Power Electronic Testing Market Report Scope & Overview:

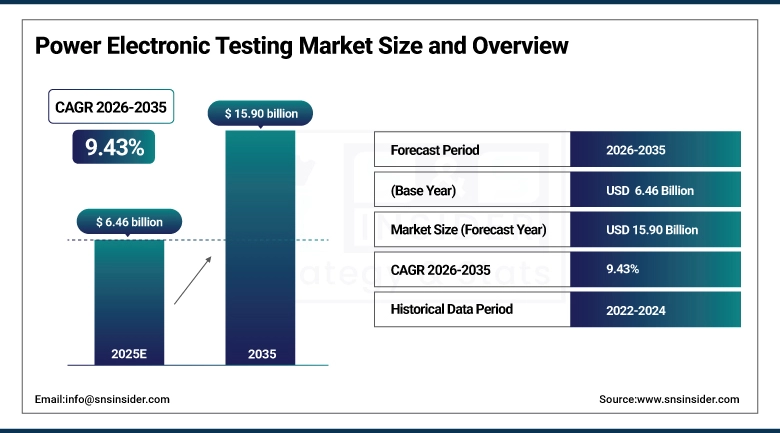

The Power Electronic Testing Market size was valued at USD 6.46 Billion in 2025 and is projected to reach USD 15.90 Billion by 2035, growing at a CAGR of 9.43% during 2026–2035.

The power electronic testing market is experiencing robust growth due to the increasing adoption of electric vehicles, renewable energy systems, and advanced semiconductor materials including SiC and GaN are driving strong growth in the power electronic testing market. Such technologies require deadline-bound testing solutions that accurately characterize the powertrain performance of, and assure safety and optimize energy efficiency in these technologies with relentless efficiency and reliability. The scope of power electronic testing is expanding to include multi-mode, thermal, and high-voltage aspects, driven by the integration of digital control and IoT, increasing system complexity and interdependence.

Power Electronic Testing Market Size and Forecast:

-

Market Size in 2025: USD 6.46 Billion

-

Market Size by 2035: USD 15.90 Billion

-

CAGR: 9.43% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Power Electronic Testing Market - Request Free Sample Report

Power Electronic Testing Market Key Trends:

-

Rising adoption of SiC and GaN semiconductors is increasing demand for advanced high-voltage and high-efficiency power electronics testing solutions.

-

Rapid growth of electric vehicles (EVs) is driving testing requirements for inverters, power modules, and battery management systems.

-

Increasing deployment of automated test equipment (ATE) is improving testing accuracy, efficiency, and high-volume semiconductor production.

-

Expansion of renewable energy systems is boosting testing needs for power converters, inverters, and grid-connected electronics.

-

Growing focus on reliability and compliance testing is encouraging adoption of advanced validation tools across semiconductor and electronics industries

U.S. Power Electronic Testing Market Size Outlook

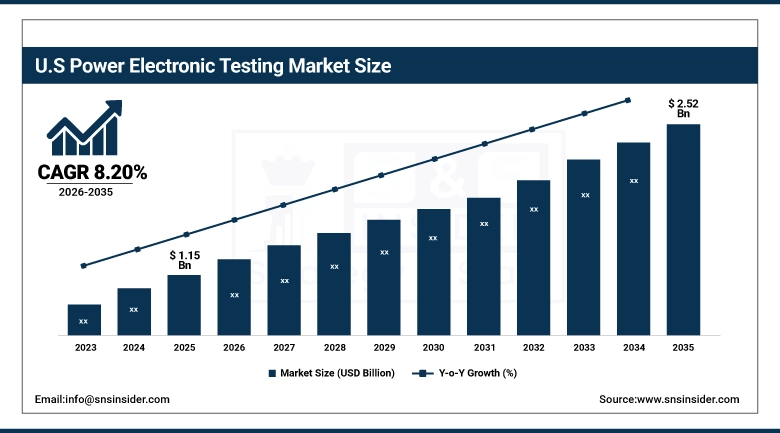

The U.S. Power Electronic Testing Market has been valued at USD 1.15 Billion in 2025 and is expected to reach USD 2.52 Billion in 2035, growing at a CAGR of 8.20% from 2026 to 2035. Growth is driven by increase in use of electric vehicles, renewable energy systems, and advance semiconductor, such as SiC and GaN. Automotive, energy, and industrial applications are generating strong growth in demand for various testing solutions to ensure efficiency, reliability, and compliance to these technologies that require precise, high-voltage, and high frequency testing.

