Ransomware Protection Market Report Scope & Overview:

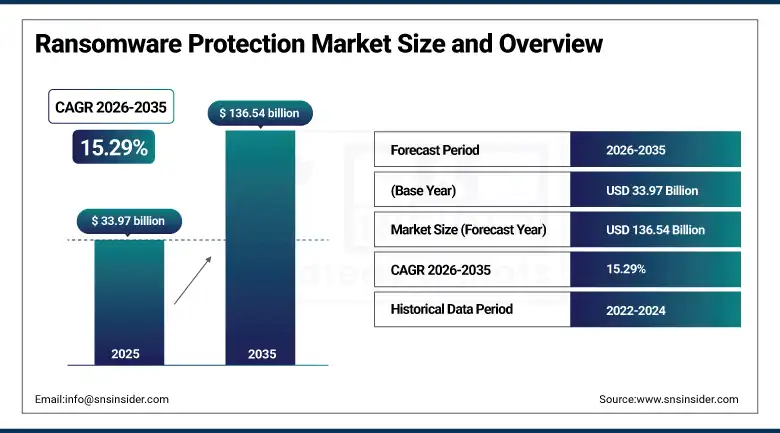

The Ransomware Protection Market was valued at USD 33.97 Billion in 2025 and is expected to reach USD 136.54 Billion by 2035, growing at a CAGR of 15.29% from 2026–2035.

The global ransomware protection market is growing at an exceptional pace. Ransomware attacks have become the most financially damaging class of cybercrime, costing global businesses over USD 20 billion annually through ransom payments, operational disruption, and remediation costs. Regulatory frameworks including CISA mandates, the EU NIS2 Directive, and HIPAA breach notification requirements are creating compliance-driven procurement that sustains investment independent of discretionary IT budget cycles. Cloud migration and hybrid work have expanded the attack surface. Organisations are responding with AI-driven detection, immutable backup infrastructure, zero-trust access controls, and managed detection and response services that collectively define the modern ransomware defence stack.

In January 2024, Veeam Software announced its Cyber Secure Program, combining purpose-built recovery technology with expert services to help enterprises prepare for, protect against, and recover from ransomware. The programme directly addressed the commercial gap between security prevention tools and recovery capability, acknowledging that enterprises must plan for successful breaches rather than assuming prevention will always succeed.

Market Size and Forecast

-

Market Size in 2026E: USD 39.16 Billion

-

Market Size by 2035: USD 136.54 Billion

-

CAGR: 15.29% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

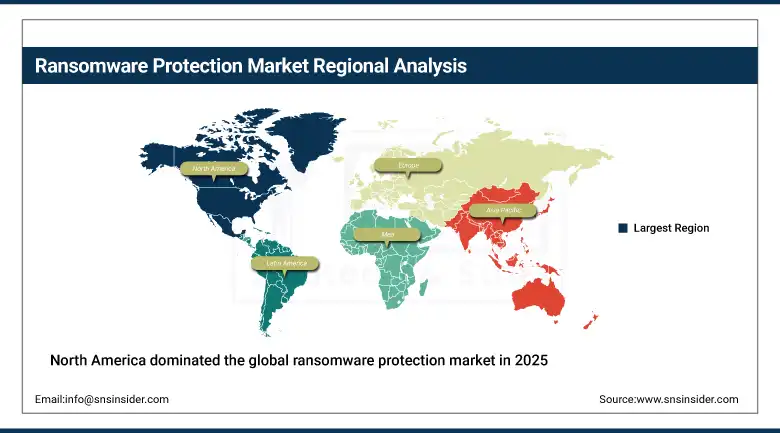

Largest Region: North America

To Get more information On Ransomware Protection Market - Request Free Sample Report

Ransomware Protection Market Trends

-

AI and machine learning integration is enabling behavioural anomaly detection that identifies ransomware activity before file encryption begins, reducing response time from hours to seconds.

-

Immutable backup and air-gapped data isolation technologies are becoming standard enterprise recovery infrastructure, ensuring clean restore points that ransomware cannot encrypt or delete.

-

Ransomware-as-a-service affiliate models are lowering the technical barrier for attackers, creating a broader and more frequent threat landscape that sustains investment in advanced protection layers.

-

Zero-trust network segmentation is limiting lateral movement post-compromise, containing ransomware propagation within isolated network segments rather than allowing cross-enterprise spread.

-

SME-focused affordable ransomware protection products are capturing the fastest-growing market segment as small businesses face the same criminal targeting as large enterprises without equivalent security budgets.

