Pharmaceutical Cleaning Validation Market Report Scope & Overview:

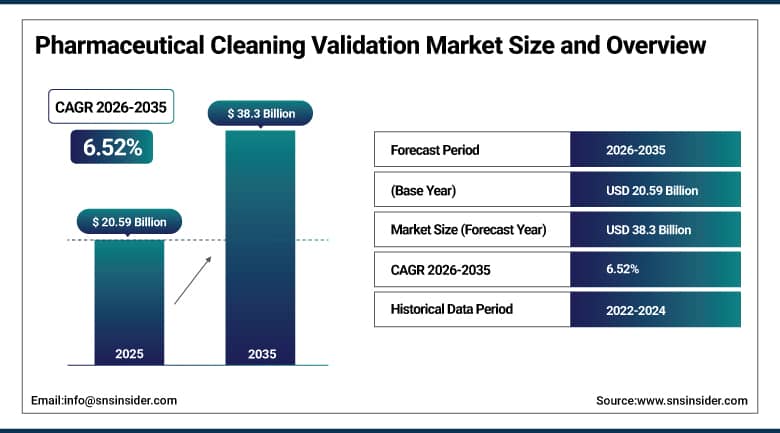

The Pharmaceutical Cleaning Validation Market was valued at USD 20.59 Billion in 2025 and is expected to reach USD 38.3 Billion by 2035, growing at a CAGR of 6.52% from 2026–2035.

Pharmaceutical cleaning validation is the documented process of confirming that manufacturing equipment surfaces are free from residues of previously manufactured products, cleaning agents, and microbial contamination before the next batch is produced. It is a mandatory requirement of current Good Manufacturing Practice regulations enforced by the FDA in the United States, the European Medicines Agency, and the World Health Organization globally. The market encompasses the analytical testing, validation methodology, cleaning agents, and professional services involved in establishing, executing, and maintaining cleaning validation programmes across pharmaceutical and biopharmaceutical manufacturing facilities. Regulatory agencies are progressively tightening their expectations for cleaning validation. FDA warning letters and EMA inspection findings related to inadequate cleaning validation have increased substantially over the past decade, raising the regulatory and commercial consequences of inadequate cleaning validation programmes. This enforcement intensity is the most commercially significant driver of cleaning validation market growth, as pharmaceutical manufacturers invest in robust validation programmes to avoid the operational and financial consequences of regulatory action.

FDA issued 47 warning letters specifically citing inadequate cleaning validation as a key deficiency during fiscal year 2024. Each warning letter represents a significant commercial and operational disruption for the recipient manufacturer, confirming the direct commercial incentive that regulatory enforcement creates for cleaning validation programme investment globally.

Market Size and Forecast

-

Market Size in 2026E: USD 21.93 Billion

-

Market Size by 2035: USD 38.3 Billion

-

CAGR: 6.52% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Pharmaceutical Cleaning Validation Market - Request Free Sample Report

Pharmaceutical Cleaning Validation Market Trends

-

Risk-based cleaning validation approaches are replacing uniform validation methods to improve efficiency and regulatory compliance in pharmaceutical manufacturing.

-

Advanced analytical technologies like TOC analyzers and HPLC are improving low-level pharmaceutical residue detection accuracy significantly.

-

Biopharmaceutical manufacturing growth is increasing demand for specialized cleaning validation protocols for complex biological therapeutic residues.

-

Digital cleaning validation platforms are replacing paper-based systems through electronic documentation and audit-ready regulatory compliance capabilities.

-

Contract manufacturing organizations are expanding cleaning validation services due to increasing pharmaceutical manufacturing outsourcing activities globally.

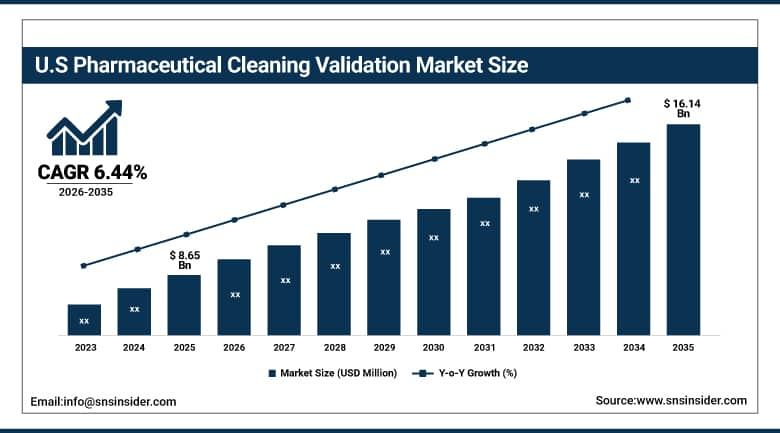

The U.S. Pharmaceutical Cleaning Validation Market Outlook

The U.S. Pharmaceutical Cleaning Validation Market was valued at approximately USD 8.65 Billion in 2025 and is expected to reach approximately USD 16.14 Billion by 2035, growing at a CAGR of 6.44%.

