Fiber Optics Market Report Scope & Overview:

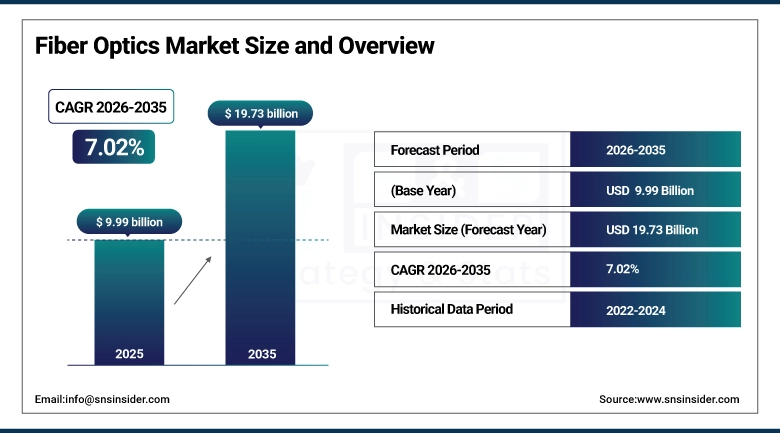

The Fiber Optics Market was valued at USD 9.99 billion in 2025 and is expected to reach USD 19.73 billion by 2035, growing at a CAGR of 7.02% from 2026-2035.

The Fibre Optics Market is driven by Glass threads thinner than a human hair are, in a very real sense, the physical substrate of the modern digital economy. The internet traffic that businesses and consumers rely on is carried by fiber optics, the financial transaction data that run markets run on, the medical imaging data that clinical decisions are built around. But its eyeballs are trained on the fiber optic infrastructure market- data use grows every year, and the physics of fiber make it orders of magnitude better than copper for any kind of high-bandwidth long-distance transmission, while its alternatives (wireless) simply supplement, not supplant fiber in the network topology of any grown-up telecom works. Broadly the sectors have always known the necessity of fiber, but what is genuinely new is that fiber is now being accepted as necessity and not optional. High-speed networks with low latency are required by healthcare facilities for imaging and telemedicine. Manufacturers of automotive devices require fiber for in-vehicle network solutions for high-bandwidth advanced driver assistance systems (ADAS) and infotainment. For inherent advantages in immunity to electromagnetic interference, the military and aerospace programs need fiber. Probably the single biggest driver of new fiber demand globally is the 5G rollout, because wireless 5G is ultimately being carried on fiber backhaul networks between towers.

USD 65 billion has been earmarked for broadband in the U.S. Infrastructure Investment and Jobs Act, with a larger share assigned to fiber network rollouts in unserved communities. The Broadband Data Collection project run by the FCC has pinpointed more than 8 million U.S. locales still without at least one access to broadband service from a wireline provider, a sizeable addressable fiber expansion opportunity with federal funding behind it..

Fiber Optics Market Size and Forecast

-

Market Size in 2025: USD 9.99 Billion

-

Market Size by 2035: USD 19.73 Billion

-

CAGR: 7.02% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Fiber Optics Market - Request Free Sample Report

Fiber Optics Market Trends

-

5G network rollout globally is requiring dense fiber backhaul infrastructure connecting every base station, generating fiber cable procurement volumes that will persist through the forecast period as 5G densification continues.

-

Hyperscale data center expansion driven by AI computing demand is generating unprecedented fiber cabling requirements both within facilities and for the high-capacity interconnects between data centers.

-

Government-backed broadband expansion programs in the U.S., EU, India, and China are providing structural demand for fiber to the home (FTTH) deployments in previously underserved rural and semi-rural areas.

-

Medical applications for fiber optics endoscopy, surgical illumination, telemedicine network infrastructure are expanding as healthcare digitalization requires both clinical instrument fiber and facility network fiber.

-

Plastic optical fiber (POF) is gaining adoption in automotive and consumer electronics for its flexibility, light weight, and lower installation cost advantages over glass fiber in applications where shorter transmission distances are involved.

-

Submarine fiber cable installations are seeing renewed investment as growing intercontinental data traffic between AI computing clusters, cloud regions, and global users demands higher-capacity undersea connectivity.

-

Green data center requirements are favoring fiber over copper for server rack connectivity as fiber's lower energy requirements and heat generation reduce the cooling burden of high-density computing environments.