U.S. Ransomware Protection Market Outlook

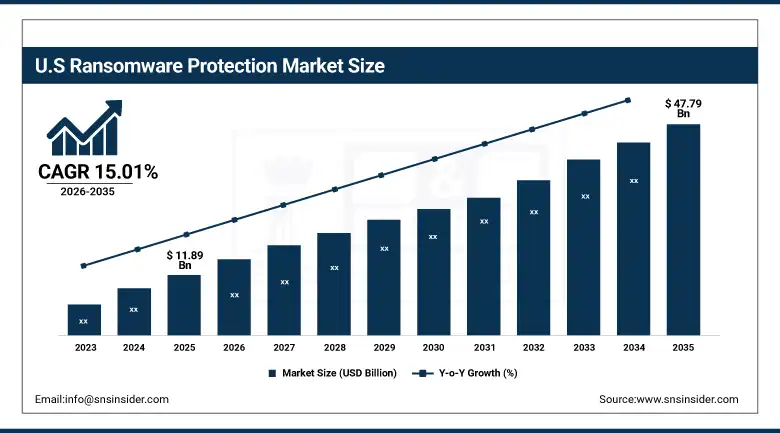

The U.S. Ransomware Protection Market was valued at approximately USD 11.89 Billion in 2025 and is expected to reach approximately USD 47.79 Billion by 2035, growing at a CAGR of approximately 15.01%.

The U.S. is the world’s largest ransomware protection market. MEITY data confirms that nearly 50% of global ransomware attacks target U.S. organisations. Critical infrastructure sectors including healthcare, energy, and government face mandatory reporting requirements under CISA guidance. The SEC’s cybersecurity disclosure rules require public companies to report material breaches within four days, creating board-level urgency around ransomware preparedness.

In November 2025, Arctic Wolf announced plans to enhance its Aurora Endpoint Security platform with AI-powered ransomware prevention and rollback capabilities, accelerated by the acquisition of UpSight Security. The upgrade targets the enterprise endpoint protection market whose ransomware detection and automatic rollback features reduce attack dwell time and recovery cost for mid-market enterprises that cannot afford dedicated SOC operations.

Ransomware Protection Market Segment Analysis

-

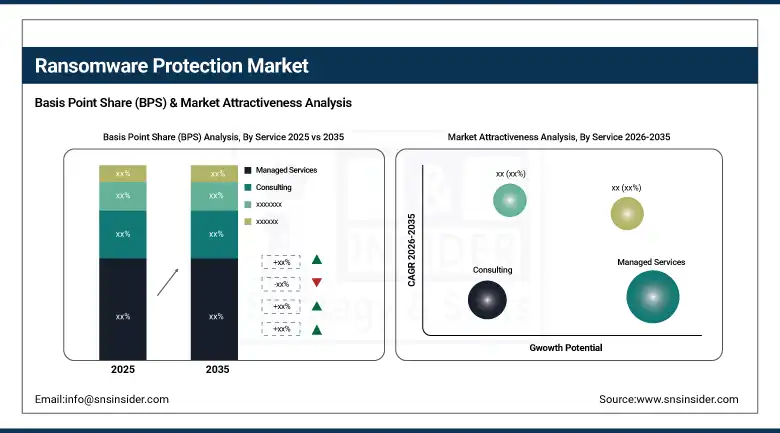

By Service, the Managed Services segment dominated the Ransomware Protection Market with approximately 43.80% share in 2025, while the Consulting segment is the fastest growing with a CAGR of 17.90% during the forecast period.

-

By Deployment Mode, the Cloud segment dominated the Ransomware Protection Market with approximately 61.50% share in 2025, while the On-Premises segment is expected to grow at a CAGR of 14.20% during the forecast period.

-

By Organization Size, the Large Enterprises segment dominated the Ransomware Protection Market with approximately 67.30% share in 2025, while the SMEs segment is the fastest growing with a CAGR of 18.60% during the forecast period.

-

By End User, the BFSI segment dominated the Ransomware Protection Market with approximately 24.90% share in 2025, while the Healthcare segment is the fastest growing with a CAGR of 19.40% during the forecast period.

By Service, managed services dominate, consulting grows fastest

Managed services retained the dominant service position in the ransomware protection market in 2025. Enterprises outsource 24/7 security operations because skilled threat analysts are scarce and expensive to recruit. Managed detection and response providers deliver continuous monitoring, threat hunting, and incident containment at a cost that is commercially lower than equivalent in-house capability. The 2023-2025 wave of high-profile ransomware incidents demonstrated that detection speed is the primary determinant of attack impact, creating procurement motivation that sustains managed service contract growth across enterprise and mid-market customer segments simultaneously.

Consulting is the fastest-growing service because regulatory compliance frameworks increasingly mandate formal risk assessments, penetration testing, and incident response planning documentation. NIS2 in Europe, CISA guidance in the U.S., and sector-specific regulations require evidence of security programme rigor that consulting engagements produce. Each new regulatory tightening event creates a compliance consulting procurement wave whose commercial scale reflects the breadth of affected organisations and the legal consequences of non-compliance.

