Ethyl Acetate Market Report Scope & Overview:

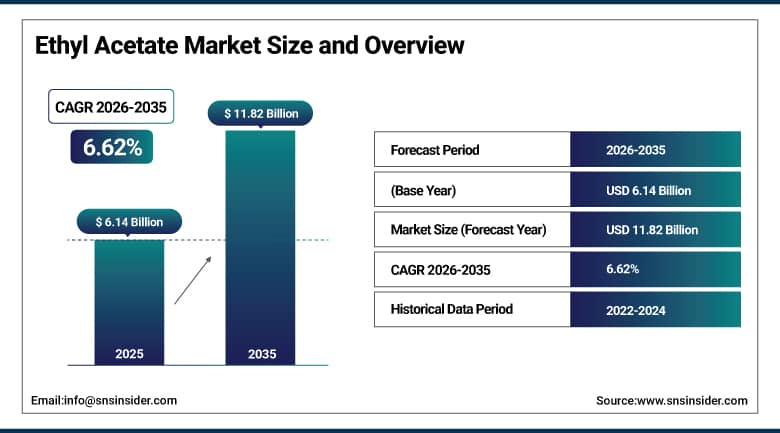

Ethyl Acetate Market was valued at USD 6.14 billion in 2025 and is expected to reach USD 11.82 billion by 2035, growing at a CAGR of 6.62% from 2026-2035.

The growth of the Ethyl Acetate Market is influenced by rising demand in paints and coatings, adhesives, pharmaceuticals, and packaging sectors. The extensive use of Ethyl Acetate as a solvent in flexible packaging and ink for printing drives the market growth. Increased industrialization and construction activity also positively impacts the consumption rate. The growing preference for eco-friendly solvents also increases the use of Ethyl Acetate. The increasing application in the food processing industry and cosmetics further propels the market growth.

The U.S. EPA's National Emission Standards for Hazardous Air Pollutants (NESHAP) and VOC solvent regulations have progressively restricted high-toxicity solvent alternatives, creating a regulatory tailwind for ethyl acetate as a preferred lower-toxicity option. The European Chemicals Agency (ECHA) REACH regulation classifies ethyl acetate as a substance of low concern, sustaining its approval for use across the full range of industrial solvent applications within the EU.

Ethyl Acetate Market Size and Forecast

- Market Size in 2025: USD 6.14 Billion

- Market Size by 2035: USD 11.82 Billion

- CAGR: 6.62% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026-2035

- Historical Data: 2022-2024

To Get More Information On Ethyl Acetate Market - Request Free Sample Report

Ethyl Acetate Market Trends

- Rising demand from paints, coatings, and adhesives industries is driving the ethyl acetate market.

- Growing use as a solvent in pharmaceuticals, printing inks, and packaging is boosting market growth.

- Expansion of flexible packaging and food-grade applications is fueling product demand.

- Increasing focus on eco-friendly and low-toxicity solvents is shaping adoption trends.

- Advancements in bio-based ethyl acetate production are enhancing sustainability and supply diversification.

- Rising demand from cosmetics, nail care, and personal care products is supporting market expansion.

- Collaborations between chemical manufacturers, end-use industries, and distributors are accelerating innovation and global adoption.

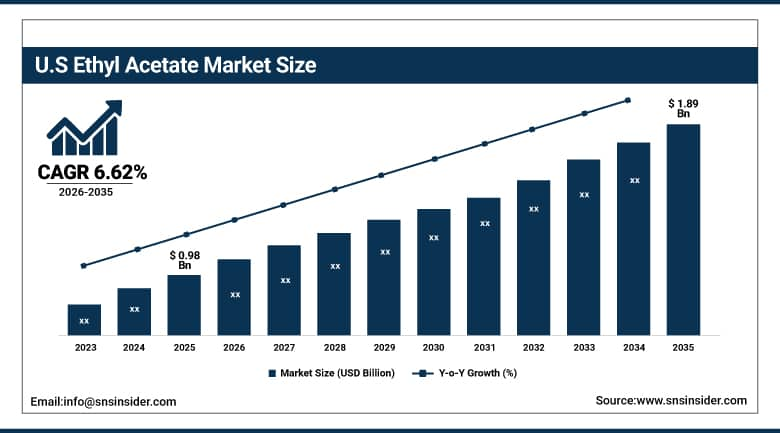

U.S. Ethyl Acetate Market was valued at USD 0.98 billion in 2025 and is expected to reach USD 1.89 billion by 2035, growing at a CAGR of 6.62% from 2026-2035.

U.S. Ethyl Acetate Market Growth Factors include increased demand from the paints & coatings, adhesives, and packaging sectors, as well as growing popularity for low-volatility organic compound solvents. Pharmaceutical and food processing applications also contribute to continuous growth within the market forecast period.

