Intravenous (IV) Solutions Market Report Scope & Overview:

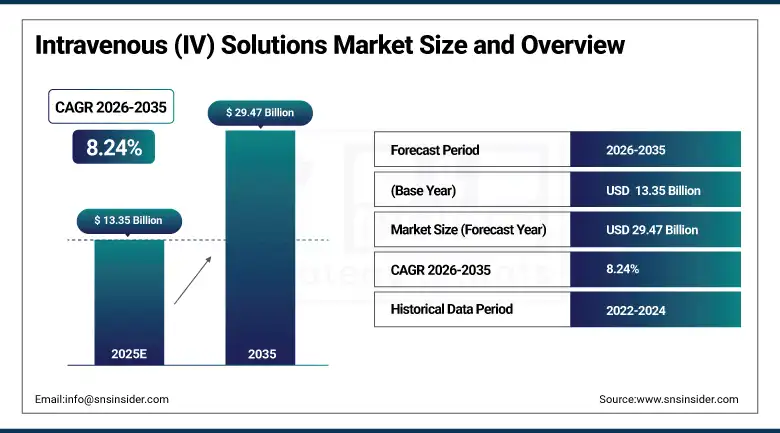

The Intravenous (IV) Solutions Market Size was valued at USD 13.35 Billion in 2025 and is expected to reach USD 29.47 Billion by 2035 and grow at a CAGR of 8.24% over the forecast period 2026-2035.

IV Solutions Market based on ongoing rise in prevalence of chronic diseases and forms of critical care such as cancer, cardiovascular diseases, undernourishment, and desiccation. The growing number of pediatric and geriatric patients approaching hospitals for admissions & surgical procedures, and increasing demand for parenteral nutrition solutions have all led to a significant surge in demand for IV solutions. Hospital-based IV usage has been growing 6–7% per year, driven by a rise in hospital admissions and surgical procedures

Intravenous (IV) Solutions Market Size and Forecast:

-

Market Size in 2025: USD 13.35 Billion

-

Market Size by 2035: USD 29.47 Billion

-

CAGR: 8.24% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Intravenous (IV) Solutions Market - Request Free Sample Report

Intravenous (IV) Solutions Market Trends

-

Growing chronic disease prevalence increases reliance on intravenous therapy in hospitals.

-

Rising surgeries and critical care needs drive higher IV solutions consumption.

-

Paediatric and geriatric patient populations boost parenteral nutrition demand globally.

-

Expansion of home healthcare increases adoption of portable and user-friendly IV devices.

-

Pre-mixed and easy-to-administer IV solutions enhance treatment efficiency and patient safety.

-

Remote and outpatient IV therapy adoption creates new growth opportunities for manufacturers.

U.S. Intravenous (IV) Solutions Market Insights:

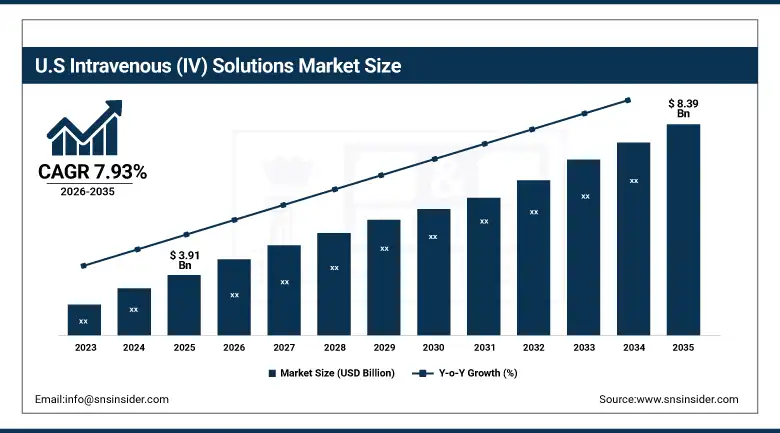

The U.S. Intravenous (IV) Solutions Market size was USD 3.91 Billion in 2025 and is expected to reach USD 8.39 Billion by 2035, growing at a CAGR of 7.93% over the forecast period of 2026-2035, driven by advanced healthcare infrastructure, high adoption of innovative IV therapies, strong hospital networks, and growing demand for nutritional support, fluid management, and critical care across hospitals and home healthcare settings.

