Acrylonitrile Market Report Scope & Overview:

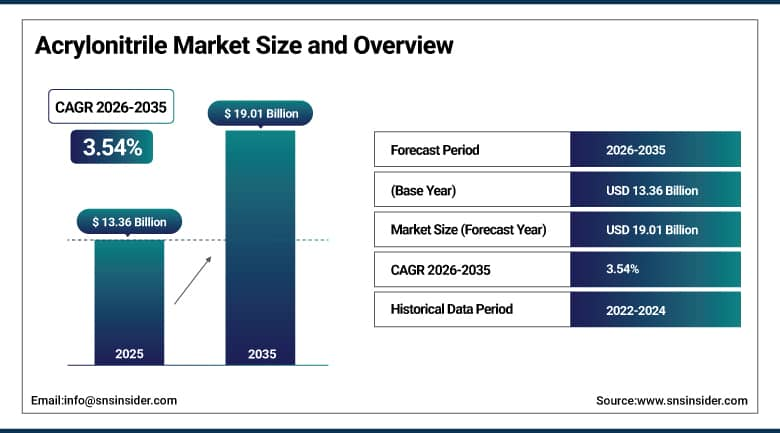

The Acrylonitrile Market was valued at USD 13.36 Billion in 2025 and is expected to reach USD 19.01 Billion by 2035, growing at a CAGR of 3.54% from 2026–2035.

The global acrylonitrile market is advancing at a steady pace. Acrylonitrile is a highly reactive, volatile organic nitrile compound that serves as a fundamental monomeric building block in the synthesis of high-performance engineered polymers and specialised elastomers. Its chemical versatility enables production of ABS and SAN resins for automotive and consumer electronics, acrylic fibres for the textile industry, nitrile rubber for industrial and medical gloves, acrylamide for water treatment and mining, and carbon fibre for aerospace and clean energy applications. The market's key growth factors are expanding automotive and electronics industries, rising demand for ABS resins, and increasing infrastructure development requiring acrylamide applications.

In 2023, LG Chem partnered with a major EV manufacturer to supply high-performance ABS materials for next-generation electric vehicles, strengthening its position in the automotive sector. The partnership reflects the commercial logic of acrylonitrile’s value chain whose ABS resin application's automotive adoption is growing with EV production volume. Lightweight ABS components that replace steel and aluminium in EV body panels and battery enclosures reduce vehicle weight whose contribution to range extension creates a commercially compelling material specification motivation.

Market Size and Forecast

-

Market Size in 2026E: USD 13.83 Billion

-

Market Size by 2035: USD 19.01 Billion

-

CAGR: 3.54% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Acrylonitrile Market - Request Free Sample Report

Acrylonitrile Market Trends

-

Carbon fibre production from polyacrylonitrile precursors is expanding steadily as aerospace, wind energy, and electric vehicle manufacturers increase demand for lightweight, high-strength materials driving greater acrylonitrile consumption

-

Bio-based acrylonitrile development from renewable feedstocks is gaining momentum as manufacturers pursue sustainable alternatives to conventional production methods supporting decarbonisation goals across the chemical value chain

-

ABS resin demand is rising due to increasing use in EV body panels, battery housings, and interior components creating new growth opportunities for acrylonitrile beyond traditional automotive applications

-

Nitrile rubber consumption remains strong as healthcare and industrial sectors continue to require high volumes of disposable gloves and protective equipment following long-term changes in hygiene and safety standards

-

Investments in green chemistry and emission reduction technologies are helping acrylonitrile producers improve environmental performance while meeting evolving regulatory requirements and sustainability expectations from downstream customers

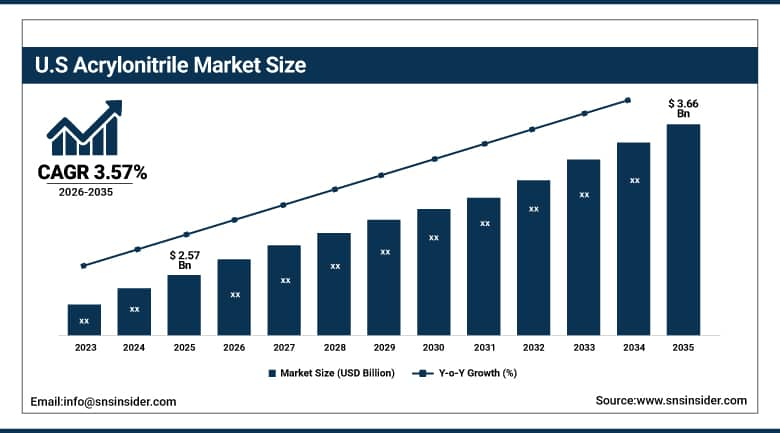

U.S. Acrylonitrile Market Outlook

The U.S. Acrylonitrile Market was valued at approximately USD 2.57 Billion in 2025 and is expected to reach approximately USD 3.66 Billion by 2035, growing at a CAGR of approximately 3.57%.

The U.S. is the most commercially significant acrylonitrile market within the fastest-growing North American region. Ineos Nitriles’ U.S. operations, Ascend Performance Materials, and INVISTA’s domestic production define the North American acrylonitrile supply landscape. The automotive industry’s ABS resin consumption, the textile industry’s acrylic fibre procurement, and the water treatment industry’s acrylamide demand collectively sustain consistent U.S. acrylonitrile demand across market cycles. The growing carbon fibre industry’s PAN precursor requirement creates above-average quality specification demand whose commercial value per unit substantially exceeds commodity ABS resin feedstock pricing.

In 2024, Ascend Performance Materials piloted bio-feedstock acrylonitrile production and produced around 5% of its pilot batch from bio-derived propylene, targeting a 10% shift in future capacity toward renewable feedstocks. The development demonstrates the commercial viability of bio-based acrylonitrile production whose sustainability credentials could command premium pricing from downstream customers whose corporate sustainability commitments create motivation for bio-content procurement at modest cost premiums.

Acrylonitrile Market Segment Analysis

-

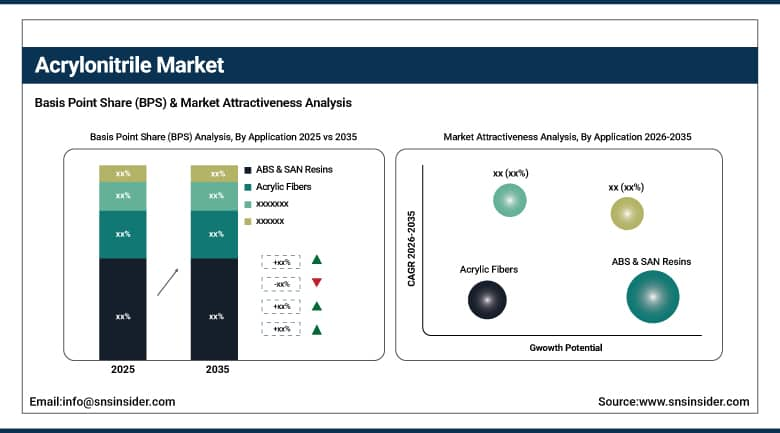

By Application, the ABS & SAN Resins segment dominated the Acrylonitrile Market with approximately 49% share in 2025, while the Acrylic Fiber segment is the fastest growing segment.

-

By Process Technology, the Ammoxidation (SOHIO) segment dominated the Acrylonitrile Market with approximately 75% share in 2025, while the Alternative process segment is the fastest growing segment.

-

By Purity Grade, the Above 99% segment dominated the Acrylonitrile Market with approximately 86.7% share in 2025, while the Up to 99% segment is the fastest growing segment.

-

By End User, the Automotive & Transportation segment dominated the Acrylonitrile Market with approximately 45% share in 2025, while the Electronics & Electrical segment is the fastest growing segment.

By Application, ABS & SAN resins dominate, acrylic fiber grows fastest

ABS and SAN resins retained the dominant application position with approximately 49% of the acrylonitrile market in 2025. ABS resin’s commercial primacy reflects its extraordinary versatility across automotive body panels, consumer electronics housings, household appliances, and construction materials whose combined consumption creates the largest single acrylonitrile application category globally. Each automobile produced globally consumes approximately 10-15 kg of ABS resin for interior and exterior plastic components, creating procurement that compounds with global vehicle production volume. Consumer electronics’ universal adoption of ABS for smartphone, laptop, and appliance housing creates additional consistent high-volume procurement. SAN resin’s clarity and chemical resistance add specialty applications that complement ABS’s structural plastic role.