Power Electronic Testing Market Key Drivers:

-

Growing Adoption of Advanced Semiconductors Fuels Demand for Power Electronic Testing

The power electronic testing market is driven by factors such as the rising demand for testing solutions due to the rising importance of advanced semiconductor materials such as silicon carbide (SiC) in high-performance applications. These semiconductor materials must be tested extensively for durability, temperature, and high voltage. These factors are driving the market for power electronic testing. In addition, the complexity of power electronic systems in various applications such as electric vehicles, renewable energy systems, and aerospace is another factor driving the market for power electronic testing. These systems must be tested accurately to ensure their safety and efficacy. Thus, power electronic testing is significant in developing next-generation power electronic systems.

China successfully orbit tested a new silicon carbide (SiC) power device aboard Tianzhou-8, the spacecraft demonstrating its efficiency and radiation resistance for potential aerospace applications. China's aspirations for advanced lightweight energy systems for its lunar and deep space missions are supported by this breakthrough.

Power Electronic Testing Market Key Restraints:

-

High Equipment Costs Limit SME Participation, Slowing Innovation and Competition in Power Electronic Testing

The high cost of the latest technology in test equipment, in particular, in systems that deal with wide bandgap semiconductors such as silicon carbide (SiC) and gallium nitride (GaN), is a major constraint in the power electronic test market. This involves making a huge investment in capital-costly test equipment that can deal with high-frequency and high-voltage signals, to say the least. Having such technology at one's disposal may not be financially viable for a small or medium-sized enterprise (SME), thus making them unable to enter or compete in the market. There may also be other expenses, such as that of hiring specialists. These barriers not only affect the development of new technology or products, but also play a role in market concentration, where fewer players in the market result in less competition, thus affecting the rate at which the technology will be adopted.

Power Electronic Testing Market Key Opportunities:

-

Rising Complexity in High-voltage, Multi-channel Systems Creates Demand for Advanced Power Electronic Testing Solutions

As power electronic systems become increasingly complex with high voltage and multi-channel architectures, and advanced semiconductor materials, it is critical to have precise and high-bandwidth testing tools. This trend presents significant market opportunities for testing solutions that provide galvanic isolation, high-frequency accuracy, and parallel testing capabilities. The electric vehicle, renewable energy, and aerospace industries are some of the emerging and high-growth applications that may increasingly demand compact and high-performance test tools with high efficiency in handling different voltage and current ranges. The emphasis on energy recovery, miniaturization, and integration in modern systems is creating a significant demand for high-end and multi-functional testing equipment.

Power Electronic Testing Market Segments:

-

By Provision Type: In 2025, Test Instruments and Equipment dominated with 66% share; Professional Testing Services is the fastest growing segment during 2026–2035.

-

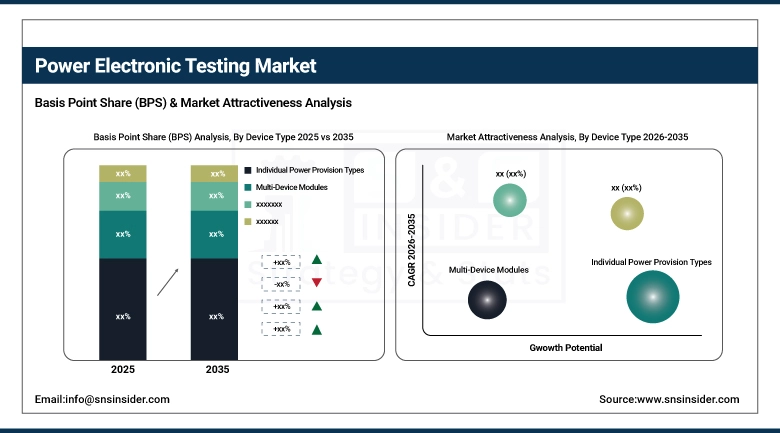

By Device Type: In 2025, Individual Power Devices dominated with 47% share; Multi-Device Modules is the fastest growing segment during 2026–2035.

-

By End Use: In 2025, Consumer Electronics and Devices dominated with 30% share; Automotive and Mobility Solutions is the fastest growing segment during 2026–2035.

By Device Type: Individual Power Devices Dominates, Multi-Device Modules Fastest-Growing

Individual power devices lead the market, with discrete devices like MOSFETs, IGBTs, and Diodes being used universally in consumer electronics, automotive electronics, and various industrial applications. Due to high volumes, extensive testing of performance and reliability of the devices is necessary.

