Battery Recycling Market Report Scope & Overview:

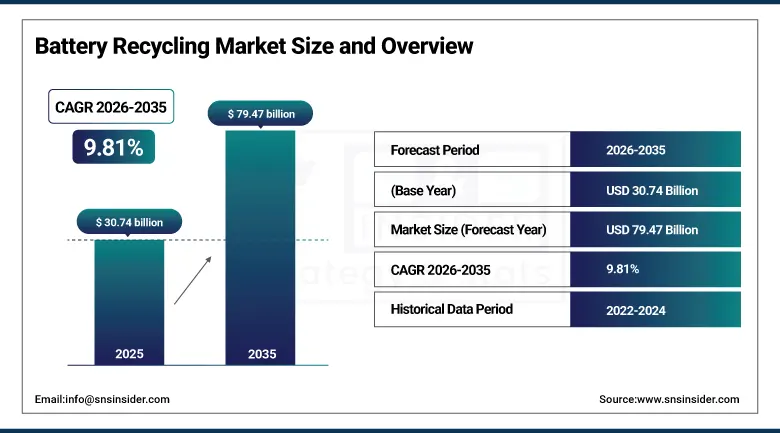

The Battery Recycling Market size was valued at USD 30.74 billion in 2025 and is expected to reach USD 79.47 billion by 2035, growing at a CAGR of 9.81% from 2026-2035.

Battery Recycling Market growth factors include increased use of electric vehicles, high demand for crucial metals including lithium, cobalt, and nickel, as well as stringent environmental policies that encourage circular economy approaches. Further, development in recycling technology and increased investments from companies such as Redwood Materials and Li-Cycle contribute towards expansion of capacity. Moreover, increasing e-waste generation and reduced reliance on virgin materials play a crucial role in market expansion.

The U.S. Department of Energy's ReCell Center has invested over USD 200 million in battery recycling research to develop direct recycling processes that recover cathode materials at up to 50% lower cost than conventional pyrometallurgical routes. The EU Battery Regulation mandates minimum recycled content of 6% for lithium, 26% for cobalt, 12% for nickel, and 85% for lead in new batteries by 2031.

Market Size and Forecast

-

Market Size in 2025: USD 30.74 Billion

-

Market Size by 2035: USD 79.47 Billion

-

CAGR: 9.81% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Battery Recycling Market - Request Free Sample Report

Battery Recycling Market Trends

-

Rising adoption of electric vehicles and energy storage systems is driving the battery recycling industry.

-

Growing concerns over environmental impact and hazardous waste management are boosting market growth.

-

Expansion of lithium-ion battery usage across automotive, electronics, and industrial sectors is fueling recycling demand.

-

Increasing focus on recovering valuable materials such as lithium, cobalt, and nickel is shaping adoption trends.

-

Advancements in hydrometallurgical and pyrometallurgical recycling technologies are enhancing efficiency and yield.

-

Rising government regulations and circular economy initiatives are supporting market expansion.

-

Collaborations between battery manufacturers, recyclers, and automotive companies are accelerating innovation and global adoption.

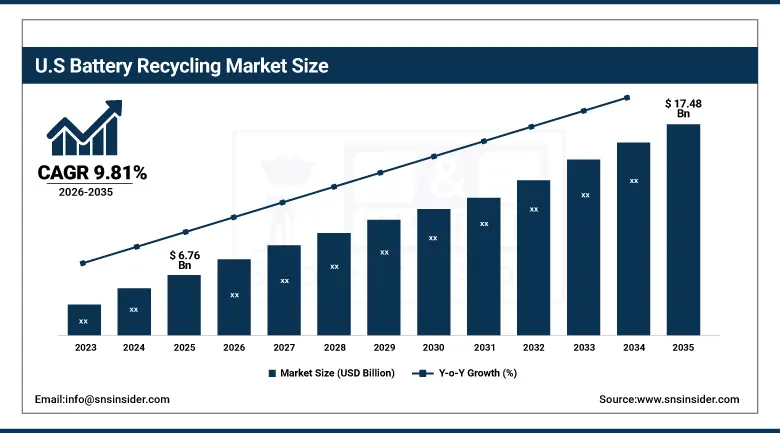

U.S. Battery Recycling Market Size Outlook:

