Rapid Medical Diagnostic Kits Market Report Scope & Overview:

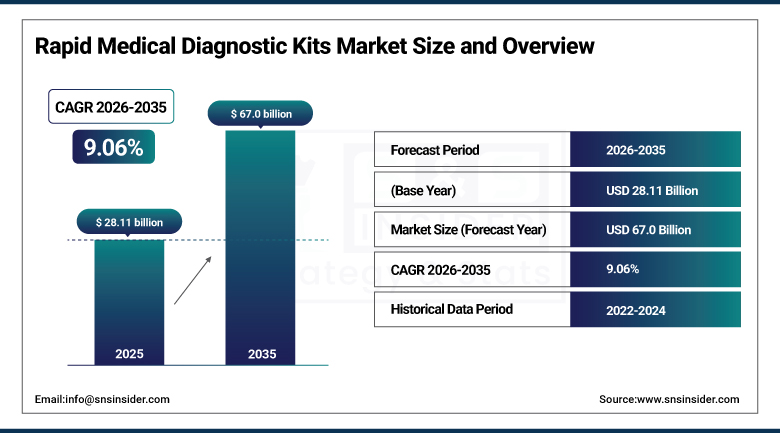

The Rapid Medical Diagnostic Kits Market was valued at USD 28.11 Billion in 2025 and is expected to reach USD 67.0 Billion by 2035, growing at a CAGR of 9.06% from 2026 to 2035.

The Rapid Medical Diagnostic Kits Market is witnessing strong growth owing to an increase in incidence of infections and chronic diseases, need for early diagnosis of diseases and increasing adoption of POCT technologies. Innovations like lateral flow assays and advanced biosensor based diagnostic tests are leading to better speeds and precision in test results. The growing development of healthcare facilities, particularly in developing nations and growing inclination towards at-home testing is fueling market growth. In addition, rising public awareness about health and favorable government measures for rapid diagnostics have led to significant market growth.

According to the World Health Organization (WHO), infectious diseases account for millions of deaths annually, including approximately 1.3 million deaths from tuberculosis in 2022 and around 2.5 million deaths from lower respiratory infections each year, underscoring the critical need for rapid and accurate diagnostic solutions. Furthermore, WHO data indicates that there were approximately 249 million malaria cases in 2022, with the majority occurring in low-resource regions where rapid diagnostic tests (RDTs) serve as the primary screening and detection tool, significantly driving global adoption of rapid medical diagnostic kits.

Market Size and Forecast

-

Market Size in 2026E: USD 30.66 Billion

-

Market Size by 2035: USD 67.0 Billion

-

CAGR: 9.06% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Rapid Medical Diagnostic Kits Market - Request Free Sample Report

Rapid Medical Diagnostic Kits Market Trends

-

Rising prevalence of infectious diseases and outbreaks driving strong demand for rapid medical diagnostic kits for early and on-site disease detection

-

Growing adoption of point-of-care testing solutions enabling quick diagnosis in clinics, emergency settings, and remote healthcare environments

-

Increasing focus on early screening and preventive healthcare supporting widespread use of rapid diagnostic kits for timely clinical decision-making

-

Expanding applications in respiratory infections, pregnancy testing, glucose monitoring, and infectious disease screening boosting market penetration

-

Continuous advancements in lateral flow assays, immunoassay technologies, and portable diagnostic platforms improving test accuracy, speed, and accessibility

