players:

-

Inogen, Inc.

-

Philips Respironics

-

CAIRE Inc.

-

Invacare Corporation

-

Drive DeVilbiss Healthcare

-

Nidek Medical Products, Inc.

-

O2 Concepts

-

GCE Group

-

Teijin Limited

-

Chart Industries

-

ResMed Inc.

-

React Health

-

Precision Medical Inc.

-

OMRON Healthcare

-

Longfian Scitech Co., Ltd.

-

Oxymat A/S

-

DeVilbiss Healthcare LLC

-

Medical Depot, Inc.

-

Koninklijke Philips N.V.

-

Yuwell (Jiangsu Yuyue Medical)

Oxygen Concentrator Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.48 Billion |

| Market Size by 2035 | USD 5.98 Billion |

| CAGR | CAGR of 5.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Fixed Medical Oxygen Concentrators, Portable Medical Oxygen Concentrators) • By Technology (Continuous Flow, Pulse Flow) • By End-Use (Home Care, Non-Home Care) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Inogen, Inc., Philips Respironics, CAIRE Inc., Invacare Corporation, Drive DeVilbiss Healthcare, Nidek Medical Products, Inc., O2 Concepts, GCE Group, Teijin Limited, Chart Industries, ResMed Inc., React Health, Precision Medical Inc., OMRON Healthcare, Longfian Scitech Co., Ltd., Oxymat A/S, DeVilbiss Healthcare LLC, Medical Depot, Inc., Koninklijke Philips N.V., Yuwell (Jiangsu Yuyue Medical) |

Frequently Asked Questions

Ans: The Oxygen Concentrator Market is expected to grow at a CAGR of 5.56% from 2026 to 2035.

Ans: Increasing incidence of chronic respiratory disorders including COPD and asthma combined with a growing aging population, rising preference for home-based oxygen therapy, and advances in portable concentrator technology is the primary driver of sustained market growth through 2035.

Ans: The Fixed Medical Oxygen Concentrators segment dominated the Oxygen Concentrator Market in 2025, accounting for approximately 58.14% of global revenue, owing to its extensive clinical and homecare application for patients requiring long-term continuous oxygen therapy.

Ans: The Continuous Flow segment dominated the Oxygen Concentrator Market in 2025 with approximately 57.16% revenue share, driven by its widespread application in intensive care, hospital, and home care settings requiring uninterrupted oxygen delivery.

Ans: North America dominated the Oxygen Concentrator Market in 2025, accounting for approximately 39.24% of global market revenue, driven by advanced healthcare infrastructure, strong insurance reimbursement for home oxygen therapy, and high awareness of chronic respiratory disorders.

Get in Touch