Premium Messaging Market Report Scope & Overview:

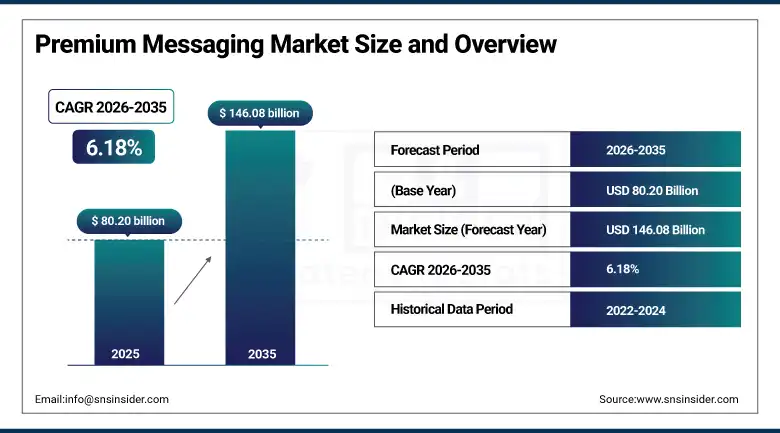

The Premium Messaging Market was valued at USD 80.20 Billion in 2025 and is expected to reach USD 146.08 Billion by 2035, growing at a CAGR of 6.18% from 2026–2035.

Premium messaging encompasses the commercial messaging services through which enterprises communicate with consumers at scale using SMS, MMS, and emerging Rich Communication Services channels. Application-to-person messaging, commonly designated A2P, is the core commercial format in which software systems send messages to individual mobile subscribers. Banking transaction alerts, one-time passcodes for two-factor authentication, delivery notifications, appointment reminders, marketing promotions, and emergency public alerts are all A2P messaging use cases whose combined volume reaches billions of messages globally every day. Person-to-application messaging, P2A, enables consumers to interact with enterprise systems through mobile messaging channels, initiating transactions, requesting information, or triggering automated service responses.

Google's RCS platform reached 550 million monthly active users globally, reflecting the accelerating enterprise adoption of Rich Communication Services as a higher-capability successor to plain-text SMS. Sinch reported that 53% of its Q2 2025 revenue came from messaging services, confirming that A2P SMS and MMS continue to generate the majority of premium messaging revenue even as RCS adoption grows alongside the established text messaging base.

Market Size and Forecast

-

Market Size in 2026E: USD 85.16 Billion

-

Market Size by 2035: USD 146.08 Billion

-

CAGR: 6.18% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Premium Messaging Market - Request Free Sample Report

Premium Messaging Market Trends

-

Rising adoption of Rich Communication Services (RCS) is enhancing enterprise messaging with interactive and branded communication features.

-

AI-powered conversational messaging is improving personalized customer engagement and campaign optimization.

-

Growing use of two-factor authentication and OTP messaging is driving A2P messaging traffic globally.

-

Expanding anti-fraud and data privacy regulations are increasing demand for compliant premium messaging platforms.

-

CPaaS platform integration is enabling unified management of SMS, RCS, email, voice, and messaging applications.

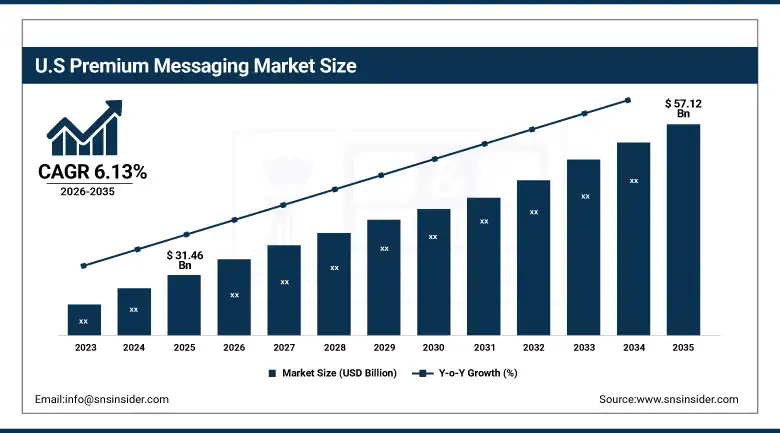

The U.S. Premium Messaging Market Outlook

The U.S. Premium Messaging Market was valued at approximately USD 31.46 Billion in 2025 and is expected to reach approximately USD 57.12 Billion by 2035, growing at a CAGR of 6.13%.

