Polyols Market Report Scope & Overview:

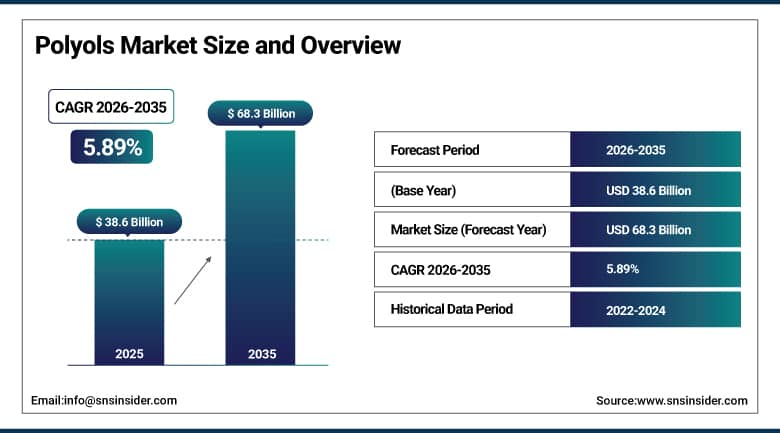

The Polyols Market was valued at USD 38.6 Billion in 2025 and is expected to reach USD 68.3 Billion by 2035, growing at a CAGR of 5.89% from 2026–2035.

The Polyols Market is witnessing rapid growth due to increased use of polyurethane foam in construction, automobile, and insulation industries. Increased use of energy-efficient buildings and lightweight vehicles is leading to increased consumption of rigid and flexible foams. Increased activity within the packaging and furniture sectors is adding impetus to market growth. Furthermore, increased use of bio-polyols, advanced polyurethane technology, and an increased demand for sustainable products are further fueling market growth. Urbanization and industrialization in emerging markets are further adding to increased usage.

According to the International Energy Agency, buildings account for nearly 30% of global final energy consumption, reinforcing strong demand for insulation materials such as polyurethane foams derived from polyols. Furthermore, World Bank data highlights that over 56% of the global population resides in urban areas as of 2024, with this share projected to reach around 68% by 2050, significantly driving construction activity and housing development, which in turn supports sustained demand for polyols across insulation, furniture, and building applications.

Polyols Market Size and Forecast:

-

Market Size in 2026E: USD 40.85 Billion

-

Market Size by 2035: USD 68.3 Billion

-

CAGR: 5.89% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Polyols Market - Request Free Sample Report

Polyols Market Trends:

-

Rising demand for polyurethane foams in construction, automotive, and furniture industries driving strong consumption of polyols as a key raw material

-

Growing focus on energy-efficient insulation materials boosting adoption of polyols in rigid foam applications for thermal insulation in buildings and appliances

-

Increasing use of bio-based and renewable polyols supported by sustainability initiatives and shift toward eco-friendly chemical production

-

Expanding applications in automotive lightweighting and interior components to improve fuel efficiency and reduce vehicle emissions

-

Rising demand from packaging, adhesives, and coatings industries supporting overall growth of polyols in diverse industrial formulations

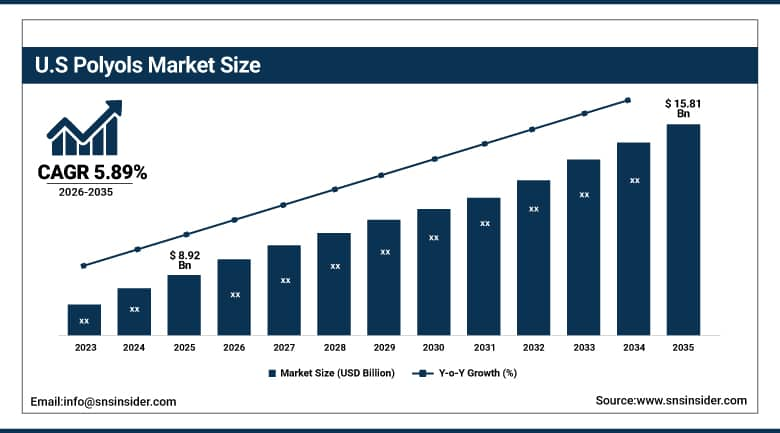

U.S. Polyols Market Outlook:

The U.S Polyols Market was valued at USD 8.92 Billion in 2025 and is expected to reach USD 15.81 Billion by 2035, growing at a CAGR of 5.89% from 2026–2035.

