Pet Wearable Market Report Scope & Overview:

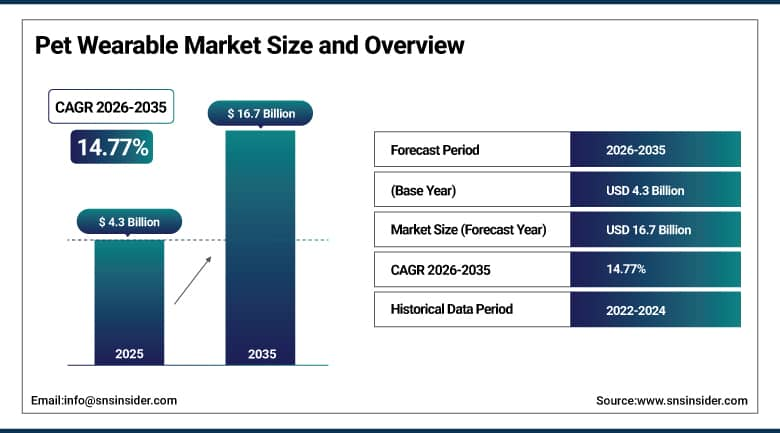

The Pet Wearable Market Size was valued at USD 4.3 billion in 2025 and is expected to reach USD 16.7 billion by 2035, growing at a CAGR of 14.77% from 2026-2035.

Pet Wearables Industry has been expanding owing to increased humanization of pets, increase in the demand for monitoring health of pets in real time, as well as increasing awareness about safety and wellness monitoring solutions. The increasing use of GPS enabled collars, wearable devices, and fitness trackers is also contributing to demand. The rise in urbanization, increase in disposable income, and increased pet ownership are propelling market growth. Moreover, the growth in e-commerce channels, as well as the availability of affordable smart devices, is also aiding market growth.

The American Pet Products Association’s 2025–2024 National Pet Owners Survey reports that pet spending in the United States reached a record USD 147 billion in 2025, with veterinary services and pet supplies, including technology-based products, emerging as the fastest-growing spending segments.

Market Size and Growth Forecast:

-

Market Size in 2025: USD 4.3 Billion

-

Market Size by 2035: USD 16.7 Billion

-

CAGR: 14.77% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Pet Wearable Market - Request Free Sample Report

Pet Wearable Market Trends Highlights

-

Rising pet ownership and increasing spending on pet care are driving the pet wearable market.

-

Growing adoption of smart collars, GPS trackers, and health monitoring devices is boosting market growth.

-

Expansion of pet health awareness and preventive care practices is fueling product demand.

-

Increasing focus on real-time tracking, activity monitoring, and safety features is shaping adoption trends.

-

Advancements in IoT, sensors, and mobile app integration are enhancing functionality and user experience.

-

Rising demand for connected pet ecosystems and personalized pet care solutions is supporting market expansion.

-

Collaborations between pet tech companies, veterinarians, and retailers are accelerating innovation and global adoption.

U.S. Pet Wearable Market Size Outlook:

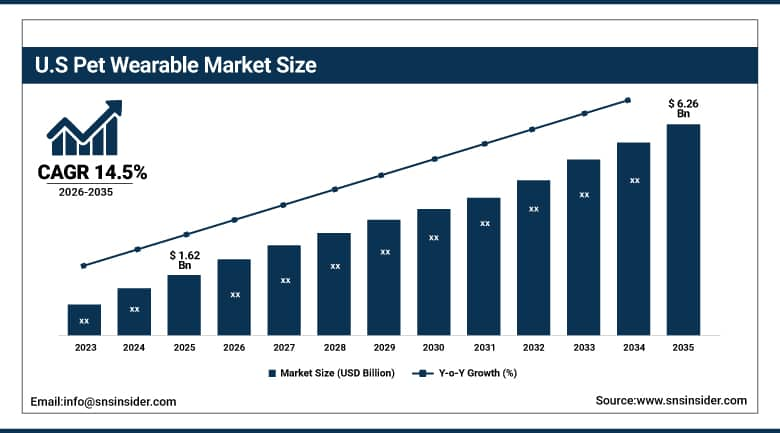

The U.S. Pet Wearable Market was valued at USD 1.62 billion in 2025 and is expected to reach USD 6.26 billion by 2035, growing at a CAGR of 14.5% from 2026-2035. The U.S. Pet Wearables Market is witnessing growth owing to the rise in pet ownership and investments in the health and safety of pets. The usage of smart collars, GPS, and health monitoring devices is contributing to demand. Growth in IoT and wearable technology innovations, along with an increased focus on preventive care, is aiding market expansion.