The United States is the world's largest single-country premium messaging market, representing nearly 39% of global revenues, a concentration reflecting the country's advanced CPaaS ecosystem, the highest enterprise digital communication investment globally, and the U.S. regulatory framework that has structured the commercial A2P messaging market in ways that sustain above-average revenue per message relative to markets with less developed compliance infrastructure. Twilio, Bandwidth, Vonage, and Sinch have each established significant U.S. operations anchored by A2P SMS and MMS volumes generated by the country's largest enterprises across banking, retail, healthcare, and technology sectors.

The U.S. Federal Communications Commission's 2025 enforcement actions against A2P messaging spam resulted in USD 1.2 billion in proposed fines across non-compliant operators, reinforcing the 10DLC compliance framework's commercial value to enterprises whose registered campaigns are differentiated from spam through network-level filtering that improves message deliverability and consumer engagement rates.

Premium Messaging Market Segment Analysis

-

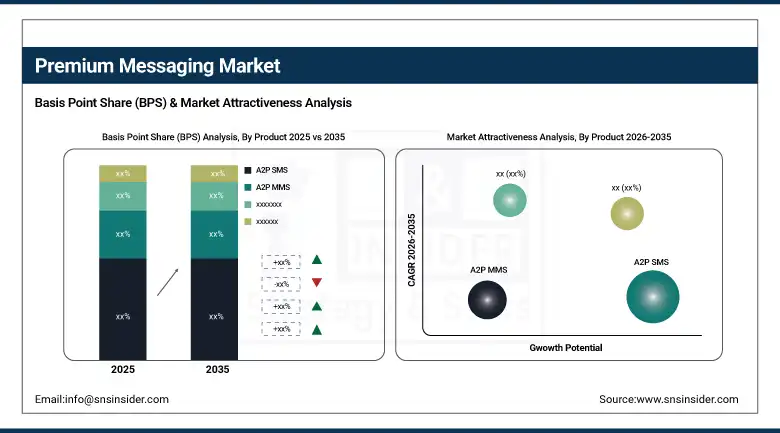

By Product, A2P SMS dominated the market with approximately 38.60% share in 2025 through its universal delivery reach across all mobile devices regardless of smartphone model, operating system, or data connectivity. A2P MMS is the fastest-growing product at a CAGR of approximately 7.43%.

-

By Application, BFSI held the largest share of approximately 34.20% in 2025 as banks, insurers, and fintech companies generate the highest volumes of transactional alerts, OTPs, fraud notifications, and payment confirmations among all enterprise messaging verticals. Retail is the fastest-growing application at a CAGR of approximately 7.81%.

-

By Enterprise Size, large enterprises dominated the market in 2025 through their higher messaging volumes, more complex multi-channel communication requirements, and larger digital communication budgets that justify enterprise CPaaS platform investment. SMEs are the fastest-growing segment as self-service messaging platform accessibility lowers the minimum viable investment threshold for business SMS and MMS marketing.

By Product, A2P SMS dominates, A2P MMS grows fastest

A2P SMS held approximately 38.60% of the premium messaging market in 2025. The commercial dominance of A2P SMS reflects its unique delivery characteristic that no alternative messaging channel can replicate: reliable message delivery to essentially every mobile phone on the planet, regardless of smartphone model, data plan, internet connectivity, or consumer app installation choices. An SMS message sent to a subscriber in rural India, sub-Saharan Africa, or a signal-challenged area of North America will arrive when it could not be delivered through WhatsApp, iMessage, or any data-dependent messaging alternative. This universal reach is the commercial justification for continued A2P SMS investment even as richer messaging alternatives grow in sophisticated consumer markets. The banking sector's requirement for OTP delivery to every account holder regardless of smartphone capability makes SMS the non-negotiable foundation of financial services messaging strategy.

A2P MMS is the fastest-growing product segment at a CAGR of approximately 7.43% through 2035. Multimedia messaging enables enterprise brands to deliver product images, promotional videos, animated GIFs, branded content cards, and interactive visual experiences through native mobile messaging channels without requiring consumer app installation. Research consistently demonstrates that MMS messages deliver higher open rates, click-through rates, and conversion rates than equivalent plain-text SMS messages for promotional and marketing communication use cases. The declining cost of MMS relative to its engagement premium is making it commercially attractive for retail, entertainment, and consumer brand advertisers who had previously viewed the cost differential versus SMS as prohibitive for high-volume campaigns.