The United States leads North American polyols revenues through its large construction insulation market driven by DOE energy code requirements, the automotive industry’s flexible foam seating and interior component procurement, and the furniture and bedding manufacturing sector’s consistent foam demand. Dow Inc., Huntsman International, and Covestro sustain U.S. market leadership through their comprehensive polyether and polyester polyol portfolios serving both rigid insulation and flexible cushioning applications across construction and consumer goods sectors.

According to the U.S. Energy Information Administration, buildings account for around 40% of total U.S. energy consumption, making energy efficiency a major priority. This significantly drives demand for insulation materials, including polyurethane foams derived from polyols, used to reduce energy loss.

Polyols Market Segment Analysis:

-

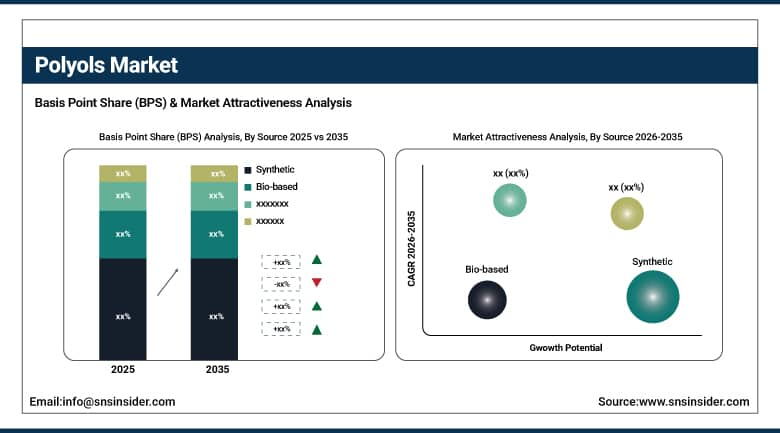

By Source, Synthetic segment dominated the Polyols Market in 2025 with 86% share; Bio-based segment is the fastest growing segment.

-

By Type, Polyether Polyols segment dominated the market in 2025 with 61% share; Polyester Polyols segment is the fastest growing segment.

-

By Application, Flexible Foam segment dominated the market in 2025 with 48% share; Rigid Foam segment is the fastest growing segment.

-

By End-Use Industry, Building & Construction segment dominated the market in 2025 with 39% share; Automotive segment is the fastest growing segment.

By Source, synthetic polyols segment dominates the polyols market, while bio-based polyols segment is the fastest-growing segment

Synthetic polyols dominated the market in 2025 owing to consistent quality, large volumes and cost efficiency involved in their production for industrial PU applications. Synthetic polyols have broad application potential in construction, automotive, furniture, and insulation sectors. Their chemically stable nature makes them preferable than their natural counterparts, and thus, companies can benefit from established supply chains and manufacturing capabilities. The increasing demand for flexible and rigid foams is expected to continue making synthetic polyols dominant in the global polyols market.

Bio-based polyols are the fastest growing segment driven by sustainability concerns, regulatory pressure for eco-friendly chemicals, and demand for low carbon emission products. These products are obtained from renewable raw material sources and are mainly utilized in green construction, automotive interior, and packaging applications. Increasing emphasis on eco-friendliness, along with improved performance characteristics, will drive the use of such polyols across end-use applications. Many companies will invest in innovation activities involving eco-friendly solutions to align with ESG objectives.

By Type, polyether polyols segment dominates the polyols market, while polyester polyols segment is the fastest-growing segment

Polyether polyols dominated the market in 2025 owing to their flexibility, hydrolytic stability, and low-cost in the process of producing polyurethanes. They are largely consumed in applications involving flexible foams such as in furniture, beddings, automobile seats, and insulations. Processability and suitability for use in several formulas make them the choice for manufacturers. Growing consumption from both construction and consumer goods industries would further consolidate their leading position. Usage in industries on a consistent basis would ensure dominance of polyether polyols in the market scenario.

