Positive Displacement Pumps Market Report Scope & Overview:

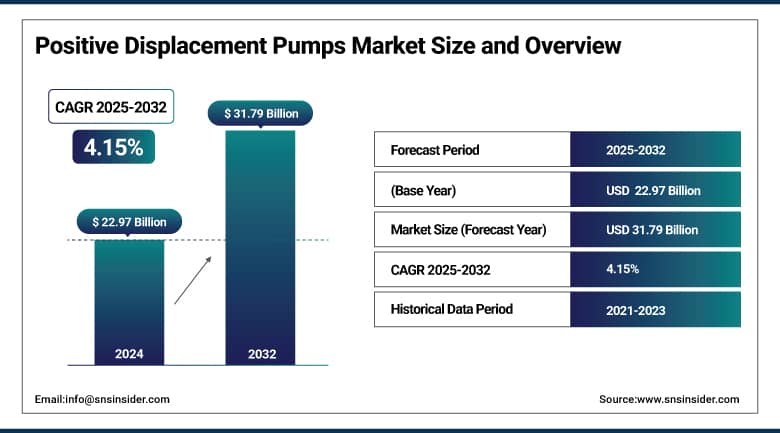

The Positive Displacement Pumps Market size was valued at USD 22.97 billion in 2024 and is expected to reach USD 31.79 billion by 2032, growing at a CAGR of 4.15% over the forecast period of 2025-2032.

The positive displacement pumps market growth is driven by demand in various industries like oil & gas, water treatment, chemical processing, and food & beverage. They work by trapping a fixed volume of fluid and forcing it through the system, which makes it perfect for both high-viscosity fluids and consistent flow applications. Volumetric pump systems, a prime segment under this market, offer precision and improved efficiency for fluid handling. Reciprocating positive displacement pumps are some of the more prevalent and are a larger share type due to their ability to attain high pressure and high reliability in critical operations. The segment of industrial positive displacement pumps is continuing to grow since industries are focusing on energy efficiency and solid solutions for fluid control. The development of technology and the smart monitoring and control features are amplifying pump performance and reliability.

Market Size and Forecast:

-

Market Size in 2024: USD 22.97 Billion

-

Market Size by 2032: USD 31.79 Billion

-

CAGR: 4.15% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get More Information On Positive Displacement Pumps Market - Request Free Sample Report

Moreover, growing investment in infrastructure and energy sectors in the emerging economies is propelling the growth of the positive displacement pumps industry. It still has its issues, like maintenance cost and possible pulsations, but ongoing R&D is working to address these. The positive displacement pumps market is poised to continue its growth trajectory, supported by its essential role in contemporary industrial landscapes and the increasing reliance on positive displacement pumps for long-lasting and efficient pumping operations.

In March 2025, Honeywell International revealed its acquisition of Sundyne, a leading producer of pumps and compressors in a USD 2.16 billion cash deal. This acquisition is part of Honeywell’s strategy to strengthen its energy and petrochemical operations, especially as it prepares for a three-way corporate split focusing on aviation, automation, and energy. Sundyne’s technologies are set to enhance Honeywell’s energy portfolio and broaden its aftermarket service capabilities.

Positive Displacement Pumps Market Trends:

-

Increasing demand from oil & gas, water & wastewater, and chemical processing industries is driving steady market growth.

-

Rising adoption of energy-efficient and low-maintenance pumping systems is boosting the deployment of rotary and reciprocating positive displacement pumps.

-

Growing infrastructure development and industrial expansion in emerging economies are accelerating product demand.

-

Stringent environmental and wastewater management regulations are supporting the installation of advanced pumping solutions.

-

Technological advancements such as smart monitoring, IoT-enabled pumps, and improved sealing technologies are enhancing operational efficiency and reliability.

-

Expansion of food & beverage and pharmaceutical manufacturing sectors is increasing the need for hygienic and precision fluid handling systems.

