Protein Chip Market Report Scope & Overview:

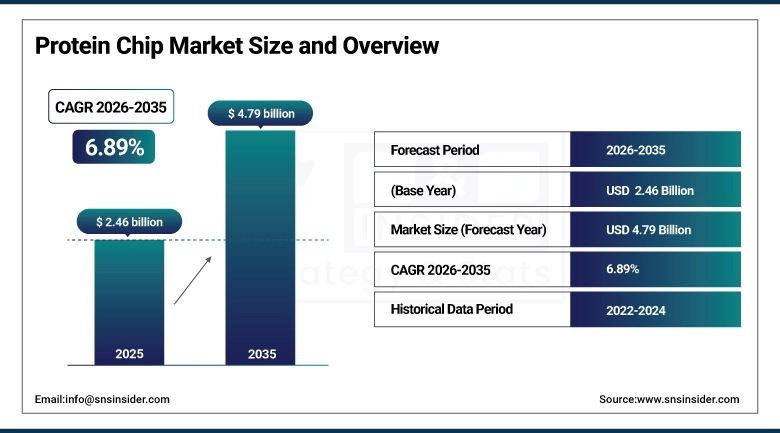

The Protein Chip Market size was valued at USD 2.46 billion in 2025 and is expected to reach USD 4.79 billion by 2035, growing at a CAGR of 6.89% over the forecast period 2026-2035.

The worldwide protein chip market exhibits stable and healthy growth, fueled by the rapid adoption of mass-screening proteomics technologies, sustained investment in marker discovery programs, and increased utilization of protein microarray platforms in clinical diagnostics and pharmaceutical drug development pipelines. Also known as protein microarrays, protein chips allow characterization of thousands of proteins in a single experiment, and are thus key instruments in protein research, antibody characterization and functional proteomics, biomarker profiling, or disease prediction, for example. Growing focus of precision medicine, increasing translational research activities, and wide use of reverse phase protein micro arrays in oncology and immunology, and other research areas are continuously establishing a strong commercial base for this market. Improvements in surface chemistry, signal detection technologies, and multiplexed assay design continue to increase assay sensitivity, specificity and throughput and widespread implementation of these assays across academic research institutes, pharmaceutical companies, diagnostic laboratories and hospital settings worldwide has been facilitated as a result.

For instance, in April 2024, the National Institutes of Health (NIH) reported a 17.3% year-over-year increase in proteomics-related research grant funding, with protein microarray platforms cited in over 34% of newly funded protein interaction and biomarker validation studies, reflecting the expanding role of protein chip technologies in federally supported life science research in the United States.

Protein Chip Market Size and Forecast:

-

Market Size in 2025: USD 2.46 billion

-

Market Size by 2035: USD 4.79 billion

-

CAGR: 6.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Protein Chip Market - Request Free Sample Report

Protein Chip Market Trends

-

Growing adoption of functional protein microarrays in drug target identification and protein-protein interaction studies is expanding application scope within pharmaceutical and biotechnology research pipelines globally.

-

The integration of artificial intelligence and machine learning algorithms with protein chip data analysis platforms is accelerating biomarker discovery timelines and improving the clinical translatability of proteomics findings.

-

Miniaturization of protein microarray platforms and advances in nano-fabrication technologies are enabling point-of-care diagnostic applications, reducing assay turnaround times and improving accessibility in resource-limited clinical settings.

-

Increasing utilization of reverse phase protein microarrays (RPPA) in oncology research for tumor pathway profiling, treatment response monitoring, and companion diagnostic development is generating significant commercial demand from cancer research centers.

-

Expansion of autoimmune disease diagnostics using analytical microarrays for autoantibody profiling is driving adoption across hospital-based clinical immunology laboratories and specialty diagnostic networks.

-

Growing strategic collaborations between protein chip technology developers, contract research organizations (CROs), and pharmaceutical companies are accelerating the commercialization of next-generation multiplexed protein detection platforms.

-

Rising demand for label-free detection technologies, including surface plasmon resonance-integrated protein chips, is improving quantitative protein interaction analysis capabilities and displacing traditional fluorescence-based detection formats in research settings.