Acrylic fibre is the fastest-growing application because the textile industry’s demand for wool-like synthetic fibre with superior UV resistance, dyeability, and moisture management is creating above-average growth in warm climate markets and outdoor textile applications. Carbon fibre’s PAN precursor requirement, whose 8-10% annual growth reflects aerospace, wind turbine, and EV structural application adoption, simultaneously creates premium acrylonitrile demand whose per-unit commercial value substantially exceeds commodity acrylic textile fibre economics.

By Process Technology, ammoxidation dominates, alternatives grow fastest

Ammoxidation retained the dominant process technology position with approximately 75% of the acrylonitrile market in 2025. The SOHIO ammoxidation process’s commercial primacy reflects its position as the global industry standard for acrylonitrile production since its introduction in the 1960s. Propylene, ammonia, and air react over bismuth molybdate catalyst systems at 420-460°C to produce acrylonitrile at conversions above 80% whose commercial efficiency creates the most economically competitive production route for large-scale capacity.

Alternative process technologies are the fastest-growing segment because environmental pressure on propylene ammoxidation’s nitrous oxide and cyanide by-product streams is creating research and commercial investment in alternative production routes. Bio-based acrylonitrile production from glycerol, 3-hydroxypropionitrile, and bio-derived propylene create renewable feedstock pathways whose carbon footprint reduction creates sustainability credentials.

By Purity Grade, above 99% dominates, up to 99% grows

Above 99% purity acrylonitrile retained the dominant grade position with approximately 86.7% of the acrylonitrile market in 2025. The high-purity grade’s commercial dominance reflects the quality requirements of the majority of acrylonitrile applications whose polymer synthesis quality, fibre performance, and resin property consistency depend on feedstock purity specifications. ABS and SAN resin production whose polymer chain length distribution and optical clarity specification require consistent high-purity monomer feedstock, acrylic fibre production whose tenacity and colour consistency require above 99% grade acrylonitrile, and carbon fibre PAN precursor production whose structural performance requirements demand the highest available purity collectively sustain the dominant grade position.

Up to 99% purity acrylonitrile finds application in less demanding industrial chemical synthesis applications where minor impurity tolerance allows procurement of lower-cost grades whose economic advantage over premium purity justifies application acceptance. Acrylamide water treatment chemical synthesis and lower-specification nitrile rubber production represent the primary applications whose tolerance for 99% grade creates differentiated procurement from the majority of higher-specification uses.

By End User, automotive dominates, electronics grows fastest

Automotive and transportation retained the dominant end user position with approximately 45% of the acrylonitrile market in 2025. The automotive industry’s extraordinary ABS resin consumption for interior trim, exterior body panels, underbody components, and EV battery housing creates the most commercially concentrated acrylonitrile demand of any end user category. Each vehicle model that specifies ABS for a new component application creates procurement that scales with the vehicle’s production volume.

Electronics and electrical is the fastest-growing end user because the semiconductor industry’s fab expansion under CHIPS Act and equivalent programmes, combined with consumer electronics’ continued product cycle investment, is creating growing ABS and SAN resin demand for electronics housing and structural component applications. Each new semiconductor fab facility’s electronics-grade plastic component requirements, combined with the consumer electronics market’s continuous product refresh cycle, creates structured ABS procurement growth that sustains the electronics sector’s above-average market share growth rate.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Acrylonitrile Market Insights

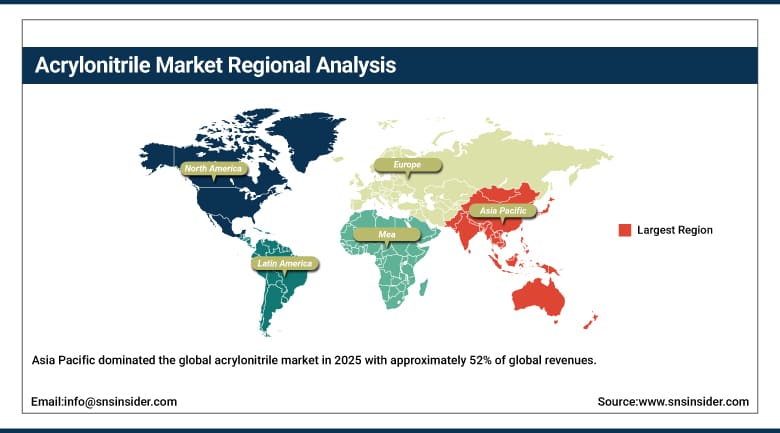

Asia Pacific dominated the global acrylonitrile market in 2025 with approximately 52% of global revenues. China accounts for approximately 54.6% of Asia Pacific revenues through its position as the world’s largest ABS resin producer and consumer, whose integrated acrylonitrile-to-ABS value chain creates the commercial scale that defines global market dynamics. The acrylic fibre textile industry’s concentration in China, India, and South Korea creates additional consistent acrylonitrile demand that reinforces Asia Pacific’s market dominance.