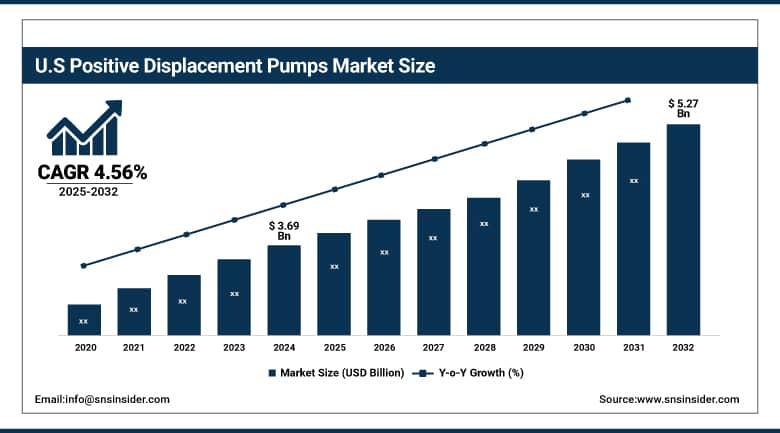

The U.S. Positive Displacement Pumps Market is projected to grow from USD 3.69 billion in 2024 to USD 5.27 billion by 2032, at a CAGR of 4.56%. The gradual growth can be attributed to growth in major industrial sectors, along with a growing preference for more energy-efficient pump technologies. The U.S. continues to play a leading role in North America, bolstered by robust industrial activity and infrastructure growth.

Positive Displacement Pumps Market Dynamics

Drivers

-

Rapid Industrialization and Urbanization in Emerging Economies Are Driving Demand for Positive Displacement Pumps

The growing industrialization and urbanization across emerging economies, such as India, China, and Brazil, is one of the top factors contributing to the growing demand for positive displacement (PD) pumps. Positive displacement pumps are widely used in oil & gas, water treatment, chemicals, and food processing, where they transport high-viscosity fluids and require accurate flow control. For example, the increasing pipeline infrastructure and the government initiatives to expand water management systems in India is also anticipated to stimulate the PD pumps demand in different sectors. Likewise, China is driving the need for improved fluid handling capabilities by turning its attention to industrial facility upgrades and water resource management. Such trends highlight the pivotal contribution of PD pumps towards industrial expansion and urban infrastructure development.

For Instance, in 2023, an article on Water Online highlights that rapid industrial growth is boosting demand for positive displacement (PD) pumps. With global manufacturing up 7.2% in 2021 and India's pharmaceutical sector set to reach USD 130 billion by 2030, PD pumps are critical for handling complex fluids. India’s plan to expand its gas pipeline network by 54% further emphasizes its growing importance in infrastructure.

Restraint

-

Overcoming High Costs and Maintenance Issues in Positive Displacement Pumps Through Innovation and Design

Positive displacement (PD) pumps are tremendously significant in industrial applications requiring the accurate flow of fluids; however, their high cost of installation and maintenance continues to be a roadblock. This leads SME to less access to PD pumps, since the initial cost of PD pumps is higher than that of centrifugal pumps. PD pumps have more moving parts and closer tolerances than centrifugal, so critical components like seals, O-rings, and gears need to be checked and replaced at regular intervals. Such maintenance, labour-intensive and skilled nature of maintains increases operational costs and loss of good operational hours. Such factors may restrict these technologies in low-cost markets. In order to combat these problems, operators are developing design improvements and predictive maintenance technologies to lengthen the periods between pump replacements while also minimizing upkeep costs.

For instance, KSB Limited acquired proprietary technology from Bharat Pumps and Compressors Ltd. (BP&CL), aiming to enhance its service capabilities and support a wide range of industries, including oil and gas exploration and nuclear power plants. This strategic acquisition enables KSB Limited to leverage its strengths and market potential, expanding its product offerings in both new pump systems and aftermarket markets