By Application, BFSI dominates, retail grows fastest

BFSI held approximately 34.20% of the premium messaging market in 2025. Financial institutions are the most intensive enterprise users of A2P messaging because the nature of financial services generates a continuous, high-volume stream of transactional events requiring immediate consumer notification. Every card transaction, every account login, every fund transfer, every low-balance threshold breach, and every suspicious activity detection generates an alert message whose time-sensitive delivery is commercially and regulatorily critical. Digital banking adoption has intensified this structural demand by moving account management interactions online, creating more notification-triggering events per customer per day than branch-era banking generated. The banking sector's requirement for OTP-based two-factor authentication for every digital transaction has added a second parallel high-volume message stream that grows with digital banking adoption.

Retail is the fastest-growing application at a CAGR of approximately 7.81% through 2035. E-commerce growth is the most direct driver, as every online order generates a sequence of shipping confirmation, dispatch notification, out-for-delivery alert, and delivery confirmation messages that collectively constitute a per-order messaging consumption that grows with online retail volume. Marketing SMS and MMS campaigns from retailers promoting flash sales, loyalty rewards, personalized offers, and seasonal promotions are each growing as retailers quantify the commercial return on messaging investment and increase budgets for direct-to-consumer mobile communication. The growing adoption of conversational commerce, in which consumers initiate product enquiries, check order status, or complete purchases through messaging threads, is extending retail messaging use beyond one-way notification into two-way transactional dialogue.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.3% |

|

Europe |

United Kingdom |

28.6% |

|

Asia Pacific |

China |

36.4% |

|

Middle East & Africa |

UAE |

27.8% |

|

Latin America |

Brazil |

43.7% |

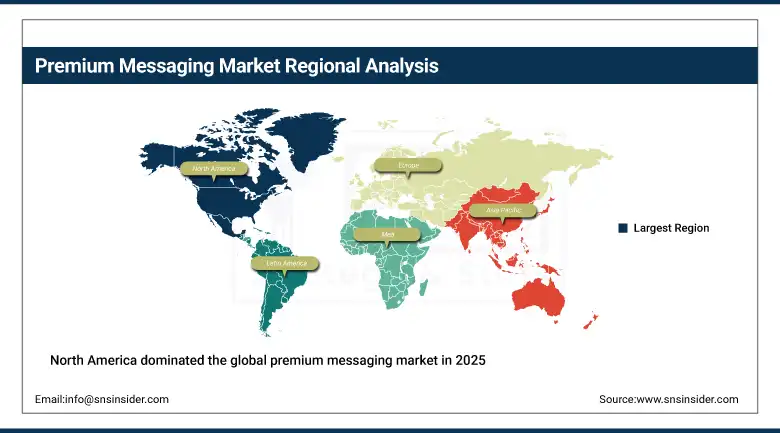

North America Premium Messaging Market Insights

North America dominated the global premium messaging market in 2025 with the largest regional share of approximately 36%, anchored by the United States' position as the world's most commercially developed enterprise messaging market. The United States accounts for approximately 82.3% of North American revenues through its concentration of global technology companies, largest enterprise digital communication budgets, and the 10DLC compliance framework that has structured the U.S. A2P messaging market into a commercially defensible quality tier commanding premium pricing. The CPaaS vendor ecosystem anchored by Twilio, Bandwidth, Vonage, and Sinch has built the technical and commercial infrastructure through which American enterprises manage their A2P messaging programmes at national scale.

Get Customized Report as per Your Business Requirement - Enquiry Now

Canada is a growing premium messaging market with strong enterprise adoption across banking, retail, and government sectors. Canadian financial institutions including the major banks are among the most active A2P messaging users in the country, generating high volumes of transactional alerts and authentication messages. Canadian anti-spam legislation creates a compliance framework for enterprise messaging that sustains premium managed platform demand among businesses seeking to navigate consent management and opt-out requirements with confidence. The Canadian mobile telecommunications market's high smartphone penetration rate supports strong engagement rates for enterprise A2P messaging campaigns.

Europe Premium Messaging Market Insights

Europe is a large and regulation-shaped premium messaging market where GDPR consent requirements, ePrivacy Directive rules on electronic marketing, and national telecommunications regulations collectively create the most complex compliance environment for enterprise A2P messaging outside the United States. The United Kingdom accounts for approximately 28.6% of European revenues as the region's most commercially active enterprise messaging market with the highest concentration of premium messaging platform providers and enterprise marketing technology investment. GDPR's explicit consent requirements for marketing SMS messaging have raised the commercial value of permission-based subscriber lists and created demand for consent management platform integration with A2P messaging infrastructure.