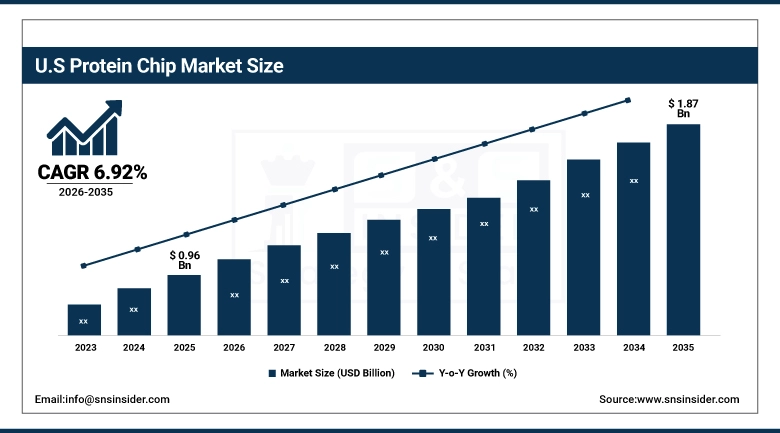

The U.S. Protein Chip Market was valued at USD 0.96 billion in 2025 and is expected to reach USD 1.87 billion by 2035, growing at a CAGR of 6.92% from 2026-2035. As a result of world-class academic and research infrastructure, the most concentrated density of pharmaceutical and biotechnological companies, and continuous federal support of proteomic and precision medicine research through NIH, NCI, or DARPA efforts, the United States represents the largest national protein chips market worldwide. The continued adoption of protein microarray platforms within the top research institutions in the United States including the National Cancer Institute's Clinical Proteomic Tumor Analysis Consortium (CPTAC) mapped with strong private sector R&D investment with antibody based therapeutics and companion diagnostics will continue to strengthen U.S. market leadership throughout the forecast period.

Protein Chip Market Growth Drivers:

-

Expanding Proteomics Research and Biomarker Discovery Investments are Driving the Protein Chip Market Growth

The increasing global investment in proteomics research, biomarker discovery programs, and precision oncology initiatives is the largest structural growth driver for protein chip market. Unlike traditional technologies, including Western blotting and enzyme-linked immunosorbent assays (ELISA), protein microarray platforms allow for the simultaneous characterization of thousands of protein interactions, post-translational modifications and disease-associated expression patterns in a single experimental workflow, thus give it unparalleled throughput advantages. The increase in companion diagnostics demand, integration of liquid biopsy with drug development pipelines, and generation of multi-omic data across TRP and medicinal oncology will directly increase procurement of high-density protein chip systems between CROs, academic medical centers, and biopharmaceutical manufacturers worldwide.

For instance, in August 2024, the global proteomics research market surpassed USD 31.4 billion in total funding disbursements, with protein microarray-based platforms accounting for an estimated 8.2% of total proteomics technology procurement spending, underscoring the growing commercial significance of protein chip solutions in large-scale research and clinical programs.

Protein Chip Market Restraints:

-

High Instrument Costs and Technical Complexity of Protein Microarray Workflows are Hampering the Protein Chip Market Growth

However, the high capital costs of protein chip instrumentation, specialized surface chemistry consumables, and complex data analysis software are a significant barrier to adoption, especially for small to mid-sized research institutions in developing regions. Due to technical complexities in protein microarray experimental design (such as those related to protein stability, cross-reactivity, surface immobilization efficiency, and assay reproducibility), the need for specialized personnel and stringent quality-control measures makes protein microarrays too technologically demanding for the majority of resource-constrained laboratories to maintain. These hurdles coupled with the lower degree of standardization of protein chip platforms across vendors, lead to adoption reluctance of potential end users in Asia Pacific, Latin America and the Middle East which restrict global market penetration to levels below the theoretical full growth potential.

Protein Chip Market Opportunities:

-

Growing Clinical Diagnostics Applications and Point-of-Care Integration Create Significant Growth Opportunities for the Protein Chip Market

This commercial opportunity of protein chip market is transformed from existing pure researchoriented platforms of locally used protein microarray technologies to clinically validated bio-microarray based diagnostic applications. Increases in the use of multiplexed autoantibody arrays in diagnostics for autoimmune disease, infectious disease serology, and early cancer detection are widening the clinical market served to more than just traditional research and pharmaceutical end-use segments. Recently, miniaturized protein chip formats integrated with microfluidics and compatible with point-of-care testing conditions are making great progress and potentials for emergency care, primary care, and low-resource clinical settings to achieve rapid multi-analyte detection. Moreover, increasing regulatory approvals of protein microarray-based in vitro diagnostic devices by FDA and CE mark programs in Europe are lowering commercialization barriers to diagnostic applications and fostering revenue growth in the clinical segment.

For instance, in November 2024, the FDA cleared a next-generation multiplexed protein microarray system for clinical autoimmune disease diagnostics capable of simultaneously detecting 22 disease-specific autoantibodies from a single patient blood sample, representing a significant regulatory milestone for the commercial expansion of protein chip platforms into the U.S. clinical diagnostics market.

Protein Chip Market Segment Analysis

-

By type, analytical microarrays held the largest share of approximately 42.18% in 2025, while the reverse phase protein microarrays segment is expected to register the highest CAGR of 8.14% through 2035.

-

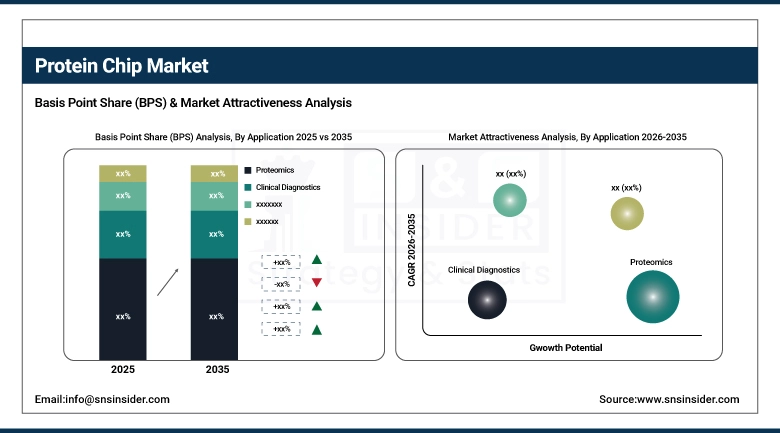

By application, proteomics accounted for the dominant share of approximately 34.76% in 2025, while clinical diagnostics is expected to register the highest CAGR of 8.42% over the forecast period.

-

By end-use, pharmaceutical and biotechnology companies held the leading share of approximately 37.93% in 2025, while diagnostic laboratories are expected to register the highest CAGR of 8.97% through 2035.

By Type, Analytical Microarrays Lead the Market, While Reverse Phase Protein Microarrays Register Fastest Growth

In 2025, analytical microarrays held the largest revenue share, nearly 42.18%, due to their established use for antibody profiling, protein expression analysis, and clinical biomarker validation, along with high adoption among pharmaceutical drug discovery, academic proteomics research, and immunology laboratories. Thirdly, the revenue leadership of this segment is facilitated by standardization of analytical microarray reagent kits and availability of mature detection platforms. In 2025, the second largest share, about 37.64% was functional protein microarrays owing to the bolstering demand for protein-protein interaction mapping and enzyme substrate profiling in the biopharma development. During 2026-2035, the highest CAGR ~ 8.14% is anticipated to be achieved by the reverse phase protein microarray segment propelled by accelerating clinical uptake in oncology tissue profiling, increased integration of RPPA platforms into clinical trial biomarker programs, and the unique capability of RPPA platforms to characterize signaling pathway activation states in tumor samples with high sensitivity and minimal sample input requirements.

By Application, Proteomics Leads the Market, While Clinical Diagnostics Registers Fastest Growth

The proteomics segment accounted for the largest revenue share of around 34.76% in 2025, driven by the essential function of protein microarrays as enabling technologies for high-throughput protein expression profiling, post-translational modification analysis, and protein interaction network characterization in both academic and pharmaceutical research organizations. The share of antibody characterization remained constant over around 27.43% in 2025, owing to demand monoclonal antibody developers and biosimilar manufacturers for high-throughput epitope mapping and cross-reactivity assessment solutions. The clinical diagnostics segment is estimated to be the fastest growing segment with a 8.42 % CAGR during the period 2026-2035 owing to increase regulatory approvals for microarray-based devices for diagnosis, growing demand for multiplex serological testing for autoimmune and infectious disease diagnostics and increasing commercial opportunity for protein chip integration with next-generation clinical laboratory information management systems.

By End-Use, Pharmaceutical and Biotechnology Companies Lead, While Diagnostic Laboratories Register Fastest Growth

The largest end-use share was 37.93% for pharmaceutical and biotechnology companies in 2025, characterized by high institutional investment in the protein microarray platform (target identification, antibody drug candidate screening, off-target binding profiling, and biomarker-driven patient stratification during clinical. The second-largest share was held by academic and research institutes around 28.64% as a result of continued public research funding and the organic importance of protein chips in fundamental proteomics and systems biology research. The fastest growing segment, in terms of revenue, is diagnostic laboratories and is anticipated to reach a CAGR of nearly 8.97% till 2035, as a result of the continual movement of validated protein microarray assays into accredited clinical laboratory workflows, mounting demand for multiplexed immunoassay testing panels and increased reimbursement coverage for a range of protein chip-based diagnostic applications in key North American and European markets. In 2025, hospitals and clinics accounted for 20.17% of revenue share in terms of end use, (incremental growth of which will be driven by increasing adoption of bedside and rapid diagnostic applications.

Protein Chip Market Regional Highlights:

Asia Pacific Protein Chip Market Insights:

Protein Chip Market in Asia Pacific projected to reach USD 8.30 billion USD million in market value growing at quickest growth rate of 9.12% over the forecast period, owing to growing pharmaceutical and biotechnology manufacturing sector in China, India, Japan, South Korea, increasing government investments in proteomics and genomics infrastructures, increasing investments in R&D of proteomics, domestic demand for sophisticated diagnostic and research tools, growing domestic economy with rapid results and change, and upgrading lives of citizens in the region. The China National Precision Medicine Initiative and the rapidly growing CRO industry in India are driving an ever increasing purchase of protein microarray platforms from both domestic and global technology providers. Regional gain from Korea and Japan are driven by mature capabilities in both semiconductor and bio-nanotechnology which are being increasingly integrated for next-generation protein chip manufacturing processes. Meanwhile, the regional protein chip end-user base will continue to widen with the improvement in scientific talent pipelines, heightened growth of university-industry research partnerships and the development of clinical research organisation networks throughout Southeast Asia.

North America Protein Chip Market Insights:

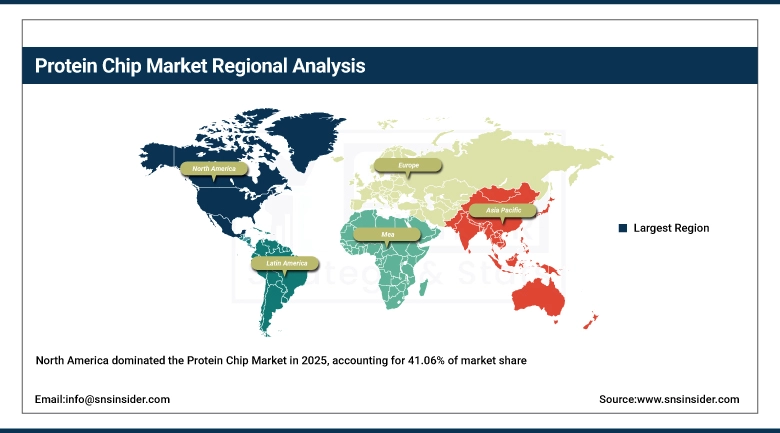

Protein Chip Market Revenue by Region, 2022 - 2025 (USD Million) North America accounted for the largest revenue share of 41.06% in 2025 of the protein chip market, due to the unprecedented presence of top protein microarray technology developers coupled with the largest cluster of pharmaceutical and biotechnology industries of the globe and favorable public and private funding environment for proteomics research programs in the region of USD 165 million. US leadership in regional market via NIH-funded research initiatives, FDA regulatory pathways supporting clinical protein microarray diagnostics, and significant commercial demand from antibody drug manufacturers for protein microarray-based assays and precision oncology programs. Canada does so at the margin through its developing biomedical research ecosystem and collaborative proteomics initiatives in partnership with U.S.-based academic medical centers and pharmaceutical partners.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Protein Chip Market Insights:

Europe accounts for a major share of the global protein chips market sales, making it the second-largest regional market. The key factors attributing for this stimulation such as the strong academic tradition in proteomics research, significant Horizon Europe-based funding supporting life science technology development and clinical integration of protein microarray diagnostics for the management of autoimmune disease and oncology contribute to a revenue share of 26.84% in 2025. Germany, the U.K., France and Switzerland comprise the top European markets all with active protein chip technology development ecosystems and high adoption rates in national cancer research programs. The updated IVDR framework is resulting in increased regulatory support for multiplex in vitro diagnostic platforms at a European-wide level, which is gradually broadening the clinical market for protein chip-based diagnostic systems.

Latin America (LATAM) and Middle East & Africa (MEA) Protein Chip Market Insights:

In areas such as Latin America and the Middle East & Africa, the increase public and private investment in biomedical research infrastructure, rise in pharmaceutical manufacturing capacity, and improved access to high-end laboratory instrumentation set the scene for emerging demand protein chip technologies. Brazil and Mexico dominate the LATAM market, buoyed by growing domestic biotechnology industries as well as academics partnering with North American and European institutions. Protein Microarray Technologies to MEA Region – Saudi Arabia, UAE, and Israel are leading Markets for Protein Microarray Technologies in MEA Region; Aligned with Growing National Life Science Development Programs, Clinical Research Capacity, and Diagnostic Laboratory Networks Expanding in Major Urban Healthcare Centers

Protein Chip Market Competitive Landscape:

Thermo Fisher Scientific Inc. (est. 1956) is a global leader in life science tools, analytical instruments, and laboratory reagents with a comprehensive protein microarray product portfolio spanning analytical, functional, and clinical diagnostic applications. The company leverages its extensive distribution network, integrated bioinformatics solutions, and broad antibody and protein reagent catalog to maintain a leading commercial position across pharmaceutical, academic, and clinical laboratory end-use segments.