Positive Displacement Pumps Market Segmentation Analysis

By Type

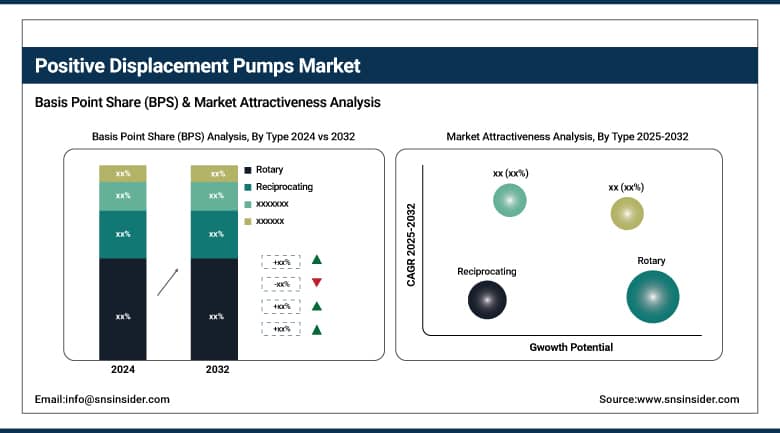

The rotary pumps segment dominated the market and accounted for 58% of the positive displacement pumps market share. These pumps are highly sought after in diverse industrial segments due to their constant flow characteristics over a wide range of pressures and are perfect for accurate fluid handling. The ability of these valves to manage viscous fluids and slurries and their minimal maintenance requirements enhance their overall market presence. Moreover, growing innovative rotary pump technologies, such as better materials and energy-saving designs, are steering their preference by industrial sectors.

Reciprocating pumps are the fastest-growing segment in the positive displacement pumps market, which results in their growing popularity in oil & gas, chemical processing, and water treatment industries due to their appropriateness for precise dosing and high-pressure applications. The fast-growing demand for pumps in hydraulic fracturing and other energy-intensive processes, in conjunction with technological innovations improving pump durability and efficiency, is driving the rapid uptake of reciprocating pumps. That growth is predicted to stay as industries continue to search for simply dependable, high-performance pumping solutions.

By End-Use

The Oil & Gas segment dominated the positive displacement pumps market with a 28% share in 2024, supported by high demand from the industry for reliable and efficient pumping systems in exploration, production, and refining processes. Positive displacement pumps are fundamental for viscous fluids, high-pressure transfer, and metering in the harsh conditions of a normal oil and gas operation. This is primarily due to a gradual increase in enhanced oil recovery techniques and increasing offshore drilling activities that have cemented the status of this end-use segment. Moreover, high precision pumping requirements due to strict safety and environmental regulations are expected to make this sector the largest market share holder.

The Chemical segment represents the fastest-growing end-use segment in the positive displacement pumps market, due to the rising need for effective fluid handling in chemical processing, pharmaceutical, and specialty chemicals production. Positive-displacement pumps offer several advantages, such as accurate flow control, handling of corrosive and hazardous fluids, and reliable continuous operations. This segment also benefits from the growth in the use of automation and process optimization technologies, which require consistent and precise pumping. Other factors, such as growth in developing countries and increasing environmental regulations regarding safe chemical handling, also drive the demand for these markets.

Positive Displacement Pumps Market Regional Outlook

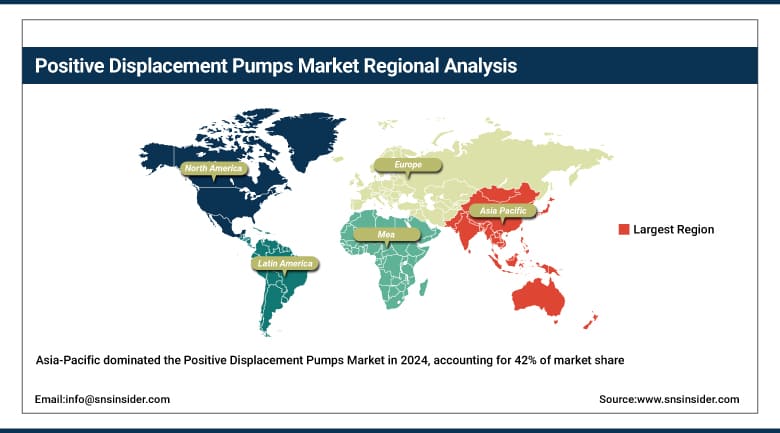

The Asia-Pacific region dominated the positive displacement pumps market, accounting for 42% of the market share in 2024. Rapid industrialization and urbanization, along with growth in critical end-use verticals including oil & gas, chemical manufacturing, and water treatment, are driving this dominance. Infrastructure and energy goods, China and India are spending heavily on projects that are driving the require for dependable pumping remedies. Besides, a well-established end-user base along with the presence of advanced technologies are other factors responsible for the dominance of this region. In addition, Asia-Pacific aggressively retains first place in this market due to sturdy government initiatives encouraging industrial growth.

