Preparative and Process Chromatography Market Report Scope & Overview:

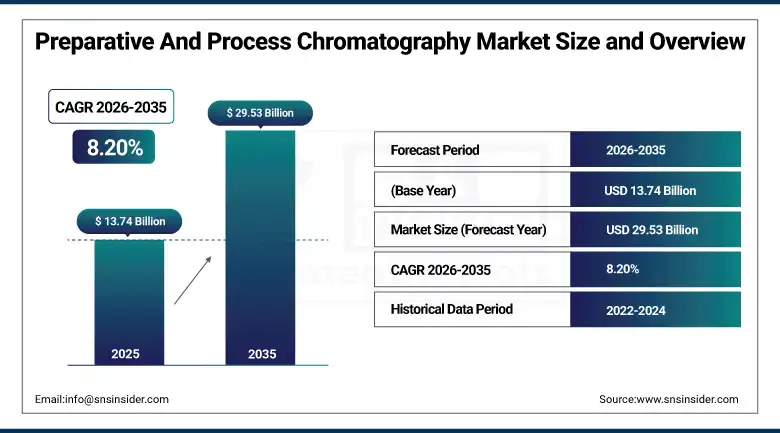

The Preparative and Process Chromatography Market was valued at USD 13.74 Billion in 2025 and is expected to reach USD 29.53 Billion by 2035, growing at a CAGR of 8.20% from 2026 to 2035.

The global preparative and process chromatography market is experiencing robust growth. The market is embedded deeply in pharmaceutical and biotechnology workflows for drug purification, biomolecule separation, and regulatory-compliant manufacturing, with biologics accounting for more than 40% of new drug approvals, which drives sustained procurement of process-scale chromatography systems and consumables. Rising investments in research and development, coupled with strict quality standards from the FDA and EMA, have reinforced the role of preparative and process chromatography as a critical downstream processing technology. Technological advancements including continuous chromatography, single-use systems, and AI-driven analytics are enhancing throughput while reducing operational costs, enabling manufacturers to optimise production timelines and improve reproducibility across GMP-regulated biomanufacturing environments.

In September 2024, Gilson launched the VERITY Preparative LC system, a high-performance purification platform with integrated software designed to support contract research organisations and biotech R&D scientists in synthetic drug discovery, including peptide and oligonucleotide synthesis. The platform addresses the growing demand from CROs and biotech R&D teams for scalable, automated preparative liquid chromatography solutions that integrate seamlessly with digital data management workflows and deliver reproducible purification performance across iterative drug candidate screening campaigns.

Market Size and Forecast

-

Market Size in 2026E: USD 14.87 Billion

-

Market Size by 2035: USD 29.53 Billion

-

CAGR: 8.20% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Preparative And Process Chromatography Market - Request Free Sample Report

Preparative and Process Chromatography Market Trends

-

Continuous chromatography adoption is improving resin utilization, reducing buffer consumption, and enhancing biopharmaceutical manufacturing efficiency.

-

Single-use chromatography systems are gaining popularity due to flexibility, rapid changeovers, and reduced contamination risks.

-

AI-driven process development is accelerating chromatography method optimization and reducing experimental workload during development.

-

Biosimilar monoclonal antibody production growth is increasing demand for Protein-A affinity chromatography resins.

-

Cell and gene therapy expansion is driving demand for specialized chromatography purification technologies and materials.

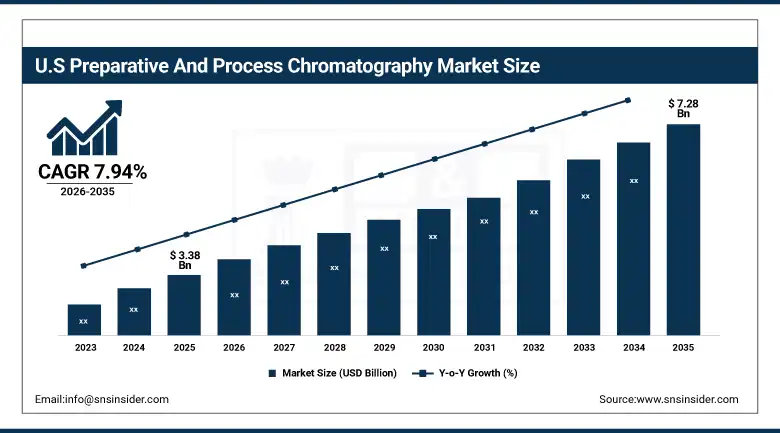

The U.S. Preparative and Process Chromatography Market Outlook

The U.S. Preparative and Process Chromatography Market was valued at approximately USD 3.38 Billion in 2025 and is expected to reach approximately USD 7.28 Billion by 2035, growing at a CAGR of approximately 7.94%.

