Rapid Prototyping Materials Market Report Scope & Overview:

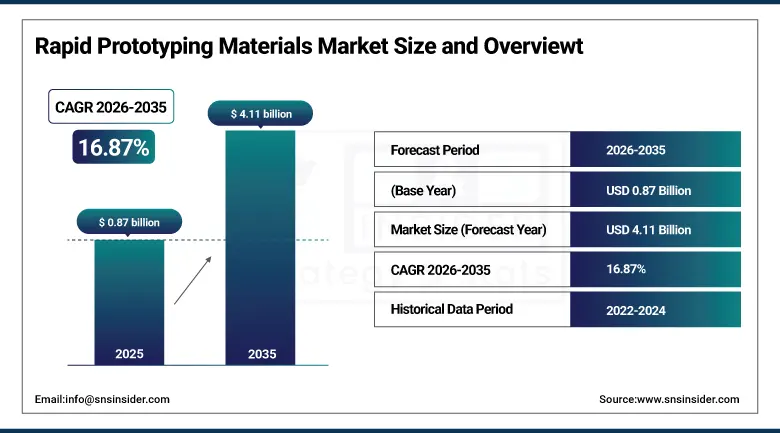

The Rapid Prototyping Materials Market was valued at USD 0.87 Billion in 2025 and is expected to reach USD 4.11 Billion by 2035, growing at a CAGR of 16.87% from 2026 to 2035.

The market for rapid prototyping materials has emerged as arguably one of the most commercially vital and technologically significant markets within the advanced manufacturing and additive manufacturing industry on a global level, playing an instrumental role in revolutionizing product development through the emergence of a paradigm shift in which product development teams from various industries including aerospace, automotive, medical devices, consumer electronics, and industrial machinery are increasingly using additive manufacturing technologies to develop prototypes, design verification models, and even tools at significantly reduced timeframes and costs.

Over 68% of industrial prototyping workflows globally now rely on additive manufacturing materials (photopolymers, thermoplastics, and metal powders) rather than traditional subtractive prototyping methods, reflecting a structural shift toward digital manufacturing and rapid iteration cycles across product development ecosystems.

Market Size and Forecast

-

Market Size in 2026E: USD 1.010 Billion

-

Market Size by 2035: USD 4.11 Billion

-

CAGR: 16.87% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Rapid Prototyping Materials Market - Request Free Sample Report

Rapid Prototyping Materials Market Trends

-

Rising use of high-performance photopolymer resins is expanding stereolithography into functional and end-use prototyping applications.

-

Demand for biocompatible and medical-grade materials is accelerating adoption in healthcare, dental, and surgical planning applications.

-

Development of advanced metal powders is enabling direct metal prototyping for aerospace and automotive components.

-

Growth of multi-material and composite printing is reducing the need for multi-step assembly in prototyping workflows.

-

AI-driven process optimization is improving material efficiency and first-build success rates across key prototyping technologies.

The U.S. Rapid Prototyping Materials Market Outlook

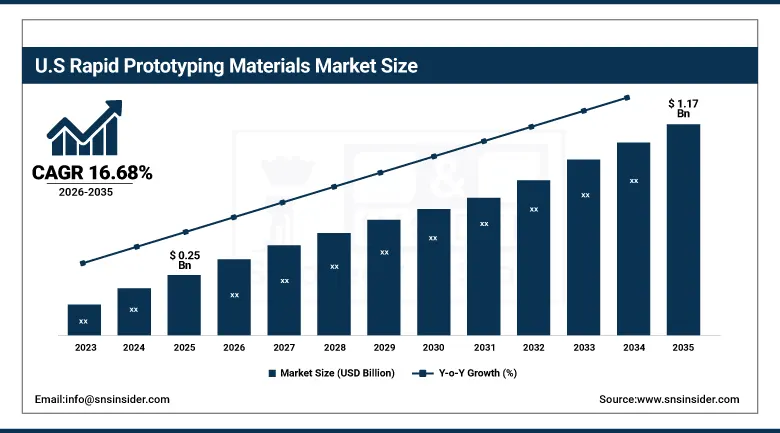

The U.S. Rapid Prototyping Materials Market was valued at USD 0.25 Billion in 2025 and is expected to reach USD 1.17 Billion by 2035, growing at a CAGR of 16.68%.

The U.S. is home to the largest national market for rapid prototyping materials in the world, considering that the country has an unprecedented number of industries such as advanced manufacturing, aerospace and defense, medical devices, and consumer electronics. These industries have programs for developing and qualifying products using functional prototyping materials, creating a global record for highest demand in each sector. The demand for rapid prototyping materials in the U.S. is driven by the high number of additive manufacturing companies like 3D Systems, Stratasys, EOS, and Carbon operating in the country. These companies have research centers and applications in the country, creating a massive base of consumption in North America.

Stratasys Ltd. expanded its FDM Nylon 12CF carbon fiber thermoplastic material in 2025 for aerospace structural prototyping, enabling lightweight, high-strength prototype components with production-like performance at lower costs.

Rapid Prototyping Materials Market Segment Analysis

-

By Material Type, photopolymer resins dominated the market with 32.45% share in 2025, while metal powders are the fastest growing material type with the highest CAGR of 17.88% during 2026 to 2035.

-

By Technology, stereolithography (SLA) dominated the market with 30.29% share in 2025, while fused deposition modeling is the fastest growing technology with the highest CAGR of 17.61% during 2026 to 2035.

-

By Form, powder dominated the market with 38.45% share in 2025, while powder also represents the fastest growing form category with the highest CAGR of 17.37% during 2026 to 2035.

-

By Application, concept modeling dominated the market with 34.15% share in 2025, while tooling & manufacturing aids is the fastest growing application with the highest CAGR of 19.33% during 2026 to 2035.

By Material Type, photopolymer resins dominate the rapid prototyping materials market, while metal powders are the fastest-growing segment.

Photopolymer resins segment dominated the market with the highest revenue share of 32.45% in 2025. Due to the widespread commercial adoption of stereolithography and digital light processing platforms across industrial design, consumer products, jewelry, dental, and medical device sectors whose prototyping requirements prioritize surface finish quality, dimensional accuracy, and geometric complexity reproduction capabilities that photopolymer-based vat photopolymerization processes deliver with greater fidelity than competing additive manufacturing technologies at comparable or lower per-part material costs.

Metal powders segment is projected to witness the fastest growth during the forecast period of 2026–2035 driven by the accelerating industrial adoption of laser powder bed fusion and directed energy deposition platforms for producing functional metallic prototypes and near-net-shape production components in titanium, stainless steel, aluminum, nickel superalloy, and cobalt-chrome material systems whose mechanical, thermal, and corrosion resistance properties are required for aerospace structural, medical implant, oil and gas downhole, and automotive powertrain prototyping applications that cannot be addressed by polymer-based rapid prototyping alternatives.

By Technology, stereolithography (SLA) dominates the rapid prototyping materials market, while fused deposition modeling (FDM) is the fastest-growing segment.

Stereolithography (SLA) segment dominated the market with the highest revenue share of 30.29% in 2025, driven by its high-resolution output capabilities, superior surface finish quality, and strong adoption across precision-demanding industries such as industrial design, healthcare, dental modeling, jewelry manufacturing, and consumer product development, where complex geometries, fine feature reproduction, and dimensional accuracy are critical requirements best achieved through vat photopolymerization systems.

Fused Deposition Modeling (FDM) segment is projected to witness the fastest growth during the forecast period of 2026–2035, supported by its cost-effective material utilization, broad thermoplastic compatibility, low operational complexity, and increasing penetration across decentralized manufacturing environments, engineering prototyping facilities, and educational institutions, alongside growing industrial use for functional testing prototypes, fixture development, and iterative product design workflows that require rapid turnaround times and scalable production flexibility.

By Form, powder dominates the rapid prototyping materials market, while powder also leads growth driven by metal platform adoption.

The powder segment dominated the market with the highest revenue share of approximately 38.45% in 2025, supported by extensive consumption in selective laser sintering (SLS) polymer systems and laser powder bed fusion metal systems across aerospace, automotive, medical, and industrial prototyping applications, where high-performance material properties, complex geometries, and functional end-use capabilities drive strong demand for powder-based additive manufacturing processes. The dominance is further reinforced by the rapidly growing installation of metal powder-based systems, which consume significantly higher material volumes compared to polymer platforms.

The powder segment is also projected to witness the fastest growth during the forecast period of 2026–2035, driven by accelerating adoption of metal additive manufacturing technologies for functional prototyping and near-production components requiring superior strength, thermal resistance, and structural performance.

By Application, concept modeling dominates the rapid prototyping materials market, while tooling & manufacturing aids is the fastest-growing segment.

Concept modeling segment dominated the rapid prototyping materials market with the highest revenue share of approximately 34.15% in 2025 owing to the universal requirement across all product-developing industries for physical three-dimensional representations of digital design concepts at early product development stages where visual communication of form, proportion, and aesthetic intent to design review, marketing, and client audiences demands physical model production at frequencies and iteration velocities that only rapid prototyping processes can economically accommodate.

Tooling and manufacturing aids represent the fastest-growing application segment as the adoption of additive manufacturing for producing jigs, fixtures, assembly aids, inspection gauges, injection mold inserts, and end-of-arm tooling components accelerates across automotive, electronics, and consumer goods manufacturing environments where the geometric customization, lead time compression, and per-unit economics of additively manufactured tooling increasingly outperform conventional CNC-machined and injection-molded tooling alternatives, particularly for short-production-run, design-iteration-intensive, and highly customized manufacturing environments.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.54% |

|

Europe |

Germany |

26.54% |

|

Asia Pacific |

China |

37.46% |

|

Middle East & Africa |

UAE |

34.45% |

|

Latin America |

Brazil |

29.36% |

North America Rapid Prototyping Materials Market Insights

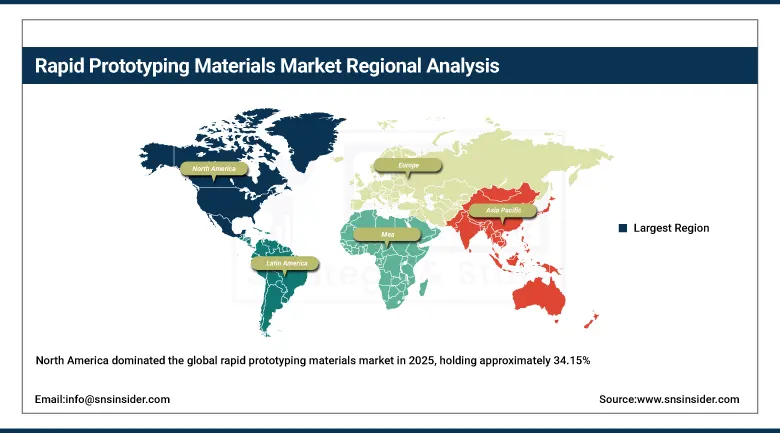

North America dominated the global rapid prototyping materials market in 2025, holding approximately 34.15% of global revenues at USD 0.300 Billion, with the United States accounting for 84.54% of regional revenue. The region's market leadership reflects the unparalleled concentration of advanced manufacturing, aerospace, defense, medical device, and consumer electronics industries whose engineering development programmed collectively generate the world's highest aggregate demand for functional prototyping materials across resin, thermoplastic, and metal powder categories. The U.S. additive manufacturing ecosystem, led by Stratasys, 3D Systems, Carbon, Desktop Metal, and Markforged, drives continuous material innovation and qualification, positioning North America as the global hub for rapid prototyping materials development and applications.

The U.S. additive manufacturing ecosystem generates more than USD 15 billion annually in combined hardware, materials, and services revenues, with materials representing a growing proportion of total ecosystem revenues as installed platform bases mature and consumable consumption per platform reaches steady-state operational levels across industrial and professional user segments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Rapid Prototyping Materials Market Insights

The revenue generated from the consumption of rapid prototyping materials within Europe. The rapid prototyping materials market within Europe constitutes one of the technically advanced regions in the entire world in terms of industrial diversity in the rapid prototyping materials market. The European market for rapid prototyping materials is highly influenced by the presence of a number of industries such as precision engineering, automotive industry, aerospace and medical devices in countries like Germany, France, the UK, Sweden and the Netherlands, which feature highly advanced engineering development programs that support the world's most rapid prototyping material consumption per industrial workforce ratio.

Europe's automotive sector, which collectively produces over 12 million vehicles annually, maintains among the world's most intensive rapid prototyping material consumption profiles per development programme, with premium OEMs including BMW, Mercedes-Benz, Volkswagen, and Stellantis operating extensive in-house additive manufacturing centers consuming hundreds of tonnes of polymer and metal prototyping materials annually across their combined vehicle development programmers.

Asia Pacific Rapid Prototyping Materials Market Insights

Asia Pacific is the fastest-growing regional rapid prototyping materials market at a CAGR of 17.32% through 2035, growing from USD 0.232 Billion in 2025 to USD 1.128 Billion by 2035. China accounts for the largest share of Asia Pacific revenues as the world's most extensive manufacturing economy whose government-driven additive manufacturing industry development policies, massive electronics and consumer goods manufacturing base, and rapidly expanding aerospace and automotive sectors are generating the world's fastest-growing aggregate demand for rapid prototyping materials across all major material type and technology categories. China’s Made in China 2025 initiative prioritizes additive manufacturing, driving strong government funding, subsidies, and domestic material development, resulting in rapid prototyping materials market growth above the global average.

China accounts for nearly 60% of Asia Pacific’s additive manufacturing material consumption, driven by strong government industrial policy support, national standardization efforts, and the rapid expansion of domestic material suppliers such as Farsoon Technologies and BLT, which are steadily replacing imported photopolymer and metal powder materials in industrial rapid prototyping applications across automotive, aerospace, electronics, and machinery sectors.

MEA & Latin America Rapid Prototyping Materials Market Insights

MEA and Latin America represent regions where rapid prototyping materials are emerging markets. This is due to the fact that countries from these regions have seen increasing demand in aerospace, oil & gas, healthcare, and manufacturing industries for additive manufacturing prototypes. MEA revenues have been led by the UAE, which accounts for roughly 30% of total MEA revenues because Dubai is recognized as a leading centre for adopting advanced manufacturing technology and the MRO segment of the aerospace industry. In addition, UAE's national target for adopting additive manufacturing technology is well established, whereby a certain percentage of new constructions and government procurements use additive manufacturing parts.

The UAE's national 3D printing strategy targets 25% of Dubai's new buildings to incorporate 3D-printed construction components by 2030, representing one of the world's most ambitious government commitments to additive manufacturing adoption and creating structural demand for large-format construction and industrial additive manufacturing material consumption alongside the conventional rapid prototyping material categories serving the region's aerospace, oil and gas, and consumer goods industries.

Market Dynamics

Growth Drivers: Industrial additive manufacturing adoption and material performance advancement

The increasing pace at which additive manufacturing gains traction in production manufacturing uses such as aerospace, automotive, medical devices, and consumer electronics has resulted in the development of a significantly larger and rapidly growing customer base for rapid prototyping materials in comparison with the limited prototyping use cases on which the market was initially based because the very same materials that have been used in prototyping are increasingly being applied for producing small quantities of end components, making tools, and even low-volume production runs. New developments in photopolymer, thermoplastic, and metal powders have helped rapid prototyping materials transition from merely prototyping to full-fledged manufacturing.

Restraints: Material cost premiums and post-processing complexity

The price premiums for rapid prototyping materials are quite high compared to the materials used in conventional molding and CNC manufacturing due to economies of scale resulting from the bulk production of petrochemical commodities. In cases where the value added by the rapid prototyping process cannot outweigh these premiums, the technology will not be affordable to use within such sectors. Additional processes associated with rapid prototyping materials including UV curing, annealing, or metal sintering increase the cost of production compared to those of conventional molding and machining processes.

Opportunities: Biomedical materials innovation and sustainable material development

The rapid prototyping materials market represents an important commercial boundary in biomedical applications where the creation of biocompatible, bioresorbable, and drug-eluting rapid prototyping material solutions for surgical implants, tissue scaffolds, customized medical devices, and drug dosage forms is generating valuable applications that have performance criteria and regulatory standards that ensure ongoing material development investments, as well as premiums on prices that far surpass those of other commodity materials used in rapid prototyping. Increasing concerns about waste, energy consumption, and emissions from both regulators and consumers are spurring interest in sustainable rapid prototyping materials.

Recent Developments:

-

2026: EOS GmbH launched its AlSi10Mg-0403 aluminum powder for laser powder bed fusion, improving elongation, fatigue resistance, and enabling die-cast–like mechanical performance for aerospace and automotive structural prototyping applications.

-

2026: Carbon Inc. introduced EPX 86 epoxy-based engineering resin for Digital Light Synthesis, designed for automotive under-hood functional prototypes with high thermal resistance up to 135°C and strong chemical resistance against fuels, oils, and lubricants.

-

2025: Stratasys Ltd. launched SAF PA11 bio-based nylon powder for Selective Absorption Fusion platforms, offering a sustainable, castor oil–derived material with PA12-equivalent mechanical strength for automotive, industrial, and consumer goods prototyping and low-volume production.

-

2025: 3D Systems Corporation introduced Figure 4 PRO-BLK 10 photopolymer resin, providing ABS-like impact strength and heat resistance up to 88°C, enabling functional prototyping and design validation for automotive interiors, electronics, and industrial components.

Rapid Prototyping Materials Market Key Players are:

-

3D Systems Corporation

-

Stratasys Ltd.

-

EOS GmbH

-

Carbon Inc.

-

Desktop Metal Inc.

-

Markforged Inc.

-

Formlabs Inc.

-

BASF SE (Forward AM)

-

Evonik Industries AG

-

Arkema S.A. (Sartomer)

-

Henkel AG & Co. KGaA

-

DSM (Covestro acquired SB)

-

Materialise NV

-

HP Inc. (Jet Fusion)

-

Trumpf GmbH + Co. KG

-

Renishaw plc

-

SLM Solutions Group AG

-

Voxeljet AG

-

ExOne Company

-

GKN Additive (Hoeganaes)

Rapid Prototyping Materials Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.88 Billion |

| Market Size by 2035 | USD 4.11 Billion |

| CAGR | CAGR of 16.87% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Photopolymer Resins, Thermoplastics, Metal Powders, Ceramics, Others) • By Technology (Stereolithography (SLA), Selective Laser Sintering (SLS), Fused Deposition Modeling (FDM), Others) • By Form (Powder, Filament, Liquid Resin, Sheet/Laminate, Others) • By Application (Concept Modeling, Functional Prototyping, Design Verification & Testing, Tooling & Manufacturing Aids, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amazon Web Services (AWS), Microsoft Corporation (Azure Edge), Google LLC (Google Distributed Cloud), Huawei Technologies Co. Ltd., Ericsson, Nokia Corporation, Cisco Systems Inc., IBM Corporation, Intel Corporation, NVIDIA Corporation, Samsung Electronics (Networks Division), Oracle Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies, Qualcomm Incorporated, Verizon Communications Inc., AT&T Inc., T-Mobile US Inc., ZTE Corporation, Fujitsu Limited |

Frequently Asked Questions

The rapid prototyping materials market is expected to grow at a CAGR of 16.87% from 2026 to 2035.

The rapid prototyping materials market was valued at USD 0.878 Billion in 2025.

Key drivers include growing additive manufacturing adoption, advanced material performance, and agile, rapid-iteration product development.

Fused Deposition Modeling (FDM) platforms including represent the fastest-growing technology segment in the Rapid Prototyping Materials Market during 2026 to 2035.

North America dominated the rapid prototyping materials market in 2025, holding 34.15% of global revenues, with the United States accounting for 84.54% of North American revenues.

Get in Touch