Reactive Hot Melt Adhesives Market Report Scope & Overview:

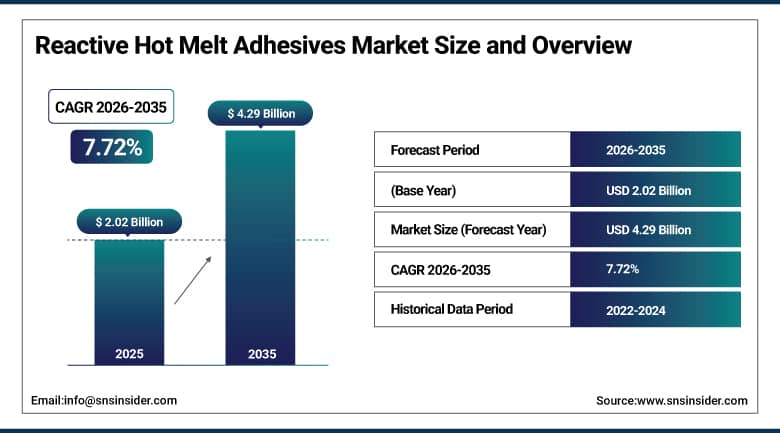

The Reactive Hot Melt Adhesives Market was valued at USD 2.02 Billion in 2025 and is expected to reach USD 4.29 Billion by 2035, growing at a CAGR of 7.72% from 2026 to 2035.

The global reactive hot melt adhesives market is growing at a sustained pace. The market is driven by the progressive replacement of solvent-based adhesives in response to stringent VOC emission regulations including the EPA's air quality standards and EU REACH regulations, the growing adoption of polyurethane-reactive hot melt adhesives in automotive lightweighting programmes whose multi-substrate bonding capability addresses the mixed-material construction challenge of composite, aluminum, and high-strength steel vehicle body design, and the furniture and woodworking industry's adoption of PUR hot melt for edge banding, profile wrapping, and panel lamination whose water and temperature resistance advantage over conventional EVA hot melt sustains premium specification.

Henkel AG introduced a new range of Technomelt PUR reactive hot melts with an advanced moisture curing formulation in 2024 to be used in the assembly of automotive interiors. These adhesives offer high initial tack for rapid positioning of assemblies and higher than conventional heat resistance suitable for applications within the bonnet area and on sunny days for automotive interiors. This product development demonstrates the transition from two-part structural adhesives and solvent-borne contact adhesives to one-part PUR reactive hot melt adhesives in the automotive industry.

Market Size and Forecast

-

Market Size in 2026E: USD 2.18 Billion

-

Market Size by 2035: USD 4.29 Billion

-

CAGR: 7.72% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get More Information On Reactive Hot Melt Adhesives Market - Request Free Sample Report

Reactive Hot Melt Adhesives Market Trends

-

UV-curing reactive hot melt adhesives are gaining adoption in electronics, medical devices, and precision optical bonding applications.

-

Bio-based adhesive formulations are expanding to meet sustainability goals and circular economy requirements across industries.

-

Robotic adhesive dispensing is increasing demand for reactive hot melts with consistent viscosity and controlled application.

-

High-performance PUR hot melt adhesives are witnessing strong growth in textile lamination and technical fabric manufacturing.

-

PUR edge banding adhesives are gaining popularity in premium furniture manufacturing due to superior durability and moisture resistance.

The U.S. Reactive Hot Melt Adhesives Market Outlook

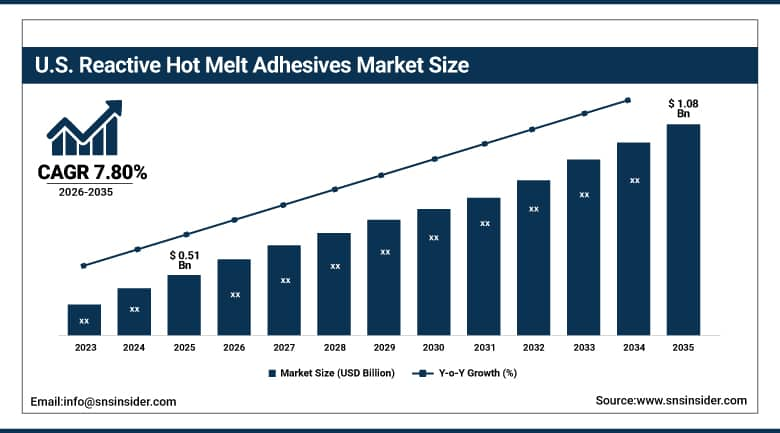

The U.S. Reactive Hot Melt Adhesives Market was valued at approximately USD 0.51 Billion in 2025 and is expected to reach approximately USD 1.08 Billion by 2035, growing at a CAGR of approximately 7.80%.

The U.S. is the most commercially significant reactive hot melt adhesives market within North America. Henkel, H.B. Fuller, 3M, Sika, Bostik (Arkema), and Dow collectively define the domestic commercial landscape. The EPA's air quality regulations creating VOC emission compliance motivation, the automotive sector's lightweighting programme creating multi-substrate bonding demand, and the construction industry's moisture-resistant window and door assembly specification collectively sustain above-average U.S. procurement. The packaging sector's adoption of reactive hot melt for moisture-barrier label and carton assembly, and the textile industry's performance apparel PUR lamination investment create additional domestic commercial demand channels.

In 2023, H.B. Fuller released its latest Swift-melt PUR 400 range of reactive polyurethane hot melt adhesives designed for use in high-speed packaging applications requiring fast cure times that are suitable for use at speeds in excess of 200 meters per minute without compromising on peel strength and temperature resistant requirements for refrigerated food packaging where regular EVA hot melts' inability to handle moisture presents issues.

Reactive Hot Melt Adhesives Market Segment Analysis

-

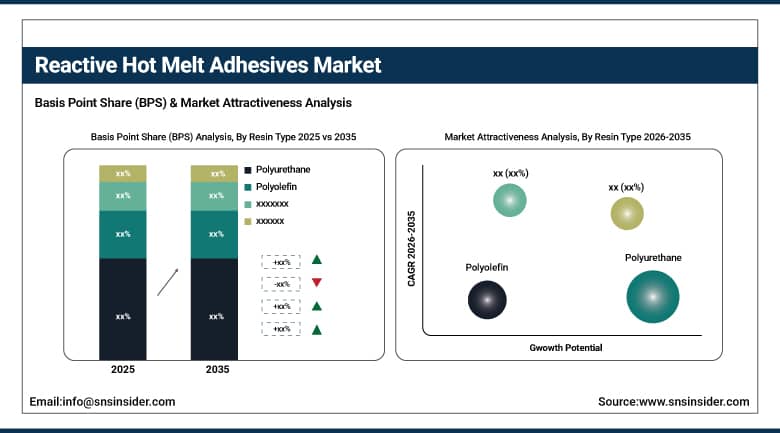

By Resin Type, the polyurethane segment dominated the reactive hot melt adhesives market with approximately 48% share in 2025, while the polyolefin segment is the fastest growing.

-

By Type, the high temperature reactive hot melt adhesives segment dominated the market with approximately 62% share in 2025, while the low temperature segment is the fastest growing.

-

By Substrate, the plastic segment dominated the reactive hot melt adhesives market with approximately 48% share in 2025, while the wood segment is the fastest growing.

-

By Application, the automotive & transportation segment dominated the reactive hot melt adhesives market with the largest share in 2025, while the doors & windows segment is the fastest growing.

By Resin Type, polyurethane dominates, polyolefin grows fastest

Polyurethane reactive hot melt adhesives retained the dominant resin type position with approximately 48% of the market in 2025. PUR hot melt's commercial primacy reflects the unique performance advantage of moisture-curing crosslinking chemistry whose final thermoset bond properties of heat resistance above 120 degrees Celsius, high chemical and solvent resistance, and outstanding mechanical properties across temperature extremes create specification preference across the most demanding automotive, woodworking, and electronics assembly applications. Each automotive OEM whose interior assembly specification migrates from solvent-based contact adhesive to PUR reactive hot melt creates long-duration procurement relationships whose adhesive consumption scales with production volume.

Polyolefin reactive hot melt adhesives are the fastest growing resin type because metallocene catalyst technology advances create polyolefin formulations with adhesion on low-surface-energy polyolefin substrates that conventional hot melt adhesives cannot bond without surface treatment. Each flexible packaging application whose polyethylene and polypropylene substrate combination requires adhesive bonding without corona or flame surface treatment creates polyolefin reactive hot melt procurement whose total process cost advantage over treated substrate bonding sustains specification adoption. The automotive interior component sector's growing use of polypropylene composite panels creates additional polyolefin reactive hot melt application demand.

By Application, automotive dominates, doors & windows grow fastest

Automotive and transportation retained the dominant application position in the reactive hot melt adhesives market in 2025. Vehicle interior assembly's demanding combination of substrate diversity, performance requirements, and production rate creates the most commercially intensive reactive hot melt adhesive application. Each vehicle whose headliner assembly requires adhesion of fabric, foam, and substrate layers across a temperature range from subarctic winter to tropical sun-heated vehicle interior creates PUR hot melt specification whose performance breadth no conventional hot melt alternative can achieve. Door panel assembly, seat foam bonding, carpet lamination, and acoustic insulation panel attachment collectively create per-vehicle reactive hot melt consumption whose aggregate across global automotive production creates the application's dominant commercial volume.

Doors and windows is the fastest growing application because building energy efficiency standards including EN 14351 in Europe, ENERGY STAR in North America, and equivalent Asian certification programmes create technical performance requirements for window frame assembly, spacer bonding, and panel lamination whose moisture resistance, dimensional stability, and service life requirements sustain reactive hot melt specification above conventional EVA alternatives. Each window manufacturer whose edge-seal adhesive specification migrates from conventional thermoplastic to reactive hot melt creates long-duration procurement relationships whose specification investment sustains adoption independent of individual project economics. The global construction sector's emphasis on energy-efficient building envelope performance creates growing reactive hot melt demand in the glazing and joinery sectors.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Europe Reactive Hot Melt Adhesives Market Insights

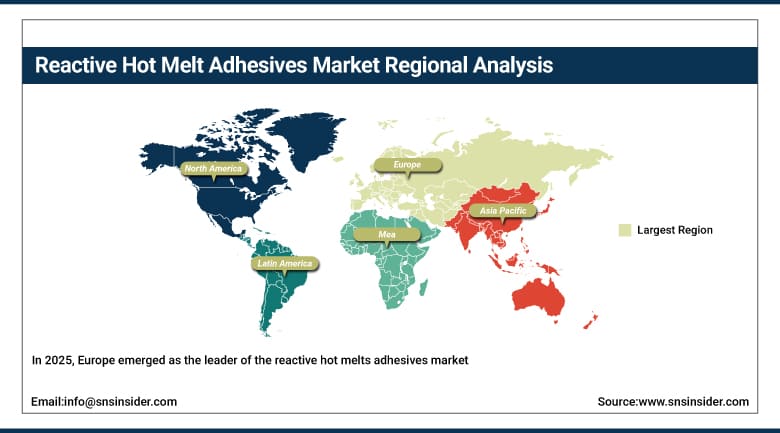

In 2025, Europe emerged as the leader of the reactive hot melts adhesives market, owing to the traditional use of PUR hot melt in the furniture manufacturing industry for edge banding and panel lamination; the automotive sector's solvent adhesives substitution program due to VOC regulation; and stringent chemical safety regulations required under the EU REACH regulation. Germany is responsible for generating around 22.3% of revenue share in Europe owing to automotive OEMs and Tier 1 suppliers' purchase in the region; furniture manufacturing exports originating from Bavaria and Westphalia; and home of Henkel's and Sika's headquarters.

Italy, France, and the United Kingdom are significant secondary markets where the Italian furniture and footwear manufacturing industries, the French automotive assembly supply chain, and the British construction sector's window and door manufacturing create consistent commercial procurement. Jowat SE's German operations and Bostik's French headquarters sustain regional reactive hot melt supply.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Reactive Hot Melt Adhesives Market Insights

North America is the second-largest reactive hot melt adhesives market where the U.S. held approximately 44% of regional revenues, driven by the automotive sector's lightweighting programme, the packaging industry's moisture-barrier specification, and the construction sector's energy-efficient window and door assembly demand. The United States accounts for approximately 87.4% of North American revenues through H.B. Fuller, Henkel, 3M, Sika, and Bostik's commercial operations.

Canada contributes approximately 12.6% of North American revenues through its automotive manufacturing supply chain in Ontario and Quebec, the construction sector's building envelope adhesive investment, and the packaging industry's moisture-resistant carton assembly applications.

Asia Pacific Reactive Hot Melt Adhesives Market Insights

Asia Pacific is the fastest growing regional reactive hot melt adhesives market, driven by China's extraordinary furniture manufacturing export industry, the automotive production sector's reactive hot melt adoption, India's growing furniture and packaging industries, and the Southeast Asian shoe manufacturing sector's PUR hot melt specification. China accounts for approximately 44.8% of Asia Pacific revenues through its world-leading furniture panel and edge banding manufacturing volume, domestic automotive OEM procurement, and the packaging sector's moisture-resistant label and carton application.

India represents the most commercially dynamic emerging market within Asia Pacific where the furniture manufacturing sector's quality specification upgrade, the automotive industry's lightweighting investment, and the packaging sector's barrier specification create above-average reactive hot melt adoption growth from a rapidly expanding commercial base.

MEA & Latin America Reactive Hot Melt Adhesives Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its construction sector's window and door manufacturing, the automotive assembly sector's adhesive procurement, and Vision 2030's industrial development investment creating new manufacturing procurement. The UAE's furniture manufacturing and construction sector add complementary Gulf demand.

Brazil leads Latin American revenues at approximately 44.2% through its furniture manufacturing export industry, the automotive OEM supply chain's adhesive procurement, and the packaging sector's growing moisture-barrier specification. Mexico's automotive Tier 1 supply chain and Argentina's furniture sector collectively sustain regional growth through 2035.

Market Dynamics

Growth Drivers: VOC regulation replacement of solvent adhesives and automotive lightweighting creating multi-substrate bonding demand

Stringent VOC emission regulations including the EPA's National Emission Standards for Hazardous Air Pollutants, EU REACH, and equivalent national chemical safety frameworks are the reactive hot melt adhesives market's most commercially certain compliance-driven growth driver. Each manufacturing facility whose solvent-based adhesive use creates regulatory exposure to VOC emission penalties creates a technology migration motivation whose compliance timeline creates defined reactive hot melt adoption procurement. The furniture manufacturing sector's systematic migration from solvent-based contact adhesives to PUR reactive hot melt for edge banding and panel lamination demonstrates the commercial scale of regulatory-driven adhesive technology substitution.

Automotive lightweighting creates a structural demand for reactive hot melt adhesives whose multi-substrate bonding capability addresses the mixed-material construction challenge of contemporary vehicle body and interior design. Each vehicle model transition to mixed-material construction incorporating aluminum, carbon fiber composite, glass, textile, and thermoplastic components simultaneously creates adhesive specification requirements that no single conventional single-substrate adhesive can satisfy, creating PUR reactive hot melt specification as the technically enabling bonding solution.

Restraints: Limited shelf life and high initial equipment investment

Reactive hot melt adhesives’ limited shelf life and moisture sensitivity in storage create logistics and inventory management complexity that sustains specification caution among end users whose storage condition control capability is limited. PUR adhesives’ requirement for moisture-free, temperature-controlled storage whose breach creates premature curing and material waste creates inventory management burden that conventional EVA hot melt alternatives’ ambient storage tolerance avoids. Each reactive hot melt adoption that creates storage protocol training, dedicated climate-controlled warehousing investment, and moisture barrier packaging requirement adds operational cost that moderates specification migration pace in cost-sensitive manufacturing environments.

High initial capital investment for specialized reactive hot melt dispensing equipment, whose precision temperature control, moisture protection, and automated metering requirements create above-conventional-hot-melt system cost, creates adoption barriers for small and medium-sized manufacturers whose capital budget limitations require clear ROI justification. Each reactive hot melt dispensing system installation whose equipment cost ranges from tens of thousands to hundreds of thousands of dollars creates a capital commitment barrier that moderates SME adoption pace in cost-sensitive manufacturing sectors.

Opportunities: UV-curing reactive hot melt and bio-based sustainable formulations

UV-curing reactive hot melt adhesive development represents the most commercially premium near-term application expansion opportunity whose instantaneous polymerization on UV light exposure eliminates the moisture curing time dependency that PUR reactive hot melt's production line integration requirement creates. Each electronics assembly or optical component bonding application whose UV-cure adhesive adoption enables above-conventional-hot-melt production line speed creates premium product procurement whose application-specific performance justifies above-commodity formulation pricing. The medical device assembly sector's biocompatibility-certified UV-cure adhesive adoption demonstrates the commercial premium that UV-curing reactive hot melt can command in critical specification applications.

Bio-based reactive hot melt adhesive development represents the most commercially significant long-term sustainability opportunity whose reduced fossil feedstock content creates supply chain sustainability certification eligibility that automotive and furniture OEM sustainability programmes increasingly require from adhesive suppliers. Each furniture manufacturer whose FSC or PEFC certification programme creates bio-based adhesive specification preference creates procurement motivation for bio-polyol PUR hot melt alternatives whose sustainability performance compounds with commercial performance equivalence.

Recent Developments:

-

2026: Henkel AG & Co. KGaA expanded its sustainable reactive hot melt adhesive portfolio with bio-based formulations for packaging, automotive, and furniture applications.

-

2026: Jowat SE enhanced its reactive PUR hot melt adhesive range with low-emission formulations developed for furniture, construction, and edge-banding applications.

-

2025: H.B. Fuller Company introduced advanced PUR reactive hot melt adhesives designed to improve bonding performance in woodworking, textiles, and product assembly.

-

2025: Sika AG expanded its high-performance hot melt adhesive solutions to support automated manufacturing and industrial assembly applications.

Reactive Hot Melt Adhesives Market key players are:

-

Henkel AG & Co. KGaA

-

H.B. Fuller Company

-

3M Company

-

Sika AG

-

Bostik (Arkema)

-

Jowat SE

-

Dow Inc.

-

Huntsman Corporation

-

Dymax Corporation

-

Beardow Adams Ltd.

-

Kleiberit Klebstoffe GmbH & Co. KG

-

Evonik Industries AG

-

Wacker Chemie AG

-

Avery Dennison Corporation

-

Paramelt B.V.

-

Daicel Corporation

-

Tex Year Industries Inc.

-

Power Adhesives Ltd.

-

Robatech AG

-

Buhnen GmbH & Co. KG

Reactive Hot Melt Adhesives Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.02 Billion |

| Market Size by 2035 | USD 4.29 Billion |

| CAGR | CAGR of 7.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Polyurethane, Polyolefin, Others) • By Type (High Temperature, Low Temperature) • By Substrate (Wood, Plastic, Others) • By Application (Automotive & Transportation, Doors & Windows, Furniture & Upholstery, Lamination, Textile, Assembly, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Sika AG, Bostik (Arkema), Jowat SE, Dow Inc., Huntsman Corporation, Dymax Corporation, Beardow Adams Ltd., Kleiberit Klebstoffe GmbH & Co. KG, Evonik Industries AG, Wacker Chemie AG, Avery Dennison Corporation, Paramelt B.V., Daicel Corporation, Tex Year Industries Inc., Power Adhesives Ltd., Robatech AG, Buhnen GmbH & Co. KG |

Frequently Asked Questions

Europe dominated the Reactive Hot Melt Adhesives Market in 2025.

Polyurethane dominated with approximately 48% share in 2025.

The Reactive Hot Melt Adhesives Market is expected to grow at a CAGR of 7.72% from 2026 to 2035.

The Reactive Hot Melt Adhesives Market was valued at USD 2.02 Billion in 2025.

Stringent VOC emission regulations creating compliance-driven specification migration from solvent-based adhesives to reactive hot melt alternatives, and automotive lightweighting programmes.

Get in Touch