The U.S. is the world's most commercially significant preparative and process chromatography market within North America's dominant 34.55% regional revenue position. Thermo Fisher Scientific, Cytiva (Danaher), Merck KGaA's MilliporeSigma division, Bio-Rad Laboratories, Waters Corporation, and Agilent Technologies collectively define the domestic commercial landscape. The extraordinary concentration of biopharmaceutical manufacturing in the U.S., over 5,000 pharmaceutical companies and the world's most advanced biologics production infrastructure, creates the most commercially intensive preparative and process chromatography procurement environment globally. Higher R&D activity, favourable FDA regulatory frameworks, extensive manufacturing capacity, and biopharmaceutical companies' analytical instrument investments collectively sustain above-average market growth throughout the forecast period.

In April 2023, Thermo Fisher Scientific acquired MarqMetrix, adding Raman-based inline process analytical technology to its chromatography portfolio, enabling real-time monitoring and control of chromatographic separation processes within GMP manufacturing environments. The acquisition demonstrates the commercial direction of process chromatography technology toward integrated real-time quality monitoring that supports continuous manufacturing programmes and regulatory compliance with FDA and EMA process analytical technology guidance.

Preparative and Process Chromatography Market Segment Analysis

-

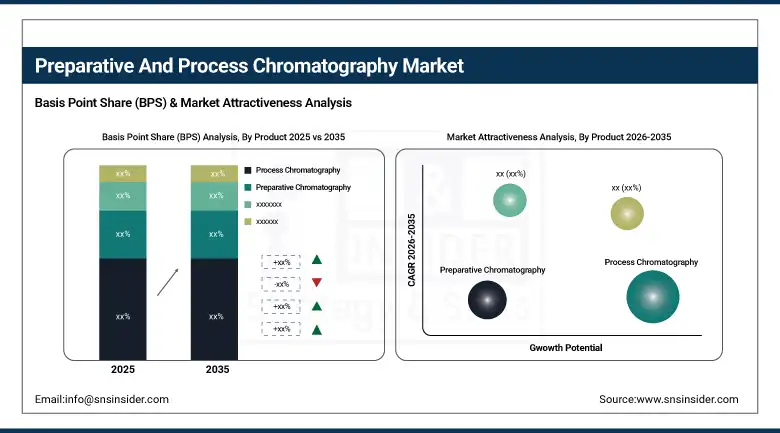

By Product, the process chromatography segment dominated the market with approximately 68.46% share in 2025, while the preparative chromatography segment is the fastest growing at 8.53% CAGR.

-

By Chromatography Type, the liquid chromatography segment dominated the market with approximately 31.20% share in 2025, while the affinity chromatography sub-segment is the fastest growing.

-

By Application, monoclonal antibodies & recombinant proteins dominated the market with approximately 39.3% share in 2025, while cell & gene therapies segment is the fastest growing.

-

By End User, the biopharmaceutical industry segment dominated the market with approximately 43.56% share in 2025, while the contract research organisations segment is the fastest growing.

By Product, process chromatography dominates, preparative grows fastest

Process chromatography retained the dominant product position in 2025. The commercial primacy of process chromatography reflects its role as the essential downstream processing step in all biopharmaceutical manufacturing programmes whose commercial-scale antibody, vaccine, and recombinant protein production requires GMP-validated purification systems whose performance directly determines final drug substance quality, regulatory compliance, and commercial yield economics. Each new biologic drug approval creates a commercial manufacturing programme requiring process chromatography system installation, resin procurement, and ongoing consumable supply whose aggregate across the global biologics production base sustains the segment's dominant revenue position.