The U.S. Battery Recycling Market was valued at USD 6.76 billion in 2025 and is expected to reach USD 17.48 billion by 2035, growing at a CAGR of 9.81% from 2026-2035. U.S. Battery Recycling Industry Growth Factors include high adoption rate of electric vehicles, environmental concerns, higher e-waste production, and high demand for critical metals like lithium, cobalt, and nickel among others.

The U.S. Department of Energy's Bipartisan Infrastructure Law allocated USD 3 billion for battery manufacturing and recycling projects. The EPA designated lithium-ion batteries as a universal waste under RCRA, streamlining collection and transport regulations that had previously complicated battery recycling logistics across state lines.

Battery Recycling Market Segment Analysis

-

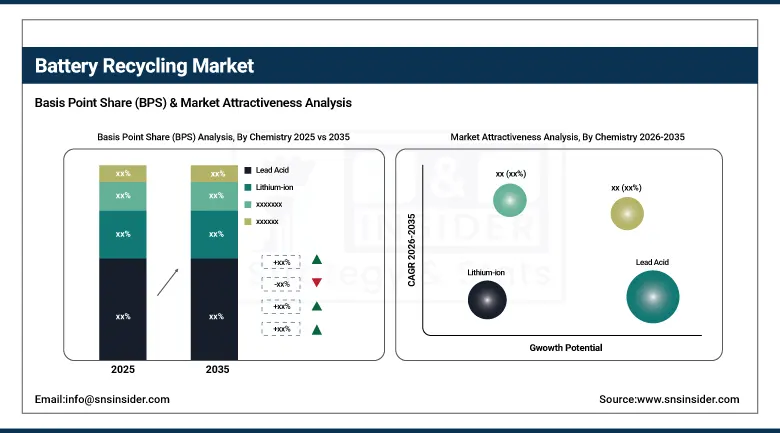

By Chemistry, Lead Acid segment dominated with ~82% share in 2025; Lithium-ion segment fastest growing (CAGR).

-

By Application, Transportation segment dominated with ~70% share in 2025; Consumer Electronics segment fastest growing (CAGR).

-

By Material, Metals segment dominated with ~62% share in 2025; Electrolyte segment fastest growing (CAGR).

By Chemistry, Lead Acid segment dominates the Battery Recycling Market, Lithium-ion expected to grow fastest

Lead acid batteries held over 82% of the Battery Recycling Market in 2023, and this reflects the extraordinarily high recycling rate that lead acid batteries have achieved over decades of established collection and processing infrastructure. In the U.S., Europe, and most developed markets, lead acid battery recycling rates exceed 95% making it one of the most successfully recycled products in the industrial economy. The regulatory requirements, the economic incentive, and the well-established dealer return programs at automotive retailers collectively make lead acid battery recycling a mature, high-volume industrial process that anchors the market's total revenue base.

Lithium-ion battery recycling is growing at the fastest CAGR, fueled by the rapid accumulation of spent lithium-ion batteries from electric vehicles, consumer electronics, and power tools that are reaching end-of-life in growing volumes globally. The economic incentive for lithium-ion recycling is also improving as the value of recoverable cobalt, nickel, and lithium per battery pack increases with battery size and as commodity prices reflect supply scarcity concerns.

By Application, Transportation segment dominates the Battery Recycling Market, Consumer Electronics expected to grow fastest

Transportation dominates the Battery Recycling Industry, owing to the rapid growth of electric vehicles that contribute to the generation of more dead lithium-ion batteries. Lithium, cobalt, and nickel need to be recovered from batteries through recycling processes. The regulatory support received by electric vehicles with regards to their sustainability as well as the production and disposal rates of batteries will continue to make transportation a dominant segment of battery recycling globally.