The U.S. Rapid Medical Diagnostic Kits Market Outlook

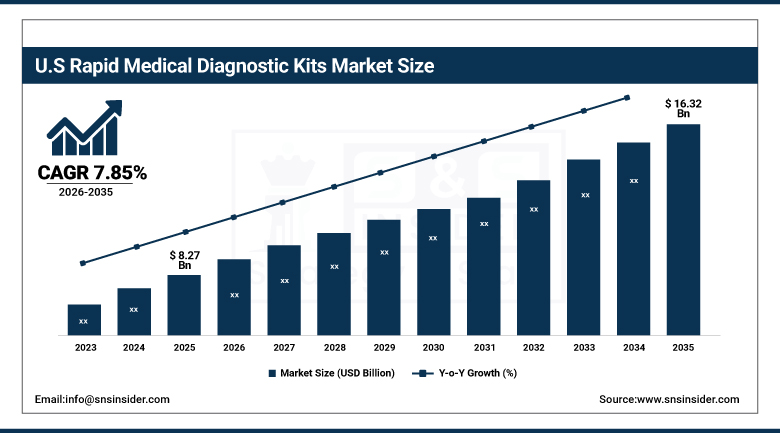

The U.S. Rapid Medical Diagnostic Kits Market was valued at approximately USD 8.27 Billion in 2025 and is expected to reach approximately USD 16.32 Billion by 2035, growing at a CAGR of approximately 7.85%.

The United States rapid medical diagnostic kits market is supported by the strong demand for digital glucose monitors, COVID-19 antigen kits, influenza diagnostics, and multidisease rapid test panels that is anticipated to stay strong throughout the forecast period because of the increasing acceptance of self-testing by both consumers and practitioners in America. The US market holds the leading position in the total revenues generated in the industry because of growing demand for home testing kits and the presence of market leaders such as Abbott, Quidel, and Becton Dickinson.

The Centers for Disease Control and Prevention (CDC) reports that influenza alone causes approximately 9–41 million illnesses annually in the United States, significantly driving continuous demand for rapid antigen testing and respiratory diagnostic kits.

Rapid Medical Diagnostic Kits Market Segmentation Analysis

-

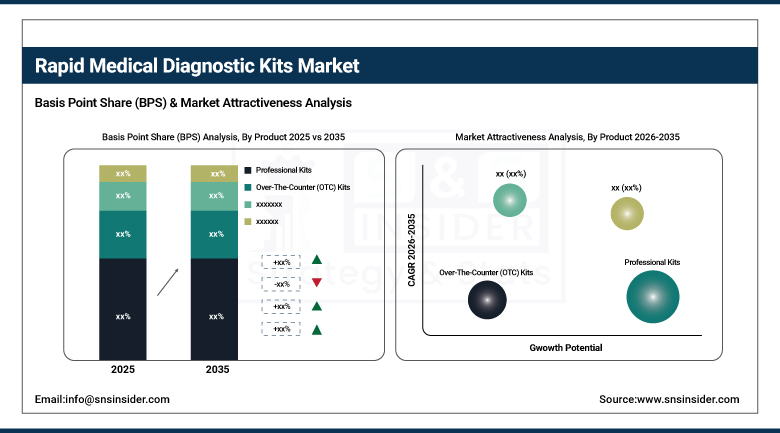

By Product, professional kits segment dominated the Rapid Medical Diagnostic Kits Market in 2025 with 58% share; over-the-counter (OTC) kits segment is the fastest growing segment.

-

By Technology, lateral flow segment dominated the market in 2025 with 63% share; solid phase segment is the fastest growing segment.

-

By Application, infectious disease testing segment dominated the market in 2025 with 41% share; toxicology testing segment is the fastest growing segment.

-

By End-use, diagnostic laboratories segment dominated the market in 2025 with 46% share; home care segment is the fastest growing segment.

By Product, Professional Kits segment dominates the Rapid Medical Diagnostic Kits Market, OTC Kits segment expected to grow fastest

The professional kits segment dominated the Rapid Medical Diagnostic Kits Market because of their wide use in hospitals, clinics, and diagnostic laboratories where accuracy and compliance are vital. Professional kits are intended for professionals who require high sensitivity, standardization, and accuracy for disease diagnosis. The growth of the number of patients who need testing, the spread of infectious diseases, and preference for clinically approved diagnostic kits contributed to the domination of this segment in the market.

The OTC kits segment is the fastest growing in the Rapid Medical Diagnostic Kits Market because of the growing needs of consumers for convenient self-testing products. The increase in the awareness of the importance of early diagnosis, the availability of diagnostic kits, and the preference for home-based health care contributed to the popularity of this segment. The deep penetration of e-commerce, affordability of products, and attention to prevention are contributing factors to the fast development of OTC diagnostics globally.