Preparative chromatography is the fastest growing product segment because the expansion of drug discovery programmes, the growth of peptide and oligonucleotide therapeutics whose synthetic production requires medium-scale preparative purification, and the development of personalized medicine approaches that require flexible small-batch purification capabilities collectively create above-average demand growth. Each pharmaceutical company and CRO that expands its drug candidate screening operation creates preparative chromatography procurement whose commercial value grows with the breadth of therapeutic modalities under development.

By Chromatography Type, liquid chromatography dominates, affinity grows fastest

Liquid chromatography retained the dominant type position in 2025. Liquid chromatography's commercial primacy reflects its universality across biopharmaceutical applications, encompassing ion exchange chromatography for charge-based protein separation, size exclusion chromatography for molecular weight-based polishing, hydrophobic interaction chromatography for aggregation removal, and reversed-phase HPLC for small molecule and peptide purification. Each biopharmaceutical purification process that employs a multi-step column chromatography train creates liquid chromatography procurement across multiple technique types whose aggregate per manufacturing programme creates above-average per-customer commercial value.

Affinity chromatography is the fastest growing sub-segment because the monoclonal antibody and biosimilar production wave's universal adoption of Protein-A affinity capture as the first downstream purification step creates resin procurement that grows proportionally with antibody production volume. Each new biosimilar programme entering commercial production and each novel antibody therapeutic scaling from clinical to commercial manufacturing creates Protein A resin procurement whose cumulative commercial impact compounds with the extraordinary expansion of the global antibody therapeutics pipeline.

By End User, biopharmaceutical industry dominates, CROs grow fastest

The biopharmaceutical industry retained the dominant end-user position in 2025. Biopharmaceutical companies’ combination of large-scale manufacturing programmes, stringent GMP quality requirements, extensive downstream processing infrastructure, and growing pipeline of biologics, biosimilars, and advanced therapy medicinal products creates the most commercially concentrated and highest-quality-specification preparative and process chromatography procurement of any end-user category. Each commercial biologic drug whose annual sales volume requires hundreds of batches of manufacturing creates ongoing resin replacement, buffer procurement, and system maintenance investment whose cumulative commercial value substantially exceeds development-stage equivalent procurement.

Contract research organisations are the fastest growing end user because the progressive pharmaceutical industry outsourcing of drug discovery, process development, and clinical manufacturing activities is creating CRO investment in chromatography infrastructure that serves multiple client programmes simultaneously. Each CRO that expands its purification capability to address client demand for scalable, high-purity preparative chromatography creates system and consumable procurement whose commercial aggregate grows with the CRO sector's capacity expansion. The Asia Pacific CRO market's rapid growth, driven by cost-competitive service delivery in China, India, and South Korea, creates particularly dynamic chromatography procurement as regional CROs invest in Western-standard preparative and process chromatography infrastructure to serve global pharmaceutical client programmes.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

28.4% |

|

Latin America |

Brazil |

44.2% |

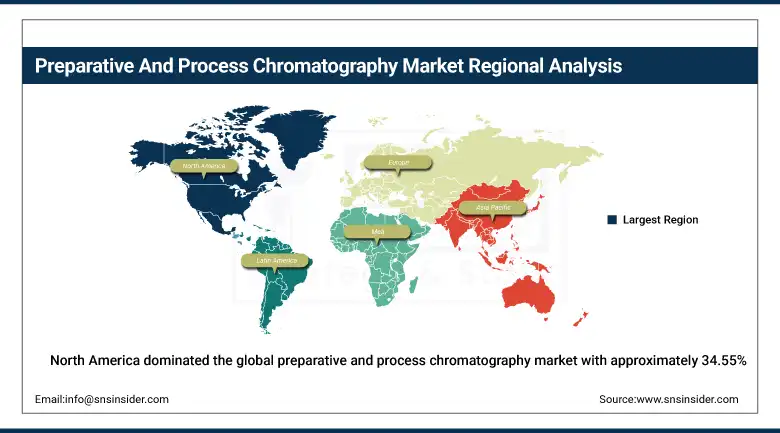

North America Preparative and Process Chromatography Market Insights

North America dominated the global preparative and process chromatography market with approximately 34.55% of revenues in 2025, supported by a strong biopharmaceutical ecosystem, advanced regulatory frameworks, high R&D investments, and the commercial concentration of leading chromatography system and consumable suppliers. The United States accounts for approximately 87.4% of North American revenues through Thermo Fisher Scientific, Cytiva, MilliporeSigma, Bio-Rad, Waters, and Agilent's enterprise procurement relationships across domestic biopharmaceutical manufacturing and research institutions.