Japan and South Korea represent technically sophisticated secondary markets where Toray Industries’ carbon fibre PAN precursor production, Samsung SDI’s ABS resin manufacturing, and the automotive sector’s ABS procurement create consistent premium-grade acrylonitrile demand.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Acrylonitrile Market Insights

North America is the fastest-growing regional acrylonitrile market, driven by automotive ABS demand growth, EV production expansion’s ABS content increase, and the carbon fibre industry’s PAN precursor procurement. The United States accounts for approximately 87.4% of North American revenues through Ineos Nitriles’ domestic production, Ascend Performance Materials’ operations, and the automotive, electronics, and textile industry’s consistent procurement.

Mexico’s automotive manufacturing sector’s ABS resin procurement and Canada’s chemical industry’s acrylonitrile derivative consumption collectively contribute approximately 12.6% of North American revenues through their respective industrial chemical demand.

Europe Acrylonitrile Market Insights

Europe is a technically sophisticated acrylonitrile market where Ineos’s European production, BASF’s ABS resin manufacturing, and the automotive OEM sector’s ABS procurement create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive manufacturing sector’s ABS consumption, the chemical industry’s specialty derivative demand, and Ineos’s EU VOC capture retrofit investment.

The United Kingdom, France, and the Benelux are significant secondary markets where chemical manufacturing, automotive assembly, and textile production create consistent acrylonitrile derivative procurement.

MEA & Latin America Acrylonitrile Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through SABIC’s ABS resin manufacturing, the petrochemical complex’s acrylonitrile derivative consumption, and the construction sector’s acrylonitrile-based material procurement. Brazil leads Latin American revenues at approximately 44.2% through its automotive sector’s ABS consumption, the packaging industry’s SAN resin demand, and the textile sector’s acrylic fibre procurement.

The growing Gulf petrochemical industry investment and Africa’s industrial development are creating emerging acrylonitrile market demand whose structural growth compounds with regional manufacturing capacity expansion.

Market Dynamics:

Growth Drivers: Automotive ABS demand growth from EV lightweighting and carbon fibre PAN precursor adoption in clean energy

Automotive ABS demand from EV lightweighting is the acrylonitrile market’s most commercially transformative near-term growth driver. Each EV platform that adopts ABS for battery enclosure, underbody panel, or structural component lightweighting creates acrylonitrile demand whose per-vehicle content growth with EV market penetration creates commercial opportunity that conventional ICE vehicle ABS demand does not replicate. The automotive OEM’s systematic material substitution toward lightweight plastics whose weight reduction contributes to EV range extension creates structured ABS procurement that sustains above-average acrylonitrile demand growth.

Carbon fibre’s PAN precursor procurement is simultaneously creating a premium acrylonitrile demand category whose 8-10% annual growth in aerospace, wind turbine, and EV structural application adoption creates above-average revenue growth for acrylonitrile producers capable of supplying the highest-purity PAN precursor grade. Wind turbine blade production’s carbon fibre adoption, aerospace structure’s carbon composite specification, and EV chassis lightweighting’s structural carbon fibre use collectively create the most commercially value-accretive acrylonitrile application growth.

Restraints: Environmental classification as hazardous air pollutant and propylene feedstock price volatility

Acrylonitrile’s EPA classification as a hazardous air pollutant and IARC’s Group 2A possible human carcinogen designation create regulatory compliance investment requirements whose cost creates above-average operating expense for producers. Each new EPA emission standard tightening or EU REACH restriction creates compliance capital investment whose cost is higher for older production facilities whose process equipment was designed to less stringent emission standards. Environmental compliance cost creates competitive disadvantage for higher-cost producers relative to Asian producers operating under less stringent frameworks.