By Technology, Lateral Flow segment dominates the Rapid Medical Diagnostic Kits Market, Solid Phase segment expected to grow fastest

The lateral flow segment dominated the Rapid Medical Diagnostic Kits Market owing to its simplicity, fast results, and low cost, thus making it suitable for point-of-care diagnostics. This segment is used in screening for infectious diseases, pregnancy tests, and others. The easy-to-use nature without the need of any complex lab equipment, high penetration rate among health care facilities, and constant technological developments have been contributing factors towards its dominance in the diagnostic market.

The solid phase segment is the fastest growing in the Rapid Medical Diagnostic Kits Market owing to its enhanced analytical performance and sensitivity, in addition to increased adoption of this segment in advanced diagnostics. Rising demand for highly accurate testing techniques, including toxicology, infections, and biomarker detection, is expected to fuel the growth of this market segment.

By Application, Infectious Disease Testing segment dominates the Rapid Medical Diagnostic Kits Market, Toxicology Testing segment expected to grow fastest

The infectious disease testing segment dominated the Rapid Medical Diagnostic Kits Market owing to the high incidence of diseases such as influenza, COVID-19, HIV, and hepatitis across the globe. It is essential for early detection, timely diagnosis, and proper management of such diseases. Widespread use in hospitals, clinics, and emergency centers, coupled with rising demands, contributed to its dominance in the market.

The toxicology testing segment is the fastest growing in the Rapid Medical Diagnostic Kits Market due to Increasing concerns regarding substance abuse, health risks at workplaces, and chemical hazards are some of the factors contributing to this rise in demand. Increasing demand in forensic testing, workplace and emergency tests, and advancements in rapid testing technology have played a significant role in boosting the growth of this segment.

By End-use, Diagnostic Laboratories segment dominates the Rapid Medical Diagnostic Kits Market, Home Care segment expected to grow fastes

The diagnostic laboratories segment dominated the Rapid Medical Diagnostic Kits Market owing to their high testing capacity, advanced infrastructure, and skilled labor that can deal with huge amounts of diagnostic samples. They act as major centers for disease detection and confirmatory diagnosis. High incidences of infections, increased need for diagnostics, and expansion of lab networks are further helping the segment to strengthen its dominance in the market.

The home care segment is the fastest growing in the Rapid Medical Diagnostic Kits Market owing to the increased inclination of people towards self-diagnosis and testing at home. Increased awareness about preventive health care and ease of use of diagnostic kits have increased the popularity of this segment. Its integration with digital health services has led to faster growth in this segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Rapid Medical Diagnostic Kits Market Insights

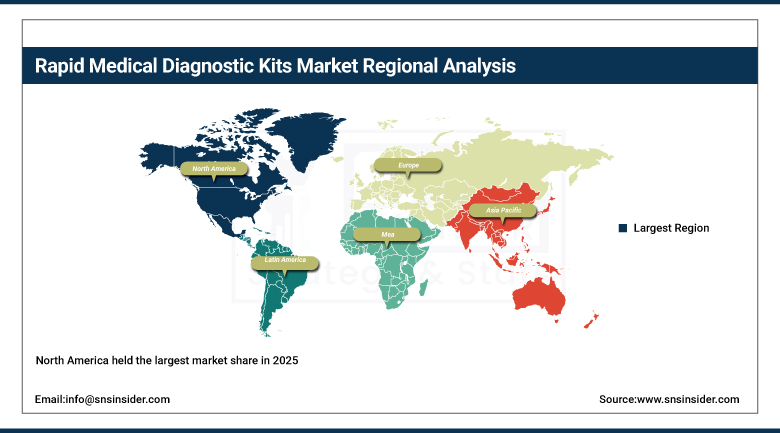

North America held the largest market share in 2023, supported by advanced healthcare infrastructure, strong OTC adoption, and powerful industry presence from Abbott, Becton Dickinson, Quidel, and other established rapid diagnostic kit manufacturers. North America dominated the global market with a 37% share in 2024, with this dominance attributable to the high prevalence of chronic diseases, particularly diabetes, combined with increasing healthcare industry awareness and growing patient demand for convenient diagnostic solutions.