Petco Health and Wellness Company's 2024 report shows 41% of U.S. dog owners researched pet health monitoring tech, mainly GPS tracking and activity features, indicating rising mainstream awareness and growing demand for affordable pet wearable solutions.

Chewy's veterinary telehealth platform Connect With A Vet generated over 3 million video consultations in 2025, establishing the digital veterinary care infrastructure that integrates most naturally with pet wearable health data for remote monitoring workflows.

Pet Wearable Market Segment Analysis

-

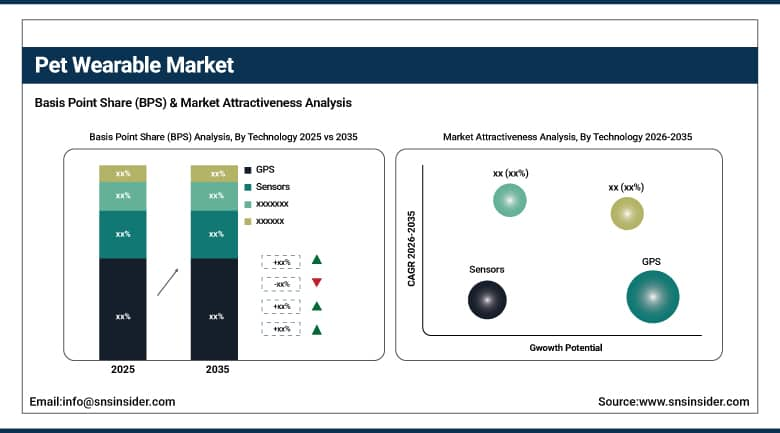

By Technology, GPS segment dominated the Pet Wearable Market in 2025 with ~36% share; Sensors segment fastest growing.

-

By Product, Smart Collar segment dominated the Pet Wearable Market in 2025 with ~48% share; Smart Harness and Vest segment fastest growing.

-

By Animal Type, Dogs segment dominated the Pet Wearable Market in 2025 with ~62% share; Cats segment fastest growing.

-

By Application, Identification & Tracking segment dominated the Pet Wearable Market in 2025 with ~39% share; Medical Diagnosis & Treatment segment fastest growing.

-

By Sales Channel, Online segment dominated the Pet Wearable Market in 2025 with ~55% share; Online segment also fastest growing.

By Technology, GPS segment dominates the Pet Wearable Market, Sensors segment expected to grow fastest

GPS segment is leading because of the importance of real-time location tracking and pet safety. Since safety is one of the major concerns among pet owners, GPS-enabled products ensure that there is no loss of pets, and it facilitates the process of recovering them. The use of mobile applications along with geofencing technology makes these products even more appealing to users. Awareness regarding the importance of monitoring pets and increased participation in outdoor activities are also driving the adoption of GPS-enabled wearable products.

The sensors segment will have the highest growth rate due to the growing need for sophisticated health monitoring systems in pets. Health monitoring devices are now getting attention from pet owners who are becoming increasingly conscious about the preventive healthcare and wellness aspect of their pets. Technological advancements in sensors are making products more reliable and accurate in performance.

By Product, Smart Collar segment dominates the Pet Wearable Industry, Smart Harness and Vest segment expected to grow fastest

The Smart Collar segment dominates because of the widespread availability, cost-effectiveness, and versatility of the devices used in this segment since they offer all-in-one technology like tracking, training, and health monitoring. Pet owners favor smart collars because they are convenient to use and comfortable for the pets. The addition of GPS systems and sensors makes them even more functional. Increased awareness regarding pet safety and the use of connected pet devices is making this trend stronger.

The Smart Harness & Vest segment will show the highest growth rate because of an increased concern over pet comfort as well as functional improvements in smart textiles and wearables. They are more comfortable to wear because they distribute the weight differently than collars do and can fit various sensors comfortably. Increased demand for safety features is also contributing to the growth of this market segment.

By Animal Type, Dogs segment dominates the Pet Wearable Market, Cats segment expected to grow fastest

The dog segment is the most dominant because of high adoption rates of pets worldwide and more investment in pet management and health care solutions for dogs compared to other pets. There is higher likelihood of taking out pets outside leading to high demand for tracking and safety devices. Emotional attachment and heightened concern about cat wellness are key drivers of the segment's dominance.

Cat segment will show the highest growth because of the high adoption rates of cats as pets in cities where space issues prevent people from having bigger animals. Awareness regarding health and safety measures for the cats is also making more people adopt these devices. Improvements in lightweight and compact devices have made it easy to use them with cats.