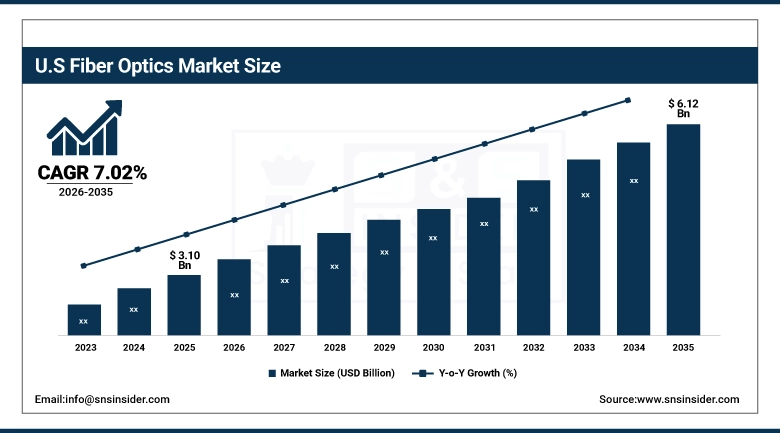

U.S. Fiber Optics Market Size Outlook:

The U.S. Fiber Optics Market was valued at USD 3.10 billion in 2025 and is expected to reach USD 6.12 billion by 2035, growing at a CAGR of 7.02% from 2026-2035.

The United States is investing in fiber optics at a scale that is structurally changing the domestic market's long-term trajectory. The Infrastructure Investment and Jobs Act's USD 65 billion broadband allocation, combined with state-level matching programs and utility company FTTH investment, is driving fiber cable deployment volumes that the market has not seen before. Major carriers including AT&T, Verizon, and a growing number of competitive fiber providers (including Frontier, Lumen, and regional operators) are actively extending fiber networks to residential and business customers. The AI computing boom is simultaneously driving hyperscale data center fiber demand in the Midwest, Mid-Atlantic, and Southeast the primary data center concentration corridors at volumes that were not anticipated even two years ago. Corning, headquartered in the U.S. and the world's leading fiber optics manufacturer, both supplies and benefits from this domestic investment cycle.

Corning said demand for its optical fiber products was hit record highs in 2024, buoyed by carriers accelerating FTTH buildouts and hyperscale data center operators expanding AI computing infrastructure. As one of the programs established under IIJA, planning and implementation grants for broadband deployment were funded by the BEAD Program, which allocated USD 42.45 billion to states, with express preference for fiber-to-the-home as the technology of choice for many of the program-eligible projects.

Fiber Optics Market Segment Analysis

-

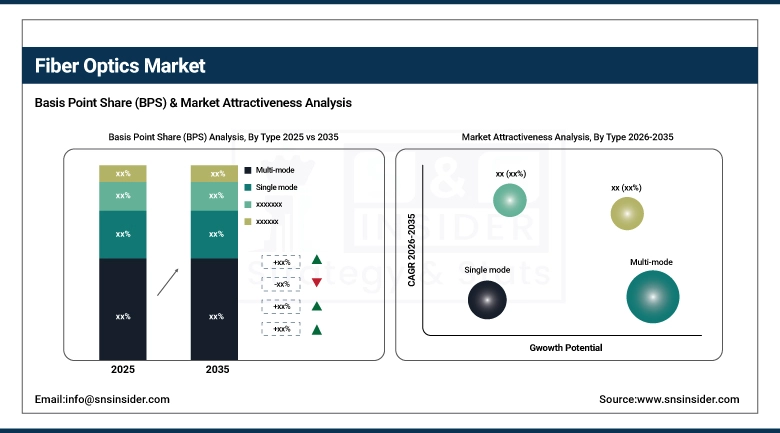

By Type, Multi-mode segment dominated with 51.3% share in 2025; Plastic Optical Fiber (POF) fastest growing (CAGR).

-

By Application, Telecom segment dominated with 40.3% share in 2025; Medical segment fastest growing (CAGR).

By Type, Multi-mode segment dominates the Fiber Optics Market, Plastic Optical Fiber (POF) expected to grow fastest

Multi-mode fiber optic cable had a 51.3% market share in 2025, and its relative share indicates where the volume of fiber installations is concentrated. Getting into applications, local area networks inside buildings, data center intra-facility connections, campus networks connecting buildings across short distances. The high bandwidth over relatively shorter distances suits enterprise network infrastructure perfectly and the lower connector and transceiver costs compared to single-mode fiber position the total installed cost competitively for cost-conscious campus and building network deployments. Hundreds of thousands multi-mode fiber is on demand globally to be used by healthcare, education, and manufacturing facilities internally and therefore have a large, steady and geographic diverse demand base.

