Ultrafast Laser Market Report Scope & Overview:

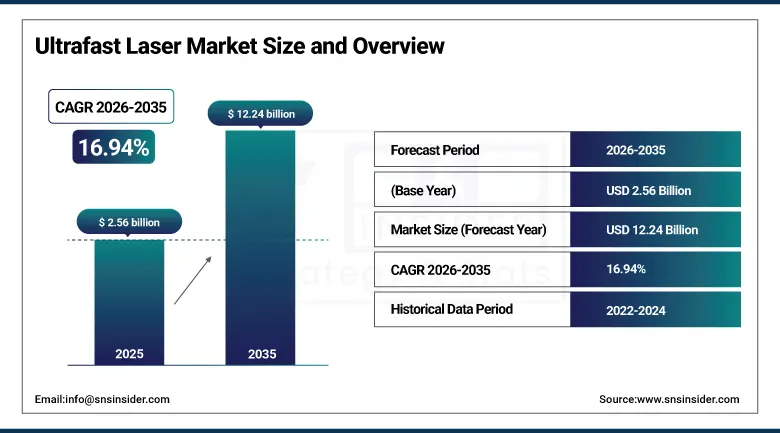

The Ultrafast Laser Market was valued at USD 2.56 billion in 2025 and is expected to reach USD 12.24 billion by 2035, growing at a CAGR of 16.94% from 2026-2035.

The ultra-fast laser market is expanding because there is an increased demand for micromachining applications in the sectors of electronics, medical devices, and semiconductors. The increased use of ultra-fast lasers in healthcare for surgery and imaging purposes and development in photonics and automation industry are other factors supporting the growth in the market.

The U.S. Department of Energy's Office of Science has funded ultrafast laser research through its Basic Energy Sciences program, with the Linac Coherent Light Source (LCLS-II) at SLAC National Accelerator Laboratory representing a USD 1 billion+ ultrafast photon science investment. The National Eye Institute reports that LASIK and advanced corneal surgeries using femtosecond lasers now account for over 85% of all refractive surgeries performed in the United States.

Ultrafast Laser Market Size and Forecast

-

Market Size in 2025: USD 2.56 Billion

-

Market Size by 2035: USD 12.24 Billion

-

CAGR: 16.94% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Ultrafast Laser Market - Request Free Sample Report

Ultrafast Laser Market Trends

-

Semiconductor advanced packaging applications including through-silicon via drilling and chiplet interconnect processing are creating new high-volume ultrafast laser application categories as packaging complexity increases with AI chip architectures.

-

EV battery electrode microstructuring using ultrafast lasers is gaining commercial adoption as manufacturers seek to improve lithium-ion battery energy density through precision electrode surface modification without thermal damage.

-

Ultrafast laser system costs are declining as fiber laser technology matures, bringing the technology within reach of industrial manufacturers who previously could not justify the investment in slower-growing market segments.

-

Attosecond laser science enabled by Nobel Prize-winning techniques for generating attosecond light pulses is transitioning from purely academic research toward applied science instrumentation with commercial platform potential.

-

Biophotonics applications including multiphoton microscopy, coherent anti-Stokes Raman scattering spectroscopy, and nonlinear optical imaging are creating specialized ultrafast laser demand in life science research and clinical diagnostics.

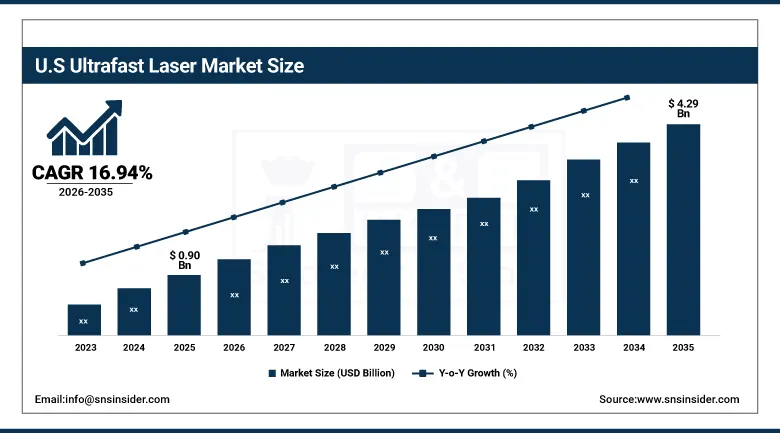

U.S. Ultrafast Laser Market was valued at USD 0.90 billion in 2025 and is expected to reach USD 4.29 billion by 2035, growing at a CAGR of 16.94% from 2026-2035.