-

In February 2025, Thermo Fisher Scientific launched an expanded ProtoArray Human Protein Microarray platform featuring over 9,400 unique human proteins with enhanced surface chemistry for improved signal-to-noise performance, targeting pharmaceutical antibody characterization and autoimmune biomarker discovery applications across global research customers.

Agilent Technologies, Inc. (est. 1999) is a leading analytical instrumentation and life science solutions provider with specialized expertise in microarray platform development, including protein chip design, surface functionalization, and associated bioinformatics software. Agilent's SurePrint and Proteome Profiler arrays are widely adopted across academic research institutes and pharmaceutical companies for multiplex protein expression profiling and signaling pathway analysis.

-

In June 2024, Agilent Technologies announced a strategic partnership with a leading U.S. oncology research consortium to deploy reverse phase protein microarray platforms across 12 NCI-designated cancer centers, supporting large-scale tumor proteome characterization and biomarker validation studies within the consortium's precision oncology program.

Bio-Rad Laboratories, Inc. (est. 1952) is a diversified life science research and clinical diagnostics company with a strong presence in protein analysis technologies, including multiplex immunoassay and protein microarray platforms. Bio-Rad's Bio-Plex and protein interaction array systems serve a broad customer base across pharmaceutical drug development, academic proteomics research, and clinical immunology laboratory applications globally.

-

In October 2024, Bio-Rad Laboratories introduced an upgraded Bio-Plex Pro protein array system with expanded 48-plex cytokine detection capabilities and integrated cloud-based data analysis tools, strengthening its competitive position in multiplex protein profiling for immunology research and clinical biomarker studies.

Protein Chip Market Key Players:

-

Thermo Fisher Scientific Inc.

-

Agilent Technologies, Inc.

-

Bio-Rad Laboratories, Inc.

-

Illumina, Inc.

-

Merck KGaA (MilliporeSigma)

-

Cytiva (formerly GE Healthcare Life Sciences)

-

Full Moon BioSystems, Inc.

-

RayBiotech Life, Inc.

-

Luminex Corporation (DiaSorin Company)

-

Sengenics Corporation

-

Proteagen AG

-

Randox Laboratories Ltd.

-

Bruker Corporation

-

Revvity, Inc. (formerly PerkinElmer)

-

Creative Biolabs

-

Abnova Corporation

-

Grace Bio-Labs, Inc.

-

Quanterix Corporation

-

Arrayit Corporation

-

Microarrays Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.46 Billion |

| Market Size by 2035 | USD 4.79 Billion |

| CAGR | CAGR of 6.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type [Analytical Microarrays, Functional Protein Microarrays, Reverse Phase Protein Microarrays] • By Application [Antibody Characterization, Clinical Diagnostics, Proteomics, Others] • By End-use [Hospitals & Clinics, Diagnostic Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific Inc., Agilent Technologies Inc., Bio-Rad Laboratories Inc., Illumina Inc., Merck KGaA, Cytiva, Full Moon BioSystems Inc., RayBiotech Life Inc., Luminex Corporation, Sengenics Corporation, Proteagen AG, Randox Laboratories Ltd., Bruker Corporation, Revvity Inc., Creative Biolabs, Abnova Corporation, Grace Bio-Labs Inc., Quanterix Corporation, Arrayit Corporation, Microarrays Inc. |

Frequently Asked Questions

The Protein Chip Market is driven by increasing adoption of proteomics technologies, rising biomarker discovery research, and growing use of protein microarrays in clinical diagnostics and drug development.

The Protein Chip Market is expected to reach USD 4.79 billion by 2035, growing from USD 2.46 billion in 2025.

Key applications in the Protein Chip Market include proteomics research, clinical diagnostics, antibody characterization, and drug discovery.

North America dominates the Protein Chip Market due to strong research infrastructure, high R&D investment, and widespread adoption of protein microarray technologies.

The Protein Chip Market is projected to grow at a CAGR of 6.89% from 2026 to 2035.

Get in Touch