From 2026 to 2035, plastic optical fiber is expected to grow, in terms of CAGR, at the highest rate. The reasons are both practical and cost: POF is much more flexible, easier to install with generic tools instead of using specialized fusion splicing hardware, and cheaper -- by 1000% on a per-meter basis -- than traditional glass fiber optics. These characteristics make POF, in-vehicle networks for consumer electronics automotive, home audio systems and short-range high-speed connections the correct specification choice. Additionally, the automotive sector might be POF biggest POF growth opportunity because modern automobiles with digital cockpits, surround-sound audio, ADAS sensor networks and multiple display screens in compact, vibration-prone environments need networking solutions for circuitry that POF serves very well.

By Application, Telecom segment dominates the Fiber Optics Market, Medical segment expected to grow fastest

In 2025, telecom remained the largest application segment (40.3%), and the demand drivers underlying the demand in this segment do not seem to be weakening. Fiber backhaul between every base station and the core network no wireless infrastructure is wireless all the way back and the requirement that 5G have a small cell no more than a few hundred meters from each other mean more fiber connections per square kilometer of coverage than any mobile networks ever required. Fiber to the home deployment programs in the U.S., EU and Asia are also aggressively deploying FTTH optical access networks to households as the performance gap between FTTH and any other alternative had made fiber the only future-proof resident broadband technology. The fiber network capital investment to be made by telecom companies over the next decade, measured in hundreds of billions of dollars, ensures a setting in which fiber supply chain will depend less on current procurement basis, providing key support for both fiber cable manufacturers and equipment suppliers at levels of activity which will carry-on over the forecast period.

The fastest growth in CAGR from 2026-2035 will be witnessed in medical segment. Clinical demand pulls are converging at once, where precision optical fiber improves fiber optic endoscopy instruments for high-definition imaging, surgical illumination and fiber light guides, whilst high-bandwidth network connectivity is required for diagnostic imaging systems to transfer large file sizes in the timeframes that clinical workflow requires and that telemedicine infrastructure will demand for consistent and reliable high-speed connectivity that only the optical domain can deliver to hospital quality standards. Digital transformation and AI diagnostic tools, remote patient monitoring, and high-definition telehealth is booming, and the network infrastructure requirements are climbing in a way that makes fiber the communications medium of choice for even the most serious clinical technology investmen.

Fiber Optics Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

55% |

|

North America |

United States |

88% |

|

Europe |

Germany |

24% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

45% |

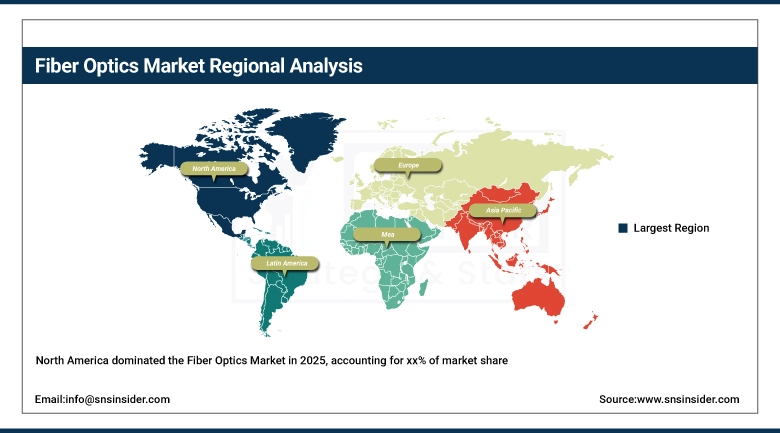

North America Fiber Optics Market Insights

North America is a leading region in the global Fiber Optics Market, with the U.S. pushing an accelerated fiber deployment cycle driven by federal infrastructure funding, carrier investment programs and unprecedented hyperscale data centre construction. Focus on fiber deployment in underserved areas by Amercian states across a multi-year procurement program totalling USD 42.45 billion via the new Broadband Equity, Access, and Deployment (BEAD) program will be a boon for manufacturers like Corning, OFS and others. AI computing infrastructure demand boom driven by hyperscalers decision to build massive data centre capacity in USA coexisting with fiber need from high-capacity fiber between facility interconnects and in-facility cabling to support the scale of distributed infrastructure needed for AI workloads and their large model training datasets and inference results transport.