Polyester polyols are the fastest growing segment due to properties of higher strength, resistance against chemicals and suitability in the production of rigid foams among others. These are employed in various industries in coatings, sealants, adhesives, and elastomers. Growing demand for tough insulation materials and lightweight automobile parts are contributing to their rising consumption. Growing activity in the construction sector and development of infrastructures would also drive their consumption. Enhanced durability provided by polyester polyols would accelerate growth in demand.

By Application, flexible foam segment dominates the polyols market, while rigid foam segment is the fastest-growing segment

Flexible foam dominated the Polyols Market in 2025 owing to its extensive application in furniture, bedding, automobile seats, and packaging. The cushioning and lightweight nature of this product make it an ideal choice for commercial as well as industrial purposes. Demand for the same has been fueled by growing consumption of residential furniture and automotive seating. In addition, the cost-efficiency and ease in production have helped the segment retain its leadership position. The rise in urbanization and increasing consumer lifestyle standards are expected to favor its growth in the coming years.

Rigid foam is the fastest growing segment owing to increasing requirements for insulating and energy-efficient materials in buildings, refrigerators, and other industry applications. It has excellent insulating qualities along with high resistance and durability that make it suitable for constructing insulated walls and storage systems in industries. Growing emphasis on sustainable buildings and energy conservation is helping drive its growth. Growing need for rapid urban infrastructure developments has also been favoring its demand in recent years.

By End-Use Industry, building & construction segment dominates the polyols market, while automotive segment is the fastest-growing segment

The Building & Construction segment dominated the market in 2025 due to high usage of polyols for insulation purposes, as well as sealants and structural foams. Polyols are applied for enhancing energy efficiency of constructions and their use in roofings and walls insulation. The key factors stimulating the growth of this sector include urbanization processes, infrastructure development, and increased number of construction works. The rising focus on sustainability of buildings and their energy-saving properties contributes to growth of segment significantly.

The Automotive segment is the fastest growing owing to the increased consumption of polyols in production of lighter and efficient materials in automotive sector. The polyols are applied in various car parts such as seat coverings, interior and exterior insulation, as well as noise reduction systems. The growing need in fuel-efficiency vehicles contributes to high application rate of polyols in manufacturing sector. Growth in global automotive production and innovative solutions related to lightweight materials boost the segment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

48.6% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Middle East & Africa |

Saudi Arabia |

22.8% |

|

Latin America |

Brazil |

43.8% |

Asia Pacific Polyols Market Insights

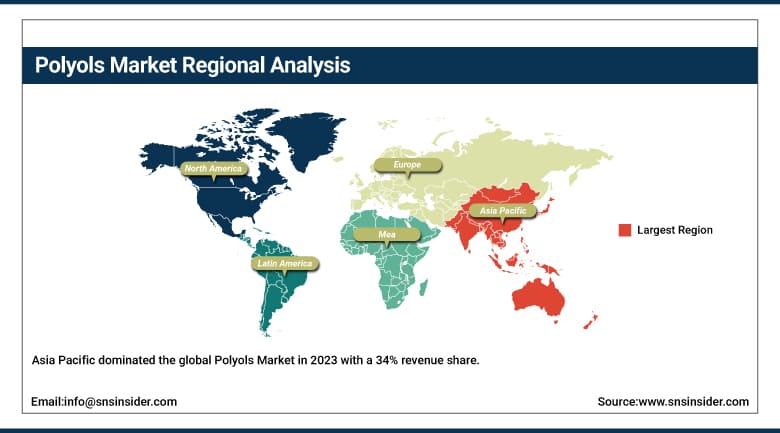

Asia Pacific dominated the global Polyols Market in 2023 with a 34% revenue share, driven by rapid industrialisation and urbanisation in China and India creating substantial construction insulation and automotive foam demand. China accounts for approximately 48.6% of Asia Pacific revenues through its massive construction sector’s rigid foam insulation procurement, the world’s largest automotive production base’s flexible foam seating demand, and the domestic presence of Wanhua Chemical’s integrated polyol manufacturing capacity.