The consumer electronics segment is growing at fastest rate within the Battery Recycling Market because of the extensive use of portable electronic gadgets such as cell phones, laptops, and wearable tech gadgets. Their short lifecycles make it necessary to dispose of their batteries on a regular basis. Growing awareness about e-waste management and advancements in technology for small battery recycling processes are contributing to its growth.

By Material, Metals segment dominates the Battery Recycling Market, Electrolyte expected to grow fastest

Metal is leading in the Battery Recycling Market because of its economic importance, recoverability, and importance in battery production. The most important metals include lithium, cobalt, nickel, and lead. Efficiently recycling them allows avoiding primary metal extraction, decreasing environmental footprint, and ensuring the security of supply chains. Metals make up the most commercial and established sector in battery recycling processes because of all the benefits mentioned above.

The electrolyte segment is experiencing the fastest growth in the Battery Recycling Industry because of the growing trend of chemical component recovery from lithium-ion batteries. This is possible through technological development, which increases the efficiency of electrolyte extraction and purification for further recycling into new batteries. Moreover, rising demand for batteries stimulates innovations and investments in this field.

Battery Recycling Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

55% |

|

North America |

United States |

82% |

|

Europe |

Germany |

28% |

|

Middle East & Africa |

South Africa |

35% |

|

Latin America |

Brazil |

48% |

Asia Pacific Battery Recycling Market Insights

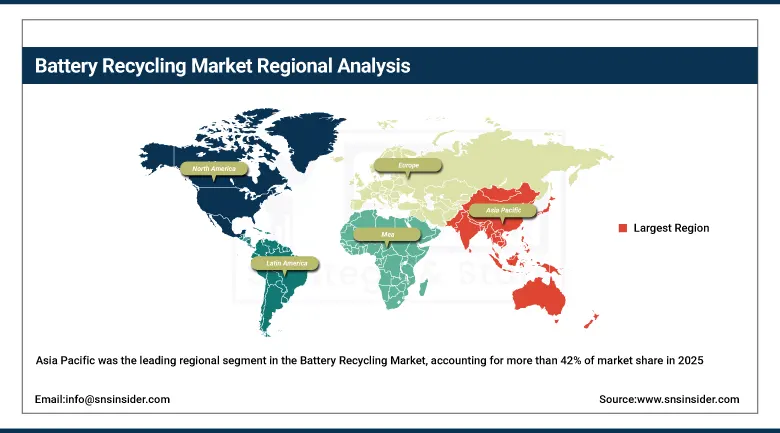

The Asia Pacific was the leading regional segment in the Battery Recycling Market, accounting for more than 42% of market share in 2025. It can be attributed to the fact that the region is both the largest producer of batteries in the world and also consumes batteries the most intensively. China is the biggest manufacturer of batteries and is well-known across the globe for having the best capacities in terms of recycling batteries. In fact, some of the companies in this segment, such as GEM Co, Brunp Recycling, and Hunan Jinkang Greenpower, operate on an enormous scale as compared to their international counterparts. Apart from this, China's government has adopted very stringent laws for battery recycling, such as New Energy Vehicle Battery Recycling Pilot Policy and Extended Producer Responsibility.

China's Ministry of Industry and Information Technology's battery recycling management measures require all EV battery manufacturers to establish take-back and recycling systems for batteries they produce. China's battery recycling rate for used power batteries reached approximately 70% in 2023 according to MIIT data, one of the highest in the world for lithium-ion traction batteries.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Battery Recycling Market Insights

Europe is one of the most actively regulated battery recycling markets globally, with the EU Battery Regulation representing the most comprehensive circular economy framework for batteries enacted anywhere in the world. The regulation's mandatory recycled content requirements for new batteries taking effect progressively from 2026 to 2031 are creating direct commercial demand for recycled battery materials that is pulling investment into European recycling capacity. Umicore in Belgium, Retriev Technologies' European operations, Northvolt's recycling division in Sweden, and Accurec in Germany represent the core of European battery recycling capacity, with additional new entrants attracted by the regulatory certainty that EU Battery Regulation creates.

