Roofing Anchors Market Report Scope & Overview:

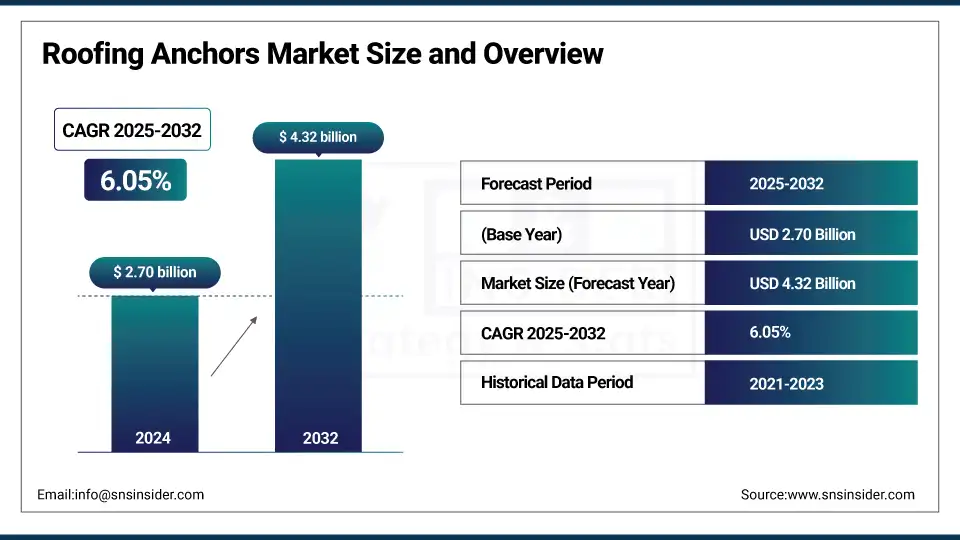

The Roofing Anchors Market Size was valued at USD 2.70 billion in 2024 and is expected to reach USD 4.32 billion by 2032 and grow at a CAGR of 6.05% over the forecast period of 2025-2032.

Roofing Anchors market analysis emphasizes the impact of large end-user segments, including residential, commercial, and industrial sectors. New construction projects experience a strong uptick as urbanization intensifies and infrastructure development remains a focus of developed and emerging economies. Housing is fighting against residential development, as office towers, shopping malls, archives warehouse, and parking lots want to occupy the site using land. In addition, facilities relating to industries, such as factories and logistics centers are also seeing a resilient demand for new builds in connection with an expansion of manufacturing and e-commerce. These combined factors are all contributing to the increasing need for roof anchor points, as safety standards and fall safety systems are integrated as a part of contemporary construction protocols, which drive the roofing anchors market growth.

Market Size and Forecast:

-

Market Size in 2024: USD 2.70 Billion

-

Market Size by 2032: USD 4.32 Billion

-

CAGR: 6.05% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Roofing Anchors Market - Request Free Sample Report

Roofing Anchors Market Trends:

-

Increasing construction and infrastructure development activities worldwide are driving demand for advanced fall protection systems, including roofing anchors.

-

Stringent occupational safety regulations across residential, commercial, and industrial sectors are boosting the adoption of compliant roof anchoring solutions.

-

Rising awareness regarding worker safety and mandatory use of personal fall arrest systems is accelerating market growth.

-

Growth in renovation and maintenance of aging buildings is increasing the need for temporary and permanent roofing anchor installations.

-

Technological advancements in lightweight, corrosion-resistant, and reusable anchor materials are enhancing product durability and performance.

-

Expansion of commercial real estate, warehouses, and industrial facilities is fostering higher deployment of certified roof safety equipment.

For instance, the housing construction in the U.S. and underway and gaining momentum. According to the Census. gov, the spending on residential construction in 2024 totalled nearly USD 917.9billion, up by 5.9% from USD 866.9 billion in 2023.

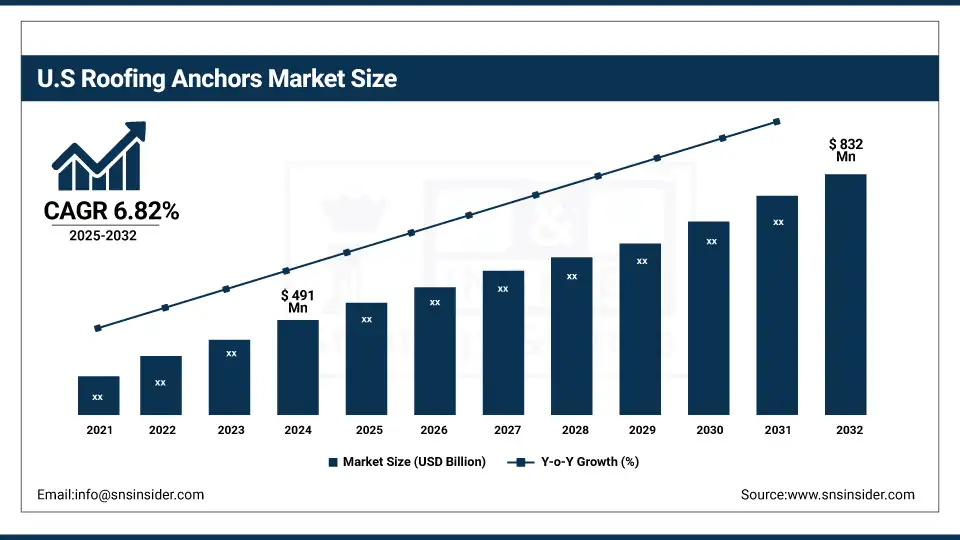

The U.S Roofing Anchors market size was USD 491 million in 2024 and is expected to reach USD 832 million by 2032 and grow at a CAGR of 6.82% over the forecast period of 2025-2032. It is driven by electric regulations, LEED-certified buildings, and a desire for shortened building timelines. In late 2023, U.S. homebuilder Lennar purchased construction tech company Veeva to scale digital panelized construction.

Market Dynamics:

Key Drivers:

-

Stringent Occupational Safety Regulations Drive the Market Growth

Favorable regulations imposed by bodies, such as OSHA (Occupational Safety and Health Administration) have enhanced the sales of fall protection systems including roofing anchors. These standards require certified fall arrest gear on high-risk construction sites, which is a demand that tends not to vary. Failure to adhere leads to legal sanctions and production stoppages, which make the safety investment a priority for companies. Increasing sensitivity toward the safety of the workers at the site has led construction companies and contractors to incorporate rooftop safety systems at the design stage itself. Roofing anchors are key elements of fall protection systems, and they are poised to directly benefit from this regulatory trend.

In 2023, OSHA gained a USD 35 million dollar increase in their budget for inspections, resulting in over 40,000 inspections at construction sites in the U.S., prompting construction workers to order more safety equipment in including anchor systems.

Restraints:

-

High Cost of Advanced Anchor Systems May Hamper the Market Growth

Safety anchors are a must-have, but their cost, particularly for the stainless steel or corrosion-resistant coated ones, can inhibit penetration for price-sensitive markets. Lesser contractors will endeavor to take cheap alternatives or push off installation. Moreover, costs are also increased if anchors must be custom-designed for specific roof configurations, buildings, or environmental conditions. Slow approval and certification for safety equipment can be a barrier to implementation as well. Installation complexities and the skilled labor needed could contribute to greater cost, particularly where permanent installations or portable installations in industrial facilities are placed in service. These cost considerations, however, prevent them from being widely used in developing countries and low-volume buildings.

Opportunities:

-

Technological Advancements in Anchor Design and Materials Creates an Opportunity for the Market Growth

Advancements in anchor equipment, including the use of lightweight alloys, corrosion-proof coatings, and smart anchors with check inspection alarms, are also opening paths. These enhancements result in longer-lasting, easier to install, and more weather-resistant anchors that are compatible with more types of roofs. The addition of temporary roof anchors systems to IoT devices also opens up new possibilities for live safety-critical checks and predictive maintenance. Intelligent anchors also facilitate monitoring of usage and stress loads for better safety monitoring. These new features appeal to businesses looking for nonconnotative and dependable safety systems. Manufacturers with R&D investments can distinguish their products and personal protective equipment (PPE) market segments, which drive the roofing anchors market trends.

For instance, in 2023, a large roofing equipment maker pumped USD 18 million into a new R&D centre to look at “smart” fall protection systems that would include sensor-based anchors for high-risk construction safety equipment sites.

Segment Analysis:

By Product Type

Permanent anchors held the largest market share, around 32% in 2024. It is due to the used as it can be built into building construction, reinforcing structures. They are usually fitted in the early stages of roofing and are preferred in large-scale industrial and commercial structures. These anchors also help to maintain long-term OSHA compliance and are more reliable at stopping rooftop falls.

Temporary anchors the rising demands on retrofitting, maintenance, and residential repair, the temporary anchors are developing quickly. Such anchors are portable, less expensive, and easier to deploy. This segment is also powered by the increasing participation of small contractors working on short-duration projects, particularly in urban housing and telecom maintenance.

By Material

Stainless steel remains the dominant material due to its superior strength, corrosion resistance, and compliance with international safety standards. Its extensively used in commercial buildings, industrial facilities, and offshore platforms where durability under extreme conditions is a must. These factors make stainless steel anchors preferred for permanent installations.

Aluminum anchors are increasingly adopted for residential and mobile applications due to their lightweight nature and ease of installation. They’re ideal for portable and temporary systems where mobility and efficiency are critical. The rise in home improvement and solar panel installations is fueling demand for these anchors in lightweight setups.

By Application

In 2024, commercial roofing held the largest share of the roofing anchors market, comprising 48% of the global market. This is largely attributed to the common use of anchors in office buildings, hospitals, retail centers, or schools, where workers must often access a rooftop to service an HVAC unit, sign, or other equipment. These are frequently required to have OSHA-compliant fall protection for the life and safety compliance needs of the building. In addition, there is a surge of retrofitting commercial property rooftops with solar panels and energy systems that are adding to the demand for certified rooftop anchors.

By End-Use Industry

The roofing anchors market was led by the building & construction industry in 2024, and is projected to grow for this industry and account for around 32% of the market share. Roofing Anchors Application Insights Due to optimum utilization of roofing anchors at the time of construction for new structures, general contractors and engineering, procurement, and construction (EPC) companies form the major customer base.

It is particularly high in big projects of residential, commercial, and industrial construction, where regulatory compliance, health, and safety planning are carried out from the design phase. Among end-use categories, energy & utilities is the fastest-growing sector which includes solar energy, telecom, and maintenance services.

Regional Analysis:

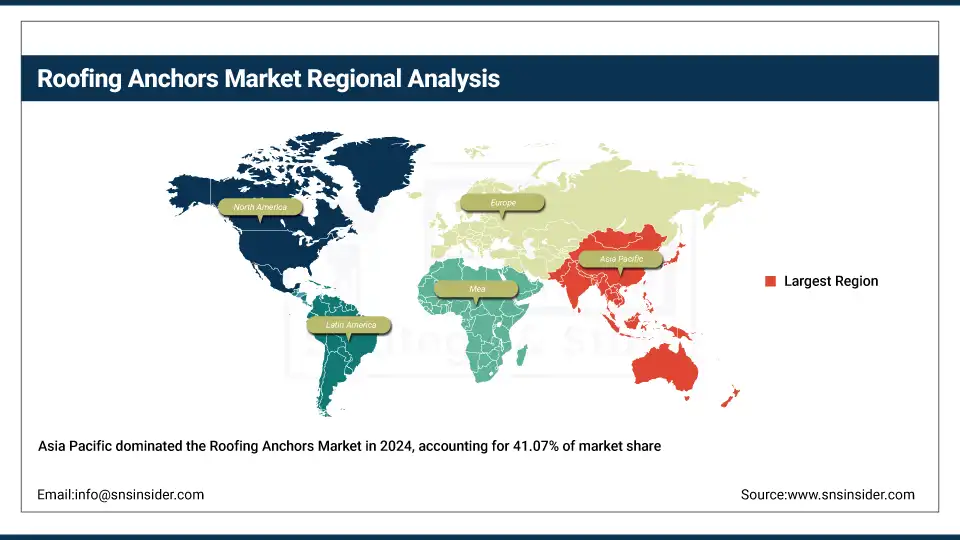

Asia Pacific held the Roofing Anchors market share largest market share, around 41.07%, 2024. It is due to the rising, flourishing construction sector, increasing urbanization, government housing policies, and demand for cost-effective construction products. Nations such as China and India are providing a super-strong market for prefabricated panels to address the housing shortages arising from burgeoning urban populations. In July 2024, India’s Ministry of Housing & Urban Affairs announced the completion of over 7,100 panel-based residential projects in 100 cities, supported by nearly USD 17.3 billion in public funding, pointing to the market’s commitment to panelized construction for mass housing and smart cities.

Get Customized Report as per Your Business Requirement - Enquiry Now

The North America region is the fastest-growing market. It is due to the technology and construction capabilities, supported by skilled labor, that are more developed and as the demand for energy-efficient and sustainable buildings is increasing. A surplus of expensive labor and a shortage of workers in the U.S. and Canada have been forcing the industry toward off-site modular construction, in which prefabricated panels make it possible to install buildings more quickly and cheaply. One significant catalyst to this trend was the US General Services Administration’s 2024 investment of USD 80 million from the Inflation Reduction Act to retrofit federal buildings with this energy-efficient material, such as UHPC slab panels, driving wider use in public infrastructure.

Europe maintains a significant share of the Roofing Anchors market, due to stringent building energy codes, highly skilled labor, and regulatory backing of sustainable urban development. Several EU nations are moving towards ‘zero-energy building’ goals, promoting the use of high-performance, pre-insulated panels for quick, sustainable construction. Moreover, the increasing trend of renovation activity in Western Europe, particularly in countries, such as Germany, France, and the Nordic countries, is contributing to the overall demand for prefabricated solutions from both residential and non-residential construction applications.

Key Players:

Major Roofing Anchors companies are 3M, MSA Safety, Honeywell, WernerCo, Guardian Fall Protection, FallTech, Kee Safety, Tractel, XSPlatforms, Capital Safety, Super Anchor Safety, Reliance Fall Protection, Malta Dynamics, Safe Approach, DBI-SALA, Big Rock Supply, FrenchCreek Production, SafeWaze, FLS (Flexible Lifeline Systems), and RidgeGear.

Recent Development:

-

In July 2024, Wells completed the acquisition of GATE Precast, broadening its U.S. presence and architectural and structural precast panel capabilities. The merger expanded Wells’ manufacturing profile to 14 operations in more than 30 states.

-

In 2024, Carlisle acquired MTL Holdings and added to its building envelope in order “to enable Carlisle to offer customers a combination of metal edge systems with Carlisle’s industry-leading prefabricated roofing and panel solutions, improving integrated offsite solutions for the commercial construction industry.

| Report Attributes | Details |

| Market Size in 2024 | USD 2.70 Billion |

| Market Size by 2032 | USD 4.32 Billion |

| CAGR | CAGR of6.05% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Permanent Anchors, Temporary Anchors, Mobile Anchors, Fixed Anchors, and Others) • By Material (Steel, Aluminum, Stainless Steel, Composite Materials, and Others (e.g., high-strength alloys, plastic-coated metals) • By Application (Residential Roofing, Commercial Roofing, Industrial Roofing, Infrastructure Projects, and Others (e.g., maintenance services, temporary event structures) • By End-Use Industry (Construction, Oil & Gas, Energy & Utilities, Telecom, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | 3M, MSA Safety, Honeywell, WernerCo, Guardian Fall Protection, FallTech, Kee Safety, Tractel, XSPlatforms, Capital Safety, Super Anchor Safety, Reliance Fall Protection, Malta Dynamics, Safe Approach, DBI-SALA, Big Rock Supply, FrenchCreek Production, SafeWaze, FLS (Flexible Lifeline Systems), RidgeGear |

Frequently Asked Questions

Recent innovations include modular mobile anchors, lightweight composite anchors, and smart monitoring-enabled anchor systems.

They are primarily used in residential, commercial, and industrial roofing projects for fall protection.

Key players include 3M, Honeywell, MSA Safety, WernerCo, Guardian Fall Protection, and Reliance Industries.

Permanent anchors and fixed anchors are the most widely used due to their durability and compliance standards.

North America and Europe are leading due to stringent safety regulations and high construction activity.

Get in Touch