Intravenous (IV) Solutions Market Growth Drivers:

-

Rising Chronic Diseases Accelerate Demand for Intravenous Solutions Worldwide Rapidly

Intravenous (IV) Solutions Market growth is due to incidence of chronic diseases such as cancer, cardiovascular disorders, kidney failure, and malnutrition is a primary driver for the IV Solutions Market. Patients with these conditions often require parenteral nutrition, fluid replacement, and electrolyte balance, which can only be administered effectively via intravenous solutions. Increasing hospital admissions, surgeries, and critical care requirements for paediatric and geriatric populations further fuel demand. Healthcare providers are increasingly relying on IV therapy as a standardized treatment, making it a major growth driver for the market.

In Gaza, over 54,600 children under 5 are acutely malnourished, with more than 12,800 severely affected, underscoring the need for IV nutrition support.

Intravenous (IV) Solutions Market Restraints:

-

Contamination Risks and Adverse Reactions Challenge IV Solutions Market Growth

Risks of contamination, infections, and adverse reactions owing to improper handling or administration would restrain the market. Infectious diseases may develop with intravenous (IV) solutions contaminated by bacteria, resulting in bloodstream infections, sepsis, or severe complications in immunocompromised patients. The potential risk, when handling the product, has led to stringent regulatory guidelines and quality checks which can increase the manufacturing costs and hamper product distribution. The high initial cost associated with the training, sterilization, and monitoring systems in hospitals, delay the rapid market growth in emerging regions, as hospital and home care provider are investing heavily in these services.

Intravenous (IV) Solutions Market Opportunities:

-

Home Healthcare Expansion Unlocks Lucrative Market for Portable IV Solutions

Home healthcare and outpatient IV dedicated to both are fast growing and represents an opportunity for market penetration. Reduced need of hospital stay and low cost made patients to prefer home IV therapy. This presents an opportunity for companies to develop portable IV infusion devices, pre-mixed solutions, and user-friendly administration kits that facilitate self-administration and help with remote monitoring. The expanding market for IV home therapy is proving to be a goldmine for manufacturers.

Over 60% of patients express preference for receiving IV therapy at home to reduce hospital visits and associated costs.

Intravenous (IV) Solutions Market Segmentation Analysis:

-

By Type: In 2025, Total parenteral nutrition led the market with a share of 65.10%, while Peripheral parenteral nutrition is the fastest-growing segment with a CAGR of 8.90%.

-

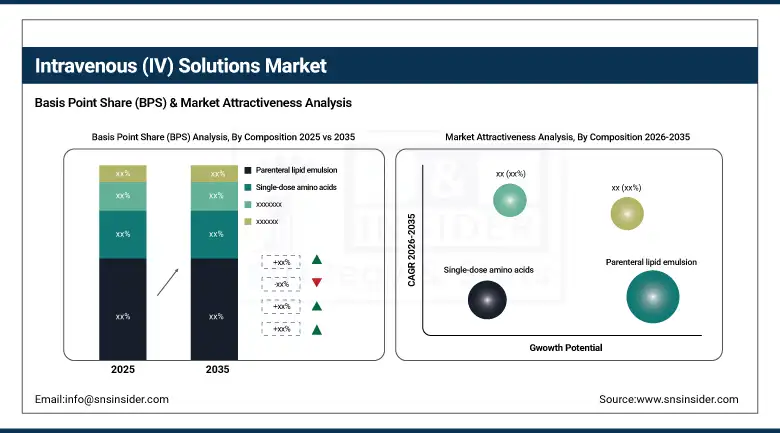

By Composition: In 2025, Parenteral lipid emulsion led the market with a share of 32.60%, while Single-dose amino acids is the fastest-growing segment with a CAGR of 9.20%.