The ultrafast lasers market in the United States is expanding because of the high demand for semiconductor manufacturing, the development of medical devices, and research purposes. Investments in photonics, precision micromachining, and military applications will further aid the market growth.

The American Academy of Ophthalmology reports that over 700,000 LASIK procedures are performed annually in the United States, the majority using femtosecond laser flap creation technology. The U.S. CHIPS Act has allocated USD 52 billion for domestic semiconductor manufacturing, creating procurement pull for advanced laser processing equipment including ultrafast systems for next-generation packaging applications.

Ultrafast Laser Market Segment Analysis

-

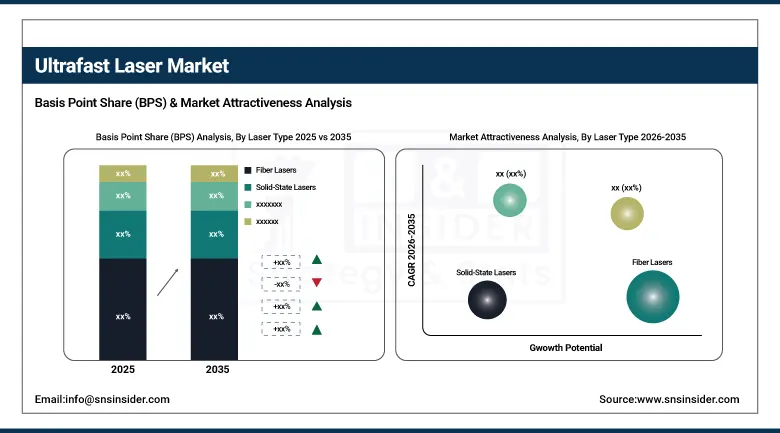

By Laser Type, Fiber Lasers dominated with ~41.3% share in 2025; Mode-locked Lasers fastest growing (CAGR).

-

By Pulse Duration, Femtosecond Lasers dominated with ~49.6% share in 2025; Attosecond Lasers fastest growing (CAGR).

-

By Application, Material Processing dominated the Ultrafast Laser Market in 2025; Medical & Healthcare fastest growing (CAGR).

By Laser Type, Fiber Lasers segment dominates the Ultrafast Laser Market, Mode-locked Lasers expected to grow fastest

Fiber Lasers held the dominant laser type share of approximately 41.3% in 2025. This leadership reflects fiber lasers' outstanding combination of efficiency, reliability, and cost-effectiveness relative to other ultrafast laser architectures. Fiber ultrafast lasers leverage the mature manufacturing ecosystem developed for telecommunications fiber components, benefiting from economies of scale that solid-state and mode-locked systems cannot match at comparable performance levels. Their high wall-plug efficiency typically 20-30% versus 5-10% for solid-state systems reduces operating costs in production environments where laser runtime is a significant operational expense.

Mode-locked Lasers are expected to register the fastest CAGR through 2035, driven by their unmatched pulse duration stability and coherence properties that make them indispensable for advanced scientific applications in biomedical imaging, attosecond physics, and spectroscopy. Their outstanding pulse characteristics enable applications including multiphoton microscopy that requires precise control of pulse duration, peak power, and repetition rate to achieve optimal nonlinear excitation of biological fluorophores without photodamage.

By Pulse Duration, Femtosecond Lasers segment dominates the Ultrafast Laser Market, Attosecond Lasers expected to grow fastest

Femtosecond Lasers held the dominant pulse duration share of approximately 49.6% in 2025, reflecting the commercial maturity of femtosecond technology across ophthalmic surgery, precision micromachining, and scientific research applications. Their extremely short pulse duration typically 100-500 femtoseconds produces minimal heat-affected zones during material processing while delivering sufficient peak power for highly efficient laser-matter interaction. In ophthalmic surgery, femtosecond lasers have become the gold standard for LASIK flap creation and cataract lens fragmentation, where their precision and reproducibility exceed mechanical alternatives. In micromachining, femtosecond systems achieve cutting quality on glasses, ceramics, and polymers that nanosecond and picosecond lasers cannot replicate with equivalent edge quality.

Attosecond Lasers are expected to grow at the highest pulse duration CAGR, driven by the profound scientific significance of attosecond physics and the commercial instrumentation that the Nobel Prize-validated science is beginning to generate. Attosecond lasers produce pulses in the range of 100-1,000 attoseconds short enough to capture electron dynamics within atoms and molecules enabling direct observation of chemical bond formation and breaking, electron correlation phenomena, and ultrafast charge transfer processes that are invisible to longer-pulse laser probes. As attosecond laser technology transitions from proof-of-concept to standardized research platforms, commercial instrument manufacturers are developing accessible attosecond laser systems that research institutions worldwide can purchase and operate without requiring specialized laser physics expertise.

By Application, Material Processing segment dominates the Ultrafast Laser Market, Medical & Healthcare expected to grow fastest

Material Processing maintained the dominant application position in the Ultrafast Laser Market in 2025, reflecting the broad and growing industrial adoption of ultrafast laser precision across electronics manufacturing, aerospace component fabrication, and advanced materials processing. Semiconductor and electronics manufacturing applications including via drilling in printed circuit boards, LCD glass cutting, solar cell scribing, and advanced packaging processes represent the highest-volume material processing deployment. Aerospace applications require ultrafast laser precision for turbine blade cooling hole drilling and composite material cutting where thermal damage is structurally unacceptable. Each of these industrial applications represents a steady-state procurement requirement rather than a one-time adoption event, sustaining material processing as the anchor application segment.

Medical & Healthcare is the fastest-growing application segment, driven by expanding clinical adoption across ophthalmology, dermatology, oncology, and neurosurgery, combined with growing demand in life science research instrumentation. Femtosecond laser ophthalmic platforms for LASIK, SMILE, and cataract surgery have become mainstream clinical tools in developed markets and are expanding rapidly into emerging markets as system costs decline. Dermatology applications including ultrashort pulse tattoo removal, skin resurfacing, and melanoma treatment represent growing clinical markets where ultrafast lasers achieve results that conventional laser modalities cannot match in terms of precision and collateral tissue damage minimization. The biophotonics research market multiphoton microscopy, optical coherence tomography, and coherent Raman imaging — adds high-value scientific instrumentation demand that sustains premium pricing in the medical applications segment.

Ultrafast Laser Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

86% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

Japan |

40% |

|

Middle East & Africa |

Israel |

35% |

|

Latin America |

Brazil |

45% |

North America Ultrafast Laser Market Insights

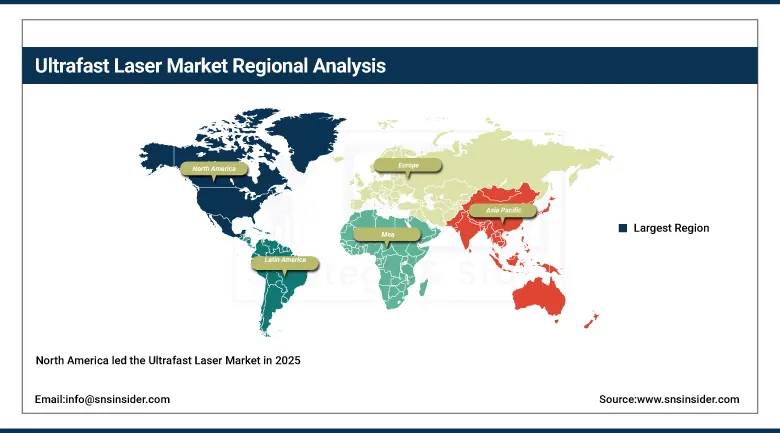

North America led the Ultrafast Laser Market in 2025, anchored by the U.S. combination of world-class ultrafast laser research programs, a mature medical laser surgery market, the semiconductor industry's growing ultrafast laser procurement, and the presence of leading ultrafast laser manufacturers including Coherent Corp., II-VI, and Newport. Federal research investment through DOE national laboratories particularly Lawrence Berkeley National Laboratory and SLAC sustains the frontier science that feeds into commercial ultrafast laser product development. The U.S. ophthalmic surgery market generates consistent femtosecond laser system procurement at large volumes as LASIK center upgrades and new clinical site openings sustain demand independent of research funding cycles.