According to the U.S. Telecom Industry Association, domestic fiber optic cable sales were setting records in 2025, spurred by carrier FTTH programs and hyperscale data center building. AT&T, for example, is in the middle of a massive FTTH buildout, with sweeping fiber-to-the-home deployment programs targeting 30 million locations by 2025, and Verizon is also pursuing similar goals, so this is the largest concurrent FTTH buildout in U.S. history.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Fiber Optics Market Insights

Asia Pacific represents a prominent fibre optics revenue region, holding over 29.7% of the total fibre optics market in 2025, and is expected to reach the highest CAGR during the forecast period. This leadership is propelled by rapid uptake of modern technologies across the region and extensive infrastructure projects as well as robust demand for high-speed Internet services. China's "Broadband China" campaign has been establishing a nationwide backbone fiber optic facilities that guarantees access to all people within cities and in rural areas. In India, the BharatNet project aims to connect around 250,000 villages with fiber optics, to fill gaps in connecting villages. Notably, Japan and South Korea are at the forefront of 5G deployment, which sees them incorporating fiber optics into their plans to deliver high-speed, low-latency communication for mobile and fixed broadband services. The vast manufacturing industry of the region also generates significant enterprise fiber demand both in automotive, electronics and industrial companies.

According to China's Ministry of Industry and Information Technology, China has built the largest optical fiber network in the world, with more than 6 million kilometers of optical fiber cable laid within its borders. India's massive BharatNet project has already achieved fibre installation in more than 180,000-gram panchayats (village clusters), and the central government has pledged more and more funds through additional budgets to provide high-speed connectivity to every single one of India's 600,000 villages.

Europe Fiber Optics Market Insights

The EU's Digital Decade targets aim for gigabit connectivity for all European households by 2030 as well as 5G coverage everywhere by 2030, and Germany has historically under-deployed fiber compared to its peers, but is seeing a significant acceleration in the government's Next Generation Broadband Initiative, which is providing funds to support FTTH rollout in cases where commercial build is uneconomic. National fiber deployment programs such as those in France's Plan France Très Haut Debit are some of the more progressive programs in Europe, with fiber connections covering nearly all of the French households. Much of the funding funnelling into fibre network builds across several southern and eastern European countries, who had previously very little fibre penetration, has stemmed from the EU's post-pandemic recovery fund commitments to digital infrastructure.

The Digital Decade target from the European Commission aims for all EU households to be covered by gigabit-speed connectivity by 2030 - which means deploying lots of fiber across member states. As one of the financial components of digital communication support programs expected to be implemented in the next five years in EU Member States, the European Investment Bank has allocated funding to multi-billion euro fiber network expansion projects..

Middle East & Africa and Latin America Fiber Optics Market Insights

Governmental vision programs and expansion of digital economy initiatives are powering infrastructure investments where subscriber basis and other macro-economic factors designate fiber a growing market within the Middle East and Africa. NEOM in Saudi Arabia is a fully funded project that alone needs an extensive fiber backbone across a development footprint of 26,500 square kilometres. UAE's telecom operators Etisalat (now e&) and du are some of the most advanced fibre operators for consumers in the region, ranking with some of the highest FTTH penetration rates in the world in the UAE's major cities. Submarine cable landing stations and national fiber backbone networks are laying the foundation for future broadband growth in Africa. Wide government programs and telecom operator investments make Brazil the undisputed regional heavyweight for fiber deployment in Latin America, while Mexico and Colombia both transition to phase II of their fiber builds via competitive telecom market dynamics..

In a recent report from the Communications and Space Technology Commission (CST), Saudi Arabia boasts fiber optic penetration in urban areas of over 80% making the Kingdom one of the leading countries in the region for fiber connectivity. Brazil's National Broadband Plan commits fiber to all 5,570 Brazilian municipalities, with implementation under the supervision of the National Telecommunications Agency (ANATEL) and funded through telecom operator investment programs.

Market Growth Drivers: Rising high-speed internet demand and global 5G infrastructure rollout driving sustained fiber optics market growth worldwide

The growth case for fiber optics is anchored in physics that do not change glass fiber carries data with lower loss over longer distances at higher speeds and a level of electromagnetic interference immunity that copper cables cannot match and that wireless cannot deliver (for high-bandwidth fixed applications). As the volumes of data that networks must carry continues to increase as a result of streaming media, cloud computing, AI workloads and IoT sensor networks, the gaps between the advantages of fiber and its alternatives only become larger, not smaller. The push for 5G is the most immediate and concentrated driver of new fiber demand, since 5G small cell architecture needs fiber backhaul for every individual antenna site which means fiber deployment density must scale up dramatically simply to support the wireless coverage consumers and businesses have come to expect. The expansion of cloud computing and AI computing infrastructure is coinciding with another fiber demand cycle for data center interconnects. Both drivers have well-known multi-year runway.

Ericsson's Mobility Report projects that 5G subscriptions will reach 5.6 billion globally by 2030, each requiring fiber backhaul infrastructure. Corning's fiber demand projections indicate that fiber to the home programs in the U.S. alone will require the equivalent of 10 times Earth's circumference in new fiber cable annually through 2027.