By End User, BFSI dominates, healthcare grows fastest

BFSI retained the dominant end user position in the ransomware protection market in 2025. Financial institutions hold the highest-value data assets, face the most comprehensive regulatory cybersecurity requirements, and have the strongest financial motivation to prevent disruption. Ransomware attacks on banks and insurers trigger regulatory reporting obligations, potential fines, and reputational damage whose combined cost substantially exceeds security investment. This calculus creates non-discretionary security procurement that sustains above-average investment through economic cycle variation.

Healthcare is the fastest-growing end user because ransomware attacks on hospitals create immediate life-safety consequences that no other industry faces equivalently. When ransomware encrypts clinical systems, patient monitoring, imaging, and medication management are disrupted at a severity that creates direct patient harm risk. Healthcare regulators including HHS have elevated enforcement activity, mandatory reporting timelines, and security investment expectations following high-profile hospital attacks. Each major healthcare ransomware incident creates a procurement wave across peer institutions whose risk awareness drives emergency security budget allocation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Ransomware Protection Market Insights

North America dominated the global ransomware protection market in 2025 as the primary target of global ransomware campaigns and the largest enterprise security investment market. The U.S. accounts for approximately 87.4% of North American revenues through its concentration of critical infrastructure, regulated industries, and enterprise headquarters. CISA’s mandatory cyber incident reporting, the SEC’s four-day material breach disclosure requirement, and HIPAA enforcement are collectively creating the world’s most comprehensive compliance-driven security procurement environment.

Canada contributes approximately 12.6% of North American revenues through its financial services and energy sector security investment, federal government cyber resilience programme funding, and the alignment of Canadian privacy law with U.S. enterprise security standards that creates consistent procurement across the North American market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Ransomware Protection Market Insights

Europe is a significant and rapidly evolving ransomware protection market. NIS2 Directive implementation across EU member states is creating mandatory security investment requirements for critical infrastructure operators whose compliance deadlines drive procurement urgency. GDPR’s breach notification requirements add financial and reputational penalty risk that sustains investment in prevention and detection.

Germany accounts for approximately 22.3% of European revenues through its industrial and financial services sector security investment, the BSI’s active threat guidance, and the commercial presence of leading security vendors.

The United Kingdom and France are significant secondary European markets where financial services regulation, government digital service security investment, and the NCSC and ANSSI’s active industry guidance create structured institutional demand. The post-pandemic acceleration of cloud adoption across European enterprises simultaneously expanded attack surfaces and drove cloud security procurement that strengthens the ransomware protection market.

Asia Pacific Ransomware Protection Market Insights

Asia Pacific is the fastest-growing regional ransomware protection market, driven by rapid digitisation, expanding cloud adoption, and the growing sophistication of ransomware attacks targeting Asian enterprises. China accounts for approximately 44.8% of Asia Pacific revenues through its large enterprise sector’s security investment and domestic cybersecurity regulation.

India and Southeast Asia are the most commercially dynamic emerging markets, where financial services digitalisation, government digital infrastructure, and growing awareness of ransomware risk are creating first-time enterprise security procurement at above-average growth rates.

Japan and South Korea represent technically sophisticated secondary markets whose industrial and technology sector security investment, active national cybersecurity agencies, and above-average enterprise security maturity create consistent premium product procurement. Australia’s Essential Eight cybersecurity framework and the government’s mandatory ransomware reporting legislation create compliance-driven procurement aligned with the most stringent Western market standards.

MEA & Latin America Ransomware Protection Market Insights

The Middle East and Africa and Latin America are growing ransomware protection markets where digital transformation, critical infrastructure targeting, and progressive regulatory development are creating structured security investment. UAE leads MEA revenues at approximately 38.4% through its financial services sector’s advanced security posture, the CBUAE’s cybersecurity standards for banks, and government digital infrastructure protection investment under the UAE National Cybersecurity Strategy.

Brazil leads Latin American revenues at approximately 44.2% through its large financial services sector, LGPD data protection requirements, and the active Latin American threat actor ecosystem. Brazil’s financial services organisations are among the most targeted in the region, creating institutional procurement motivation that sustains above-average security investment relative to the broader Latin American enterprise market.

Market Dynamics

Growth Drivers: Escalating ransomware attack frequency and financial impact and compliance mandates creating non-discretionary investment

Ransomware attack frequency and financial impact are the market’s most direct commercial growth drivers. Average ransom payments exceed USD 1 million. Operational disruption during and after an attack extends total cost to multiples of the ransom demand. Each high-profile attack creates a quantifiable financial case study that enterprise CFOs use to justify security investment. The criminal ecosystem’s professionalisation through RaaS platforms ensures that attack frequency will continue growing regardless of defensive improvements, creating a permanent commercial motivation for protection investment.

