Proximity Sensor Market Size & Overview:

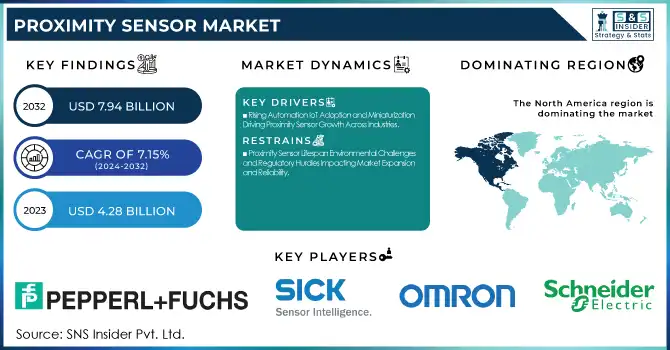

The Proximity Sensor Market was valued at USD 4.28 billion in 2023 and is expected to reach USD 7.94 billion by 2032, growing at a CAGR of 7.15% over the forecast period 2024-2032. The Proximity Sensor Market is mainly fueled by the automation trend, demand for touchless interfaces, and Internet of Things advancements in various industries. Consumers are looking for precise readings, long-lasting devices, and less energy consumption, while industries want speed and robustness against environmental conditions. Things to Look for in Performance Benchmarks: Sensing Range, Reliability, and AI Integration Some of the prominent applications are vehicular ADAS, industrial robotics, home intelligent apparatuses, and medical instruments. Continued innovation fueled by increasing adoption in these industries enables proximity sensors to play a crucial role in precision detection and seamless automation.

Get more information on Proximity Sensor Market - Request Sample Report

Market Dynamics

Key Drivers:

-

Rising Automation IoT Adoption and Miniaturization Driving Proximity Sensor Growth Across Industries

Growing automation adoption and increasing IoT penetration in industrial sectors are expected to fuel the growth of the proximity sensor market. The growth in the automotive sector is attributed to the large-scale adoption of Advanced Driver Assistance Systems (ADAS), parking assistance, and autonomous driving features, driving the consumption of sensors. Furthermore, development concerning Industry 4.0 and smart manufacturing is contributing to the rise of proximity sensors in robotics, predictive maintenance, and industrial automation. Moreover, the increasing trend of miniaturization in consumer electronics including smartphones and wearables also propels the growth of the market.

Restrain:

-

Proximity Sensor Lifespan Environmental Challenges and Regulatory Hurdles Impacting Market Expansion and Reliability

One of the other major restraints is that certain proximity sensors have a shorter lifetime, especially in aggressive environments. Taking photoelectric and ultrasonic sensors as examples, such sensors have already been in a large proportion of measured sites working for a long time, it will apply extreme conditions, severe vibration, and mechanical stress causing stronger or weaker degree of deterioration. In addition, manufacturers must also tackle further challenges such as standardization issues and regulatory compliance, which can add significant complications, especially when expanding their business into a region with different safety and performance standards.

Opportunity:

-

Advancing Sensor Technologies Smart Infrastructure and RFID Adoption Unlock Growth in Proximity Sensor Market

The technology market has an opportunity in the evolution of sensor technologies, such as artificial intelligence device-based and/or wireless proximity sensor technology, which interact to maximize the efficiency of operations and create new added-value applications. Additionally, the growth of smart infrastructure and connected cities is anticipated to fuel market growth in terms of security and surveillance systems. Moreover, the need for energy-efficient and robust sensors in demanding environments, including aerospace and defense, provides new growth opportunities. RFID technology, especially in the Asia-Pacific region, has attractive prospects in the future with the rapid industrialization and development of the automotive industry as well as the increasing of consumer electronic consumption level

Challenges:

-

Detection Range Accuracy and Environmental Sensitivity Challenges Hindering Proximity Sensor Adoption in Precision Applications

Technological limitations in detection range and accuracy are some of the major factors hampering the growth of the proximity sensor market. However, proximity sensors operate well in a laboratory setup, but this sensor is ill-affected by external factors such as temperature measurement, humidity, and electromagnetic interference. As an example, inductive sensors have a challenge detecting non-metallic objects, while capacitive sensors are very sensitive to environmental contaminations, such as dust and moisture. It poses consistency problems in some of the high-precision applications, such as industrial automation and automotive safety systems.