According to the automotive sector, Asia produces over 50% of global vehicles, significantly increasing demand for lightweight polyurethane components used in seating, insulation, and interior applications to improve fuel efficiency and vehicle performance.

According to the World Bank, Asia accounts for more than 50% of global urban population growth, driving large-scale construction activity and increasing demand for polyurethane-based materials in residential and commercial infrastructure development.

India represents the most commercially dynamic emerging market within Asia Pacific, where rapidly growing construction activity under national housing programmes, the expanding automotive manufacturing sector’s flexible foam component sourcing, and growing furniture manufacturing capacity collectively create above-regional-average polyols demand growth. Japan and South Korea’s advanced automotive and electronics manufacturing sectors contribute premium regional demand.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Polyols Market Insights

North America is a significant polyols market where the United States’ large construction insulation sector driven by DOE energy code requirements, the automotive industry’s flexible foam component procurement, and the furniture manufacturing sector’s consistent foam demand create substantial regional consumption. The United States accounts for approximately 82.5% of North American revenues through Dow, Huntsman, and Covestro’s comprehensive polyol manufacturing and distribution infrastructure.

According to the U.S. Department of Energy, improving building insulation can reduce overall energy consumption by 20–30%. This substantial efficiency gain is increasing the adoption of polyurethane foam-based insulation materials, thereby supporting strong demand growth for polyols across construction applications.

According to the U.S. Census Bureau, the construction sector contributes over 4% of U.S. GDP. This steady economic contribution supports ongoing infrastructure development and construction activity, further driving demand for foam-based materials and polyols in building applications.

Canada contributes supplementary North American revenues through its construction sector’s insulation material demand in its cold climate building stock, the automotive parts manufacturing sector’s flexible foam procurement for Ontario-based vehicle assembly operations, and the growing focus on energy-efficient building retrofit programmes creating rigid foam insulation specification.

Europe Polyols Market Insights

Europe is a significant polyols-consuming region, driven by the demand for insulation in low-income households and favourable regulatory support for energy efficiency upgrades under the EU’s Energy Performance of Buildings Directive. Germany accounts for approximately 22.4% of European revenues through its large automotive sector’s flexible foam seating procurement, the construction industry’s rigid foam insulation demand, and Covestro’s German manufacturing leadership.

According to Eurostat, construction contributes approximately 5–6% of EU GDP, with a strong focus on energy-efficient building materials. This supports steady demand for insulation solutions used in residential and commercial construction activities across Europe. According to the European Commission, the Energy Performance of Buildings Directive targets zero-emission buildings by 2050. This is increasing demand for high-performance insulation materials to improve energy efficiency and reduce carbon emissions.

According to the European Environment Agency, buildings account for nearly 40% of Europe’s energy consumption, making insulation a key driver for energy reduction and supporting the adoption of advanced building efficiency materials.

MEA & Latin America Polyols Market Insights

Saudi Arabia leads MEA revenues at approximately 22.8% through its growing petrochemical sector’s polyol production capacity, the construction sector’s insulation material demand under Vision 2030 infrastructure investment, and the automotive assembly sector’s flexible foam component sourcing. UAE’s construction boom contributes growing regional demand for rigid foam insulation materials.

Brazil leads Latin American revenues at approximately 43.8% through its large furniture and bedding manufacturing sector’s flexible foam consumption, the automotive sector’s component procurement, and the construction industry’s growing insulation material adoption. Mexico’s large automotive manufacturing sector for North American export creates substantial flexible foam polyol procurement from regional suppliers.

Market Dynamics:

Growth Drivers: Energy efficiency building codes mandating insulation upgrades and automotive lightweighting creating structured polyol demand growth

The polyols market’s consistent growth is driven by the global construction sector’s progressive building energy code tightening, where mandatory insulation R-value increases across developed and emerging markets create structured rigid foam polyol demand whose growth tracks both new construction activity and the expanding building retrofit and renovation market addressing existing inadequately insulated building stock. The rise in construction activities globally, coupled with stringent energy regulations, has led to a surge in the use of polyols in this sector, with companies increasingly incorporating polyols into building materials to improve energy efficiency and sustainability.

Restraints: Petroleum feedstock price volatility and growing bio-based alternative competition creating margin pressure on conventional polyol producers

Polyol production’s dependence on propylene oxide and ethylene oxide feedstocks whose pricing tracks crude oil and natural gas commodity markets creates manufacturing cost volatility that conventional polyether polyol producers cannot fully hedge through long-term supply contracts whose pricing structures lag spot market fluctuations. Each petroleum feedstock price spike that increases polyol production costs creates margin pressure on producers whose customer pricing agreements may not permit rapid cost pass-through in competitive commodity foam markets.

Opportunities: Bio-based polyol commercial scale-up and emerging market construction growth creating premium and volume expansion opportunities

Bio-based polyol commercial scale-up, where vegetable oil-derived and recycled content polyols achieve cost-competitive economics with conventional petroleum-based alternatives while delivering documented sustainability credentials, creates a premium product category whose growing brand owner specification preference sustains above-commodity pricing. Consumer awareness and preferences are also playing a crucial role in driving the demand for bio-based polyols, with manufacturers developing innovative formulations to meet evolving sustainability expectations across construction, automotive, and furniture end markets.

Recent Developments:

-

2024: Wanhua Chemical Group expanded polyol production capacity at its Yantai integrated petrochemical complex, adding new polyether polyol manufacturing lines to serve growing domestic and export demand from China’s construction and automotive foam sectors.

-

2023: Covestro AG launched its Baynat bio-based polyol product line incorporating renewable plant-derived feedstocks for flexible foam applications in furniture and automotive seating, providing reduced carbon footprint materials matching conventional polyether polyol performance.

-

2025: Tosoh Corporation announced expansion of polyols production capacity at its Nanyo complex in Japan, aiming to meet rising domestic and export demand from the construction insulation and automotive flexible foam sectors across the Asia Pacific region.

Polyols Market Key Players are:

-

BASF SE

-

Dow Inc.

-

Covestro AG

-

Huntsman Corporation

-

Shell Chemicals

-

Mitsui Chemicals, Inc.

-

Repsol S.A.

-

ExxonMobil Chemical Company

-

LyondellBasell Industries N.V.

-

Eastman Chemical Company

-

Cargill, Incorporated

-

Stepan Company

-

INEOS Group

-

SABIC

-

Arkema S.A.

-

Bayer AG

-

FENC

-

Tosoh Corporation

-

Perstorp Holding AB

-

Wanhua Chemical Group Co., Ltd.

Polyols Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 38.6 Billion |

| Market Size by 2035 | USD 68.3 Billion |

| CAGR | CAGR of 5.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Synthetic, Bio-based) • By Type (Polyether Polyols, Polyester Polyols) • By Application (Rigid Foam, Flexible Foam, Coatings, Adhesives & Sealants, Elastomers, Plasticizers, Others) • By End-Use Industry (Building & Construction, Automotive, Furnishings & Bedding, Packaging, Electronics & Electricals, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Covestro AG, Huntsman Corporation, Shell Chemicals, Mitsui Chemicals, Inc., Repsol S.A., ExxonMobil Chemical Company, LyondellBasell Industries N.V., Eastman Chemical Company, Cargill, Incorporated, Stepan Company, INEOS Group, SABIC, Arkema S.A., Bayer AG, FENC, Tosoh Corporation, Perstorp Holding AB, Wanhua Chemical Group Co., Ltd. |

Frequently Asked Questions

The Polyols Market is expected to grow at a CAGR of 5.89% from 2026 to 2035.

The Polyols Market was valued at USD 38.6 Billion in 2025.

Energy efficiency codes, automotive lightweighting, and bio-based polyols drive Polyols Market growth globally.

The Polyether Polyols segment dominated the Polyols Market.

Asia Pacific dominated the Polyols Market in 2025.

Get in Touch