The U.S. National Science Foundation's Major Research Instrumentation program funds ultrafast laser laboratory equipment at universities nationwide, creating institutional research demand that transitions to commercial procurement as technologies mature. Coherent Corp.'s annual report documents laser revenue growth across semiconductor, scientific, and medical end markets as ultrafast technology penetrates new industrial and clinical applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe and Asia Pacific Ultrafast Laser Market Insights

Europe held approximately 25% of the global Ultrafast Laser Market in 2025, with Germany, France, and the UK as the primary markets. Europe's strength in scientific instrumentation manufacturing including ultrafast laser-based spectroscopy and microscopy systems from companies including Trumpf (Germany), Toptica Photonics (Germany), and Amplitude Laser (France) sustains both production and domestic consumption of ultrafast laser technology. Asia Pacific is the fastest-growing regional market, driven by Japan's precision manufacturing and scientific research intensity, South Korea's semiconductor manufacturing, China's rapidly growing laser processing industry, and Taiwan's advanced PCB and display manufacturing sectors where ultrafast laser precision is increasingly specified for next-generation products. The region's manufacturing density creates industrial ultrafast laser demand that is growing faster than any other geographic market.

Japan's Ministry of Economy, Trade and Industry (METI) has funded ultrafast laser manufacturing technology programs as part of Japan's manufacturing competitiveness strategy. China's 14th Five-Year Plan specifically identifies high-power laser technology as a strategic manufacturing capability, driving state-supported investment in domestic ultrafast laser system development and procurement.

Ultrafast Laser Market Growth Drivers:

-

Surging precision manufacturing demand and medical applications expansion driving global ultrafast laser market growth

Ultrafast laser adoption is being pulled by industrial and clinical quality requirements that conventional laser and mechanical processing cannot satisfy. In semiconductor manufacturing, the transistor density progression that Moore's Law describes requires ever-smaller feature processing with decreasing thermal budgets a requirement that ultrafast lasers meet through their minimal heat-affected zone processing. In EV battery manufacturing, micro structuring electrode surfaces to increase accessible surface area improves battery capacity without increasing material content a performance improvement only achievable through the precision that ultrafast processing delivers. In clinical medicine, the precision and tissue selectivity of femtosecond laser surgery consistently produces better patient outcomes than conventional surgical techniques, creating an evidence-based adoption pull that regulatory approvals and clinical guidelines are formalizing. Each of these drivers is structural and long-duration, sustaining demand growth that is not dependent on individual technology cycles.

The International Society of Refractive Surgery reports that femtosecond laser-assisted LASIK procedures produce statistically superior visual outcomes compared to mechanical microkeratome procedures, with lower rates of flap complications that have been documented in multiple large-scale clinical studies. The Semiconductor Industry Association projects that advanced packaging adoption a major ultrafast laser application will encompass over 80% of high-performance computing chips by 2027.

Ultrafast Laser Market Restraints:

-

High system costs and operational complexity limiting ultrafast laser adoption among smaller manufacturers and clinical facilities

Ultrafast laser systems represent a significant capital investment typically USD 50,000 to over USD 1 million per system depending on pulse duration, average power, and application-specific configuration that creates meaningful barriers for small and medium-sized industrial manufacturers and independent clinical practices. The sophistication of ultrafast laser operation requires personnel trained in laser physics and optics who understand how to optimize pulse parameters for specific material interactions, maintain beam quality over time, and troubleshoot alignment and performance issues that arise in production environments. This human capital requirement adds to total cost of ownership in ways that standardized automation solutions cannot fully resolve. Unlike conventional laser cutting or welding systems, ultrafast laser tools require significant application engineering investment before reliable production deployment, extending payback timelines that budget-conscious potential adopters find challenging.