The EPA's Safer Choice program which certifies solvents and chemical products meeting stringent human health and environmental safety criteria has certified ethyl acetate, driving its specification in green chemistry procurement programs at major U.S. manufacturers. The American Coatings Association reports that architectural and industrial coatings represent the largest domestic solvent consumption category, with ethyl acetate preferred in solvent-borne formulations across multiple application segments.

Ethyl Acetate Market Segment Analysis

- By Application, Paint & Coatings segment dominated the Ethyl Acetate Market in 2025; Process Solvents segment fastest growing (CAGR).

- By End-Use, Packaging segment dominated the Ethyl Acetate Market in 2025; Pharmaceutical segment fastest growing (CAGR).

- By Distribution Channel, Offline segment dominated the Ethyl Acetate Market in 2025; Online segment fastest growing (CAGR).

By Application, Paint & Coatings segment dominates the Ethyl Acetate Market, Inks segment growing steadily

The Paint & Coatings application segment dominates the Ethyl Acetate Market owing to its extensive use as a highly volatile solvent, improving the performance of coatings and finishing. The product finds wide usage in the construction industry, automobile sector, and various other industries where coating performance is crucial. With the growing demand for infrastructure development, urbanization, and coating products, the application segment is expected to retain its dominance in the overall market.

Process Solvents is the fastest-growing application segment in the Ethyl Acetate Market, due to the beneficial properties of ethyl acetate such as low toxic levels and high solvability, it is widely used in the synthesis, purification, and extraction processes. The increasing demand for pharmaceutical, specialty chemical, and manufacturing products and the inclination towards using environment-friendly solvents are fueling the growth of this segment.

By End-Use, Automotive segment dominates the Ethyl Acetate Market, Pharmaceutical and Artificial Leather fastest growing

Packaging dominates the Ethyl Acetate Market by end-use owing to the critical importance of this segment in flexible packaging, printing inks, and laminating applications. The drying rate and versatility to work with different substrates improve efficiency and yield quality products. The surge in online sales through e-commerce, food delivery, and other consumer goods businesses has led to high demand in this segment.

The pharmaceutical industry is the fastest-growing category in the market due to the rising usage of ethyl acetate in the production and purification of medicines. The ability of ethyl acetate to serve as an effective solvent makes it a perfect choice for the pharmaceutical sector. Increasing demand for healthcare, pharmaceutical manufacturing, and drug discovery drives its growth.

By End-Use, Offline segment dominates the Ethyl Acetate Market, Online fastest growing

Offline distribution dominates the Ethyl Acetate Market due to the preferences of large industrial customers for direct purchasing via distributors. Offline distribution allows for ensuring a constant flow of supply, providing bulk quantities, and maintaining good relations between manufacturers and distributors. High levels of logistics development and reliable management of bulk sales help maintain the dominance of offline distribution.

Online distribution is the fastest-growing channel within the Ethyl Acetate Market because of the growing popularity of online purchasing. The online purchasing platform provides businesses with greater price transparency and the convenience to choose from a variety of suppliers. With more industries engaging in digital procurement, the prevalence of online distribution channels is expected to rise rapidly across the globe.

Ethyl Acetate Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

55% |

|

North America |

United States |

86% |

|

Europe |

Germany |

28% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

48% |

Asia Pacific Ethyl Acetate Market Insights

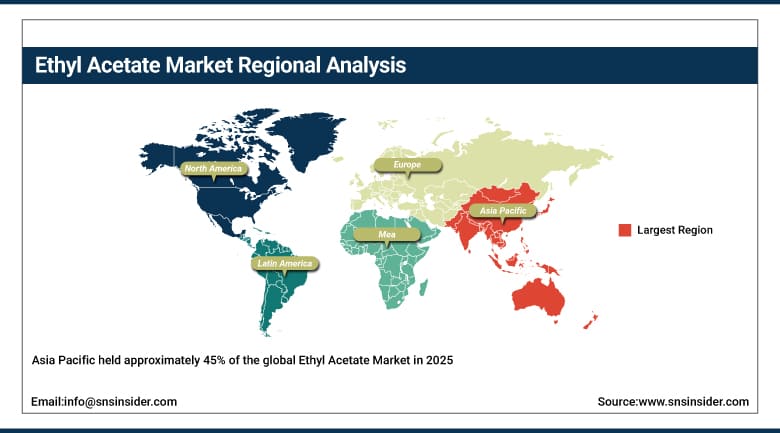

Asia Pacific held approximately 45% of the global Ethyl Acetate Market in 2025, a position anchored by China and India's rapid industrial growth, expanding manufacturing infrastructure, and the region's growing automotive, paint, and adhesives sectors. China is both the world's largest producer and one of its largest consumers of ethyl acetate, with major domestic producers including Shandong Hualu Hengsheng Chemical and Jiangsu Zhongneng Chemical serving both domestic and export markets. India's growing pharmaceutical manufacturing sector already the world's largest generic medicine producer generates expanding demand for pharmaceutical-grade ethyl acetate in API synthesis and tablet coating processes. Southeast Asian artificial leather production for global fashion brands is an additional demand driver that has no direct equivalent in mature Western markets.