Germany, France, the Netherlands, and Scandinavia each represent significant European premium messaging markets. RCS adoption is advancing faster in Europe than in North America relative to existing SMS infrastructure, as European mobile network operators have been more active in RCS deployment programmes through the GSMA's universal profile initiative. Deutsche Telekom's active RCS commercial deployment across German subscribers is creating one of the most commercially developed RCS markets in the world, providing an early reference environment for the enterprise branded messaging experiences that RCS enables beyond SMS capability.

Asia Pacific Premium Messaging Market Insights

Asia Pacific is the fastest-growing premium messaging region at a CAGR of approximately 7.89% through 2035, driven by its position as the world's largest mobile subscriber market and the rapid enterprise messaging adoption across its major economies. China accounts for approximately 36.4% of Asia Pacific revenues through its extraordinary mobile ecosystem scale, the dominance of WeChat as an enterprise-to-consumer messaging channel supplementing SMS, and the regulatory structure of Chinese A2P messaging that routes commercial traffic through licensed aggregators under China Telecom, China Unicom, and China Mobile infrastructure. India is the world's second most important A2P messaging market by volume through the extraordinary scale of financial services, e-commerce, and government digital service messaging that its 1.4 billion mobile subscribers generate as digital transformation accelerates.

MEA & Latin America Premium Messaging Market Insights

Middle East and Africa and Latin America are growing premium messaging markets where mobile-first digital transformation, expanding financial services adoption, and rapid e-commerce development are creating enterprise messaging demand. The UAE leads MEA revenues at approximately 27.8% of the regional share through its advanced digital economy and the high enterprise messaging sophistication of its banking, retail, and government digital services sectors. South Africa, Nigeria, Kenya, and Egypt are each growing A2P messaging markets where mobile money, digital banking, and e-commerce platform adoption is generating the transactional and notification messaging volumes that sustain commercial messaging revenue. Brazil leads Latin American revenues at approximately 43.7% through its large digital economy, the extraordinary scale of its Pix instant payment network generating financial notification messaging, and the rapid expansion of WhatsApp Business as an enterprise-to-consumer communication channel alongside SMS.

Market Dynamics

Growth Drivers: Rising enterprise digital communication adoption, increasing two-factor authentication messaging demand.

Enterprise digital transformation is the foundational structural driver of premium messaging market growth. As enterprises move customer interactions from physical branches, call centres, and paper communications to digital channels, they generate message volume that grows with every percentage point of digital adoption. Banking customers who previously received paper statements now receive monthly balance alerts and every transaction notification by SMS. Retail customers who previously visited stores now receive order confirmations, shipping updates, and delivery notifications for every purchase. Healthcare patients who previously were reminded by phone call now receive appointment confirmations and medication reminders by SMS. Each of these digital migration events converts a non-messaging interaction into a recurring A2P message that sustains enterprise messaging volume growth independently of expanding consumer populations.

Two-factor authentication messaging represents the most structurally resilient and fastest-growing component of A2P SMS volume. As cybersecurity threats, regulatory requirements, and consumer security awareness collectively make OTP authentication the standard for high-value digital transactions, the number of authentication messages generated per digital platform user per day is growing. A bank customer who logs into mobile banking, initiates a transfer, and adds a new payee generates three OTP messages in a single session. An e-commerce customer creating an account, logging in, and completing a purchase generates multiple authentication touchpoints.

Restraints: Rising SMS spam and fraudulent messaging, growing adoption of OTT messaging apps, and complex international compliance requirements are restraining premium messaging market growth.

Spam and fraudulent messaging delivered through premium messaging infrastructure is the most commercially damaging challenge facing the legitimate enterprise messaging market. Consumers who receive spam, phishing, or smishing messages over SMS associate the negative experience with the entire SMS channel rather than distinguishing between compliant enterprise messaging and fraudulent actor abuse. This trust degradation reduces consumer responsiveness to legitimate enterprise SMS communications, lowering engagement rates and reducing the commercial return on investment that justifies enterprise messaging budget. Regulatory responses including the U.S. 10DLC registry, India's distributed ledger technology solution, and UK network-level filtering are each addressing this challenge through different technical and regulatory mechanisms.

Over-the-top messaging applications including WhatsApp, iMessage, and Line have captured a significant share of enterprise-to-consumer communication in markets where these platforms have achieved near-universal consumer adoption. WhatsApp Business API has become the primary enterprise customer communication channel in India, Brazil, and several European markets, providing richer messaging capabilities than SMS at lower per-message costs for conversations initiated by the consumer. In markets where WhatsApp penetration is very high, enterprises face the commercial decision of whether to maintain parallel SMS infrastructure for consumers not using WhatsApp or to migrate fully to OTT channels and accept reduced reach to the non-WhatsApp subscriber segment.