The United States is the world's largest pharmaceutical cleaning validation market driven by the combination of the world's most stringent GMP regulatory environment, the highest concentration of pharmaceutical and biopharmaceutical manufacturing facilities operating under FDA oversight, and the most active enforcement record globally for cleaning validation deficiencies. American pharmaceutical manufacturers spend more per facility on cleaning validation than their counterparts in any other jurisdiction because the FDA's inspection-readiness standards and warning letter consequences create financial incentives for comprehensive programme investment that match or exceed the cost of regulatory non-compliance.

The CHIPS and Science Act analogue in pharmaceuticals, the BIOSECURE Act and FDA's domestic manufacturing incentive frameworks, are supporting American pharmaceutical production expansion that creates new cleaning validation demand. U.S. contract manufacturing organizations including Lonza, Catalent, Patheon, and Samsung Biologics' American facilities are each investing in cleaning validation infrastructure to serve their pharmaceutical client bases. The growth of advanced therapy manufacturing for cell and gene therapies in U.S. facilities is creating the most technically demanding cleaning validation challenges the industry has encountered, requiring new validated cleaning methods for equipment that has never been used for conventional small molecule drug production.

The FDA's 2025 revision to its Pharmaceutical Cguidance for Cleaning Validation confirmed risk-based approaches as regulatory best practice while maintaining the expectation of documented scientific rationale for all acceptance criteria. This guidance clarity is expected to accelerate cleaning validation programme modernisation investment across U.S. pharmaceutical manufacturers updating legacy validation systems to current regulatory expectations.

Pharmaceutical Cleaning Validation Market Segment Analysis

-

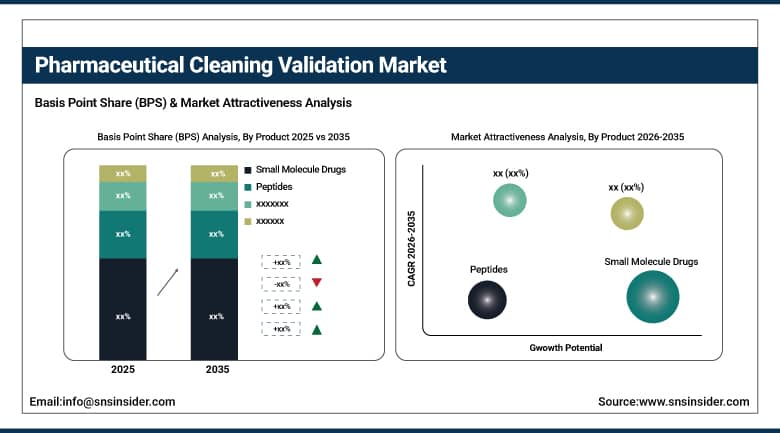

By Product, small molecule drugs dominated the market with approximately 45.23% share in 2025; peptides and proteins are the fastest-growing segment.

-

By Validation Test, product-specific analytical tests dominated with approximately 64.5% share in 2025; non-specific tests including TOC analysis are growing.

-

By Method, swab sampling held the largest share in 2025 through its established status as the primary regulatory-accepted method; rinse sampling is growing in multi-product campaigns and aseptic manufacturing.

-

By End User, pharmaceutical companies held the largest share in 2025; contract manufacturing organizations are the fastest-growing end user.

By Product, small molecule drugs dominate, peptides and proteins grow fastest

Small molecule drugs held approximately 45.23% of the pharmaceutical cleaning validation market in 2025. This dominance reflects the foundational commercial importance of conventional synthetic pharmaceutical manufacturing in global drug supply. Small molecule drugs are the backbone of treatment for cardiovascular disease, infectious diseases, cancer, diabetes, and the vast majority of chronic conditions that account for the highest prescription volumes globally. The manufacturing of these drugs in multi-product facilities where the same equipment is used for different active pharmaceutical ingredients creates the cross-contamination risk scenario that cleaning validation is specifically designed to control. Every equipment train used for multiple small molecule drugs requires cleaning validation protocols establishing residue limits and verified cleaning procedures for each product changeover combination.

Peptides and proteins are the fastest-growing product segment as the biopharmaceutical industry's expansion creates cleaning validation requirements that differ substantially from conventional small molecule validation. Biological molecules including monoclonal antibodies, fusion proteins, peptide hormones, and advanced therapy products are heat-labile, complex in structure, and degrade in ways that make conventional analytical methods insufficient for residue detection. Protein-based drug residues can denature and adhere to equipment surfaces in patterns that require validated cleaning procedures specifically developed for biological product contact surfaces. The rapid expansion of mAb, biosimilar, and cell and gene therapy manufacturing is creating the fastest-growing segment of cleaning validation programme development and analytical testing demand.

By Validation Test, product-specific analytical tests dominate, TOC grows fastest

Product-specific analytical tests held approximately 64.5% of the pharmaceutical cleaning validation market in 2025. HPLC is the dominant analytical method for cleaning validation because it provides the sensitivity, specificity, and quantitative accuracy needed to detect and measure specific drug substance residues at the parts-per-million or parts-per-billion concentrations required by risk-based acceptance criteria. UV spectroscopy provides a faster but less specific alternative for some residue types. Mass spectrometry combined with liquid chromatography is entering cleaning validation as the most sensitive available analytical approach for highly potent APIs where acceptance criteria are set at extremely low residue levels measured in micrograms per surface area. The growing use of HPLC for cleaning validation is creating instrument procurement and analytical method development demand that represents a significant commercial stream within the broader market.

Total organic carbon analysis and other non-specific tests are growing through their suitability for process analytical technology integration in continuous pharmaceutical manufacturing. TOC analysers provide rapid, instrument-based total carbon measurement that can serve as a non-specific cleaning endpoint indicator before product-specific confirmation testing. Their speed makes them operationally attractive for manufacturing campaigns where cleaning validation turnaround time is a production scheduling constraint. SUEZ's December 2024 launch of the M500 TOC Analyser, which reduced testing times by 50%, demonstrated how instrument innovation is making non-specific testing methods more commercially competitive in cleaning validation applications.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.4% |

|

Europe |

Germany |

26.8% |

|

Asia Pacific |

India |

34.7% |

|

Middle East & Africa |

Israel |

26.4% |

|

Latin America |

Brazil |

42.3% |

North America Pharmaceutical Cleaning Validation Market Insights

North America dominated the global pharmaceutical cleaning validation market in 2025 with approximately 42.09% of global revenues. The United States accounts for approximately 79.4% of North American revenues as the world's most regulated pharmaceutical manufacturing jurisdiction and the market with the highest cleaning validation programme investment intensity per facility. FDA's GMP inspection programme for both domestic and foreign drug manufacturers, its active warning letter enforcement record, and its progressive guidance on cleaning validation risk assessment collectively create the most commercially significant regulatory driver of cleaning validation investment globally. American pharmaceutical manufacturers include the world's largest companies by revenue whose scale creates proportionally large cleaning validation service and product procurement.

Canada is a significant pharmaceutical cleaning validation market through its domestic drug manufacturing sector operating under Health Canada's GMP standards, which are closely aligned with FDA requirements. Canadian pharmaceutical manufacturers including Apotex, Pharma science, and the Canadian facilities of multinational pharmaceutical companies maintain cleaning validation programmes meeting both domestic and export market regulatory expectations. Health Canada's updated master cleaning validation guide, released progressively through 2024 and 2025, is prompting Canadian facilities to review and update legacy cleaning validation systems.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Pharmaceutical Cleaning Validation Market Insights

Europe is a large and technically sophisticated pharmaceutical cleaning validation market where EMA guidelines and European Pharmacopoeia standards establish comprehensive cleaning validation requirements for pharmaceutical manufacturers operating within EU member states. Germany accounts for approximately 26.8% of European revenues as the EU's largest pharmaceutical manufacturing economy and the location of major pharmaceutical companies including Bayer, Boehringer Ingelheim, and Merck KGaA whose global manufacturing operations require extensive cleaning validation programme management. The EU's Annex 15 to the GMP guidelines specifically addresses validation including cleaning validation, providing detailed expectations that manufacturers across the EU must satisfy for both product approval and manufacturing licence compliance.