-

By Application: In 2025, Nutritional support led the market with a share of 55.60%, while Fluid and electrolyte balance is the fastest-growing segment with a CAGR of 8.70%.

-

By End Use: In 2025, Hospitals and clinics led the market with a share of 70.20%, while home care settings is the fastest-growing segment with a CAGR of 9.50%.

By Type, Total parenteral nutrition Lead Market and Peripheral parenteral nutrition Fastest Growth

The Total parenteral nutrition leads the market in 2025, due to its extensive use in hospitals, clinics, and home care settings for patients requiring complete nutritional support. Its widespread adoption is driven by increasing prevalence of chronic illnesses, post-surgical recovery needs, and critical care requirements. Meanwhile, Peripheral parenteral nutrition is the fastest-growing segment, supported by rising awareness of targeted, short-term nutritional therapies, convenience of peripheral administration, and growing adoption in ambulatory and home healthcare facilities.

By Composition, Parenteral lipid emulsion Lead Market and Single-dose amino acids Fastest Growth

The Parenteral lipid emulsion leads the market in 2025, due to its essential role in providing high-calorie nutritional support to critically ill and malnourished patients. Its extensive use in hospitals and clinics is driven by the increasing demand for complete parenteral nutrition formulations. Meanwhile, Single-dose amino acids represent the fastest-growing segment, fueled by the rising need for precise, patient-specific amino acid supplementation, ease of administration, and growing adoption in home healthcare and specialty medical facilities.

By Application, Nutritional support Lead Market and Fluid and electrolyte balance Fastest Growth

The Nutritional support leads the market in 2025, due to the growing prevalence of chronic diseases, malnutrition, post-surgical recovery needs, and critical care requirements. Hospitals and clinics extensively use nutritional IV solutions to provide complete patient support, driving steady demand. Meanwhile, Fluid and electrolyte balance is the fastest-growing application segment, supported by increasing cases of dehydration, electrolyte imbalances, and critical care interventions, along with rising awareness of preventive and supportive intravenous therapies in ambulatory and home care settings.

By End Use, Hospitals and clinics Lead Market and Home care settings Fastest Growth

The Hospitals and clinics lead the market in 2025, due to the high demand for IV solutions in critical care, surgical procedures, and chronic disease management. Hospitals and clinics remain the primary users because of their well-established infrastructure, trained medical staff, and the need for continuous patient monitoring. Meanwhile, Home care settings represent the fastest-growing segment, driven by the increasing preference for at-home treatment, rising awareness of home-based healthcare services, and the convenience of administering IV therapy outside traditional medical facilities.

Intravenous (IV) Solutions Market Regional Analysis:

North America Intravenous (IV) Solutions Market Insights:

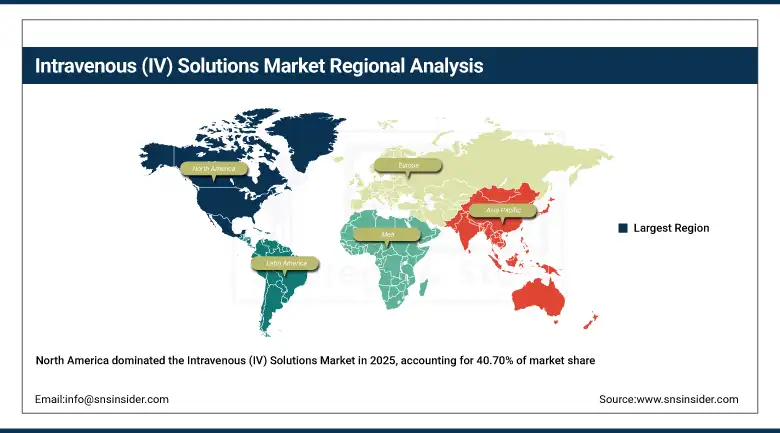

In 2025, North America is expected to hold over 40.70 % of the revenue share in the Intravenous (IV) Solutions Market as it is characterized by advanced healthcare infrastructure, high rate of chronic and critical illness prevalence, along with intense government funding for healthcare. Due to well-established protocols for nutritional support, fluid management, and critical care, hospitals and clinics consume most of the IV solution The region is characterized by faster adoption of advance IV technologies such as pre-mixed solutions, smart infusion pumps, and automated compounding systems. Moreover, growing awareness of home healthcare and outpatient IV therapy is further driving the expansion of the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Intravenous (IV) Solutions Market Insights:

U.S and Canada hold the dominant share of the Intravenous (IV) Solutions market due to better healthcare infrastructure, adoption of innovative IV technologies, dense hospital networks and significantly high health care expenditure. High penetration in critical care, surgical, and home healthcare units, along with favorable government measures keep the region as a consistent market leader.

Asia Pacific Intravenous (IV) Solutions Market Insights:

The Asia-Pacific region is expected to have the fastest-growing CAGR 9.46%, driven by rising healthcare expenditure, expanding hospital and clinic infrastructure, and increasing awareness of advanced IV therapies. The demand for nutritional support, fluid management, and critical care applications is growing rapidly due to a rising patient population and increasing prevalence of chronic illnesses. Adoption of pre-mixed solutions, smart infusion pumps, and home-based IV therapy is accelerating. Strategic investments by key market players in distribution, manufacturing, and technological advancements are further fueling market growth across healthcare facilities and home care settings throughout the region.

China and India Intravenous (IV) Solutions Market Insights:

China and India are the fastest-growing markets for Intravenous (IV) Solutions due to increasing healthcare investment, expanding hospital and clinic infrastructure, and rising awareness of IV therapies. Growing patient populations, higher prevalence of chronic illnesses, and the adoption of home-based and advanced IV solutions further accelerate market growth in these regions.

Europe Intravenous (IV) Solutions Market Insights:

High adoption of advance healthcare technologies and strong hospital infrastructure makes Europe a prominent market for Intravenous (IV) Solutions. The bulk of IV solution consumption happens in hospitals and clinics to cater to the rising requirement for nutritional support, fluid, and electrolyte management, and critical care applications. Continuous investments in absent pre-mixed IV formulations, smart infusion systems, and automated compounding technologies in the region are driving the development in the area. Moreover, increasing awareness regarding home-based IV therapy is slowly boosting their presence across market systems outside healthcare facilities.

Germany and U.K. Intravenous (IV) Solutions Market Insights:

The U.K. and Germany are growing in the Intravenous (IV) Solutions market due to well-established healthcare systems, increasing demand for nutritional support and critical care, and adoption of advanced IV technologies. Investments in hospital infrastructure, home healthcare services, and government initiatives supporting patient care further drive steady market expansion.

Latin America (LATAM) and Middle East & Africa (MEA) Intravenous (IV) Solutions Market Insights:

The Latin America (LATAM) and Middle East & Africa (MEA) Intravenous (IV) Solutions Market are emerging regions showing steady growth, driven by improving healthcare infrastructure, rising awareness of advanced IV therapies, and increasing demand for nutritional support, fluid management, and critical care applications. Hospitals and clinics remain the primary consumers, while home care settings are gradually gaining traction. Market expansion is supported by strategic initiatives from key players, including investments in distribution networks, technological advancements, and training programs for healthcare professionals.

Intravenous (IV) Solutions Market Competitive Landscape:

Braun Melsungen AG, a prominent player in IV Solutions Market underlines its focus on safety and usability of products. The Nurse Approved-approved solutions are DEHP-free and PVC-free for patient safety and easy handling. Its consistent innovation, ongoing quality-focused efforts, compliance, and adoption in hospitals, clinics, and emerging home-care settings make it a leader.

-

In September 2025, B. Braun received the Nurse Approved Certification for its entire IV Solutions portfolio not made with DEHP or PVC, Plastic Irrigation Containers, and Piperacillin and Tazobactam in DUPLEX® Drug Delivery System, highlighting its commitment to excellence in usability and alignment with nursing practice needs.