Segment Analysis

By Products

In 2023, Fixed Distance Proximity Sensors accounted for 63.6% of the total proximity sensors market share, and this segment is anticipated to grow at the fastest CAGR in 2024-2032. Posted via Industry Today. This growth mainly comes from: Industrial automation, Automotive (Safety Systems), and Smart consumer electronics (A pair of application categories). Providing high reliability and efficiency while detecting an object at a specified distance, they are used in manufacturing, robotics, and assembly lines where reliable object detection is important. Secondly, further accelerating their adoption in smart factories and autonomous vehicles are rapid developments in sensor miniaturization and integration with IoT. The rising need for contactless sensing technology in different sectors, especially after the pandemic, has also propelled the growth of the fixed-distance proximity sensor market. They are ideal for automated doors, conveyor belt systems, and medical devices due to their benefits such as low power consumption, increased lifespan, and accurate object identification. In addition, the continued focus on R&D with respect to AI-based proximity sensing and wireless connectivity solutions is predicted to bolster their functionalities which will continue to drive demand in the near future.

By Technology

In 2023, inductive sensors had the largest market share at 32.4%. Inductive proximity sensors account for the vast majority of applications in industrial automation, automotive, and related manufacturing applications. These sensors always provide robust and reliable detection of metal in a harsh environment, making them well-suited to applications in robotics, conveyor systems, and predictive maintenance. Widely used in factories, assembly lines, heavy machinery, etc. because of its high durability, moisture-proof, dustproof, and accurate object recognition.

Ultrasonic proximity sensors are projected to be the fastest-growing sector over the forecast period from 2024-2032, due to the rising application of ultrasonic sensors in automotive safety systems, smart infrastructure, and healthcare systems. Ultrasonic sensors, unlike inductive sensors, can detect metallic and non-metallic objects (including liquids) so they are much more versatile than inductive sensors. The growing adoption of self-driving vehicles, parking assistance, and touchless sensing in consumer electronics and medical devices is driving their growth.

By Application

In 2023, the automotive sector held the proximity sensor market with a 36.8% share owing to the increasing adoption of advanced driver assistance systems (ADAS), autonomous vehicles, and safety features. However, proximity sensors are critical for parking assistance, collision-aversion, and hands-free access systems that help enhance vehicle safety and convenience. The widespread adoption of electric vehicles (EVs) and connected cars was accelerated by the increasing integration of these sensors in such systems. In addition, the influence of severe government norms related to vehicle safety and the requirement for automation in the automobile sector have also propelled the adoption of the proximity sensors

Consumer electronics will have the fastest CAGR during 2024 –2032 owing to the growing usage of proximity sensors in smartphones, wearables, and smart home devices. Touchless controls, gesture recognition, and power-saving functionalities are a few of them that have fueled the demand for this segment. These accelerating IoT, the miniaturization of sensors, and the growing consumer demand for smart and connected devices are the major drivers that will continue to stimulate market growth.

Regional Analysis

In 2023, the proximity sensor market was led by North America, with a 34.3% share, owing to increased demand in the automotive, industrial automation, and consumer electronics sectors. Globally, the market is expected to expand due to an increase in the usage of advanced driver assistance systems (ADAS) in vehicles and the presence of top automotive companies such as Ford and General Motors. The industrial sector in the U.S. and Canada further uses proximity sensors to automate processes, instead of using human labor in a manually controlled environment, which is then applicable for smart manufacturing processes in robotics. Companies such as Rockwell Automation and Honeywell are instrumental in embedding these sensors into industrial automation solutions, thereby reinforcing the region in the market space.