The United Kingdom, France, Switzerland, Italy, and Ireland are also significant pharmaceutical cleaning validation markets. Ireland is disproportionately important relative to its population size as a pharmaceutical manufacturing hub hosting the European manufacturing operations of major U.S. pharmaceutical companies whose FDA-oversight facilities must simultaneously meet EMA standards. Merck KGaA partnered with Agilent Technologies in August 2025 to enhance process analytical technologies for cleaning validation applications, reflecting the active collaboration between European pharmaceutical technology suppliers and manufacturers on next-generation validation approaches.

Asia Pacific Pharmaceutical Cleaning Validation Market Insights

Asia Pacific is the fastest-growing pharmaceutical cleaning validation market at a CAGR of 7.24% through 2035. India accounts for approximately 34.7% of Asia Pacific revenues as the world's largest generic drug manufacturing nation whose thousands of FDA and EMA registered facilities require cleaning validation programmes meeting international regulatory standards. India's pharmaceutical manufacturing sector serves global drug markets, and every facility producing drugs for the U.S. or EU market must demonstrate cleaning validation compliance to the standards of those export markets. China's pharmaceutical manufacturing expansion under its national drug quality regulatory reform programme is creating systematic cleaning validation investment as domestic manufacturers upgrade to international GMP standards required for drug export.

MEA & Latin America Pharmaceutical Cleaning Validation Market Insights

The Middle East and Africa and Latin America are growing pharmaceutical cleaning validation markets where pharmaceutical manufacturing investment, regulatory system strengthening, and export market aspirations are creating cleaning validation programme demand. Israel leads MEA revenues at approximately 26.4% of the regional share through its active pharmaceutical manufacturing sector producing generic drugs for global export markets including the United States. Teva Pharmaceutical, headquartered in Israel, maintains major international manufacturing operations with extensive cleaning validation requirements. Brazil leads Latin American revenues at approximately 42.3% through its large domestic pharmaceutical manufacturing sector regulated by ANVISA and its growing pharmaceutical export programme requiring international GMP standard cleaning validation.

Market Dynamics

Growth Drivers: Intensifying regulatory enforcement of cleaning validation standards and biopharmaceutical manufacturing growth creating new validation complexity are the primary pharmaceutical cleaning validation market growth drivers.

Regulatory enforcement is the most commercially immediate driver of cleaning validation market growth. FDA warning letters, EMA inspection findings, and WHO prequalification requirements create direct financial consequences for inadequate cleaning validation that motivate manufacturing investment. Each 483 observation or warning letter related to cleaning validation deficiencies represents significant remediation cost, potential market withdrawal risk, and reputational damage that pharmaceutical companies invest in prevention programmes to avoid. The regulatory agencies' increasing use of risk-based inspection approaches that specifically evaluate cleaning validation programme robustness has made cleaning validation a high-priority audit area that manufacturing quality teams cannot neglect without significant exposure.

Biopharmaceutical manufacturing growth is creating the most technically demanding cleaning validation challenges the pharmaceutical industry has encountered. The development of monoclonal antibodies, fusion proteins, ADCs, mRNA therapeutics, and cell and gene therapy products in manufacturing facilities that must maintain contamination control at unprecedented levels is requiring new cleaning validation methodology, new analytical testing approaches, and new equipment design standards. The global biopharmaceutical pipeline's rapid expansion, represented by more than 1,400 biologic candidates in clinical development in 2025, is creating sustained downstream manufacturing investment that includes the cleaning validation infrastructure these products require.

Restraints: Complexity and cost of validation protocol development for multi-product facilities and skilled personnel shortage in pharmaceutical quality and analytical chemistry are restraining market growth.

The complexity of cleaning validation programme development is the most significant operational barrier for pharmaceutical manufacturers. Each new product introduced to a shared equipment facility requires cleaning validation studies establishing the worst-case residue scenarios, appropriate acceptance criteria, and verified cleaning procedures for every product combination possible on that equipment. The number of pairwise product combinations grows rapidly as product portfolios expand, creating programme management complexity that scales non-linearly with facility throughput. Contract manufacturing organisations handling multiple client products on shared equipment face particularly acute validation complexity that requires significant dedicated analytical chemistry and quality assurance resources.

The shortage of qualified pharmaceutical validation professionals is a structural market constraint. Cleaning validation requires expertise combining analytical chemistry, pharmaceutical regulation, quality risk management, and process understanding that takes years to develop. The pharmaceutical industry's rapid expansion globally is outstripping the supply of experienced validation professionals. This talent constraint limits the velocity of cleaning validation programme development and creates wage inflation for specialised validation personnel that increases cleaning validation programme operating costs independent of any change in the underlying regulatory or manufacturing drivers.

Opportunities: AI-assisted continuous process verification for cleaning validation, advanced analytical testing for highly potent active pharmaceutical ingredients represent the strongest market growth opportunities.

AI-assisted continuous process verification represents the most commercially transformative opportunity in pharmaceutical cleaning validation. Real-time analytical monitoring systems combined with machine learning models that predict cleaning endpoint achievement from process parameter data could enable a shift from fixed-protocol cleaning validation toward adaptive, data-driven verification. Regulatory agencies are actively engaging with pharmaceutical manufacturers on continuous verification concepts as part of their embrace of advanced manufacturing technology. Manufacturers that achieve regulatory acceptance for continuous cleaning verification would gain operational flexibility and efficiency that is commercially valuable beyond the validation programme cost savings alone.

Highly potent API manufacturing is creating a premium cleaning validation service market whose growth rate substantially exceeds the broader market average. HPAPI manufacturing requires cleaning validation acceptance criteria set at residue levels measured in micrograms or nanograms per surface area, requiring the most sensitive analytical methods available and the most rigorous swab recovery validation. The HPAPI manufacturing market is growing as oncology drug development drives an expanding pipeline of cytotoxic and targeted cancer therapies whose manufacturing requires specialized containment and cleaning validation systems. Service providers with validated HPAPI cleaning validation capability command premium fees in a market where few suppliers have the specialized expertise and equipment to deliver credible services.

Recent Developments:

-

2025: Thermo Fisher Scientific acquired Solventum's purification and filtration business for USD 4.1 billion, strengthening its bioprocessing filtration capabilities that are critical for cleaning validation in complex biologic drug production environments.

-

2025: Sartorius AG projected continued growth in biopharmaceutical production investment and highlighted increasing cleaning validation adoption among its bioprocessing equipment customer base as a driver of its filtration and testing product demand.

-

2025: Merck KGaA partnered with Agilent Technologies to enhance process analytical technologies for pharmaceutical manufacturing, including applications in cleaning validation where real-time analytical monitoring improves cleaning endpoint determination accuracy.

Pharmaceutical Cleaning Validation Market key players are:

-

Thermo Fisher Scientific Inc.

-

Merck KGaA

-

Agilent Technologies Inc.

-

Waters Corporation

-

Shimadzu Corporation

-

HORIBA Ltd.

-

Ecolab Inc.

-

Sartorius AG

-

BioTechLogic Inc.

-

Lonza Group AG

-

Catalent Inc.

-

Patheon

-

Charles River Laboratories

-

ICON plc

-

Eurofins Scientific SE

-

SGS SA

-

Novatek International

-

PharmOut Pty Ltd.

-

ValGenesis Inc.

-

Kneat Solutions Inc.

Pharmaceutical Cleaning Validation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.59 Billion |

| Market Size by 2035 | USD 38.3 Billion |

| CAGR | CAGR of 6.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Small Molecule Drugs, Peptides, Proteins, Cleaning Detergents) • By Validation Test (Non-Specific Tests, Product-Specific Analytical Tests) • By Method (Swab Sampling, Rinse Sampling, Placebo Sampling) • By End User (Pharmaceutical Companies, Contract Manufacturing Organizations, Biotechnology Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Merck KGaA, Agilent Technologies Inc., Waters Corporation, Shimadzu Corporation, HORIBA Ltd., Ecolab Inc., Sartorius AG, BioTechLogic Inc., Lonza Group AG, Catalent Inc., Patheon, Charles River Laboratories, ICON plc, Eurofins Scientific SE, SGS SA, Novatek International, PharmOut Pty Ltd., ValGenesis Inc., Kneat Solutions Inc. |

Frequently Asked Questions

Intensifying regulatory enforcement of cleaning validation standards globally and biopharmaceutical manufacturing growth creating new validation complexity are the primary drivers.

Small molecule drugs dominated with approximately 45.23% of revenues in 2025.

North America dominated the pharmaceutical cleaning validation Market in 2025 with approximately 42.09% of global revenues.

The pharmaceutical cleaning validation market was valued at USD 20.59 Billion in 2025.

The pharmaceutical cleaning validation market is expected to grow at a CAGR of 6.52% from 2026 to 2035.

Get in Touch