Multi-device modules are growing at the highest rate, with increased demand for electric vehicle technology, renewable energy systems, and various industrial applications, which are incorporating various forms of integrated power modules, thereby increasing the demand for sophisticated testing solutions.

By Provision Type: Test Instruments and Equipment Dominates, Professional Testing Services Fastest-Growing

Test instruments and equipment hold the major market share in the power electronic test market due to the increasing demand for precise measurement, validation, and reliability test requirements of power semiconductors, converters, and inverters. Semiconductor manufacturers and EV component manufacturers are investing heavily in advanced test systems to ensure the quality of their products and meet international standards.

Professional test services have shown high growth in the market due to the increasing demand for outsourcing test and validation services. The increasing complexity in SiC and GaN devices is also encouraging manufacturers to seek professional test service providers.

By End Use: Consumer Electronics and Devices Dominates, Automotive and Mobility Solutions Fastest-Growing

Consumer electronics and devices dominate the market, as the high volume of smartphone, laptop, charger, and home appliance manufacturing necessitates the constant testing of power management devices. The high rate of product development and high-performance requirements make it imperative to test power management devices throughout the manufacturing process.

Automotive and mobility solutions represent the fastest-growing segment mainly because of the increasing adoption of electric vehicles and hybrid technologies. The power electronics used in EV inverters, chargers, and battery management systems need to be tested with high efficiency.

Power Electronic Testing Market Regional Analysis:

Asia-Pacific Power Electronic Testing Market Insights:

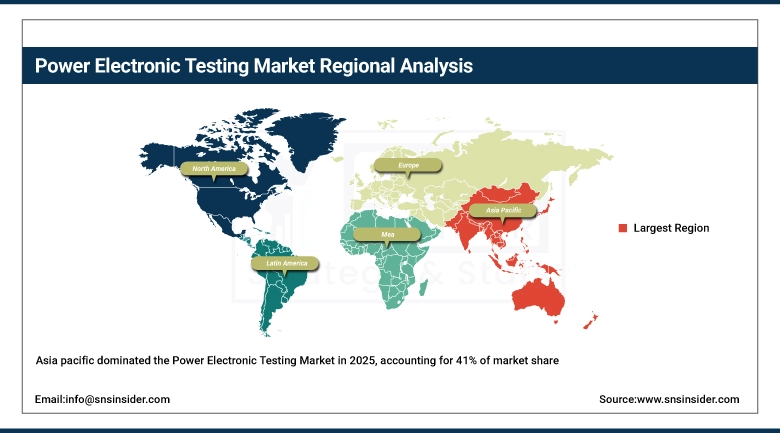

Asia-Pacific dominates the Power Electronic Testing Market , holding a market share of 41% 2025, The region’s leadership is due to its established semiconductor industry and high semiconductor device production in countries like China, Japan, South Korea, and Taiwan. Asia-Pacific is experiencing tremendous growth in the production of electric vehicles, renewable energy devices, and industrial automation, thus boosting the need for advanced power electronic devices testing. In addition, the presence of key players in the electronics industry, increasing investments in SiC and GaN-based power semiconductor devices, and government initiatives in clean energy and electric vehicles are boosting the Asia-Pacific Power Electronic Testing market.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Power Electronic Testing Market Insights:

North America is found to be the fastest-growing region in the Power Electronic Testing Market during the forecast period. This is due to increased investments in EV tech, advanced semiconductor materials, and power electronics technologies in the United States and Canada. The presence of major testing solution vendors and increased demand for SiC and GaN-based power devices in North America are contributing to the growth of the market in this region. In addition, government policies and funding for clean energy, electrification, and domestic semiconductor production are further driving the growth of the market in North America.

Europe Power Electronic Testing Market Insights:

Europe offers a promising market opportunity for power electronic test services, given the strong growth rate in electrification of automobiles, renewable power, and advanced industrial automation. Countries like Germany, France, the UK, and Italy play a major role in the European market. These countries have already established industries in the fields of automobiles and semiconductors. Moreover, the increasing use of electric vehicles, power modules, and efficient power electronic systems will boost the market for power electronic test services. In addition, investments in SiC and GaN semiconductor technology, smart grids, and aerospace will also boost the market for power electronic test services.

Latin America Power Electronic Testing Market Insights:

Latin America power electronic testing market is gradually expanding due to growing adoption of industrial automation, renewable energy projects, and consumer electronics manufacturing. Countries such as Brazil and Mexico are leading the demand, supported by increasing investments in electronics production, automotive electrification, and modernization of power infrastructure across the region.