By Application, Identification & Tracking segment dominates the Pet Wearable Industry, Medical Diagnosis & Treatment segment expected to grow fastest

The Identification & Tracking category was the market leader as it catered to the key requirement of pet owners to maintain safety and avoid the loss of pets. Devices that enable identification and tracking of pets in real time have become important tools for pet monitoring, especially because the number of cases of lost pets is increasing. The medical diagnosis and treatment of pets, using wearable devices with advanced sensor technology, form an integral part of pet healthcare.

The Medical Diagnosis & Treatment segment is the fastest-growing, driven by the emphasis placed on pet health care and timely detection of diseases. Pet wearables that can detect and diagnose health problems through sensor technology are used extensively today. As veterinarians start integrating technology into their daily operations, the need for diagnostic and treatment solutions is increasing.

By Sales Channel, Online segment dominates the Pet Wearable Market, Online segment expected to grow fastest

The online segment dominated the market because of the increased popularity of online marketplaces that offered different types of pet wearables at competitive prices. The reason behind this domination was that people find the online platform easier for comparisons and review of products as well as convenient delivery options. With an increase in digital penetration, it is expected that growth will continue to grow. Online channel is expected to experience the fastest growth because of fast development of the infrastructure in the digital market as well as consumers’ preference for online purchases. The rising use of smartphones and enhanced delivery mechanisms make the purchasing process easier and more convenient. More brands are adopting direct selling to the consumer via online means.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

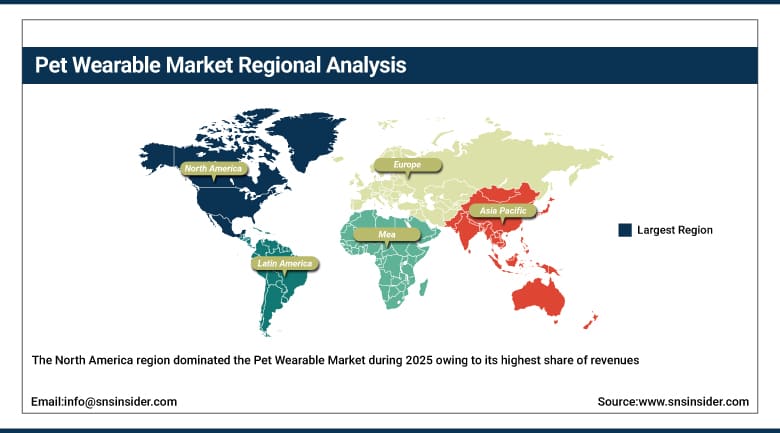

North America Pet Wearable Market Insights

The North America region dominated the Pet Wearable Market during 2025 owing to its highest share of revenues estimated at 40% due to higher rates of pet adoption and investments in pet healthcare products/services. Extensive usage of cutting-edge technologies such as GPS trackers and wellness devices boosts market growth greatly. High consciousness regarding pet safety and wellness drives demand upwards further. Leading companies, conducive regulatory policies, and availability of smart pet wearables via both offline and online modes are additional factors that help maintain regional supremacy.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Pet Wearable Market Insights

The Asia Pacific region represents the most rapidly expanding market in terms of Pet Wearables due to the increased ownership of pets, the humanization of pets, and heightened awareness regarding the importance of their health, safety, and well-being. The increasing use of GPS tracking, smart collars, and activity monitoring systems is fueling strong demand in the market. Factors such as rapid urbanization, rising disposable income levels, and an increasing number of people belonging to the middle class are adding impetus to the growth of the market.

Europe Pet Wearable Market Insights

The Europe Pet Wearable Market is growing at a moderate rate owing to high pet ownership ratios, a keen interest in animal well-being, and increasing acceptance of innovative pet monitoring solutions. The increasing need for pet wearables like GPS trackers, smart collars, and health monitors is contributing to the market growth. Increasing consumer preference for ensuring pet safety, fitness tracking, and location monitoring in real-time is boosting market growth. High standards set by the regulatory authorities for pet care and awareness about pet care are fueling market growth.

MEA and Latin America Pet Wearable Market Insights

MEA and Latin America Pet Wearable Devices Market witnessing steady growth due to higher rates of pet adoption, higher awareness about pets’ well-being, and usage of advanced and sophisticated wearable devices for pets. Usage of GPS-based collars, health monitoring devices, and activity monitors for pets is fueling market growth. Urbanization and increasing disposable income levels are adding to the trend of increasing adoption by residential consumers. Awareness and affordability are posing restrictions on market growth in some regions.

Market Dynamics

Growth Drivers: Rising Adoption of Pet Wearables Driven by Increased Focus on Health Monitoring, AI Integration, and Real-Time Tracking Solutions.