China leads the Asia-Pacific region in positive displacement pumps owing to the large industrial base in automotive, chemicals, manufacturing, etc. Demand is further enhanced by mega infrastructure projects such as treatment and desalination plants. Moreover, various government policies regarding the improvement in the management of water resources extend further upon market progress.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America is the fastest-growing region in the positive displacement pumps market, as it is characterized by the fast adoption of industrial automation and modernization across various sectors. Industries like pharmaceuticals, food & beverage, and oil & gas intend to use this technology to meet their operational requirements and boost demand for positive displacement pumps. Moreover, advancement of technology for pumps, growing environmental regulations in developed economies well as increasing focus on energy efficiency, are also propelling the market growth for the Global Nuclear Reactor and Associated Services Market. Additionally, the North American pump market is anticipated to be the fastest-growing regional market because of established pump manufacturers and continuous investment in R&D.

Europe holds a significant share in the positive displacement pumps market, supported by its mature industrial base and stringent regulatory environment. The continual requirement for positive displacement pumps in automotive, chemical processing, and wastewater management in the region is owing to its efforts towards sustainability and energy-efficient solutions. Moreover, product adoption is aided by technological innovation and strong aftermarket services in North America and Europe. Europe, being one of the most important and sustainable markets for global positive displacement pumps, is credited with a high contribution owing to countries such as Germany, the UK, and France that focus mainly on advanced manufacturing infrastructure and quality standards of positive displacement pumps.

Key Players:

-

Grundfos Holding A/S

-

Sulzer Ltd.

-

Alfa Laval AB

-

Viking Pump Inc.

-

Netzsch Pumps & Systems

-

SEEPEX GmbH

-

Dover Corporation (PSG)

Recent Development

-

In November 2024: Viking Pump unveiled its next-generation stainless steel internal gear pumps, incorporating the ProPort casing for customizable porting and the U-Plus bracket to support a variety of sealing configurations. The updated design is intended to streamline manufacturing, shorten lead times, and improve overall flexibility.

-

In April 2025: NETZSCH Pumps & Systems installed eight PERIPRO peristaltic pumps (model 10/66) at a pioneering energy self-sufficient waste and wastewater treatment facility in Singapore. The pumps, introduced at IFAT 2024, support reliable and efficient plant operations through their durable and innovative design.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 22.97 Billion |

| Market Size by 2032 | USD 31.79 Billion |

| CAGR | CAGR of 4.15% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Rotary (Gear Pump, Screw Pump, Vane Pump, Lobe Pump, Others), Reciprocating (Diaphragm, Piston, Plunger) • By End-use (Agriculture, Construction & Building Services, Water & Wastewater, Power Generation, Oil & Gas, Chemical, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Flowserve Corporation, Grundfos Holding A/S, Sulzer Ltd., SPX Flow Inc., Alfa Laval AB, Viking Pump Inc. (IDEX Corporation), Netzsch Pumps & Systems, SEEPEX GmbH, IDEX Corporation, and Dover Corporation (PSG) |

Frequently Asked Questions

The Positive Displacement Pumps Market was USD 22.97 billion in 2024 and is expected to reach USD 31.79 billion by 2032.

Rapid Industrialization and Urbanization in Emerging Economies Are Driving Demand for Positive Displacement Pumps

The Positive Displacement Pumps Market is expected to grow at a CAGR of 4.15% from 2025-2032.

The Asia-Pacific region dominated the Positive Displacement Pumps Market in 2024.

The “Rotary Pumps” segment dominated the Positive Displacement Pumps Market.

Get in Touch