Middle East & Africa (MEA) Power Electronic Testing Market Insights:

Middle East & Africa power electronic testing market is growing steadily due to increasing investments in renewable power projects, modernization of power infrastructure, and growth in industries. Countries like the UAE, Saudi Arabia, and South Africa are using advanced power electronics in solar power systems, telecommunication systems, and industries. In addition, the increasing demand for reliable power systems and growth in the electronics and automotive industries also fuel the use of advanced power electronic testing systems.

Power Electronic Testing Market Competitive Landscape:

Keysight Technologies, Inc., headquartered in Santa Rosa, California, USA, is a global leader in electronic measurement and testing solutions, including advanced systems for power electronics testing, semiconductor validation, and power device characterization. The company provides high-precision instruments, automated test systems, and software platforms used to evaluate power semiconductors, inverters, converters, and EV powertrain components. Keysight serves industries such as automotive, semiconductor manufacturing, telecommunications, and renewable energy, helping manufacturers ensure performance, efficiency, and regulatory compliance in next-generation power electronics.

-

In 2025: Keysight expanded its power semiconductor testing portfolio with advanced solutions supporting SiC and GaN device testing, strengthening partnerships with EV and semiconductor manufacturers to address the growing demand for high-efficiency power electronics.

Advantest Corporation, headquartered in Tokyo, Japan, is a leading provider of semiconductor automatic test equipment (ATE) and power device testing solutions used across the global electronics industry. The company develops advanced testing systems that evaluate the performance, reliability, and functionality of power ICs, discrete devices, and integrated power modules. Advantest’s technologies support key industries such as consumer electronics, automotive electronics, industrial automation, and telecommunications, enabling manufacturers to ensure product quality and production efficiency.

-

In 2025: Advantest strengthened its power semiconductor testing capabilities by enhancing ATE platforms designed for high-performance power devices and advanced packaging technologies, supporting increasing demand from EV, AI, and high-performance computing applications.Top of FormBottom of Form

Power Electronic Testing Companies are:

-

Keysight Technologies, Inc

-

Advantest Corporation

-

Teradyne, Inc.

-

Rohde & Schwarz GmbH & Co. KG

-

AMETEK, Inc.

-

Yokogawa Electric Corporation

-

National Instruments (Emerson Electric Co.)

-

Viavi Solutions Inc

-

Anritsu Corporation

-

Hioki E.E. Corporation

-

ITECH Electronic Co., Ltd.

-

GW Instek (Good Will Instrument Co., Ltd.)

-

Tektronix, Inc.

-

EA Elektro-Automatik GmbH & Co. KG

-

California Instruments (AMETEK Programmable Power)

-

Maccor, Inc.

-

NH Research, Inc.

-

Preen (AC Power Corp.)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.46 Billion |

| Market Size by 2035 | USD 15.90 Billion |

| CAGR | CAGR of 9.43% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Provision Type: (Test Instruments and Equipment, Professional Testing Services) • By Device Type: (Individual Power Provision Types, Multi-Device Modules, Power Management ICs) • By End Use: (Industrial Automation and Machinery, Automotive and Mobility Solutions, Information & Communication Technology (ICT), Consumer Electronics and Devices, Renewable Power and Utility Networks, Aerospace and Defense Applications, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Keysight Technologies, Inc., Advantest Corporation, Teradyne, Inc., Chroma ATE Inc., Rohde & Schwarz GmbH & Co. KG, AMETEK, Inc., Yokogawa Electric Corporation, National Instruments (Emerson Electric Co.), Teledyne LeCroy, Inc., Viavi Solutions Inc., Anritsu Corporation, Hioki E.E. Corporation, ITECH Electronic Co., Ltd., GW Instek (Good Will Instrument Co., Ltd.), Tektronix, Inc., EA Elektro-Automatik GmbH & Co. KG, California Instruments (AMETEK Programmable Power), Maccor, Inc., NH Research, Inc., Preen (AC Power Corp.). |

Frequently Asked Questions

Asia-Pacific dominated the Power Electronic Testing Market in 2025.

The Test Instruments and Equipment segment dominated during the projected period.

The key drivers of the Power Electronic Testing Market include rising EV adoption, renewable energy growth, SiC/GaN devices, industrial automation, and reliability compliance.

The market was valued at USD 6.46 Billion in 2025 and is projected to reach USD 15.90 Billion by 2035.

The Power Electronic Testing Market is expected to grow at a CAGR of 9.43% during 2026–2035.

Get in Touch