Insulin Delivery Devices Market Report Scope & Overview:

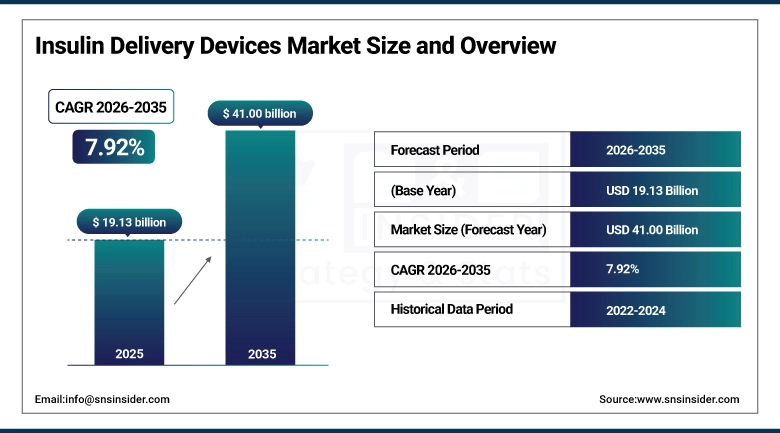

The Insulin Delivery Devices Market size was valued at USD 19.13 Billion in 2025 and is expected to reach USD 41.00 Billion by 2035, growing at a CAGR of 7.92% over the forecast period of 2026–2035.

The market for insulin delivery devices worldwide is showing continuous growth, and this is mainly because of the rising prevalence of Type 1 and Type 2 diabetes in the world population, along with developments in drug delivery technology and patient demand for less invasive and easier methods for insulin delivery. Some of the significant growth accelerators in this market are the rapid market uptake of insulin pens and smart insulin pumps, increased trend of using continuous glucose monitoring in association with closed-loop delivery devices, and the widespread presence of wearable patch pumps in this market. Furthermore, increased healthcare spending and reimbursement for diabetes management devices are also contributing to the growth of this market in both developed and emerging markets.

For instance, in January 2024, the International Diabetes Federation reported that approximately 537 million adults worldwide were living with diabetes, with projections estimating a rise to 643 million by 2030, directly intensifying global demand for advanced insulin delivery devices across all major markets.

Insulin Delivery Devices Market Size and Forecast:

-

Market Size in 2025: USD 19.13 Billion

-

Market Size by 2035: USD 41.00 Billion

-

CAGR: 7.92% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Insulin Delivery Devices Market - Request Free Sample Report

Insulin Delivery Devices Market Trends:

-

Growing adoption of smart insulin pens with Bluetooth connectivity and dose-tracking apps to enhance medication adherence and real-time glucose management.

-

Increasing integration of insulin pumps with continuous glucose monitoring systems to enable automated, closed-loop artificial pancreas functionality.

-

Rising consumer demand for wearable, tubeless patch pumps that offer discreet, on-body insulin delivery with improved quality of life for patients.

-

Expansion of prefilled, disposable insulin pen cartridges and ultra-fine pen needles to minimize injection pain and improve patient compliance across age groups.

-

Growing investment in digital therapeutics platforms that pair insulin delivery hardware with AI-driven dosing algorithms and telemedicine-enabled care management.

-

Accelerated regulatory approvals and product launches targeting pediatric and elderly diabetic populations with device ergonomics tailored to ease of use.

-

Strategic collaborations between pharmaceutical insulin manufacturers and device companies to develop combination drug-device products with streamlined regulatory pathways.

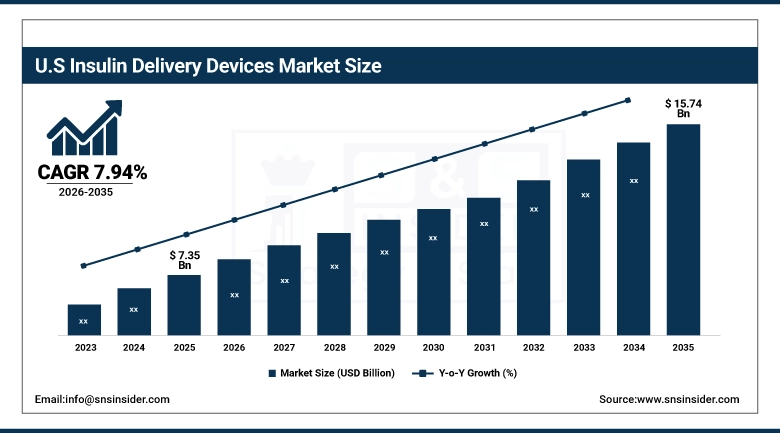

The U.S. Insulin Delivery Devices Market was valued at USD 7.35 billion in 2025 and is expected to reach USD 15.74 billion by 2035, growing at a CAGR of 7.94% from 2026–2035. The United States accounts for the largest market share of the global insulin delivery devices market owing to its exceptionally high rate of diabetes prevalence and the presence of a well-established system of private and federal insurance reimbursement. The federal government's support through Medicare and Medicaid programs for continuous glucose monitors and insulin pumps and the availability of advanced insulin delivery systems such as hybrid closed-loop insulin pumps also add to the strength of the US market.

Insulin Delivery Devices Market Growth Drivers:

-

Surging Global Diabetes Prevalence is Driving the Insulin Delivery Devices Market Growth

The ever-increasing global incidence of diabetes mellitus is the chief driver of the insulin delivery devices market share, as the populations suffering from Type 1 and insulin-dependent Type 2 diabetes need insulin therapy. The increasing sedentary lifestyle, the incidence of obesity, and the rise of the aging population, along with the rapid progression of urbanization in developing countries, are contributing factors to the increasing market share of insulin delivery devices. The increasing incidence of diabetes mellitus is directly contributing to the increasing demand for insulin pens, insulin pumps, pen needles, and syringes, thereby driving the long-term revenue chart of the insulin delivery devices market.

For instance, in March 2024, the Centers for Disease Control and Prevention (CDC) estimated that over 38.4 million Americans had diabetes, with insulin therapy being prescribed to approximately 8.4 million patients, sustaining robust domestic demand for all categories of insulin delivery devices.

Insulin Delivery Devices Market Restraints:

-

High Device Costs and Limited Reimbursement in Developing Regions are Hampering the Insulin Delivery Devices Market Growth

The high cost incurred in acquiring and using advanced insulin delivery technology, especially in the case of insulin pumps and smart connected pens, acts as a significant barrier in penetrating low- and middle-income markets where reimbursement support is limited or non-existent. Patients in Latin America, Africa, and parts of Asia-Pacific are using traditional syringes for administering insulin because of affordability issues, thus affecting the market for premium-tier products. This acts as a limitation for the market growth potential in high-growth markets and also negatively impacts the ASP for insulin delivery devices globally.

Insulin Delivery Devices Market Opportunities:

-

Closed-Loop Insulin Delivery Systems and Digital Integration Present Significant Future Growth Opportunities

The development of insulin pumps, continuous glucose monitoring, and AI-based dosing systems, which have merged into fully automated closed-loop systems, provides the greatest growth potential opportunity for the insulin delivery devices market. These artificial pancreas systems have the advantage of eliminating the need for manual dose calculations, reducing the risk of hypoglycemic episodes, and improving time-in-range metrics for diabetic patients. As regulatory bodies like the FDA and CE continue to expedite approval processes for automated insulin delivery (AID) systems, the awareness of the superiority of these systems among consumers is also increasing, thereby increasing the adoption of these systems among both Type 1 and Type 2 insulin-dependent diabetic patients.

For instance, in August 2024, the FDA cleared a next-generation hybrid closed-loop insulin delivery system that demonstrated a 74% reduction in hypoglycemic events in clinical trials, underscoring the accelerating innovation pipeline and substantial commercial opportunity within the automated insulin delivery segment.

Insulin Delivery Devices Market Segment Analysis

-

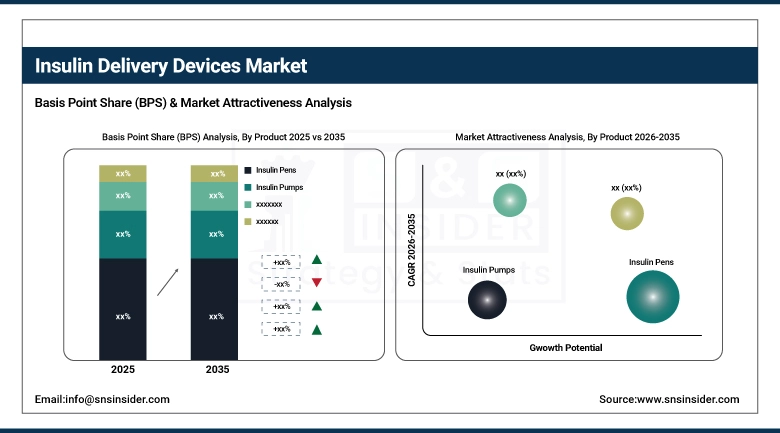

By product, insulin pens held the largest share of approximately 43.56% in 2025, while the insulin pumps segment is expected to register the highest growth with a CAGR of 9.14%.

-

By end use, the hospitals & clinics segment dominated with approximately 57.38% share in 2025, while the homecare segment is expected to register the highest growth with a CAGR of 8.64%.

By Product, Insulin Pens Lead the Market, While Insulin Pumps Register Fastest Growth

The segment of insulin pens recorded the highest revenue share of around 43.56% in 2025, owing to their high recommendation rate by physicians, better dose control compared to traditional syringes, ergonomic design for ease of handling, and worldwide availability in reusable and disposable formats. The rising demand for disposable insulin pens among newly diagnosed patients and the rising number of biosimilar insulin pens in the market from established companies are also contributing factors for this segment. On the other hand, the segment of insulin pumps is projected to register the highest CAGR of 9.14% during the forecast period ranging from 2026 to 2035, owing to rising demand for tubeless patch pumps, expanded use in pediatric patients, CGM system integration, and rising support for AI-based delivery systems for better glycemic control.

By End Use, Hospitals & Clinics Dominate, while Homecare Segment Shows Rapid Growth

The Hospitals & Clinics segment accounted for the highest revenue share of 57.38% in 2025, owing to the high volume of diabetes management cases, insulin infusion, diabetes education, and initiation of pump or pen therapy under the guidance of physicians. The homecare segment, however, is expected to register the highest CAGR of 8.64% during the forecast period of 2026-2035, owing to the increasing interest in self-managed care, the increasing availability of telehealth-enabled insulin delivery systems, the increasing penetration of connected insulin pens among tech-savvy patients, as well as the cost-effectiveness of home-based care as opposed to hospital-based care.

Insulin Delivery Devices Market Regional Highlights:

North America Insulin Delivery Devices Market Insights:

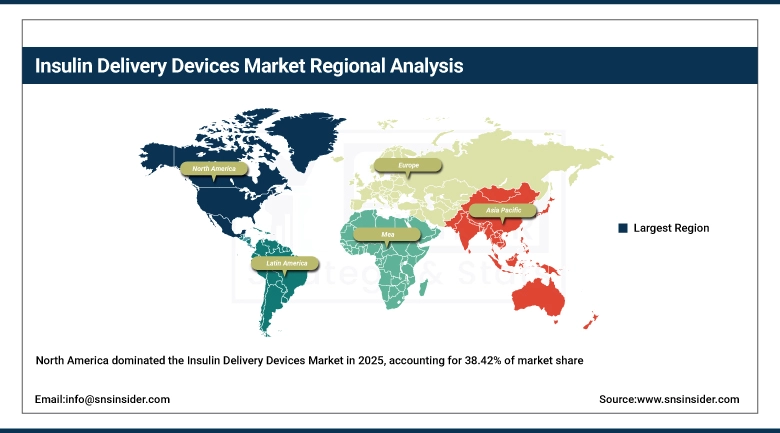

North America accounted for the highest revenue share of more than 38.42% in 2025 of the insulin delivery devices market, driven by the highest per capita healthcare expenditure rates, well-established insurance reimbursement structures for insulin pumps as well as CGM-integrated systems, and the highest concentration of prominent innovators of insulin delivery devices. The region has the advantage of consistent FDA-supported product innovations, high patient advocacy levels for improved diabetes management technologies, and increasing adoption of automated insulin delivery systems among pediatric as well as adult populations of Type 1 diabetics. The U.S. contributes the highest revenue base, driven by the increasing Medicare Advantage coverage of pump reimbursement as well as the highest out-of-pocket spend capacity.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Insulin Delivery Devices Market Insights:

Asia Pacific represents the fastest-growing segment of the insulin delivery devices market, with a CAGR of 9.76%, owing to the rapid growth of the diabetic population, improvement of the healthcare infrastructure, and the increasing investments of the governments of the respective nations towards the management of non-communicable diseases. In the case of China, India, Japan, and Korea, there has been a sharp increase in the adoption of insulin therapy, driven by the increasing coverage of universal health insurance plans, increasing awareness of the condition, and the increasing affordability of mid-tier insulin delivery devices. In addition, the rising manufacturing activities, increasing geographical outreach of the distribution networks of the companies, and the market entries of the companies have all contributed towards the accelerating growth of the Asia Pacific segment of the insulin delivery devices market.

Europe Insulin Delivery Devices Market Insights:

The European market is considered the second-largest market in the insulin delivery device market due to the availability of universal healthcare coverage in the major economies of Europe, the early adoption of hybrid closed-loop systems, and the strong CE mark regulatory efficiency in Europe, which enables the fast market entry of products in the European region. The country-level diabetes management associations in Germany, France, the UK, and Scandinavia are supporting the availability of insulin pumps and smart pens in the European region. The harmonization of the medical device regulations in the European Union, coupled with the increase in reimbursement approvals for automated insulin delivery systems, makes the European market a strategically critical and innovation-receptive market for insulin delivery device manufacturers through the forecast period.

Latin America (LATAM) and Middle East & Africa (MEA) Insulin Delivery Devices Market Insights:

In Latin America and the Middle East and Africa, the rise in the incidence of diabetes, advancements in the diagnostic infrastructure, and the availability of healthcare financing mechanisms are contributing factors in the gradual adoption of insulin delivery devices. The country-level opportunities in these regions are in the form of the highest value in Brazil, Mexico, Saudi Arabia, and the UAE, where the governments have initiated diabetes management programs and are investing in the healthcare sector. The availability of cost-effective insulin pens and needles, multilingual educational initiatives, and the expansion of the distribution channels in the urban pharmacy network are contributing factors in the gradual adoption of the products in these regions.

Insulin Delivery Devices Market Competitive Landscape:

Novo Nordisk A/S, founded in 1923, is the world’s largest insulin producer. It is also the largest manufacturer of insulin device systems, including FlexPen, FlexTouch, and NovoPen. The company’s strong brand portfolio of insulin and insulin device systems, combined with its presence and expertise in endocrinology, has allowed the company to lead the category in both pen-based and digital devices.

-

In February 2025, Novo Nordisk launched the NovoPen 10 smart insulin pen with embedded Bluetooth dose-tracking technology across 15 markets, enabling seamless digital integration with diabetes management applications to improve patient adherence and clinical outcomes monitoring.

Medtronic plc, founded in 1949, is a world leader in insulin pump technology and provides hybrid closed-loop systems under its MiniMed brand name, which combines sophisticated CGM technology and automated basal insulin delivery. Medtronic is committed to investing in new-generation automated insulin delivery technology and pump hardware to maintain its position in the high-end insulin pump market.

-

In June 2024, Medtronic received FDA clearance for its MiniMed 780G system with updated SmartGuard technology, demonstrating 80% average time-in-range in pivotal trials and reinforcing the company’s commercial leadership in the automated insulin delivery devices market.

Insulet Corp. was founded in 2000 and is the maker of the Omnipod tubeless insulin management system, a pioneering wearable patch pump technology that has revolutionized the user experience and adoption rate of insulin pump therapy. The Omnipod 5 Automated Insulin Delivery system from Insulet Corp. marks a new milestone in CGM-based, smartphone-controlled closed-loop insulin management for type 1 diabetes patients.

-

In October 2024, Insulet expanded Omnipod 5 commercial availability to 12 additional international markets, including key Asia-Pacific and Latin American countries, accelerating global penetration of its wearable patch pump platform and strengthening its international revenue base.

Insulin Delivery Devices Market Key Players:

-

Novo Nordisk A/S

-

Sanofi S.A.

-

Eli Lilly and Company

-

Becton, Dickinson and Company (BD)

-

Medtronic plc

-

Insulet Corporation

-

Tandem Diabetes Care, Inc.

-

Ypsomed AG

-

Owen Mumford Ltd.

-

Embecta Corp.

-

B. Braun Melsungen AG

-

Gerresheimer AG

-

Terumo Corporation

-

HTL-Strefa S.A.

-

Roche Diabetes Care

-

Abbott Laboratories

-

CeQur SA

-

Biocon Limited

-

Haselmeier GmbH

-

DEKA Research and Development Corp.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.13 Billion |

| Market Size by 2035 | USD 41.00 Billion |

| CAGR | CAGR of 7.92% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Insulin Pens (Reusable Insulin Pens, Disposable Insulin Pens), Insulin Pumps (Patch Pumps, Tethered Pumps), Insulin Pen Needles (Standard Pen Needles, Safety Pen Needles), Insulin Syringes, and Other Products) • By End Use (Hospitals & Clinics, Homecare, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Novo Nordisk A/S, Sanofi S.A., Eli Lilly and Company, Becton, Dickinson and Company (BD), Medtronic plc, Insulet Corporation, Tandem Diabetes Care Inc., Ypsomed AG, Owen Mumford Ltd., Embecta Corp., B. Braun Melsungen AG, Gerresheimer AG, Terumo Corporation, HTL-Strefa S.A., Roche Diabetes Care, Abbott Laboratories, CeQur SA, Biocon Limited, Haselmeier GmbH, DEKA Research and Development Corp. |

Frequently Asked Questions

The Insulin Delivery Devices Market was valued at USD 19.13 billion in 2025 and is projected to reach USD 41.00 billion by 2035.

The Insulin Delivery Devices Market is expected to grow at a CAGR of 7.92% during the forecast period of 2026–2035.

In the Insulin Delivery Devices Market, the insulin pumps segment is the fastest-growing, with a CAGR of 9.14%.

The homecare segment in the Insulin Delivery Devices Market is expanding quickly, registering a CAGR of 8.64%.

In the Insulin Delivery Devices Market, insulin pens hold the largest share, accounting for approximately 43.56% in 2025.

Get in Touch