The United States accounts for approximately 82.47% of regional revenue through its extensive home testing infrastructure, strong FDA regulatory framework that has accelerated rapid diagnostic test commercialisation, and the world's most extensive over-the-counter retail distribution network for consumer diagnostic products.

Furthermore, during the COVID-19 pandemic, the CDC documented the large-scale distribution of hundreds of millions of rapid antigen tests across the country, which substantially accelerated the adoption of home-based and point-of-care diagnostic solutions. This widespread utilization of rapid testing technologies has further strengthened the acceptance and integration of lateral flow-based diagnostics in both clinical and decentralized healthcare settings.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Rapid Medical Diagnostic Kits Market Insights

Europe held a significant share of global Rapid Medical Diagnostic Kits revenues, demonstrating a robust market while maintaining a slightly lower growth rate compared to Asia-Pacific, indicating steady but measured adoption of rapid diagnostic kits across the region. Germany accounts for approximately 28.47% of European revenues through its large pharmaceutical and healthcare industry infrastructure, comprehensive public health insurance coverage that supports rapid diagnostic test reimbursement, and stringent regulatory environment under the EU's In Vitro Diagnostic Regulation whose compliance requirements favour established manufacturers with proven product quality and clinical validation track records.

The European Centre for Disease Prevention and Control (ECDC) reports that influenza results in millions of infections annually across Europe, necessitating structured seasonal surveillance and widespread deployment of rapid testing strategies to monitor disease spread and support timely public health interventions.

Asia Pacific Rapid Medical Diagnostic Kits Market Insights

Asia Pacific is the fastest-growing regional Rapid Medical Diagnostic Kits market, with the region exhibiting a proactive approach toward adopting rapid diagnostic solutions, driven by growing healthcare infrastructure and increasing awareness of early diagnosis benefits across China, India, and Japan. Countries across the region are at the forefront of this growth, with a surge in digital health solutions and affordable diagnostic kits whose accessibility is expanding rapid diagnostic testing penetration across both urban and rural healthcare delivery settings.

China accounts for approximately 38.47% of Asia Pacific revenues through its expanding domestic manufacturing capability and growing healthcare infrastructure investment, with key regional players introducing recent medical testing kits to provide comprehensive rapid diagnosis services across the rapidly expanding Asian healthcare market.

MEA & Latin America Rapid Medical Diagnostic Kits Market Insights

Middle East and Latin America are growing Rapid Medical Diagnostic Kits markets where rising awareness of point-of-care diagnostics, increasing chronic disease prevalence, and favourable government support are creating expanding commercial demand. The Middle East and Africa region is expected to grow at a considerable CAGR as people across MEA countries become more aware of point-of-care diagnostics and rapid molecular diagnostic kits for accurate chronic disease diagnosis, with the UAE leading MEA revenues at approximately 22.84% of the regional total through its growing rapid test manufacturing capability and expanding chronic disease patient population.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large public hospital network and growing point-of-care diagnostics adoption across both clinical and home care settings.

The World Health Organization (WHO) reports that Africa accounts for over 90% of global malaria cases, highlighting the region’s disproportionate disease burden and the critical need for effective diagnostic solutions. This

Drivers: Rising chronic and infectious diseases and demand for home testing drive market growth.

The consistent growth of the medical diagnostic kits market comes from the fact that there is a structural basis in which there is a convergence between the global increase in the burden of infectious and chronic diseases, which need rapid diagnoses, and the behavioral change towards decentralized and self-administered tests that have become convenient enough to meet preferences and cost-effectiveness in the health system.

The rising need for rapid diagnosis in clinical and domestic situations constitutes one of the most powerful driving factors of the market, since the increase in the incidence of infectious and chronic diseases such as diabetes, cardiovascular diseases and respiratory infections creates a recurring testing need that, in its scale – with over 537 million adults having diabetes worldwide – generates revenue growth through consumables independent of economic cycles due to its health necessity.

Restraints: Strict regulations and performance variability delay product approvals and market entry timelines.