The EU Battery Regulation (EU 2023/1542) establishes mandatory recycling efficiency targets of 80% for lithium-ion batteries by 2031 and material recovery targets requiring 90% lead recovery, 85% nickel and cobalt recovery, and 70% lithium recovery from spent batteries. Non-compliance carries substantial financial penalties under member state enforcement frameworks.

North America Battery Recycling Market Insights

North America is experiencing the most rapid rate of change in its battery recycling industry landscape, driven by unprecedented federal investment and IRA-created commercial incentives that are attracting recycling capacity development at pace. Li-Cycle's spoke-and-hub processing network, Redwood Materials' integrated refinery model, and Retriev's established smelting operations collectively represent a growing North American recycling infrastructure for both lead acid and lithium-ion batteries. The DOE's loan guarantee programs and grants are reducing the financial risk for first-of-kind large-scale lithium-ion recycling operations that would otherwise struggle to achieve commercial viability at current processing volumes.

Middle East & Africa and Latin America Battery Recycling Market Insights

Both regions are at earlier stages of formal battery recycling infrastructure development, though lead acid battery recycling through informal and semi-formal channels is established in most major economies. Brazil has the most developed formal battery recycling infrastructure in Latin America, anchored by the ABINEE industry association's take-back program and formal lead acid battery smelting operations. South Africa hosts formal lead acid recycling capacity serving the sub-Saharan African market.

Growth Drivers: Strict environmental regulations and EV battery end-of-life volumes driving rapid global battery recycling market expansion

The battery recycling market's growth is fundamentally regulatory and supply-chain driven two forces that reinforce each other powerfully. Government regulations mandating battery EPR, establishing minimum recycled content requirements, and prohibiting landfill disposal of batteries create the compliance foundation that ensures spent batteries flow to licensed recyclers rather than informal disposal. Simultaneously, the critical materials supply chain anxiety that Electric Vehicle battery adoption has created at national government level is motivating investment in domestic recycling capacity as a strategic material security measure. Every ton of lithium, cobalt, or nickel recovered from spent EV batteries is one less ton that needs to be sourced from politically sensitive mining geographies.

The IEA's Global EV Outlook projects that the number of EV battery packs reaching end-of-life will grow from approximately 60 GWh in 2022 to over 400 GWh annually by 2030, creating a material supply for recycling that will make lithium-ion battery recycling economically self-sustaining without subsidy support. The EU's Critical Raw Materials Act identifies battery recycling as a strategic supply security tool with specific recycled material contribution targets by 2030.

Restraints: High capital investment and battery chemistry complexity creating barriers for new entrants in battery recycling industry

Setting up a battery recycling facility is not a low-capital enterprise. Specialized shredding equipment, hydrometallurgical processing vessels, safety infrastructure for handling reactive lithium-ion cells, wastewater treatment systems, and the engineering expertise to operate them safely represent substantial upfront investment before the first ton of material is processed. Regulatory permits for hazardous material handling typically required for battery dismantling operations involve environmental impact assessments, community consultation processes, and ongoing compliance monitoring that extend from application to approval over multi-year timescales. The diversity of battery chemistries lithium-iron-phosphate, nickel-manganese-cobalt, nickel-metal hydride, lead acid each requiring different processing approaches, means that a facility optimized for one chemistry type cannot easily or economically process others, limiting operational flexibility and complicating the business model.