China's Ministry of Industry and Information Technology has identified ethyl acetate as a strategic chemical in its chemical industry development plan, supporting domestic production capacity expansion. India's Chemicals and Petrochemicals Department reports ethyl acetate as among the fastest-growing specialty solvent imports, with domestic production investment being incentivized through PLI scheme provisions for specialty chemicals.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Ethyl Acetate Market Insights

The ethyl acetate market in North America exhibits steady growth driven by significant demand from the paints and coatings, adhesive, packaging, and pharmaceutical sectors. The area enjoys the advantage of well-established petrochemical facilities and availability of inexpensive feedstock. The US dominates consumption owing to its massive manufacturing sector and stringent environmental policies encouraging the use of low-toxic solvents.

Europe Ethyl Acetate Market Insights

Ethyl Acetate Market in Europe is expected to grow at a steady pace due to high consumption from end-user industries such as paints and coatings, pharmaceuticals, packaging, and artificial leather. Europe enjoys state-of-the-art manufacturing capabilities of chemicals along with regulatory initiatives for developing environment-friendly and low toxicity solvents. Rising consumption of bioethanol and increasing use of ethyl acetate in flexible packaging and printing inks contribute to market growth.

The European Commission's EU Green Deal and Chemicals Strategy for Sustainability explicitly prioritizes substitution of hazardous solvents with safer alternatives, with ethyl acetate specifically listed as a preferred substitute in multiple application categories. ECHA's restriction timeline for several aromatic solvent alternatives has created substitution demand that benefits ethyl acetate procurement volumes across EU manufacturing.

Middle East & Africa and Latin America Ethyl Acetate Market Insights

Middle East & Africa and Latin America Ethyl Acetate Market is growing steadily due to an increase in the construction, packaging, and automotive sectors. Increasing investments in infrastructure development and industrialization have resulted in an increased need for paints, coating, and solvents. The increasing pace of urbanization, along with governmental support, contributes to growth in Latin America, whereas petrochemical integration facilitates supply in the Middle East & Africa region. There are certain restraints like raw materials and logistics issues that could limit the growth somewhat.

Ethyl Acetate Market Growth Drivers:

- Rising automotive and artificial leather applications driving sustained demand growth for ethyl acetate globally

The two most dynamic demand drivers for ethyl acetate automotive coatings and artificial leather manufacturing are both benefiting from structural trends that are not short-term. The automotive industry's transition to electric vehicles is not reducing coating and finishing demand; if anything, EV adoption is sustaining premium coating investments as manufacturers differentiate their vehicles through exterior finish quality. Artificial leather's growth story is even more compelling: it is simultaneously displacing genuine leather in sustainability-driven markets where brands have committed to removing animal products from their supply chains, while also expanding into new applications in automotive interiors and fashion accessories that traditional leather's cost and supply constraints limited. Both growth drivers sustain ethyl acetate demand at the high-quality end of the product spectrum, supporting premium solvent pricing that offsets volume-reducing efficiency improvements in application technologies.

The International Organisation of Motor Vehicle Manufacturers (OICA) reports global vehicle production recovering to pre-pandemic levels with premium finishes increasingly specified across model ranges. The global artificial leather market is projected to exceed USD 45 billion by 2030 according to IMARC Group analysis, with polyurethane-based artificial leather an ethyl acetate-intensive manufacturing process accounting for the dominant and fastest-growing material type.

Ethyl Acetate Market Restraints:

- Volatile raw material prices and bio-based competition creating cost and substitution challenges for ethyl acetate producers

The price of ethyl acetate is materially influenced by the cost of its two primary feedstocks ethanol and acetic acid both of which are themselves influenced by energy prices, agricultural commodity cycles, and petrochemical feedstock markets. When ethanol prices spike due to biofuel mandates absorbing grain supply, or when acetic acid prices rise due to methanol cost increases, ethyl acetate production costs follow, and the margin compression that results can discourage capacity investment precisely when market growth is strongest. Bio-based alternatives including ethyl acetate from bio-ethanol, and other green solvents like methyl ethyl ketone from biomass are growing segments that create competitive pressure in sustainability-motivated procurement programs, though their cost parity with conventional production remains inconsistent across market conditions.

Ethyl Acetate Market Opportunities:

- Bio-based ethyl acetate innovation and pharmaceutical manufacturing expansion creating new market growth opportunities

Innovation in bio-based ethyl acetate production and the commercial framework around it represents a genuine growth opportunity that conventional solvent market analysis tends to underweight. As consumer brands, automotive OEMs, and pharmaceutical companies publish commitments to sustainable chemistry sourcing that include verified bio-based solvent content in their supply chains, they are creating a premium market segment where bio-ethyl acetate commands pricing above conventional production economics. Companies including Godavari Biorefineries in India and Vertec BioSolvents in the U.S. are building commercial-scale bio-based ethyl acetate supply that addresses this market. The pharmaceutical manufacturing expansion opportunity is equally concrete: as generic drug production volume grows in India, Southeast Asia, and Africa all regions where API synthesis and tablet coating use ethyl acetate as a primary process solvent the pharmaceutical-grade ethyl acetate market grows at rates above the overall solvent market average.

Recent Developments:

- 2025: Celanese Corporation expanded ethyl acetate production capacity at its Clear Lake, Texas facility, adding 50,000 metric tons of annual capacity to serve growing North American demand from automotive coatings, pharmaceutical, and packaging applications where Celanese supplies high-purity solvent grades under long-term supply agreements with major manufacturers.

- 2025: Godavari Biorefineries secured ISO 14001 certification and ISCC PLUS mass balance certification for its bio-based ethyl acetate produced from sugarcane bioethanol, enabling the company to supply certified bio-based ethyl acetate to European pharmaceutical and cosmetics manufacturers requiring documented renewable content under EU Green Deal procurement specifications.

- 2026: INEOS Acetate launched a new high-purity pharmaceutical-grade ethyl acetate specification meeting ICH Q3C residual solvent limits for Class 3 solvents, targeting contract pharmaceutical manufacturers implementing continuous manufacturing processes that require tighter solvent purity control than batch processes traditionally demanded.

Ethyl Acetate Market Key Players

Some of the Ethyl Acetate Market Companies

- Celanese Corporation

- INEOS Group

- Eastman Chemical Company

- Daicel Corporation

- Jiangsu Sopo Chemical Co., Ltd.

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Jubilant Ingrebia Limited

- Godavari Biorefineries Ltd.

- SEKAB Biofuels & Chemicals AB

- Shiny Chemical Industrial Co., Ltd.

- S.A. Alcoholes, Derivados y Alcoholatos

- Nantong Dongchang Boyi Chemical Co., Ltd.

- Jiangsu Mupro Food Industry

- Hangzhou Dadi Chemical Co., Ltd.

- Vertec BioSolvents Inc.

- Sasol Limited

- Myriant Corporation

- Kyowa Hakko Bio Co., Ltd.

- Haibo Petrochemical Co., Ltd.

- Lonza Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.39 Billion |

| Market Size by 2035 | USD 9.59 Billion |

| CAGR | CAGR of 6.62% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Paint & Coatings, Inks, Process Solvents, Pigments, Other) • By End-Use (Artificial Leather, Pharmaceutical, Automotive, Food & Beverage, Packaging, Other) • By Distribution Channel (Offline, Online) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles |

Celanese Corporation, INEOS Group, Eastman Chemical Company, Daicel Corporation, Jiangsu Sopo Chemical Co., Ltd., Shandong Hualu-Hengsheng Chemical Co., Ltd., Jubilant Ingrebia Limited, Godavari Biorefineries Ltd., SEKAB Biofuels & Chemicals AB, Shiny Chemical Industrial Co., Ltd., S.A. Alcoholes, Derivados y Alcoholatos, Nantong Dongchang Boyi Chemical Co., Ltd., Jiangsu Mupro Food Industry, Hangzhou Dadi Chemical Co., Ltd., Vertec BioSolvents Inc., Sasol Limited, Myriant Corporation, Kyowa Hakko Bio Co., Ltd., Haibo Petrochemical Co., Ltd., Lonza Group |

Frequently Asked Questions

North America led the Ethyl Acetate Market in the region with the highest revenue share in 2025.

The Automotive segment dominated the Ethyl Acetate Market with approximately 35% share in 2025.

The Paint & Coatings segment dominated the Ethyl Acetate Market with approximately 54% share in 2025.

The Ethyl Acetate Market is expected to grow at a CAGR of 6.62% from 2026 to 2035.

The Ethyl Acetate Market was valued at USD 6.14 billion in 2025.

Get in Touch