Canada contributes approximately 12.6% of North American revenues through its biopharmaceutical manufacturing sector's downstream processing investment, the academic research institution network's chromatography procurement, and the contract manufacturing sector's purification infrastructure serving global biologics clients.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Preparative and Process Chromatography Market Insights

Europe is a technically sophisticated preparative and process chromatography market where Airbus’s scale in manufacturing has an analogue in bioprocessing: Cytiva's Swedish headquarters, Sartorius AG's German operations, and Merck KGaA's German base collectively make Europe the global center of process chromatography technology development and manufacturing. Germany accounts for approximately 22.3% of European revenues through its pharmaceutical industry's downstream processing investment, Merck KGaA and Sartorius’ domestic operations, and the extensive GMP biomanufacturing site network in the Rhine-Main and Bavaria regions.

Switzerland, the United Kingdom, and France are significant secondary markets where Novartis and Roche's Swiss biomanufacturing operations, AstraZeneca's UK biologics production, and Sanofi's French manufacturing infrastructure create consistent above-average preparative and process chromatography procurement.

Asia Pacific Preparative and Process Chromatography Market Insights

Asia Pacific is the fastest growing regional preparative and process chromatography market at 9.03% CAGR, driven by expanding pharmaceutical manufacturing in China, India, Japan, and South Korea, increasing government support for life sciences research, and the rapid growth of the regional CRO and contract manufacturing organization sector whose infrastructure investment creates above-average system and consumable procurement. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary biopharmaceutical capacity expansion, the government's biologics development programme, and the domestic CRO sector's purification infrastructure investment.

India represents the most commercially dynamic emerging market within Asia Pacific where the government's PRIP biopharmaceutical research fund, the biosimilar manufacturing sector's downstream processing investment, and the expanding CRO industry collectively create above-average first-time and upgrade preparative chromatography procurement from both domestic and export-oriented manufacturing operations.

MEA & Latin America Preparative and Process Chromatography Market Insights

Israel leads MEA revenues through its advanced biopharmaceutical research sector, Teva Pharmaceutical's biologics development investment, and the academic research institution network's preparative chromatography procurement across multiple universities and research institutes. Saudi Arabia's Vision 2030 pharmaceutical manufacturing initiative and the UAE's growing biotech sector add complementary Gulf demand.

Brazil leads Latin American revenues through its biopharmaceutical manufacturing sector, the expanding CRO industry, and the academic research network's downstream processing investment. Mexico's pharmaceutical manufacturing and Argentina's biopharmaceutical research collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Biopharmaceutical pipeline expansion and biosimilar manufacturing investment

The extraordinary expansion of the global biologics pipeline is the preparative and process chromatography market's most commercially certain structural growth driver. Biologics accounting for more than 40% of new drug approvals creates systematic new manufacturing programme establishment whose downstream processing infrastructure requires process chromatography system installation, resin procurement, and column and buffer consumable supply. Each new biologic drug transitioning from clinical to commercial manufacturing creates a process chromatography procurement event whose commercial value ranges from tens of millions to hundreds of millions of dollars in system and resin investment across the commercial manufacturing lifecycle.

Biosimilar manufacturing investment is simultaneously creating above-average process chromatography procurement as biosimilar manufacturers replicate innovator biologic purification processes whose validated downstream processing architecture requires equivalent chromatography infrastructure. The global biosimilar market's extraordinary expansion, driven by patent expiration of major biologics, creates proportional process chromatography demand whose aggregate grows with biosimilar production volume.

Restraints: High equipment and resin costs limiting adoption among smaller manufacturers and column regeneration complexity

High equipment and resin costs create adoption barriers for smaller biopharmaceutical manufacturers, academic groups scaling research discoveries, and emerging economy contract manufacturers whose capital budget constraints require extended amortization periods for process chromatography infrastructure investment. Affinity chromatography resins representing up to 50% of total downstream processing costs create economic pressure in cost-sensitive biosimilar manufacturing programmes whose price competition erodes the commercial margin available for premium resin specification.

Column regeneration complexity and resin lifetime management create operational challenges that require specialized process development expertise to optimize resin cleaning-in-place protocols, sanitization procedures, and lifetime cycle determination. Each process change that requires column regeneration revalidation under GMP requirements creates regulatory burden that moderates the pace of process optimization beyond initial commercial launch.

Opportunities: Continuous chromatography commercialization and cell and gene therapy purification development

Continuous chromatography commercialization represents the most commercially transformative near-term opportunity whose multi-column countercurrent operation improves resin utilization by 80 to 90 percent compared to batch-mode operation, reducing per-gram-of-product purification cost substantially. Each manufacturing programme that adopts continuous chromatography creates equipment procurement for multi-column systems whose capital cost exceeds batch alternatives while delivering operating cost advantages that sustain the investment over the production lifecycle.

Cell and gene therapy purification development represents the most commercially premium emerging opportunity whose viral vector, plasmid DNA, and mRNA purification requirements create new chromatography technology development that extends the market beyond conventional biopharmaceutical application boundaries. Each approved gene therapy and mRNA vaccine programme creates manufacturing infrastructure procurement whose per-dose commercial value and production complexity sustain premium chromatography system specification.

Recent Developments:

-

2025: Sartorius AG expanded its chromatography portfolio with advanced purification technologies designed to improve productivity in biologics and cell therapy manufacturing.

-

2025: Repligen Corporation launched enhanced chromatography solutions supporting high-throughput downstream bioprocessing and intensified biopharmaceutical production workflows.

-

2025: Waters Corporation introduced new preparative chromatography innovations focused on improving separation efficiency and purification scalability for pharmaceutical applications.

-

2025: Merck KGaA strengthened its bioprocessing capabilities through expanded chromatography resin offerings targeting monoclonal antibody and advanced therapy manufacturing.

Preparative and Process Chromatography Market Key Players are:

-

Thermo Fisher Scientific Inc.

-

Danaher Corporation

-

Merck KGaA

-

Sartorius AG

-

Bio-Rad Laboratories Inc.

-

Waters Corporation

-

Agilent Technologies Inc.

-

Shimadzu Corporation

-

Tosoh Bioscience LLC

-

Novasep Holding SAS

-

Gilson Inc.

-

KNAUER Wissenschaftliche Geräte GmbH

-

Repligen Corporation

-

3M Company

-

YMC Co., Ltd.

-

Restek Corporation

-

ChromaCon AG

-

GEA Group AG

-

Sepax Technologies, Inc.

-

Mitsubishi Chemical Group

Preparative and Process Chromatography Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.74 Billion |

| Market Size by 2035 | USD 29.53 Billion |

| CAGR | CAGR of 8.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Process Chromatography, Preparative Chromatography, Others) • By Chromatography Type (Liquid Chromatography, Gas Chromatography, Others) • By Application (Monoclonal Antibodies & Recombinant Proteins, Vaccines, Peptides & Oligonucleotides, Cell & Gene Therapies, Others) • By End User (Biopharmaceutical Industry, Contract Research Organizations, Academic and Research Institutions, Food and Nutraceutical Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, Sartorius AG, Bio-Rad Laboratories Inc., Waters Corporation, Agilent Technologies Inc., Shimadzu Corporation, Tosoh Bioscience LLC, Novasep Holding SAS, Gilson Inc., KNAUER Wissenschaftliche Geräte GmbH, Repligen Corporation, 3M Company, YMC Co., Ltd., Restek Corporation, ChromaCon AG, GEA Group AG, Sepax Technologies, Inc., Mitsubishi Chemical Group |

Frequently Asked Questions

The Preparative and Process Chromatography Market is expected to grow at a CAGR of 8.20% from 2026 to 2035.

Biopharmaceutical pipeline expansion with biologics accounting for more than 40% of new drug approvals creating systematic new manufacturing programme establishment.

The Preparative and Process Chromatography Market was valued at USD 13.74 Billion in 2025.

Process Chromatography dominated the market in 2025.

North America dominated the market share in 2025.

Get in Touch