Polyamide-imide Market Report Scope & Overview:

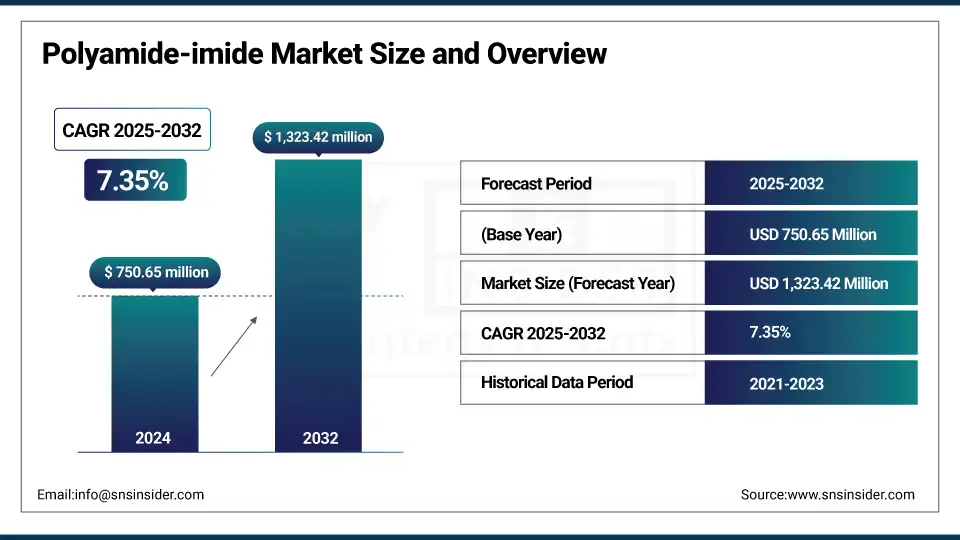

The Polyamide-imide market size was valued at USD 750.65 million in 2024 and is expected to reach USD 1,323.42 million by 2032, growing at a CAGR of 7.35% over the forecast period of 2025-2032.

The polyamide-imide market is experiencing rapid innovation due to its growing use in aerospace, automotive, and electronics sectors for high thermal and chemical resistance. Rising demand for high-performance polymers in lightweight parts and electric vehicles, along with aerospace investments by Boeing and Airbus, is fueling growth. Advances in coatings and wire enamels further support the expansion of the polyamide-imide market. Notably, Solvay and Ensinger have expanded their PAI resin solutions, reflecting changing industry needs.

To Get more information On Polyamide-imide Market - Request Free Sample Report

According to U.S. ITC and European Chemical Agency data, global export regulations and sustainability standards are shaping the size and dynamics of the polyamide-imide market. The market share is significantly influenced by North America’s leadership in aircraft manufacturing and Asia’s growth in electronics. Analysis of the polyamide-imide market shows rising demand for wire insulation and wear-resistant parts. Market trends also include bio-based formulations and circular production methods. Leading polyamide-imide companies such as Solvay, Ensinger, and Kermel are actively expanding their material offerings.

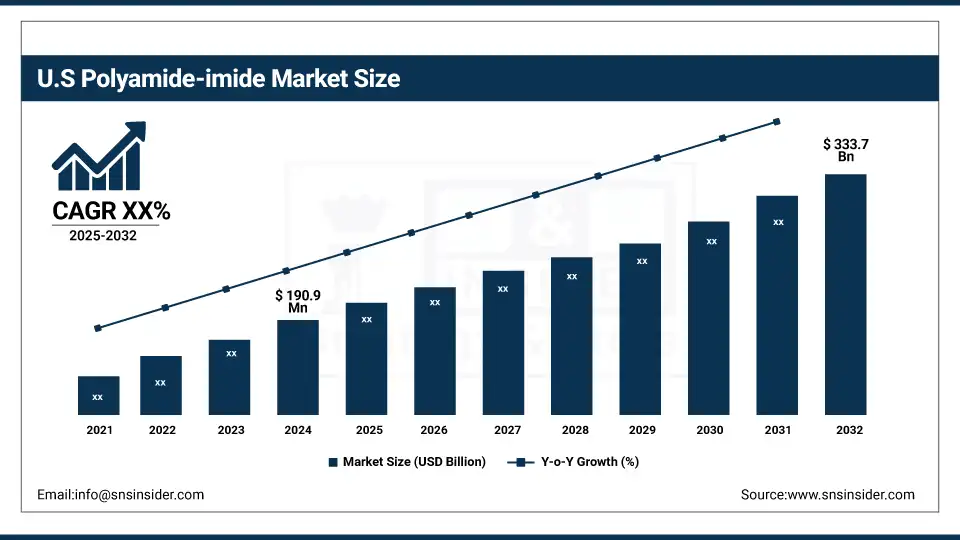

The U.S. leads holding a market share of about 74% with a market value of USD 190.9 million in 2024 and is projected to reach value of USD 333.7 million by 2032, with extensive R&D investments and regulatory support encouraging the use of PAI resin in the aerospace and automotive sectors. Wire enamels and injection molding PAI parts are increasingly utilized, supported by agencies like the U.S. Department of Energy, promoting energy efficiency. Canada’s growing industrial base also contributes to regional strength, reinforcing North America’s market leadership.

Market Dynamics:

Drivers:

-

Growing demand for sustainable high‑temp polymer materials fuels polyamide-imide market growth

Innovations in sustainable high‑temp polymer materials are propelling demand for polyamide‑imide across diverse applications. End‑user sectors such as aerospace and offshore oil operations seek materials with reduced carbon footprint and superior thermal stability. Manufacturers are formulating bio‑based variants to meet environmental regulations and corporate responsibility goals. government agencies emphasize durability and recyclability, positioning polyamide‑imide as a strategic solution. These trends encourage investment and adoption by polyamide‑imide market companies.

-

Increased utilization of glass‑filled polyamide‑imide enhances performance in high‑stress environments

Glass‑filled polyamide‑imide is gaining traction for use in components subject to mechanical stress and elevated temperatures in railway and marine applications. enhanced stiffness and dimensional stability under load make it preferable to competing polymers. suppliers such as Solvay and Toray have expanded their offerings of reinforced grades to meet industrial performance demands. regulatory pressure for lightweight, durable materials further supports this transition, boosting polyamide‑imide market growth across transportation sectors.

Restraints:

-

Complex conditions for coating and film applications slow scale in electronics sectors

Coating and film applications require stringent thermal curing and chemical control parameters, adding complexity to manufacturing of polyamide-imide components. quality assurance demands specialized equipment and laboratory-grade environments, raising throughput costs. electronics and semiconductor industries especially struggle with consistency under scale. such operational constraints limit entry by mid-tier manufacturers and delay broader acceptance in consumer technology supply chains. this operational barrier restricts polyamide-imide market growth in coating and film applications.

Segmentation Analysis:

By Grade

Glass-filled held a dominant polyamide-imide market share of 43.50% in 2024 due to its superior mechanical strength and thermal stability. This grade is widely adopted in automotive and aerospace sectors where durability and lightweight components are critical. The U.S. Environmental Protection Agency supports glass-filled polymers for emissions reduction and fuel efficiency. Companies like solvay have expanded glass-filled resin production, reinforcing this segment’s leadership in the polyamide-imide market by meeting growing industrial demand and regulatory standards.

Carbon-filled is the fastest growing with the highest CAGR of 7.65% during the forecast period over 2025 to 2032, driven by its high strength-to-weight ratio in industrial machinery and defense applications. The national institute of standards and technology reports increased use in energy-efficient solutions. Government investments in advanced manufacturing boost demand. Carbon-filled polyamide-imide composites’ ability to reduce weight while enhancing performance positions this subsegment as a key driver of polyamide-imide market growth globally.

By Type

Thermoplastic held a dominant polyamide-imide market share of 41.40% in 2024 due to its recyclability and ease of processing. It is preferred for electrical insulation and automotive lightweighting. The American Chemistry Council highlights thermoplastics’ rising demand driven by environmental compliance. Thermoplastic polyamide-imide’s flexibility and economic benefits encourage adoption across industries. Leading companies focus research on thermoplastic grades to meet evolving regulations and application needs, sustaining this segment’s dominance in the polyamide-imide market.

Thermoset is the fastest growing with the highest CAGR of 7.45% during the forecast period over 2025 to 2032, driven by its superior heat resistance and chemical stability in aerospace and oil & gas sectors. The U.S. Department of Energy highlights thermoset polymers’ advantages under extreme conditions. Investments by companies like toray in thermoset processing facilities are expanding capacity. This segment’s robustness makes it critical for demanding applications, underpinning strong growth in the polyamide-imide market.

By Form

Resin held a dominant polyamide-imide market share of 39.80% in 2024 due to its essential role in molding and coating applications. The U.S. Environmental Protection Agency emphasizes resin’s durability and recyclability, supporting sustainable manufacturing. Resins are integral in automotive and electronics industries, where leading companies have expanded capacities to meet demand. Compliance with environmental regulations further strengthens resin’s market leadership. Its versatility and core application role ensure resin’s dominance within the polyamide-imide market.