ICU Medical, Inc. plays a significant role in the IV Solutions Market with its precision infusion pumps and collaborative ventures. FDA-cleared devices like Plum Solo and Plum Duo enhance accuracy and compatibility with various therapies. Strategic partnerships with global players expand production capacity and distribution, enabling ICU Medical to address growing demand in critical care, home care, and hospital settings worldwide.

-

In April 2025, ICU Medical introduced its new category of infusion devices with FDA clearances of Plum Solo and Plum Duo precision IV pumps, offering ±3% accuracy and compatibility with whole blood and blood products.

Terumo Corporation has strengthened its position in the IV Solutions Market through the launch of innovative injection filter needles and advanced IV infusion devices. The company focuses on improving safety, precision, and patient convenience, catering to hospitals, clinics, and home care. Its technological advancements and strategic initiatives support market growth and adoption of modern IV therapies globally.

-

In January 2025, Terumo launched its Injection Filter Needle, the first step of the INFINO™ Development Program, to extend the choice for hypodermic and intravitreal injections.

Intravenous (IV) Solutions Market Key Players:

-

Baxter International Inc.

-

B. Braun Melsungen AG

-

Fresenius Kabi AG

-

Grifols, S.A.

-

ICU Medical, Inc.

-

Otsuka Pharmaceutical Co., Ltd.

-

Ajinomoto Co., Inc.

-

Terumo Corporation

-

Pfizer Inc.

-

Hospira, Inc.

-

Daiichi Sankyo Company, Limited

-

Hikma Pharmaceuticals PLC

-

Cardinal Health, Inc.

-

Abbott Laboratories

-

Novartis AG

-

Medline Industries, Inc.

-

Chongqing Huapont Pharm Co., Ltd.

-

Shanghai Fuxing Pharmaceutical Co., Ltd.

-

Taisho Pharmaceutical Co., Ltd.

-

CJ Healthcare Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.35 Million |

| Market Size by 2035 | USD 29.47 Million |

| CAGR | CAGR of 8.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Total parenteral nutrition, Peripheral parenteral nutrition) • By Composition (Carbohydrates, Vitamins and minerals, Single-dose amino acids, Parenteral lipid emulsion, Other compositions) • By Application (Nutritional support, Blood transfusion, Fluid and electrolyte balance, Other applications) • By End Use (Hospitals and clinics, Ambulatory surgery centers, Home care settings) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Baxter International Inc., B. Braun Melsungen AG, Fresenius Kabi AG, Grifols S.A., ICU Medical, Inc., Otsuka Pharmaceutical Co., Ltd., Ajinomoto Co., Inc., Terumo Corporation, Pfizer Inc., Hospira, Inc., Daiichi Sankyo Company, Limited, Hikma Pharmaceuticals PLC, Cardinal Health, Inc., Abbott Laboratories, Novartis AG, Medline Industries, Inc., Chongqing Huapont Pharm Co., Ltd., Shanghai Fuxing Pharmaceutical Co., Ltd., Taisho Pharmaceutical Co., Ltd., CJ Healthcare Corporation., and Others. |

Frequently Asked Questions

North America dominated the Intravenous (IV) Solutions Market in 2025.

The Intravenous (IV) Solutions Market is projected to be dominated by the crystalloid solutions segment during the forecast period due to their widespread use in fluid resuscitation, electrolyte balance, and routine clinical treatments.

The major growth factor of the Intravenous (IV) Solutions Market is the rising demand for nutritional support, fluid management, and critical care therapies, driven by an increasing prevalence of chronic diseases, surgical procedures, and malnutrition.

The Intravenous (IV) Solutions Market size was USD 13.35 billion in 2025 and is expected to reach USD 29.47 billion by 2035.

The Intravenous (IV) Solutions Market is expected to grow at a CAGR of 8.24% during 2026-2035.

Get in Touch