With the increase in pet ownership, there has been an increase in the need for health-conscious monitoring systems. More and more owners prefer monitoring systems that can keep track of the physiological conditions, activities, and behaviors of pets to give way to more pro-active pet care. With IoT and artificial intelligence embedded in wearables, pets can be monitored remotely and have diseases detected beforehand, making pet care a scientific process and much more efficient. Moreover, the rise in the popularity of pet tele-health care services and the role played by wearable data by insurance companies in customizing policies is also contributing to the market’s success. As pets continue to get humanized, the consumer spends more on technology that helps keep their pets healthier and safer.

Restraints: High Cost of Smart Pet Wearables Limits Adoption, Restricting Market Growth and Accessibility in Price-Sensitive Consumer Segments.

The exorbitant prices of smart collars and wearable devices represent another significant barrier that hinders the popularity and use of these innovative products. The incorporation of IoT, AI, and GPS tracking makes manufacturing costly, which makes these wearables too expensive for many pet owners. Clients would be hesitant to pay a lot of money on a device unless they find clear value, which includes an improvement in their pets' health status and saving money overall. In addition to this, the lack of low-cost substitutes poses a challenge to the market development. Thus, in order to address the issue of high prices, manufacturers have to focus on ways to reduce costs, take advantage of economies of scale, and implement flexible pricing policies.

Opportunities: Advancements in AI and IoT Drive Innovation in Smart Pet Wearables for Enhanced Health Monitoring and Real-Time Tracking

AI and IoT applications in the field of pet wearables are revolutionizing the way pet health is being managed through advanced features like real-time monitoring, predictive analysis, and automated health monitoring. The use of AI and algorithms helps monitor the behavioral patterns of pets and provide alerts about potential problems that may arise in the future, which would improve the effectiveness of veterinary care services. IoT also plays a vital role in ensuring that pets are safely monitored using advanced features such as GPS, geofencing, and remote control. Smart pet ecosystems comprising wearable devices as well as feeders, cameras, and health monitoring platforms are becoming more prevalent. Manufacturers can leverage the emerging trend towards data and technology-powered solutions for pets.

Recent Developments:

-

2026: Garmin launched Alpha 300 LTE GPS dog collar with nationwide LTE tracking, heart rate monitoring, and 72-hour battery life, targeting premium hunting dogs requiring real-time location and performance tracking at USD 599 price point.

-

2025: Whistle Health introduced Whistle GO Explore 4 with FDA-cleared respiratory monitoring using accelerometer-based sleep analysis, enabling early detection of serious diseases like heart failure and pulmonary edema in consumer pet wearables.

-

2025: Tractive expanded GPS tracking service to 175 countries using satellite-assisted GPS and LTE backup, improving global pet location continuity for travelers and increasing subscription renewals by 40% through enhanced international tracking features.

Key Pet Wearable Companies are:

-

Datamars

-

Felcana

-

FitBark Inc.

-

GoPro Inc

-

LATSEN (Pawfit)

-

Link My Pet

-

Loc8tor Ltd

-

Mars, Incorporated (Whistle Labs Inc.)

-

PETFON

-

PetPace

-

Tractive GmbH

-

PawTrax Limited

-

Dairymaster USA Inc.

-

Afimilk Ltd.

-

IceRobotics Ltd.

-

Dogtra

-

DogTelligent Inc.

-

Pod Trackers

| Report Attributes | Details |

| Market Size in 2025 | USD 4.3 Billion |

| Market Size by 2035 | USD 16.7 Billion |

| CAGR | CAGR of 14.77% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (RFID, GPS, Sensors) • By Product (Smart Collar, Smart Camera, Smart Harness and Vest, Others) • By Animal Type (Dogs, Cats, Other Animals) • By Application (Identification & Tracking, Behavior Monitoring & Control, Facilitation, Safety & Security, Medical Diagnosis & Treatment) • By Sales Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Avid Identification Systems, Inc., Datamars, Felcana, FitBark Inc., Garmin Ltd., GoPro Inc., LATSEN (Pawfit), Link My Pet, Loc8tor Ltd., Mars, Incorporated (Whistle Labs Inc.), PETFON, PetPace, Tractive GmbH, PawTrax Limited, Dairymaster USA Inc., Afimilk Ltd., IceRobotics Ltd., Dogtra, DogTelligent Inc., Pod Trackers. |

Frequently Asked Questions

Ans: Cats are the fastest growing at approximately 16.81% CAGR; Dogs dominated with 67% share.

Ans: RFID dominated with approximately 44% share; GPS is the fastest growing at 15.92% CAGR.

Ans: North America dominated; Asia Pacific is the fastest growing regional market.

Ans: The Pet Wearable Market was valued at USD 4.3 billion in 2025.

Ans: The Pet Wearable Market is expected to grow at a CAGR of 14.77% from 2026 to 2035.

Get in Touch