The strict regulatory process that requires the FDA, CE, and WHO approval processes for novel rapid diagnostic kit technologies means that there is considerable delay in their commercialization because the validation process, manufacturing standards, and post-market monitoring process required takes quite a bit of time and money to be completed. Performance inconsistencies among various rapid diagnostic kits that might have different levels of sensitivity and specificity among themselves even when they belong to the same class of products mean that it is difficult for physicians and patients to choose the right products, and on some occasions, the inconsistent performance of certain products may draw the attention of regulatory agencies, negatively affecting the whole industry.

Opportunities: AI diagnostics and biosensor innovations create major opportunities for rapid test manufacturers.

The development of diagnostic technologies that utilize AI and biosensors improves the accuracy of tests and increases their availability. It means that the implementation of this technology trend in the commercialization process of rapid diagnostic kits brings new opportunities to increase the efficiency of these kits, which was previously limited by qualitative results obtained from tests. In addition, the growing adoption of point-of-care testing in the healthcare sector due to the integration of this practice into different fields of medicine and its increased adoption by healthcare professionals who implement rapid diagnostic kits in their practice is likely to be a driving force for market growth.

The expansion of the ecosystem of connected health, which includes the integration of results of rapid diagnostic kits into the EHRs and remote patient monitoring systems, can serve as a strong business opportunity for manufacturers of such kits.

Recent Developments:

-

2024: PodTech collaborated with a medical device manufacturing company to build a state-of-the-art rapid test manufacturing facility in the UAE, enabling enhanced healthcare access and technological advancement integration across the Middle East and Africa region.

-

2023: Quidel Corporation received FDA approval for its Sofia COVID-19 Antigen Home Test, a self-administered rapid diagnostic test designed for convenient at-home use, expanding consumer access to reliable FDA-validated diagnostic testing.

-

2023: Abbott Laboratories launched its BinaxNOW COVID-19 Ag Card rapid point-of-care test, providing results in as little as 15 minutes and strengthening Abbott's comprehensive rapid diagnostic testing portfolio across infectious disease applications.

Rapid Medical Diagnostic Kits Market Key Players are:

-

Danaher Corporation

-

Becton, Dickinson and Company (BD)

-

Thermo Fisher Scientific Inc.

-

bioMérieux SA

-

QuidelOrtho Corporation

-

Hologic, Inc.

-

Qiagen N.V.

-

Sysmex Corporation

-

Chembio Diagnostics, Inc.

-

ACON Laboratories, Inc.

-

SD Biosensor, Inc.

-

Access Bio, Inc.

-

OraSure Technologies, Inc.

-

Trinity Biotech plc

-

Medline Industries, LP

-

PerkinElmer Inc.

-

Luminex Corporation

Rapid Medical Diagnostic Kits Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.11 Billion |

| Market Size by 2035 | USD 28.11 Billion |

| CAGR | CAGR of 9.06% from 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Over-The-Counter (OTC) Kits, Professional Kits) • By Technology (Lateral Flow, Agglutination, Solid Phase, Other Technologies) • By Application (Blood Glucose Testing, Infectious Disease Testing, Cardiometabolic Testing, Pregnancy and Fertility Testing, Fecal Occult Blood Testing, Coagulation Testing, Toxicology Testing, Lipid Profile Testing, Other Applications) • By End-use (Hospitals & Clinics, Home Care, Diagnostic Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Danaher Corporation, Becton, Dickinson and Company (BD), Thermo Fisher Scientific Inc., bioMérieux SA, QuidelOrtho Corporation, Hologic, Inc., Qiagen N.V., Sysmex Corporation, Chembio Diagnostics, Inc., ACON Laboratories, Inc., SD Biosensor, Inc., Access Bio, Inc., OraSure Technologies, Inc., Trinity Biotech plc, Medline Industries, LP, PerkinElmer Inc., Luminex Corporation |

Frequently Asked Questions

The Rapid Medical Diagnostic Kits Market was valued at USD 28.11 Billion in 2025.

Increasing diseases, rising home testing demand, AI diagnostics, biosensor advances, decentralised healthcare, and faster regulations drive rapid diagnostic kit market growth.

The OTC rapid diagnostic kits segment dominated the Rapid Medical Diagnostic Kits Market.

Get in Touch