Coatings are the fastest growing with the highest CAGR of 7.61% during the forecast period over 2025 to 2032, driven by innovations in protective and insulating coatings for aerospace and electronics. The national institute of standards and technology confirms improved formulations enhancing lifespan and resistance. Government programs promoting energy efficiency in coatings amplify demand. Polyamide-imide companies increasingly develop coating-specific resins, fueling rapid growth in this subsegment within the polyamide-imide market.

By Manufacturing Process

Reaction injection molding held a dominant polyamide-imide market share of 36.90% in 2024 due to its efficiency in producing complex, high-strength PAI parts. The American Chemistry Council reports RIM’s cost-effectiveness and precision boost adoption in automotive and aerospace sectors. Polyamide-imide companies invest in advanced RIM technologies to meet quality standards, driving dominance. This process’s ability to create durable, lightweight components supports its leading position in the manufacturing segment of the polyamide-imide market.

Compression molding is the fastest growing with the highest CAGR of 7.78% during the forecast period over 2025 to 2032, driven by its suitability for high-volume production of reinforced PAI composites. The U.S. Department of Energy highlights its energy efficiency and material utilization benefits. Expansion of compression molding facilities by key players supports growing demand in defense and industrial machinery sectors. These advantages make compression molding a key growth driver in the polyamide-imide market.

By Application

Wire enamels held a dominant polyamide-imide market share of 29.70% in 2024 due to their critical role in electrical insulation for motors and transformers. The U.S. Energy Information Administration highlights advanced insulating materials’ importance in improving energy efficiency. Polyamide-imide companies have tailored wire enamel formulations to comply with evolving standards, reinforcing dominance. This segment’s essential function in electrical infrastructure secures its leadership position within the polyamide-imide market.

High-temperature adhesives are the fastest growing with the highest CAGR of 8.07% during the forecast period from 2025 to 2032, driven by expanding aerospace and electronics applications requiring durable bonding under extreme conditions. The National Institute of Standards and Technology notes advances in thermal and chemical resistance. Government support for advanced adhesives accelerates adoption. These factors make high-temperature adhesives a significant growth driver in the polyamide-imide market.

By End-use Industry

Automotive held a dominant polyamide-imide market share of 35.40% in 2024 due to its lightweighting needs and high-temperature component applications. The U.S. Environmental Protection Agency’s vehicle emissions reduction initiatives promote materials like polyamide-imide for performance improvement. Collaborations between automotive manufacturers and polyamide-imide companies for custom grades strengthen this segment’s leadership. Its critical role in engine and electrical systems secures automotive’s dominant position in the polyamide-imide market.

Aerospace & defense is the fastest growing with the highest CAGR of 7.97% during the forecast period over 2025 to 2032, driven by demand for heat-resistant, lightweight composites in aircraft and military use. The Federal Aviation Administration encourages advanced materials adoption for improved fuel efficiency. Companies such as Solvay have increased aerospace-specific polyamide-imide formulations. This sector’s strict safety and performance standards fuel rapid growth, driving the polyamide-imide market forward.

