Primary Health Care Service Market Report Scope & Overview:

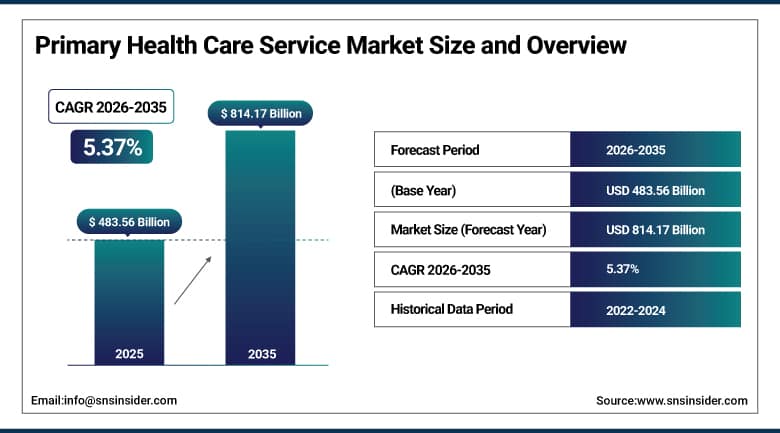

The Primary Health Care Service Market was valued at USD 483.56 billion in 2025 and is expected to reach USD 814.17 billion by 2035, growing at a CAGR of 5.37% from 2026–2035.

The Primary Health Care Service Market is witnessing steady growth in the global market owing to the increasing demand for accessible healthcare delivery, early disease detection, and preventive care services. The rising prevalence of chronic conditions and aging population is promoting the usage of primary consultations, outpatient services, and long-term disease management across healthcare systems. Investments made by governments and private organizations in healthcare infrastructure expansion, digital health technologies, and community-based care are contributing to market growth. Increasing developments in telemedicine, AI-driven diagnostics, and wearable health solutions are playing a major role in driving the demand for Primary Health Care Service Market. Growth in healthcare spending and emphasis on cost-effective treatment models are fueling the demand for market.

According to World Health Organization & Global Health Observatory 2025, primary healthcare services' coverage is inconsistent, as only around 70% of countries provide integration of primary care models within their national health policies. Furthermore, according to the WHO UHC service coverage index, on average, the world-wide coverage reaches 68%. Preventable deaths of mothers have been decreased by 38% since 2000 due to better access to primary care.

Moreover, WHO digital primary care statistics demonstrate that over 55% of countries include community health worker programs in their national PHC frameworks.

Market Size and Forecast:

-

Market Size 2026E: USD 508.55 billion

-

Market Size 2035: USD 814.17 billion

-

CAGR (2026 - 2035): 5.37%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Primary Health Care Service Market - Request Free Sample Report

Primary Health Care Service Market Trends:

-

Rapid expansion of telehealth platforms is transforming Primary Health Care Service Market by enabling remote consultations and improved healthcare accessibility globally.

-

Increasing adoption of AI based diagnostic tools is enhancing clinical decision making, improving accuracy and efficiency in primary healthcare delivery systems.

-

Growing integration of electronic health records is improving patient data management, care coordination, and continuity of treatment across healthcare providers.

-

Rising demand for virtual care services is reducing hospital visits, increasing convenience, and supporting faster healthcare service delivery models globally.

-

Government investments in digital health infrastructure are accelerating adoption of telemedicine platforms and strengthening primary care accessibility in rural areas.

-

Expansion of mobile health applications is enabling real time monitoring, personalized care, and improved patient engagement in primary healthcare systems.

U.S. Primary Health Care Service Market Size Outlook:

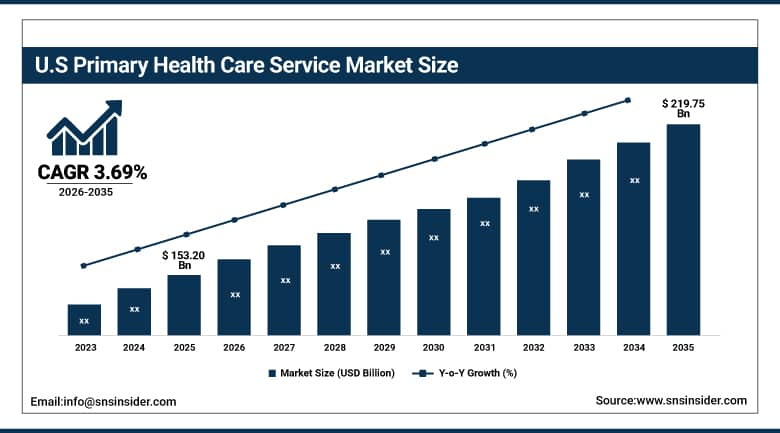

The U.S. Primary Health Care Service Market was valued at USD 153.20 billion in 2025 and is expected to reach around USD 219.75 billion by 2035, growing at a CAGR of 3.69% from 2026–2035.

The U.S. Primary Health Care Service Market is growing consistently owing to increased demand for accessible primary care services, preventive healthcare, and chronic disease management. The usage of primary healthcare services in hospitals, clinics, and outpatient departments has contributed to market growth in a consistent manner. Increased spending in healthcare modernization and digital health adoption has generated an increase in demand for virtual consultations and coordinated care services. Development of telehealth platforms, AI-based diagnostics, and community health programs is further driving the demand for this market.

According to the U.S. Centers for Disease Control and Prevention and the Health Resources and Services Administration 2025 primary care workforce reports, approximately 66% of U.S. adults had at least one primary care visit in the past year, while over 1,400 federally qualified health centers deliver care to more than 31 million patients annually.

As per CDC National Ambulatory Medical Care 2025, primary care accounts for nearly 55% of all outpatient visits, and electronic health record adoption among primary care providers remains above 95%, supporting standardized care delivery and chronic disease management across the U.S. healthcare system.

Primary Health Care Service Market Segment Analysis:

-

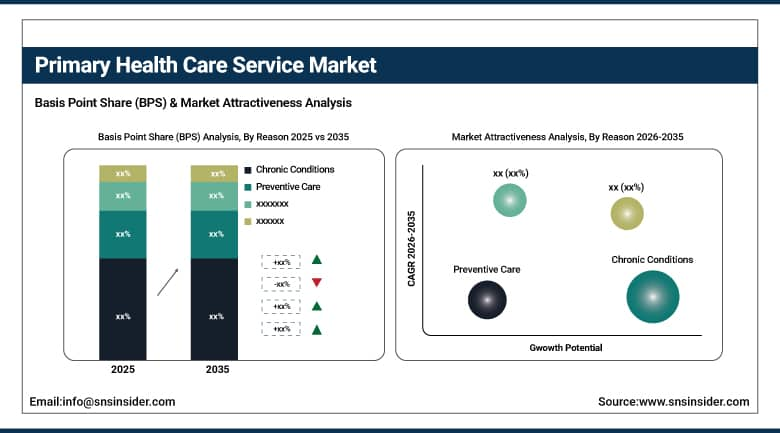

By Reason, chronic conditions dominated the market with 41.60% share in 2025; while preventive care is the fastest growing segment with CAGR of 8.58% during 2026 to 2035

-

By Age Group, adults dominated the market with 52.30% share in 2025; while geriatrics are the fastest growing segment with CAGR of 8.13% during 2026 to 2035.

-

By Mode of Consultation, physical care dominated the market with 67.55% share in 2025; while virtual care is the fastest growing segment with CAGR of 9.78% during 2026 to 2035.

-

By Provider, hospitals dominated the market with 44.80% share in 2025; while clinics are the fastest growing segment with CAGR of 8.63% during 2026 to 2035.

By Reason, chronic conditions dominated the Primary Health Care Service Market, while preventive care is the fastest growing segment.

The chronic conditions segment has been leading the market with the dominated share of revenue in 2025. The reason behind its leadership is the increased occurrence of chronic diseases like diabetes, heart diseases, and other respiratory illnesses in people around the world. There has been an increase in demand for the continuous tracking, treatment, and management of chronic diseases because of their increased presence.

The preventive care segment is anticipated to grow at a fastest CAGR from 2026 to 2035. This rapid growth will be mainly due to growing patient awareness about early disease diagnosis and healthcare through a wellness approach. Increased adoption of screenings, vaccinations, and health checkups is further contributing to the growth of the market. Healthcare companies and governments have started focusing more on preventive care to avoid future costs associated with chronic care.

By Age Group, adults dominated the Primary Health Care Service Market, while geriatrics are the fastest growing segment.

Adults' segment held the dominated share in the revenue generation within the Primary Health Care Services Market in 2025. The growing rate can be attributed to higher incidence of chronic ailments, lifestyle-based diseases, and usage of health services. Adults constitute the economic group that generates high income. Frequent visits to healthcare service providers for consultations, preventive healthcare services, and treatments make adults consume more money and utilize primary healthcare services.

Geriatrics segment will register the fastest CAGR during the forecast period from 2026-2035. Growth of the segment is due to the growing trend of aging populations, which increases life expectancy rates. Older adults need constant monitoring for a number of illnesses, which makes them visit healthcare professionals. Higher prevalence of diseases associated with aging like heart disease, diabetes, and arthritis is adding to the demand for healthcare services among this segment.

By Mode of Consultation, physical care dominated the Primary Health Care Service Market, while virtual care is the fastest growing segment.

The physical care segment held the dominated revenue share in the Primary Health Care Service Market in 2025. It was the leader due to the high level of dependency on physical meetings at hospitals, clinics, and outpatient departments. The existing structure of the healthcare industry and patients' preferences for physical check-ups contributed significantly to its dominant status. The presence of specialists and diagnostic facilities makes its use highly effective. It continues to be the most common method of disease identification and therapy provision.

The virtual care segment is projected to have the fastest CAGR between 2026 and 2035. Such rapid development can be explained by the increasing popularity of telemedicine applications and digital healthcare services. Improved access to the internet and increased numbers of smartphones positively impact the development of remote consultations. Affordable prices and decreased hospital visits contribute to higher demand. The application of wearable devices and artificial intelligence also stimulates such developments.

By Provider, hospitals dominated the Primary Health Care Service Market, while clinics are the fastest growing segment.

Hospitals held the dominated market share in the Primary Health Care Service Market in 2025 because of their robust infrastructure and multi-specialty healthcare service availability. Hospitals serve as the first touchpoint in case of complicated emergencies related to primary healthcare requirements. These institutions combine all diagnosis, treatments, and referrals at one place. A large number of patients, advanced facilities, and improved financial cover add to the prominence of hospitals in primary healthcare services.

Clinics are projected to show the fastest CAGR from 2026-2035 because of the preference for affordable and accessible healthcare services. Clinics have shorter waiting times and provide localized healthcare service. Growing demand for outpatient and preventive care services is leading to a rise in adoption of clinics. Growth in the number of small private clinics along with digital health adoption has further fueled the growth of this segment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

82.40% |

|

Europe |

Germany |

27.30% |

|

Asia Pacific |

China |

39.20% |

|

Middle East & Africa |

UAE |

17.40% |

|

Latin America |

Brazil |

46.80% |

North America Primary Health Care Service Market Insights.

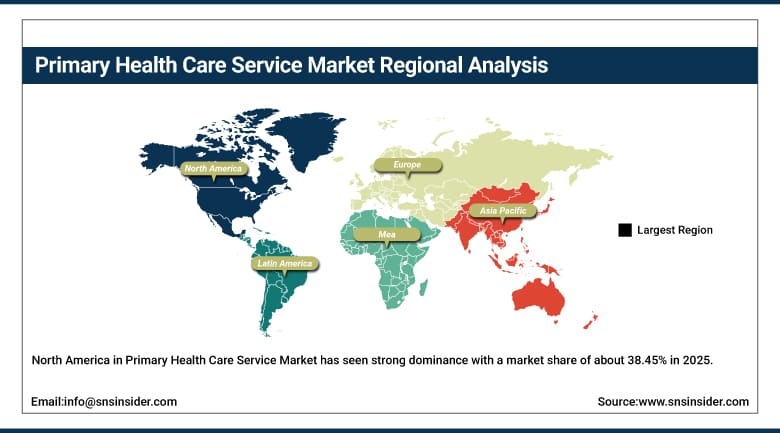

North America in Primary Health Care Service Market has seen strong dominance with a market share of about 38.45% in 2025 due to advanced healthcare infrastructure and high primary care utilization. The region benefits from strong demand in preventive care, chronic disease management, and outpatient services. Increasing demand for early diagnosis, coordinated care models, and value-based healthcare systems is driving market expansion across the United States and Canada. Rising adoption in telehealth and digital health platforms is further supporting market leadership. Strong healthcare investments are strengthening service delivery capabilities.

According to the U.S. Centers for Disease Control and Prevention 2025 National Ambulatory Medical Care Survey and Statistics Canada health system indicators, over 80% of adults in North America have at least one annual primary care visit, with approximately 88% of U.S. adults having a usual source of primary care.

As per OECD Health Statistics 2025, Canada maintains over 85% coverage of publicly funded primary care access, while telehealth integration in primary care exceeds 60% of providers across North America, reflecting strong system-wide adoption of hybrid care delivery models and preventive healthcare utilization.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Primary Health Care Service Market Insights.

The Europe Primary Health Care Service Market shows strong presence in 2025 due to universal healthcare systems and structured primary care networks. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on aging population care, preventive health programs, and chronic disease management is supporting steady market growth across the region. Increasing adoption in community healthcare, general practitioner services, and digital health consultations is further strengthening service consumption. Expanding public healthcare frameworks are driving accessible primary care delivery.

According to the World Health Organization European Region Primary Health Care Monitoring 2025, more than 85% of European countries have integrated primary care services into universal health coverage frameworks, ensuring access to essential health services. As per OECD Health at a Glance Europe 2025 indicators, approximately 75% of patient contacts in EU member states occur in primary care settings, while over 90% of general practitioners use electronic health records.

Asia Pacific Primary Health Care Service Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the Primary Health Care Service Market during the forecast period with a market share of about 7.16% in 2025. Rapid healthcare infrastructure expansion and increasing primary care accessibility are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Expanding population base, rising chronic disease burden, and growing awareness of preventive healthcare are significantly boosting adoption. Rising demand for affordable healthcare services and government initiatives is further accelerating market growth across the region. Large scale healthcare investments support strong regional demand outlook.

According to the World Health Organization & Primary Health Care Performance Initiative and 2025 Global Health Observatory, Asia Pacific countries account for more than 60% of the world’s population, with average life expectancy in the region reaching approximately 76 years. As per WHO UHC Service Coverage Index 2025, coverage in several high-income Asia Pacific economies exceeds 80, while many lower-income countries in the region remain below 60.

Middle East & Africa and Latin America Primary Health Care Service Market Insights.

The Middle East & Africa and Latin America region is witnessing steady growth due to rising healthcare infrastructure development and primary care modernization. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are emerging as key demand centers. Increasing investments in clinics, community health centers, and outpatient services are supporting market expansion. Growing need for preventive care, maternal health services, and chronic disease management is further boosting service adoption. Rising healthcare access and government initiatives strengthen long term demand outlook across both regions.

According to the World Health Organization Primary Health Care Monitoring Framework and World Bank Health Nutrition and Population 2025, primary health care coverage remains uneven across regions, with Latin America achieving over 80% average coverage of essential health services index, while Sub-Saharan Africa remains below 50% in several indicators.

As per WHO Global Health Observatory 2025, over 70% of countries in the Middle East and Africa have adopted national PHC strengthening strategies, while Latin America reports more than 85% population access to at least one primary care facility within 5 km in urban areas, highlighting expanding service penetration and infrastructure development.

Market Dynamics:

Growth Drivers: Expansion of digital health technologies and increasing adoption of telemedicine and virtual care platforms

The fast adoption of telemedicine, digital health platform, and artificial intelligence-based healthcare solutions is revolutionizing the delivery of Primary Health Care Services Market services. Patients are opting more for virtual consultations owing to their convenience and time savings. Healthcare institutions are adopting electronic health records and remote patient monitoring technologies in order to improve patient management and coordination. Moreover, government initiatives for establishing infrastructure for digital healthcare are supporting this trend. Technological evolution is positively impacting access to primary care services in both rural and urban settings around the world.

According to the World Health Organization Global Telemedicine Observatory and OECD Health at a Glance 2025, over 75% of countries globally have implemented national telehealth or digital primary care frameworks, with more than 60% integrating virtual care services into primary healthcare delivery systems. As per WHO digital health maturity assessments, around 70% of primary care facilities in high-income countries now support remote consultations or hybrid care models.

Restraints: Limited healthcare infrastructure and shortage of primary care professionals in developing and underserved regions

Limited healthcare infrastructure and insufficient numbers of qualified general practitioners hinder the development of Primary Health Care Service Market. Most underdeveloped countries experience a lack of accessibility to basic health centers, and their uneven placement. Healthcare overload affects the quality of services and prolongs waiting lines. Rural communities suffer from the inability to have quick access to general practices. The absence of financial resources for the development of healthcare infrastructure and training of qualified specialists prevents further expansion of the service.

Opportunities: Rapid growth of telehealth services and integration of AI based healthcare solutions in primary care systems

With growing penetration of tele-health services and Artificial Intelligence powered health-care services, many opportunities are being created for Primary Health Care Services Market. The use of remote consulting, diagnostics, and AI enabled decision making processes will increase the effectiveness and efficiency of primary health-care services. Smart health-care solutions and predictive analysis have been adopted by healthcare players in order to improve the performance of patients. Growth in the number of mobile applications for health-care purposes will provide another boost to the growth of the primary health-care industry.

According to the World Health Organization Global Health Observatory 2025 and OECD digital health indicators, over 70% of countries have integrated telehealth services into national primary healthcare systems, with more than 60% reporting routine virtual consultations in primary care delivery.

As per WHO 2025 digital health adoption, AI-based clinical decision support tools are implemented in approximately 45% of primary care systems globally.

Recent Developments:

-

2026: Cigna Group improved operating performance through disciplined pricing, utilization management, and enhanced AI-enabled claims and care optimization programs across payer services.

-

2025: CVS Health strengthened primary care integration through HealthHUB expansion and digital health services across community pharmacy network.

-

2025: Apollo Hospitals Enterprise advanced digital healthcare services including telemedicine expansion, AI diagnostics and hospital network capacity enhancement across India.

-

2024: Humana Inc. expanded Medicare Advantage offerings while investing in digital care coordination tools to support chronic disease management and member engagement programs.

Primary Health Care Service Market Key Players are:

-

UnitedHealth Group

-

CVS Health

-

Cigna Group

-

Humana Inc.

-

Elevance Health

-

Centene Corporation

-

Kaiser Permanente

-

HCA Healthcare

-

Tenet Healthcare

-

CommonSpirit Health

-

Ascension

-

Providence Health & Services

-

Trinity Health

-

Intermountain Health

-

Bupa

-

AXA SA

-

Ramsay Health Care

-

Apollo Hospitals Enterprise

-

Fortis Healthcare

-

Teladoc Health

Primary Health Care Service Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 483.56 Billion |

| Market Size by 2035 | USD 814.17 Billion |

| CAGR | CAGR of 5.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Reason (Injury, Preventive Care, Chronic Conditions, Acute Conditions, Pre-/Post-Surgery Care) • By Age Group (Infants, Pediatrics, Adults, Geriatrics) • By Mode of Consultation (Virtual Care, Physical Care) • By Provider (Hospitals, Clinics, Outpatient Departments, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | UnitedHealth Group, CVS Health, Cigna Group, Humana Inc., Elevance Health, Centene Corporation, Kaiser Permanente, HCA Healthcare, Tenet Healthcare, CommonSpirit Health, Ascension, Providence Health & Services, Trinity Health, Intermountain Health, Bupa, AXA SA, Ramsay Health Care, Apollo Hospitals Enterprise, Fortis Healthcare, Teladoc Health |

Frequently Asked Questions

The primary health care service market is expected to grow at a CAGR of 5.37% from 2026 to 2035.

The primary health care service market was valued at USD 483.56 billion in 2025.

Major growth factors include demand for accessible care, chronic diseases, aging population, preventive services, and adoption of digital health technologies.

The chronic conditions segment dominated the market in 2025 due to high global prevalence of diabetes, cardiovascular, and respiratory diseases.

North America dominated the primary health care service market due to advanced healthcare infrastructure, high primary care utilization, strong digital adoption.

Get in Touch