Opportunities: Strategic partnerships and AI-driven sorting innovations creating scalable sustainable battery recycling ecosystems globally

Strategic partnerships between automakers, battery manufacturers, and recyclers are the most commercially compelling opportunity being executed in the battery recycling industry right now. Closed-loop supply arrangements where an automaker guarantees spent battery supply to a recycler, which in turn guarantees recycled material supply to a cell manufacturer, which supplies batteries to the automaker create the supply security and price stability that justify long-term capital investment by all parties. Tesla's partnership with Redwood Materials, CATL's subsidiary Brunp Recycling, and Volkswagen's joint venture with Umicore represent different versions of this vertical integration model.

Recent Developments:

-

2025: Redwood Materials commenced full commercial operations at its first large-scale battery materials campus in McCarran, Nevada, with capacity to process 100 GWh of lithium-ion batteries annually and produce battery-grade lithium carbonate, nickel sulfate, and cobalt sulfate for supply to domestic cell manufacturers under multi-year supply agreements.

-

2025: Umicore SA expanded its hydrometallurgical lithium-ion battery recycling capacity at its Hoboken facility in Belgium, adding dedicated processing lines optimized for the NMC and LFP cathode chemistries prevalent in European EV batteries, targeting European OEM customers requiring certified recycled material to meet EU Battery Regulation recycled content requirements.

-

2026: Li-Cycle Holdings closed a transformative USD 475 million loan guarantee from the U.S. Department of Energy for its Rochester Hub commercial-scale hydrometallurgical processing facility, enabling the company to advance construction of North America's largest single lithium-ion battery recycling facility capable of processing black mass from multiple spoke pre-processing sites across the U.S. and Canada.

Battery Recycling Companies are:

-

Li-Cycle Holdings Corp. (Glencore Plc)

-

Umicore SA

-

GEM Co., Ltd. (China)

-

Brunp Recycling Technology Co., Ltd. (CATL)

-

Retriev Technologies Inc.

-

Battery Resources LLC

-

International Metals Reclamation Co. (INMETCO)

-

Glencore plc

-

Ecobat Technologies Ltd.

-

Stena Recycling AB

-

Northvolt AB (Revolt division)

-

Envirostream Australia Pty. Ltd.

-

Aqua Metals Inc.

-

Toxco Inc.

-

Sumitomo Metal Mining Co., Ltd.

-

TES-AMM Pte. Ltd.

-

Engitec Technologies SpA

-

Veolia Environment SA

| Report Attributes | Details |

|---|---|

|

Market Size in 2025 |

USD 30.74 Billion |

|

Market Size by 2035 |

USD 79.47 Billion |

|

CAGR |

CAGR of 9.81% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Chemistry (Lithium-ion, Lead Acid, Nickel, Others) • By Material (Metals, Electrolyte, Plastics, Other Components) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

Li-Cycle Holdings Corp., Redwood Materials, Inc., Umicore SA, GEM Co., Ltd. (China), Brunp Recycling Technology Co., Ltd. (CATL), Retriev Technologies Inc., Battery Resources LLC, Accurec Recycling GmbH, International Metals Reclamation Co. (INMETCO), Glencore plc, Ecobat Technologies Ltd., Stena Recycling AB, Northvolt AB (Revolt division), Envirostream Australia Pty. Ltd., Aqua Metals Inc., Toxco Inc., Sumitomo Metal Mining Co., Ltd., TES-AMM Pte. Ltd., Engitec Technologies SpA, Veolia Environment SA. |

Frequently Asked Questions

Asia-Pacific dominated the Battery Recycling Market in 2025.

The Lead Acid segment dominated the Battery Recycling Market with over 82% share in 2025.

Strict environmental regulations and sustainability goals are driving battery recycling adoption to reduce hazardous waste, recover critical materials, and promote a circular economy.

The Battery Recycling Market was valued at USD 30.74 billion in 2025.

The Battery Recycling Market is expected to grow at a CAGR of 9.81% from 2026 to 2035.

Get in Touch