Polyurethane Catalyst Market Report Scope & Overview:

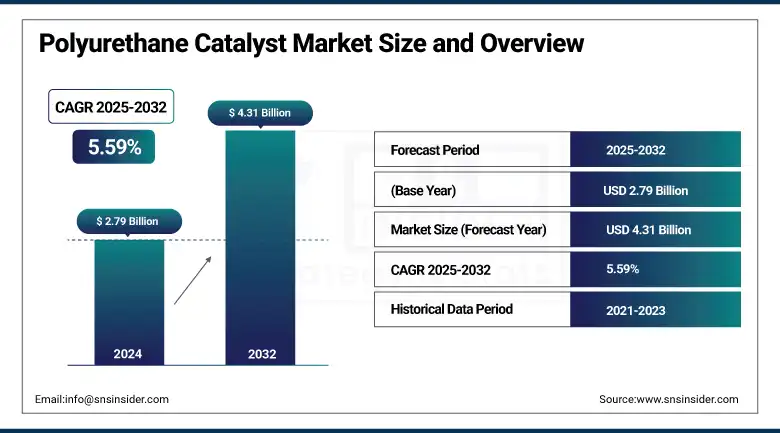

The Polyurethane Catalyst Market size was valued at USD 2.79 billion in 2024 and is expected to reach USD 4.31 billion by 2032, growing at a CAGR of 5.59% over the forecast period of 2025-2032.

Polyurethane catalyst market growth is driven by the growing demand for energy-efficient and lightweight materials in various end-users such as automotive, construction, and electronics. Growing sustainability influences contribute to the demand for polyurethanes based on bio or tin catalysts.

To Get more information On Polyurethane Catalyst Market - Request Free Sample Report

-

For example, the expansion of the Catalyst Development and Solids Processing Center of BASF in Ludwigshafen, Germany, is a hub of innovation in the polyurethane catalysts market.

Moreover, the U.S. is at the forefront, accounting for over USD 452.63 million of the market, with a share of 75% in 2024. Government programs, like the U.S. Infrastructure Investment Act, continue to speed up green building agendas and Polyurethane Additives. BASF’s 2023 capacity increase at its Geismar, Louisiana, plant raised production by 20%. Furthermore, the U.S. Department of Energy states that polyurethane foam insulation delivers an R-value of 6.0 per inch, maximizing thermal performance, driving continued growth and innovation in the polyurethane catalyst market.

Polyurethane Catalyst Market Dynamics

Drivers

-

Growing Adoption of Bio-Based Polyurethane Catalysts Boosts Sustainability in Production

Rising demand for sustainable solutions is anticipated to fuel the bio-based polyurethane catalysts market growth. The trend toward greener products is also leading companies like BASF to advance with the development of bio-based catalysts. To further support sustainability in a broad range of polyurethane applications, BASF had planned to introduce bio-based catalysts in 2024. Energy-efficient polyurethane products are helping reduce carbon footprints, and the same is driving demand for bio-based polyurethane catalysts, informs the U.S. Department of Energy. The growing trend towards ecological and sustainable substitutes in the automotive, construction, and packaging industries further drive market growth.

-

Increased Demand for Energy-Efficient Insulation Materials Propels Polyurethane Catalyst Market Growth

Energy-cured construction materials, namely, polyurethane insulations, are the main reason for the polyurethane catalyst market growth. Polyurethane insulation provides the best thermal resistance on the market, which means less energy consumption. Polyurethane foam insulation installed according to the manufacturer is one of the best for reducing heating and cooling costs, with an R-6.0 per inch. Following in the footsteps of global energy-saving movements such as the U.S. Infrastructure Investment Act, which encourages the use of energy-saving building materials, demand is on the rise for innovative insulation products in the polyurethane catalyst market. This growing demand for energy-efficient construction materials is driving market growth.

Restraints

-

Health and Environmental Regulations on Toxic Catalysts Impede Market Expansion

Health and environmental issues of toxic catalysts, such as tin-based compounds, are limiting the market growth. Stringent regulations on chemicals involved in the production of polyurethane have been defined by agencies such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA). These restrictions are intended to limit the detrimental impact of hazardous catalytic materials on users of the catalysts and the environment. Challenges such as high prices involved in meeting the green standards are restraining the polyurethane catalyst market growth.

-

Emerging Competitors from Alternative Materials Challenge Polyurethane Catalyst Demand

Increasing applications and use of substitutes, which do not utilize polyurethane catalyst, are posing a challenge to the market. In the construction and automotive industries, alternatives to polyurethane, such as epoxy resin, are becoming popular because of their comparable capabilities and reduced catalyst quantities. Increasingly successful are new foam materials, which achieve insulating performance ranges that are competitive with polyurethane. It is anticipated that these developments will restrict the application of polyurethane catalysts, in particular in industries in which low-cost, catalyst-free materials are desirable.