Propylene feedstock price volatility creates production cost uncertainty that limits acrylonitrile margin predictability for producers whose fixed-price downstream contracts cannot accommodate proportional feedstock cost pass-through. Each crude oil price cycle creates propylene price variation whose impact on acrylonitrile production economics creates margin compression during high-feedstock-cost periods that limits producer investment capacity.

Opportunities: Bio-based acrylonitrile development and carbon fibre demand from renewable energy infrastructure

Bio-based acrylonitrile development represents the most commercially transformative long-term opportunity whose successful commercialisation would differentiate sustainable acrylonitrile producers in markets where corporate sustainability commitments create premium procurement motivation. Ascend’s 2024 pilot demonstrating bio-derived propylene feedstock feasibility creates the technology proof point whose scale-up economics development will determine commercial adoption timeline.

Carbon fibre demand from wind turbine blade production and offshore wind expansion represents the most commercially certain near-term growth opportunity for premium acrylonitrile. Each gigawatt of new wind energy capacity requires carbon fibre composite blade structures whose PAN precursor procurement creates high-purity acrylonitrile demand that scales with renewable energy installation growth.

Recent Developments:

-

2023: LG Chem partnered with a major EV manufacturer in 2023 to supply high-performance ABS materials for next-generation electric vehicles, strengthening its position in the growing automotive ABS lightweighting market segment.

-

2024: Ascend Performance Materials piloted bio-feedstock acrylonitrile production in 2024, producing approximately 5% of its pilot batch from bio-derived propylene and targeting a 10% shift in future production capacity toward renewable feedstocks.

-

2024: Ineos retrofitted over 60% of its European acrylonitrile plants with VOC capture systems in 2024, improving emissions compliance by approximately 40% and positioning its European production assets for tightening EU air quality regulatory requirements.

Acrylonitrile Market Key Players:

-

Ineos Nitriles

-

Sinopec Group (CPCC)

-

PetroChina Company Ltd.

-

Ascend Performance Materials

-

Formosa Plastics Corporation

-

Asahi Kasei Chemicals

-

Jiangsu Sailboat Petrochemical Co., Ltd.

-

LG Chem Ltd.

-

INVISTA

-

Reliance Industries Ltd.

-

Evonik Industries AG

-

BASF SE

-

Adbri (Adelaide Brighton)

-

Solutia Inc. (Eastman Chemical)

-

Radici Chimica SpA

-

Toray Industries

-

Shandong Haili Chemical

-

Hebei Jinniu Chemical

-

Thai Acrylonitrile Co., Ltd.

-

Saratovorgsintez JSC

Acrylonitrile Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.36 Billion |

| Market Size by 2035 | USD 19.01 Billion |

| CAGR | CAGR of 3.54% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Application (ABS & SAN Resins, Acrylic Fibers, Nitrile Rubber, Acrylamide, Carbon Fiber, Others) • by Process Technology (Ammoxidation/SOHIO, Alternative/BP AMOCO Process, Others), Purity Grade (Above 99%, Up to 99%) • by End User (Automotive & Transportation, Electronics & Electrical, Textiles & Apparel, Construction, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Ineos Nitriles, Sinopec Group (CPCC), PetroChina Company Ltd., Ascend Performance Materials, Formosa Plastics Corporation, Asahi Kasei Chemicals, Jiangsu Sailboat Petrochemical Co., Ltd., LG Chem Ltd., INVISTA, Reliance Industries Ltd., Evonik Industries AG, BASF SE, Adbri (Adelaide Brighton), Solutia Inc. (Eastman Chemical), Radici Chimica SpA, Toray Industries, Shandong Haili Chemical, Hebei Jinniu Chemical, Thai Acrylonitrile Co., Ltd., Saratovorgsintez JSC |

Frequently Asked Questions

The Acrylonitrile Market is expected to grow at a CAGR of 3.54% from 2026 to 2035.

The Acrylonitrile Market was valued at USD 13.36 Billion in 2025.

Expanding automotive and electronics industries creating growing ABS resin demand, and carbon fibre PAN precursor adoption in renewable energy and aerospace applications creating premium acrylonitrile demand with above-average per-unit commercial value.

ABS & SAN Resins dominated the Acrylonitrile Market with approximately 49% share in 2025, while the Acrylic Fiber segment is the fastest growing.

Asia Pacific dominated the Acrylonitrile Market in 2025 with approximately 52% of global revenues, with China accounting for approximately 54.6% of Asia Pacific revenues. North America is the fastest-growing region.

Get in Touch