Opportunities: Expanding Rich Communication Services deployment, conversational AI integration, and rising digital banking messaging demand in emerging markets are creating strong growth opportunities in the premium messaging market.

The Rich Communication Services are the most commercial breakthrough in the high-end messaging market. The move by Apple in 2024 to introduce its support for RCS marked the completion of cross-platform integration, which is needed to make the RCS commercially viable as an enterprise messaging service for the mass market for the first time. RCS lets enterprises send brand messaging with their logos and color palette, interaction buttons, images in carousel format for viewing products, and location information to guide users to their stores—all using native messaging applications without the need for consumers to download dedicated applications. These features provide the rich user experience that the OTT messaging applications provide inside their own walled gardens but through the universal messaging system that can reach every smartphone user.

Conversational AI integration with enterprise messaging platforms is enabling a transition from one-way notification messaging toward intelligent two-way dialogue that resolves customer queries, processes transactions, and provides personalized service without human agent involvement. AI chatbots operating through SMS and RCS channels can handle account balance enquiries, appointment rescheduling, order status updates, and product recommendations through natural language conversation that feels responsive and helpful to consumers. Each enterprise function that conversational AI can handle through messaging channels reduces call centre volume while increasing the message throughput that generates premium messaging revenue, creating aligned commercial incentives for enterprise messaging platform investment.

Recent Developments:

-

March 2026: SNS Insider published its comprehensive premium messaging market report confirming the market's USD 80.20 billion valuation in 2025 and its trajectory toward USD 146.08 billion by 2035 at a CAGR of 6.18%, with A2P SMS maintaining dominance and Asia Pacific emerging as the fastest-growing region.

-

2025: Twilio announced expansion of its Messaging Services platform with native RCS support, enabling enterprises to manage SMS, MMS, and RCS campaigns through a unified API that automatically upgrades messages to the richest format supported by each recipient's device and carrier.

-

2025: Sinch completed the integration of its MessageMedia acquisition and expanded its CPaaS platform capabilities across North America, Europe, and Asia Pacific, strengthening its position as one of the largest global A2P messaging aggregators by volume and geographic reach.

Premium Messaging Market Key Players are:

-

Twilio Inc.

-

Sinch AB

-

Bandwidth Inc.

-

Vonage America LLC (Ericsson)

-

Infobip Ltd.

-

Kaleyra Inc.

-

Route Mobile Ltd.

-

Comviva Technologies Ltd.

-

AT&T Inc.

-

Vodafone Group plc

-

NTT DOCOMO Inc.

-

China Unicom

-

Orange Business Services

-

Deutsche Telekom AG

-

KDDI Corporation

-

MessageBird (Bird)

-

Clickatell Pty Ltd.

-

tyntec GmbH

-

CLX Communications

-

Mitto AG

Premium Messaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 80.20 Billion |

| Market Size by 2035 | USD 146.08 Billion |

| CAGR | CAGR of 6.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (A2P SMS, A2P MMS, P2A SMS, P2A MMS) •By Application (BFSI, Retail, Entertainment & Media, Hospitality, Outsourcing, Others) •By Enterprise Size (Large Enterprises, Small & Medium Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Twilio Inc., Sinch AB, Bandwidth Inc., Vonage America LLC (Ericsson), Infobip Ltd., Kaleyra Inc., Route Mobile Ltd., Comviva Technologies Ltd., AT&T Inc., Vodafone Group plc, NTT DOCOMO Inc., China Unicom, Orange Business Services, Deutsche Telekom AG, KDDI Corporation, MessageBird (Bird), Clickatell Pty Ltd., tyntec GmbH, CLX Communications, Mitto AG. |

Frequently Asked Questions

North America dominated the Premium Messaging Market in 2025.

A2P SMS dominated with approximately 38.60% of revenues in 2025.

Expanding enterprise digital communication adoption and soaring two-factor authentication messaging volume are the primary drivers. Rich Communication Services commercial deployment is creating a new premium tier messaging revenue category above the established A2P SMS baseline.

The Premium Messaging Market was valued at USD 80.20 Billion in 2025.

The Premium Messaging Market is expected to grow at a CAGR of 6.18% from 2026 to 2035.

The Premium Messaging Market is expected to grow at a CAGR of 6.18% from 2026 to 2035.

Get in Touch