Market Restraints: High installation costs and competing wireless technologies limiting fiber optic adoption in remote and cost-sensitive markets

Fiber deployment costs are real and highly geographic. Trenching through constructed urban infrastructure raising pavement, digging adjacent to current utility lines, working through permitting for each block of deployment is expensive and slow ways in which rural greenfield deployments or stringing fibre on existing utility poles is not. For small and medium telecom operators even targeting only rural and under-served marks, the capex needed for fiber builds is often larger than the commercial economics that can support without subsidy. In addition to its capital cost, it has the full cost of maintenance, the use of specialist splicing and testing equipment, and the need for technically skilled installation crews. Some of the newer wireless broadband options such as Starlink's satellite service and fixed wireless access over 5G mmWave 2+ create actual competitive pressure in specific uses, as fiber economics would be under immediate duress in deployment cost driven use case.

Market Opportunities: Government broadband funding programs and emerging healthcare applications creating significant new fiber optics growth opportunities

Fiber Optics opportunity pipeline is fuller than it has ever been. Hundreds of billions of dollars that previously would not make economic sense as a project once construct costs are zero or nearly zero are being tapped by government broadband funding programs in the U.S. (BEAD), EU (Recovery Fund and Connecting Europe Facility), and India (BharatNet) and dozens of other as national programs with funding flowing within the next five years. The fiber demand in healthcare is another type of opportunity: hospitals require fiber because the AI diagnostic tools, high-definition surgical imaging and hospital information systems that are now becoming core clinical infrastructure require the bandwidth and reliability that fiber alone can offer; not because the government is leaning on them. With the acceleration of digitalization of healthcare, fiber is now becoming a requirement for those clinical technology programs that hospitals are deploying. Each of these technologies (smart cities, energy grid modernization and autonomous vehicle infrastructure) each layer additional incremental fiber demand that will deepen the revenue base to beyond traditional telecom.

Recent Developments:

-

2025: CommScope announced an official partnership with the MoneyGram Haas F1 Team as their Official Connectivity Partner in February 2025, with the collaboration enhancing the team's trackside operations through advanced fiber-based network solutions for real-time data connectivity and race-day telemetry support systems operating under extreme conditions.

-

2025: Corning expanded fiber optic cable production capacity at its U.S. manufacturing facilities, specifically targeting the hyperscale data center and FTTH broadband market segments experiencing record demand growth from AI infrastructure investment and carrier network expansion programs funded under the Infrastructure Investment and Jobs Act.

-

2026: Prysmian Group commissioned a new high-capacity submarine fiber optic cable manufacturing line at its Arco Felice facility in Italy, targeting the growing market for trans-oceanic AI data center interconnect cables as hyperscalers commission dedicated submarine cable systems connecting their cloud regions across the Atlantic and Pacific.

Fiber Optics Companies are:

-

Cisco Systems, Inc.

-

Prysmian Group

-

CommScope Holding Company, Inc.

-

Nexans S.A.

-

Sumitomo Electric Industries, Ltd.

-

OFS Fitel, LLC

-

LS Cable & System Ltd.

-

Hengtong Group

-

Sterlite Technologies Ltd.

-

Broadcom Inc.

-

Huawei Technologies Co., Ltd.

-

TE Connectivity Ltd.

-

Zyxel Communications

-

Lumentum Holdings Inc.

-

II-VI Incorporated (Coherent Corp.)

-

AFL Global

-

Belden Inc.

-

Optical Cable Corporation (OCC)

Fiber Optics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.99 Billion |

| Market Size by 2035 | USD 19.73 Billion |

| CAGR | CAGR of 7.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Single-mode, Multi-mode, Plastic Optical Fiber (POF)) • By Application (Telecom, Oil & Gas, Military & Aerospace, BFSI, Medical, Railway, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Corning Inc., Cisco Systems, Inc., Prysmian Group, CommScope Holding Company, Inc., Nexans S.A., Sumitomo Electric Industries, Ltd., Fujikura Ltd., OFS Fitel, LLC, LS Cable & System Ltd., Hengtong Group, Sterlite Technologies Ltd., Broadcom Inc., Huawei Technologies Co., Ltd., TE Connectivity Ltd., Zyxel Communications. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Fiber Optics Market in 2025.

Ans: The Telecom segment dominated the Fiber Optics Market with approximately 40.3% share in 2025.

Ans: The Multi-mode segment dominated the Fiber Optics Market with approximately 51.3% share in 2025.

Ans: The Fiber Optics Market was valued at USD 9.99 billion in 2025.

Ans: The Fiber Optics Market is expected to grow at a CAGR of 7.02% from 2026 to 2035.

Get in Touch