Asia Pacific is expected to grow at the fastest CAGR from 2024 to 2032, owing to rapid industrialization, rising consumer electronics demand, and growth in automotive production. The comparatively high adoption of proximity sensors in countries like China, Japan, and South Korea is attributed to the presence of global smartphone manufacturing brands in the region including Samsung, and Xiaomi among others that are utilizing proximity sensors for functions like gesture control and face detection. In addition to this, supportive EV manufacturers operating in the region, such as BYD and Tata Motors, are propelling the demand for proximity sensors between advanced vehicle safety & automation features, thereby adding up revenue to the proximity sensor industry in ASEAN countries.

Get Customized Report as per your Business Requirement - Request For Customized Report

Key players

Some of the major players in the Proximity Sensor Market are:

-

Pepperl+Fuchs (Inductive Proximity Sensors, Capacitive Proximity Sensors)

-

Sick AG (Photoelectric Sensors, Ultrasonic Sensors)

-

Omron Corporation (E2E Proximity Sensors, E2B Proximity Sensors)

-

Honeywell International Inc. (Limitless™ WLS Series Wireless Limitless™ Switches, 943 Series Vibration Sensors)

-

Rockwell Automation (Allen-Bradley) (42EF RightSight™ Photoelectric Sensors, 871TM Inductive Proximity Sensors)

-

Schneider Electric (XS Inductive Proximity Sensors, XT Capacitive Proximity Sensors)

-

Balluff GmbH (BES Inductive Sensors, BOS Photoelectric Sensors)

-

IFM Electronic (Inductive Sensors, Capacitive Sensors)

-

Keyence Corporation (EZ Series Inductive Proximity Sensors, EM Series Magnetic Proximity Sensors)

-

Turck (Bi5 Inductive Proximity Sensors, Q08 Inductive Proximity Sensors)

-

Panasonic Corporation (GX Series Inductive Proximity Sensors, EQ-500 Photoelectric Sensors)

-

Autonics Corporation (PR Series Inductive Proximity Sensors, PS Series Capacitive Proximity Sensors)

-

Contrinex (DW Series Inductive Sensors, C23 Series Photoelectric Sensors)

-

Banner Engineering (M18 Series Inductive Proximity Sensors, Q12 Series Photoelectric Sensors)

-

Baumer Group (IFRM Inductive Sensors, O500 Photoelectric Sensors)

Recent Trends

-

In November 2024, Pepperl+Fuchs and Wenglor launched inductive sensors for high-temperature environments up to 250°C, ensuring reliable object detection with extended sensing distances.

-

In December 2024, Aeva will expand its partnership with SICK to integrate FMCW technology into precision sensors for factory automation.

-

In September 2024, Turck expanded its sensing and automation solutions with new radar distance sensors and the FS121 processing unit for remote flow monitoring.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 4.28 Billion |

| Market Size by 2032 | USD 7.94 Billion |

| CAGR | CAGR of 7.15% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Fixed Distance Proximity Sensor, Adjustable Distance Proximity Sensor) • By Technology (Inductive, Magnetic, Ultrasonic, Capacitive, Photoelectric) • By Application (Aerospace & Defense, Automotive, Industrial, Consumer Electronics, Food & Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Pepperl+Fuchs, Sick AG, Omron Corporation, Honeywell International Inc., Rockwell Automation (Allen-Bradley), Schneider Electric, Balluff GmbH, IFM Electronic, Keyence Corporation, Turck, Panasonic Corporation, Autonics Corporation, Contrinex, Banner Engineering, Baumer Group. |

Frequently Asked Questions

Ans: North America dominated the Proximity Sensor Market in 2023.

Ans: The Automotive segment dominated the Proximity Sensor Market in 2023.

Ans: The major growth factor of the Proximity Sensor Market is the rising demand for automation and touchless sensing technology across automotive, industrial, and consumer electronics sectors.

Ans: Proximity Sensor Market size was USD 4.28 billion in 2023 and is expected to Reach USD 7.94 billion by 2032.

Ans: The Proximity Sensor Market is expected to grow at a CAGR of 7.15% during 2024-2032.

Get in Touch