Polyurethane Catalyst Market Segmentation Analysis

By Type

The amine segment dominated the polyurethane catalyst market, which accounted for a 50.3% share of the total market in 2024. This predominance is mostly due to its indispensable contribution to the production of high-performance polyurethane foams. Amine catalysts are commonly employed for automotive and construction applications due to their fast-curing advantage, offering production efficiency. For example, major companies like BASF have applied such amine-based catalysts a lot in the development of PU, since they are low-cost and efficient for the control of the properties and performance of PU.

The metal catalyst emerged as the fastest-growing in terms of volume, with a CAGR of 6.78% in 2024. This increase is due to the rising use of polyurethane materials in the automobile and construction industries, where metal catalysts have better durability and performance, specifically in the production of rigid foams and coatings. With the continuous development of sustainability demands for more sustainable materials, the metal-based catalysts, which can improve the mechanical and durable properties of polyurethane products, become popular all the time.

By Functionality

The gelling catalyst is the largest segment in the polyurethane catalyst market based on functionality, holding 39.8% of the market share. Amine based gelling catalysts sub-segment is particularly important in the manufacture of flexible foams that are commonly employed in automotive seats, furniture, and bedding. Amine-containing catalysts offer predictable gelling and a thermo-catalytic temperature dependence, and a stable reaction time that leads to foams with good quality. Their significance is based on the capacity for boosting productivity in mass production.

The cross-linking catalyst is the fastest-growing segment with a CAGR of 7.46%. This rise in demand is attributed to the growing demand for high-performance polyurethane coatings and adhesives that necessitate the usage of cross-linked structures for enhanced strength and durability. Cross-linked foam is in particularly high demand in the electronics and automotive markets, where the above-average material strength has a huge bearing on the performance of the material being used in high-stress environments.

By Application

The Elastomer application dominated the polyurethane catalyst market industry in 2024 and accounted for over 38.2% of the share. The largest subsegment in this category is flexible polyurethane elastomers found in automotive components, footwear, and industrial uses. Having high durability also being resistant to harsh conditions, they are also indispensable materials for certain industries. Companies such as Huntsman are developing the advancement of polyurethane elastomers, which can offer improved material qualities across various applications.

The foam application is projected to be the fastest-growing at an impressive CAGR of 6.57%. Foam-based materials in general, specifically insulation in construction and lightweight components in automotive, are the reason behind this development. The excellent thermal insulation of polyurethane foam and stampable properties significantly promote its wide acceptance. Firms like Covestro have been investing in their expansion in diagnostics to respond to the demand, prioritizing sustainable options in the production of foam.

By End Use Industry

Based on end-use industry, the polyurethane catalyst market was led by the construction industry with 41.5% share of total market volume in 2024. Polyurethane systems are also key to the manufacture of rigid foam insulation for buildings, helping to conserve energy. This demand is supported by global environmental targets, particularly in countries such as the US and Europe, where legislation promotes energy-efficient materials in building. Driving this has been leading manufacturers' desire to develop their polyurethane products' insulation performance.

Automotive is expected to be the fastest-growing segment in 2024, registering a CAGR of 5.3%. It is mainly due to the rising demand for lightweight materials and polyurethane-based parts in automotives such as seats, insulators, and sound damping. With automotive companies under constant pressure to deliver enhanced fuel economy and sustainability, the application of polyurethane catalysts for the production of lighter, longer-lasting parts is rapidly proliferating. Innovations and product advancements, BASF is one of the leaders in the automotive PU segment.

Polyurethane Catalyst Market Regional Outlook

North America is the fastest-growing region, boasting the highest CAGR of 6.36% during the forecast period from 2025 to 2032, owing to energy-efficient building and automotive sector developments. The increase is driven by EPA rulings supporting low-VOC polyurethane additives and tin catalyst polyurethane. Huntsman and BASF are leading the way in flexible foams and insulation breakthroughs. Growth of 7.8% in construction underpins higher polyurethane demand in Canada. Market expansion is enhanced by green building programs such as LEED, which are reinforcing sustainability-centric polyurethane catalyst market trends and eco-friendly product development.

Europe held 28.3% of the polyurethane catalyst market in 2024, owing to the stringent EU green regulations and the mature construction industry. Germany is in the lead, supported by an automotive catalyst and innovations from Covestro AG. France and Italy are next with green building requirements. According to Cefic, low-emission catalysts are increasingly being used because of REACH. Europe’s initiatives on polyurethane recycling and demand for sustainable insulation are contributing to using tin catalyst polyurethane and polyurethane additives, making it a lucrative market player in the global market trends.

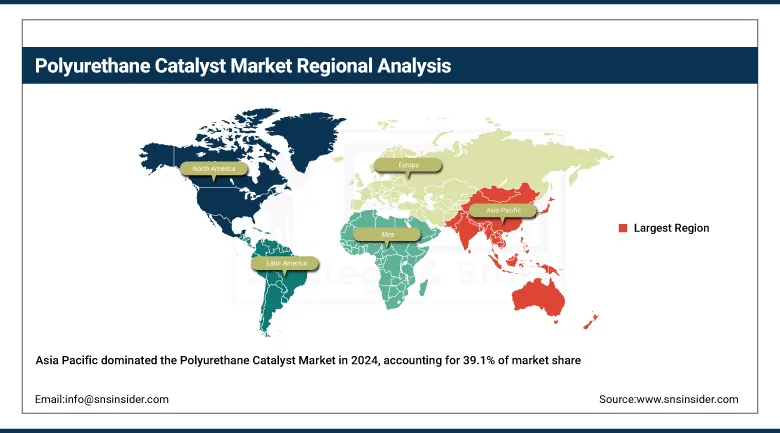

Asia Pacific dominated and held the largest polyurethane catalyst market share in 2024, accounting for more than 39.1%, and gained the maximum share following countries including China, India, and Japan. Policies supported by MIIT in China increased the demand for Tin Catalyst Polyurethane (TPU) in insulation and footwear. India’s Smart Cities Mission and the focus on EVs in Japan boosted the use of polyurethane. Industry leaders such as Wanhua and Tosoh have invested in catalyst R&D. Growing demand of consumers and infrastructure spending drives the use of polyurethane additives market, further consolidating the leading position of the region in polyurethane catalyst market growth and innovation in catalyst use.

Get Customized Report as per Your Business Requirement - Enquiry Now

Polyurethane catalyst market in LAMEA is likely to see steady growth owing to the implementation of sustainability programs, collaborations between the government and private sector, and increased demand for environment-friendly solutions. In Latin America, Brazil’s energy-efficient homes and Mexico’s automotive interiors are driving the demand for polyurethane additives and tin catalyst polyurethane. In the Middle East & Africa, support from Saudi Vision 2030, green building codes in the UAE underpin catalyst utilization for insulation, and South Africa’s furniture industry is extending the application of flexible foam, growing the regional polyurethane catalyst market size.

Key Players

The major competitors in the polyurethane catalyst market include BASF SE, Evonik Industries AG, Huntsman International LLC, The Dow Chemical Company, Covestro AG, Momentive Performance Materials Inc., Air Products and Chemicals, Inc., Wanhua Chemical Group Co., Ltd., Carpenter Co., and Polychemie Asia Pacific Permai.

Recent Developments

-

December 2023: BASF expanded specialty amines production in Geismar, Louisiana, boosting the supply of Lupragen and Baxxodur catalysts for polyurethane and epoxy applications.

-

August 2023: Gulbrandsen launched a tin catalyst plant in Dahej, India, producing Stannous Octoate and Neodecanoate for enhanced polyurethane foam manufacturing.

-

April 2023: Univar Solutions became the U.S. distributor for Patcham USA’s PATcat catalysts, strengthening its polyurethane additives portfolio with metal and tin-free options.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.79 billion |

| Market Size by 2032 | USD 4.31 billion |

| CAGR | CAGR of 5.59% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Amine, Metal, Others) •By Functionality (Gelling catalyst, Blowing Catalyst, Curing Catalyst, Foam Stabilizing Catalyst, Cross linking Catalyst, Others) •By Application (Foams, Elastomer, Sealant and adhesive, Coating, Others) •By End Use Industry (Construction, Automotive, Furniture & Bedding, Electronics, Footwear, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Evonik Industries AG, Huntsman International LLC, The Dow Chemical Company, Covestro AG, Momentive Performance Materials Inc., Air Products and Chemicals, Inc., Wanhua Chemical Group Co., Ltd., Carpenter Co., Polychemie Asia Pacific Permai |

Frequently Asked Questions

Leading companies in the Polyurethane Catalyst Market include BASF SE, Huntsman, Covestro AG, Evonik, and Dow Chemical.

The construction industry led the Polyurethane Catalyst Market in 2024, holding 41.5% due to rigid foam insulation demand.

Elastomers held the largest share of the Polyurethane Catalyst Market in 2024, driven by automotive and industrial use.

Rising demand for lightweight, energy-efficient materials across industries is a major driver for the Polyurethane Catalyst Market.

The Polyurethane Catalyst Market is expected to grow from USD 2.79 billion in 2024 to USD 4.31 billion by 2032, at a CAGR of 5.59%.

Get in Touch