Regional Analysis

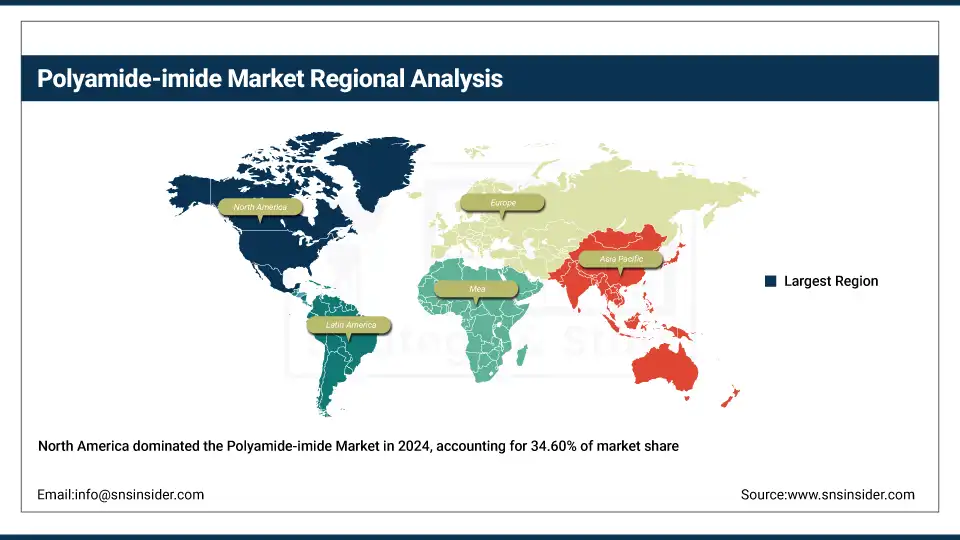

North America is dominating the polyamide-imide market with a significant market share of 34.60% in 2024, driven by its advanced manufacturing infrastructure and early adoption of sustainable high‑temp polymer materials.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region with the highest CAGR of 7.72% from 2025 to 2032, driven by expanding electronics manufacturing and automotive sectors. China leads with massive investments in injection molding PAI parts and sustainable polymer initiatives. Japan and South Korea contribute through innovations in coating and film applications. Government programs encouraging lightweight materials and energy efficiency bolster demand for polyamide-imide, positioning the Asia Pacific as a dynamic growth hub in the global market.

Europe ranks as the third dominating region with a 27.20% market share in 2024, propelled by strong demand for glass-filled polyamide‑imide in automotive and electrical sectors. Germany leads due to its robust automotive industry and environmental regulations favoring high-performance polymers. The European Chemicals Agency supports advanced coating and film applications, facilitating market growth. France and Italy also contribute through aerospace innovations, collectively sustaining Europe’s significant role in the polyamide-imide market’s regional landscape.

Key Players:

The major polyamide-imide market competitors include Solvay SA, Toyobo Co., Ltd., Mitsubishi Gas Chemical Co., Inc., Toray Industries, Inc., Elantas GmbH, Innotek Technology Ltd., Kermel S.A., Ensinger GmbH, Evonik Industries AG, Hitachi Chemical (Showa Denko), Showa Denko Materials Co., Ltd., Boyd Corporation, Quadrant Group, PanJin Zhongrun High Performance Polymers Co., Ltd., Shanghai Songhan Plastics Technology Co., Ltd., Symmtek Polymers (KT Plastics), Fujifilm, and AFT Fluorotec Ltd.

Recent Developments:

-

In July 2025, Arkema introduced the Zenimid brand for its high-performance polyimide range, highlighting thermal resistance and durability for aerospace and electronics, reinforcing its market positioning in advanced polymer applications.

-

In April 2025, Confluent Medical launched Ultra Polyimide tubing, offering nearly double the strength of standard polyimide, with thinner walls and solvent-free manufacturing, enhancing safety and compliance in medical device applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 750.65 million |

| Market Size by 2032 | USD 1,323.42 million |

| CAGR | CAGR of 7.35% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Grade (Unfilled, Glass-Filled, Carbon-Filled, Metal-Filled) •By Type (Thermoset, Thermoplastic) •By Form (Resin, Coatings, Films, Fibers) •By Manufacturing Process (Reaction Injection Molding (RIM), Compression Molding, Extrusion, Solution Casting, Others) •By Application (Wire Enamels, Coatings, High-temperature Adhesives, Seals & Bearings, Films & Tapes, Structural Parts (Molded), Fibers, Others) •By End-use Industry (Automotive, Aerospace & Defense, Electrical & Electronics, Industrial Machinery, Oil & Gas, Healthcare, Textile, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Solvay SA, Toyobo Co., Ltd., Mitsubishi Gas Chemical Co., Inc., Toray Industries, Inc., Elantas GmbH, Innotek Technology Ltd., Kermel S.A., Ensinger GmbH, Evonik Industries AG, Hitachi Chemical (Showa Denko), Showa Denko Materials Co., Ltd., Boyd Corporation, Quadrant Group, PanJin Zhongrun High Performance Polymers Co., Ltd., Shanghai Songhan Plastics Technology Co., Ltd., Symmtek Polymers (KT Plastics), Fujifilm, and AFT Fluorotec Ltd. |

Frequently Asked Questions

The Polyamide-imide market was valued at USD 750.65 million in 2024 and is projected to reach USD 1,323.42 million by 2032, growing steadily.

Key growth drivers include rising demand for high-performance polymers in aerospace, EVs, wire enamels, and sustainable high?temp polymer materials across industrial sectors.

North America dominates with a 34.60% share, led by the U.S., while Asia Pacific is the fastest-growing with a 7.72% CAGR from 2025 to 2032.

Molding resins dominate due to their widespread use in injection molding PAI parts for lightweight, heat-resistant applications in automotive and aerospace industries.

Wire enamels are growing fast due to rising demand for thermal insulation in motors and transformers, supported by energy-efficiency initiatives and advanced PAI formulations.

Get in Touch