Compliance mandates are creating non-discretionary procurement that is independent of discretionary IT budget decisions. NIS2, CISA guidance, SEC disclosure rules, and HIPAA enforcement collectively require documented security programmes whose components include the endpoint protection, network monitoring, backup infrastructure, and incident response capability that ransomware protection vendors provide. Each regulatory tightening creates an addressable compliance procurement event whose commercial scale reflects the number of affected organisations and the penalty risk of non-compliance.

Restraints: Security skills shortage limiting implementation quality and security tool proliferation creating management complexity

The cybersecurity skills shortage limits the effectiveness of security investments. Organisations that procure advanced ransomware protection tools often lack the trained personnel to configure, tune, and respond to alerts at the quality level that protection requires. This gap drives managed service adoption but creates total cost challenges for organisations whose security budgets must cover both product and service investment simultaneously.

SME budget constraints create protection gaps that attackers actively exploit. Affordable cloud-based ransomware protection is improving accessibility but has not yet eliminated the commercial barrier that prevents SMEs from achieving enterprise-equivalent protection levels. SME attacks are growing as criminal groups recognise that smaller organisations offer high-probability targets with lower security sophistication than large enterprises.

Opportunities: AI-powered autonomous response reducing human operator dependency and immutable backup market expansion

AI-powered autonomous response represents the most commercially differentiated near-term capability development. Systems that detect ransomware behavioural indicators and automatically isolate affected endpoints, terminate malicious processes, and initiate recovery workflows reduce the attack dwell time that determines breach impact from the 24-72 hours of human-response timelines to minutes. Each commercial deployment that demonstrates measurably reduced attack impact creates adoption evidence that sustains premium pricing for autonomous response capability.

Immutable backup infrastructure is creating a commercially significant adjacent market as enterprises recognise that prevention alone cannot guarantee protection. Purpose-built ransomware-resilient backup solutions including air-gapped repositories, immutable object storage, and offline encryption key management create recovery assurance that traditional backup infrastructure cannot provide against sophisticated ransomware variants designed to corrupt backup systems before triggering encryption.

Recent Developments:

-

2025: Arctic Wolf announced plans to enhance Aurora Endpoint Security with AI-powered ransomware prevention and rollback capabilities in November 2025, accelerated by the acquisition of UpSight Security. The upgrade targets mid-market enterprises that need automated endpoint ransomware containment without dedicated SOC operations.

-

2024: Veeam Software launched its Cyber Secure Program in January 2024, combining purpose-built recovery technology with expert services for ransomware preparedness, protection, and recovery. The programme addresses the commercial gap between prevention tools and validated recovery capability.

-

2025: CrowdStrike expanded its Falcon platform with AI-powered automated ransomware detection and response in 2025, achieving sub-second threat containment at endpoint level. The enhancement targeted enterprise SOC teams whose analyst capacity cannot scale proportionally with attack volume growth.

Ransomware Protection Market Key Players

-

Microsoft

-

Cisco Systems

-

CrowdStrike

-

Palo Alto Networks

-

Broadcom

-

Sophos

-

Trend Micro

-

Fortinet

-

McAfee

-

Veeam Software

-

Arctic Wolf

-

Bitdefender

-

Kaspersky

-

SentinelOne

-

Zscaler

-

Cybereason

-

Malwarebytes

-

Acronis

-

Commvault

-

Rubrik

Ransomware Protection Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 33.97 Billion |

| Market Size by 2035 | USD 136.54 Billion |

| CAGR | CAGR of 15.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solutions, Services) • by Service (Managed Services, Consulting) • by Deployment Mode (Cloud, On-Premises) • by Organization Size (Large Enterprises, SMEs) • by End User (BFSI, Healthcare, Government, IT & Telecom, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Microsoft, Cisco Systems, CrowdStrike, Palo Alto Networks, Broadcom, Sophos, Trend Micro, Fortinet, McAfee, Veeam Software, Arctic Wolf, Bitdefender, Kaspersky, SentinelOne, Zscaler, Cybereason, Malwarebytes, Acronis, Commvault, Rubrik |

Frequently Asked Questions

The Ransomware Protection Market is expected to grow at a CAGR of 15.29% from 2026 to 2035.

The Ransomware Protection Market was valued at USD 33.97 Billion in 2025.

Escalating ransomware attack frequency and financial impact creating non-discretionary security investment, compliance mandates including NIS2, CISA guidance, and SEC disclosure rules requiring documented security programmes, and AI-driven detection capability improving defence effectiveness against evolving attack methodologies.

Managed Services dominated the Ransomware Protection Market in 2025.

North America dominated the Ransomware Protection Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch