Scleroderma Therapeutics Market Report Scope & Overview:

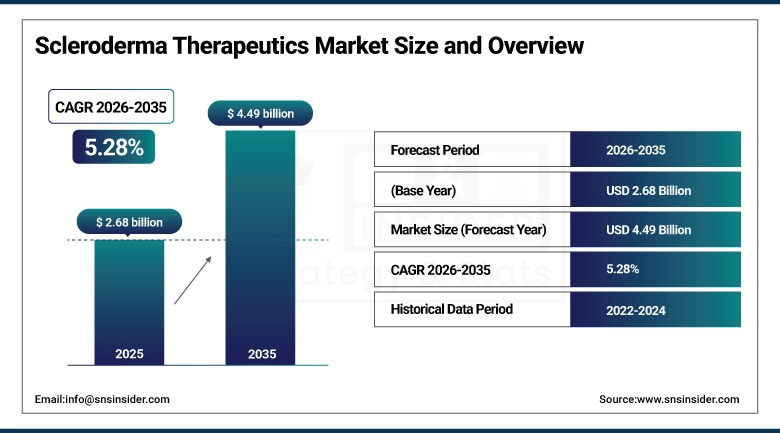

The Scleroderma Therapeutics Market size was valued at USD 2.68 Billion in 2025 and is expected to reach USD 4.49 Billion by 2035, growing at a CAGR of 5.28% over the forecast period of 2026-2035.

The Global Scleroderma Therapeutics Market is driven by the rising incidence of autoimmune disorders globally, major advances in the understanding of the disease process, and a robust pipeline of targeted biologic and disease-modifying therapies. The rising investment in research and development by pharmaceutical companies, along with the orphan drug designation and incentives from regulatory bodies for therapies targeting this rare and complex disease, are accelerating the development of novel therapies. The rising awareness of healthcare professionals about the early detection and management of the disease, as well as the development of multi-targeted therapies to treat the two major manifestations of scleroderma, are key drivers of the scleroderma therapeutics market. The market is also driven by the efforts of patient advocacy groups to seek more effective therapies and improve access to care, thus creating a supportive environment to develop therapies for the disease.

In March 2025, the FDA granted Breakthrough Therapy Designation to a novel investigational monoclonal antibody for the treatment of diffuse cutaneous systemic sclerosis, based on promising Phase II data showing significant improvement in modified Rodnan skin scores, highlighting the accelerated regulatory pathway for promising scleroderma therapies.

Scleroderma Therapeutics Market Size and Forecast:

-

Market Size in 2025: USD 2.68 Billion

-

Market Size by 2035: USD 4.49 Billion

-

CAGR: 5.28% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Scleroderma Therapeutics Market - Request Free Sample Report

Scleroderma Therapeutics Market Trends:

-

Increased focus on developing targeted biologic therapies and small molecules that specifically inhibit fibrotic pathways, such as TGF-β and CTGF, moving beyond traditional immunosuppression.

-

Growing adoption of combination therapies to simultaneously manage the complex, multi-system manifestations of scleroderma, including fibrosis, vasculopathy, and autoimmune inflammation.

-

Rising utilization of autologous hematopoietic stem cell transplantation for severe, rapidly progressive systemic sclerosis, offering the potential for long-term remission in carefully selected patients.

-

Integration of digital biomarkers and telemedicine for remote monitoring of disease progression and treatment response, improving patient management and clinical trial efficiency.

-

Expansion of precision medicine approaches, utilizing genomic and proteomic profiling to identify patient subpopulations most likely to respond to specific targeted therapies.

-

Increased investment in research focused on treating interstitial lung disease associated with systemic sclerosis, a major cause of morbidity and mortality.

-

Development of novel topical formulations for localized scleroderma, aiming to minimize systemic side effects while effectively managing cutaneous lesions.

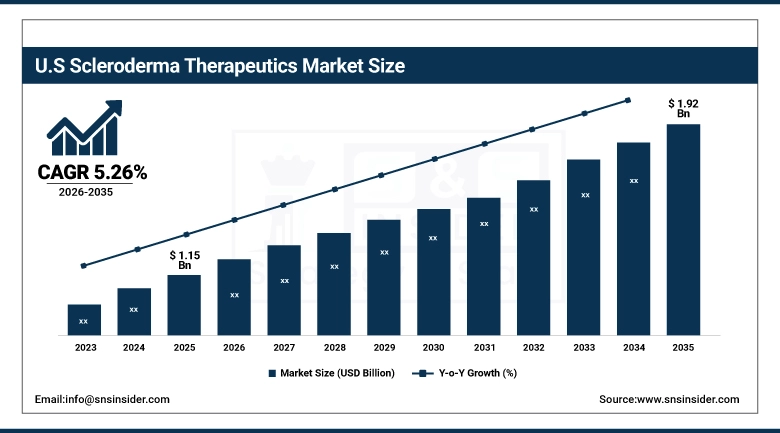

The U.S. Scleroderma Therapeutics Market is estimated at USD 1.15 billion in 2025 and is expected to reach USD 1.92 billion by 2035, growing at a CAGR of 5.26% from 2026-2035. The US has the highest share in the market due to the presence of advanced medical facilities, high health care spending, and the presence of the world's best research facilities and pharmaceutical companies. High funding by the government and private sector for research on autoimmune diseases, a favorable regulatory scenario with incentives for orphan drugs, and high patient awareness due to the presence of strong patient advocacy groups such as the Scleroderma Foundation are some of the key factors responsible for the growth of the US market.

Scleroderma Therapeutics Market Growth Drivers:

- Deepening Understanding of Disease Pathology and Target Identification Driving Drug Development

The significant change in the understanding of the complex pathophysiology of scleroderma is one of the main drivers for the growth of the global scleroderma therapeutics market. The complex pathophysiology of scleroderma has been studied extensively over the years, changing the understanding of this complex disease from just an autoimmune phenomenon to a complex phenomenon involving vasculopathy, immune system dysfunction, and fibrosis. The complex pathophysiology has opened doors to various specific molecular targets that can be used as a tool for drug development. The identification of specific cytokines, growth factors, and intracellular signaling pathways that are responsible for fibroblast activation and collagen overproduction has led to the development of promising targeted drugs that can potentially halt or reverse this complex pathophysiology with better efficacy and safety profiles.

For example, in February 2025, data from an open-label extension study of a selective ROCK2 inhibitor showed sustained improvement in skin fibrosis and lung function in patients with diffuse cutaneous systemic sclerosis, validating this novel therapeutic target for long-term disease modification.

Scleroderma Therapeutics Market Restraints:

- High Drug Development Costs and Stringent Regulatory Requirements for Rare Disease Therapies

The expensive and difficult nature of clinical trials for such a rare and heterogeneous disease as scleroderma is a major constraint on the growth of the market. It is difficult and expensive to recruit enough patients with specific sub-types of the disease for statistically significant clinical trials, which often require international collaborations. Additionally, the regulatory hurdles for demonstrating safety and efficacy, though necessary, are expensive and time-consuming in the development of a new therapy. The lack of well-validated and universally accepted surrogate end points that can predict clinical benefits in the long run is another complication in clinical trials, which could delay the introduction of new therapies.

Scleroderma Therapeutics Market Opportunities:

- Untapped Potential in Treating Interstitial Lung Disease and Pulmonary Arterial Hypertension in Scleroderma Patients

One of the major opportunities in the market is the treatment of the most severe complications of systemic sclerosis, such as interstitial lung disease and pulmonary arterial hypertension, as the majority of deaths from systemic sclerosis are due to these complications. As the understanding of the processes of fibrosis and vascular changes involved in the pulmonary complications of systemic sclerosis continues to evolve, there is the opportunity to continue to develop and apply this treatment, as the success of the antifibrotic drugs such as nintedanib in the treatment of SSc-ILD has already done, in order to develop treatments which are effective in the stabilization or improvement of lung function in these patient groups, as this represents a major high unmet medical need, which provides a tremendous opportunity for revenue growth in the future, as well as the survival rate of the patients.

For example, in November 2024, a Phase III trial of a novel inhaled prostacyclin analogue reported positive topline results, demonstrating a significant reduction in pulmonary vascular resistance and improvement in exercise capacity in SSc-PAH patients, offering a new targeted therapeutic option for this devastating complication.

Scleroderma Therapeutics Market Segment Analysis:

-

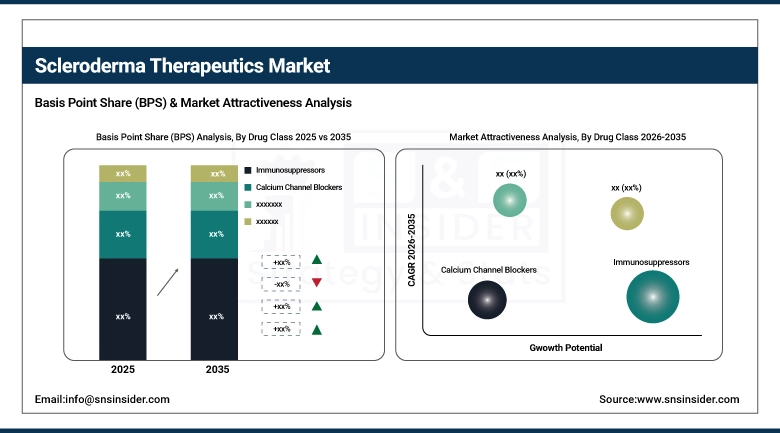

By drug class, Immunosuppressors accounted for the largest share of 32.45% in 2025, and the Endothelin Receptor Antagonists segment is anticipated to exhibit the fastest growth, at a CAGR of 6.10%.

-

By indication, Systemic Scleroderma has registered the highest market share of about 78.55% in 2025, and is also anticipated to register the highest CAGR of 5.45% during the forecast period.

By Drug Class, Immunosuppressors Lead the Market, While Endothelin Receptor Antagonists Register Fastest Growth

In 2025, the immunosuppressors segment held the highest share in terms of revenue, accounting for more than 32.45%, as these drugs have been the cornerstone in the therapeutic management of scleroderma for years. Medications such as methotrexate, mycophenolate mofetil, and cyclophosphamide are commonly used in the management of the inflammatory and autoimmune symptoms of scleroderma, especially in the early stages of the disease. On the contrary, the endothelin receptor antagonists segment, which comprises drugs such as bosentan and ambrisentan, is expected to exhibit the highest growth rate, at around 6.10%, in the period between 2026 and 2035. This is because these drugs play a crucial role in the management of SSc-PAH, which is responsible for the deaths of a large number of patients suffering from scleroderma. These drugs are known for their efficacy in improving exercise capacity and functional class in PAH, and research on their antifibrotic properties is also in progress.

By Indication, Systemic Scleroderma Dominates, While Localized Scleroderma Shows Steady Growth

The segment of systemic scleroderma accounted for the maximum revenue share of 78.55% in 2025, owing to the severe, multi-organ nature of the disease that requires aggressive, lifelong therapeutic intervention. The high morbidity and mortality rates of patients with systemic sclerosis, especially the diffuse cutaneous form, create a strong need for effective disease-modifying therapies. This segment has a broad range of targets, ranging from skin fibrosis, ILD, PAH, renal crises, etc. The segment of systemic scleroderma is expected to grow at a CAGR of 5.45% during the forecast period of 2026-2035, as the disease is severe, lifelong, and requires aggressive intervention. The localized scleroderma segment is much smaller, but it is an ongoing market that addresses the topical and phototherapy needs of patients with skin manifestations of the disease, as well as the prevention of joint contractures, especially in the pediatric population.

Scleroderma Therapeutics Market Regional Highlights:

Asia Pacific Scleroderma Therapeutics Market Insights:

The Asia Pacific market segment is the fastest-growing segment with a CAGR of 5.98%. This can be attributed to the improving healthcare infrastructure, awareness of rare autoimmune diseases, and growing healthcare expenditure in countries such as China, Japan, and Korea. The vast population of patients, along with government initiatives to promote research and treatment of rare diseases, makes this region a fertile ground for the market to grow. This region is becoming a global destination for clinical trials, attracting global pharmaceutical companies to take advantage of the vast population to carry out clinical trials. The growing biotechnology sector, along with the development of a pharmaceutical industry focusing on the development of biosimilars, is helping to drive the scleroderma therapeutics market.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Scleroderma Therapeutics Market Insights:

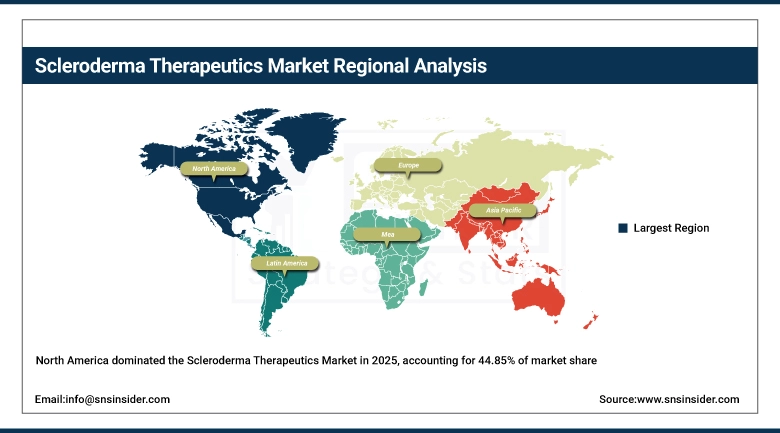

North America dominated the market with the highest share of 44.85% in terms of revenue in the year 2025 due to its highly developed healthcare system, high rate of diagnosis, and high healthcare expenditure. The key enablers are the presence of the best pharmaceutical companies in the world, the supportive environment of the regulatory and reimbursement system, and the support from patient advocacy groups that fund the research and raise awareness about the disease. The U.S. also offers incentives such as orphan drug designation and priority review by the FDA, which hasten the development of new drugs targeting scleroderma. The high level of venture capital funding in biotech companies that specialize in immunology and fibrosis also confirms the position of North America as the market leader.

Europe Scleroderma Therapeutics Market Insights:

The European region holds the second most dominant market for scleroderma therapeutics due to a high standard of healthcare facilities, centralized treatment networks, and government support for research through schemes such as Horizon Europe. The region provides access to substantial patient data and a collaborative research environment, thus supporting robust clinical trials. Countries such as Germany, France, and the UK are major contributors to the scleroderma therapeutics market due to the high standard of healthcare facilities, thus providing good access to conventional as well as advanced therapies. The European Medicines Agency places a strong emphasis on rare diseases, and the designation of orphan medicinal products continues to motivate pharmaceutical companies to launch innovative scleroderma therapies in the European region.

Latin America (LATAM) and Middle East & Africa (MEA) Scleroderma Therapeutics Market Insights:

The Scleroderma Therapeutics Market in Latin America & Middle East & Africa is expected to grow gradually with more investment in healthcare infrastructure, a growing number of specialized rheumatologists, and rising awareness of the disease. The key drivers of the market will be the gradual introduction of biologic therapies, usually through government-funded health programs, and working with international non-profit organizations to improve access to care. The market may still be small in comparison to other regions, but there is a growing need to educate healthcare professionals about the diagnosis and treatment of complex rheumatic diseases. There may be a greater understanding of the disease through patient registries and epidemiologic studies in these regions, and this could translate into more pharmaceutical companies becoming interested in the market in the future.

Scleroderma Therapeutics Market Competitive Landscape:

Boehringer Ingelheim (founded in 1885) is a global leader in respiratory and fibrosis research, leveraging its deep expertise in inflammatory and fibrotic pathways to develop therapies for scleroderma-associated interstitial lung disease, with a strong focus on innovative small molecules and biologics.

-

In May 2025, the company announced positive long-term extension data for its antifibrotic therapy in SSc-ILD, demonstrating sustained slowing of lung function decline over a four-year period, reinforcing its role as a standard of care.

Johnson & Johnson (founded in 1886), through its Janssen division, applies its extensive immunology expertise to develop targeted therapies for autoimmune diseases, including systemic sclerosis, by focusing on key cytokine pathways involved in inflammation and fibrosis.

-

In September 2024, Janssen initiated a Phase IIb trial for a novel monoclonal antibody targeting a key mediator of fibrosis in patients with diffuse cutaneous systemic sclerosis, aiming to build on preclinical evidence of disease modification.

Roche (founded in 1896) is a powerhouse in personalized healthcare, using its capabilities in genomics and targeted therapies to develop and commercialize treatments for severe autoimmune conditions, with a significant interest in the fibrotic complications of scleroderma.

-

In January 2025, Roche presented new biomarker data from a Phase III study of an immunomodulatory agent in systemic sclerosis, identifying potential predictors of treatment response, a key step toward personalized medicine in this disease.

Scleroderma Therapeutics Market Key Players:

-

Boehringer Ingelheim

-

Johnson & Johnson (Janssen)

-

Roche

-

Novartis AG

-

Pfizer Inc.

-

Bristol-Myers Squibb

-

Merck & Co., Inc.

-

Sanofi

-

AbbVie Inc.

-

Gilead Sciences, Inc.

-

GlaxoSmithKline plc

-

Astellas Pharma Inc.

-

Corbus Pharmaceuticals Holdings, Inc.

-

ChemomAb Ltd.

-

Kadmon Holdings, Inc.

-

Prometheus Biosciences, Inc.

-

Cumberland Pharmaceuticals Inc.

-

Viela Bio, Inc.

-

aTyr Pharma, Inc.

-

Citius Pharmaceuticals, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.68 Billion |

| Market Size by 2035 | USD 4.49 Billion |

| CAGR | CAGR of 5.28% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Class (Immunosuppressors, Calcium Channel Blockers, Endothelin Receptor Antagonists, Prostacyclin Analogues, Phosphodiesterase 5 inhibitors – PHA, Analgesics, Others) • By Indication (Systemic Scleroderma {Morphea, Linear}, Localized Scleroderma {Diffuse Systemic Sclerosis, Limited Cutaneous Systemic Sclerosis Syndrome}) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Boehringer Ingelheim, Johnson & Johnson (Janssen), Roche, Novartis AG, Pfizer Inc., Bristol-Myers Squibb, Merck & Co. Inc., Sanofi, AbbVie Inc., Gilead Sciences Inc., GlaxoSmithKline plc, Astellas Pharma Inc., Corbus Pharmaceuticals Holdings Inc., ChemomAb Ltd., Kadmon Holdings Inc., Prometheus Biosciences Inc., Cumberland Pharmaceuticals Inc., Viela Bio Inc., aTyr Pharma Inc., Citius Pharmaceuticals Inc. |

Frequently Asked Questions

Growth is primarily driven by rising autoimmune disease prevalence, advancements in targeted biologics, increasing R&D investments, and supportive regulatory incentives for rare diseases.

Immunosuppressors hold the largest market share due to their long-standing use, cost-effectiveness, and inclusion in standard treatment guidelines.

Endothelin receptor antagonists are projected to grow the fastest, driven by their effectiveness in treating pulmonary arterial hypertension associated with scleroderma.

North America dominates the market due to advanced healthcare infrastructure, high awareness, strong R&D funding, and favorable regulatory policies.

Key challenges include high drug development costs, difficulty in patient recruitment for trials, and stringent regulatory requirements for rare disease therapies.

Get in Touch