Ultrafast Laser Market Opportunities:

-

Semiconductor advanced packaging and quantum technology fabrication creating transformative ultrafast laser growth opportunities

The semiconductor industry's transition to chiplet architectures and 3D advanced packaging is creating a rapidly growing ultrafast laser application category that has no direct precedent in the technology's commercial history. Via drilling in glass interposers, hybrid bonding surface preparation, heterogeneous integration component singulation, and photonic integrated circuit fabrication each require the combination of precision and minimal thermal budget that only ultrafast laser processing reliably delivers. As leading logic, memory, and custom silicon companies commit to advanced packaging roadmaps that extend well into the 2030s, the ultrafast laser equipment procurement that supports those roadmaps represents a durable and growing revenue opportunity. Quantum technology fabrication creating the ion traps, photonic waveguides, and nitrogen-vacancy center arrays that quantum computing and quantum sensing devices require is separately emerging as a premium application where ultrafast laser precision is uniquely enabling.

Recent Developments:

-

2025: Coherent Corp. introduced its Monaco femtosecond laser platform with enhanced power scalability reaching 80W average power at 1035nm, targeting high-throughput semiconductor advanced packaging applications including glass interposer via drilling and dicing of ultra-thin silicon wafers where processing speed directly determines production economics.

-

2025: Trumpf launched its TruMicro Series 5000 ultrafast laser with integrated beam shaping optics enabling burst mode pulse delivery that improves material removal rates by 40% compared to conventional single-pulse ultrafast processing, targeting automotive glass cutting, display manufacturing, and aerospace composite material ablation applications.

-

2026: Amplitude Laser demonstrated its first commercial attosecond laser platform — the Synapsis — achieving reliable single-shot attosecond pulse generation accessible to users without specialized ultrafast laser physics expertise, marking the transition of attosecond science from national laboratory exclusive to commercially available research instrumentation.

Ultrafast Laser Market Key Players

Some of the Ultrafast Laser Market Companies

-

Coherent Corp.

-

II-VI Incorporated (Coherent)

-

IPG Photonics Corporation

-

Trumpf GmbH + Co. KG

-

Lumentum Holdings Inc.

-

Amplitude Laser Group

-

Toptica Photonics AG

-

Newport Corporation (MKS Instruments)

-

Spectra-Physics (MKS)

-

Ekspla UAB

-

Light Conversion Ltd.

-

Menlo Systems GmbH

-

IMRA America Inc.

-

Class 5 Photonics

-

NKT Photonics A/S

-

Fianium Ltd. (NKT Photonics)

-

Quantel Laser (Lumibird)

-

Attodyne Inc.

-

Laser Quantum Ltd.

-

JDSU (Viavi Solutions)

Ultrafast Laser Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.56 Billion |

| Market Size by 2035 | USD 12.24 Billion |

| CAGR | CAGR of 16.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Laser Type (Fiber Lasers, Solid-State Lasers, Mode-Locked Lasers, Others) • By Pulse Duration (Picosecond Lasers, Femtosecond Lasers, Attosecond Lasers) • By Application (Material Processing, Medical & Healthcare, Scientific Research & Development, Automotive & Aerospace, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Coherent Corp., II-VI Incorporated (Coherent), IPG Photonics Corporation, Trumpf GmbH + Co. KG, Lumentum Holdings Inc., Amplitude Laser Group, Toptica Photonics AG, Newport Corporation (MKS Instruments), Spectra-Physics (MKS), Ekspla UAB, Light Conversion Ltd., Menlo Systems GmbH, IMRA America Inc., Class 5 Photonics, NKT Photonics A/S, Fianium Ltd. (NKT Photonics), Quantel Laser (Lumibird), Attodyne Inc., Laser Quantum Ltd., JDSU (Viavi Solutions) |

Frequently Asked Questions

Ans: North America dominated the Ultrafast Laser Market in 2025.

Ans: The Medical & Healthcare segment is expected to register the fastest CAGR in the Ultrafast Laser Market.

Ans: The Fiber Lasers segment dominated with approximately 41.3% share in 2025.

Ans: The Ultrafast Laser Market was valued at USD 2.56 billion in 2025.

Ans: The Ultrafast Laser Market is expected to grow at a CAGR of 16.94% from 2026 to 2035.

Get in Touch