Semaglutide Market Report Scope & Overview:

The Semaglutide Market was valued at USD 27.79 Billion in 2025 and is expected to reach USD 72.34 Billion by 2035, growing at a CAGR of 10.04% over the forecast period of 2026-2035.

The global semaglutide market is growing very fast as it is more effective than existing treatments for type 2 diabetes and obesity. The primary global semaglutide market trend is that the drug offers substantial weight loss, improved glycemic control, and is the preferred therapy. Moreover, rising insurance penetration and regulatory approvals in North America, Europe, and growth markets are further expanding patient access, driving adoption momentum, with long-term global demand sustained beyond 2025.

For instance, in February 2024, The Lancet published a study showing that semaglutide achieved 15.8% average weight loss, confirming its superior real-world efficacy over other GLP-1 drugs.

Semaglutide Market Size and Forecast:

-

Market Size in 2025: USD 27.79 Billion

-

Market Size by 2035: USD 72.34 Billion

-

CAGR: 10.04% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Semaglutide Market - Request Free Sample Report

Semaglutide Market Trends:

-

Rising prevalence of type 2 diabetes and obesity is driving the semaglutide market.

-

Growing adoption of GLP-1 receptor agonists for glycemic control and weight management is boosting market growth.

-

Expansion of clinical evidence supporting cardiovascular benefits and efficacy is fueling treatment uptake.

-

Increasing awareness of early intervention and personalized diabetes care is shaping prescribing trends.

-

Advancements in oral and injectable formulations are improving patient compliance and convenience.

-

Supportive regulatory approvals and inclusion in treatment guidelines are enhancing market access.

-

Collaborations between pharmaceutical companies, healthcare providers, and research organizations are accelerating innovation and global adoption.

The U.S. Semaglutide Market was valued at USD 17.11 Billion in 2025 and is expected to reach USD 44.34 Billion by 2035, growing at a CAGR of 9.99% over 2026-2035.

The U.S. is the leader in the semaglutide industry, driven by generous insurance coverage and fast uptake through online healthcare platforms, including Ro, Hims, and Calibrate. These services help in buying prescription products for weight control and diabetes.

Semaglutide Market Growth Drivers:

-

Superior Clinical Efficacy is Driving the Semaglutide Market Growth

The growing number of regulatory approvals for semaglutide in various indications is the major factor responsible for the growth of the semaglutide market. Semaglutide was approved first for Type 2 diabetes and more recently for obesity, adolescents, and cardiovascular risk reduction. These extended indications are expanding the semaglutide market share with a much higher reach to the patient pool and bolstering its position in the global market for GLP-1 therapeutics.

For instance, in October 2024, the EMA approved semaglutide (Wegovy) for treating obesity in adolescents aged 12–17, expanding its therapeutic reach.

Semaglutide Market Restraints:

-

Ongoing Supply Shortages are Hampering the Semaglutide Market Growth

An important inhibitor for the semaglutide market growth is the global supply shortage, especially for Wegovy and Ozempic. Because of such high demand and production capacity constraints, many patients experience delays starting or continuing their treatment. This bottleneck has impacted market growth in various regions by constraining the availability to meet a growing demand with a robust clinical and commercial potential.

Semaglutide Market Opportunities:

-

Pediatric and Adolescent Treatments Drive Future Growth Opportunities for the Semaglutide Market

Pediatric and adolescent care aims to establish a safe and efficacious dose of semaglutide for children. Given the increase in childhood obesity and early onset of type 2 diabetes, a focus on this area would have the potential to reduce future morbidity. There will be momentum in the semaglutide market among the under-treated once an age-appropriate therapy is introduced.

For instance, in March 2024, the World Obesity Federation reported that over 650 million adults are obese globally, increasing demand for weight management treatments like semaglutide.

Semaglutide Market Segmentation Analysis:

-

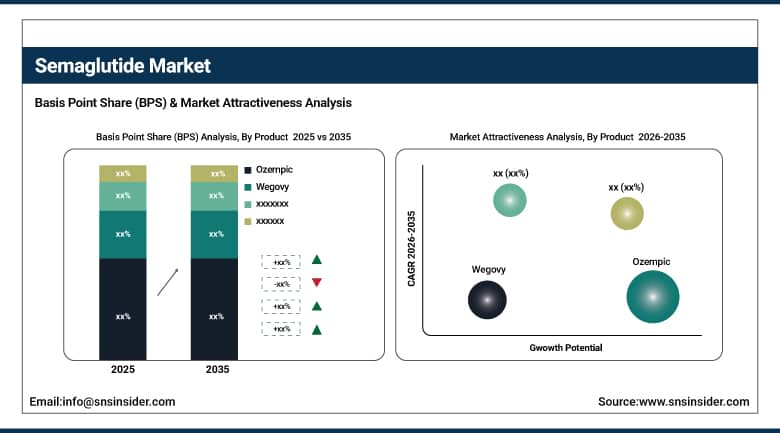

By product, Ozempic held the largest share of around 60.94% in 2025, and the Wegovy segment is expected to register the highest growth

-

By route of administration, the parenteral segment dominated the market with approximately 88.80%share in 2025, while the oral segment is expected to register the highest growth

-

By application, type 2 diabetes mellitus accounted for the leading share of nearly 70.40% in 2025, and obesity is expected to register the highest growth

-

Distribution channel, the retail pharmacies led the market with about 56.61% share in 2025, and online pharmacies are forecasted to grow the fastest

By Product, Ozempic leads the Market, While Wegovy registers the Fastest Growth

The Ozempic segment accounted for the highest revenue share of approximately 60.94% in 2025, owing to its established effectiveness in treating type 2 diabetes, its potential for reducing cardiovascular risk, and the convenience of a once-a-week dosing schedule.

In comparison, the wegovy segment is anticipated to achieve the highest CAGR of nearly 10.86% during the 2026–2035 period, driven by its FDA and EMA approval for chronic weight management in adults and adolescents. The increasing prevalence of global obesity, combined with the substantial real-life effectiveness and celebrity-fueled awareness, drives demand.

By Route of Administration, the Parenteral Segment dominates, while the Oral Segment Shows Rapid Growth

The parenteral segment held the largest revenue share of approximately 88.80% in 2025, due to semaglutide being currently only available in injectable over. Its high bioavailability, fast onset of action, and the physician’s familiarity with subcutaneous administration favor its broad utilization.

On the other hand, the oral segment is predicted to grow at the strongest CAGR of approximately 10.88% during 2026–2035, which is being fueled by the growing preference for non-invasive treatment, including Rybelsus. It is attractive to patients phobic of needles, and aids adherence and access.

By Application, Type 2 Diabetes Mellitus Lead, and Obesity Registers Fastest Growth

Type 2 diabetes mellitus accounted for the largest share of the semaglutide market with about 70.40%, driven by the drug’s demonstrated reduction in HbA1c, weight loss, and cardiovascular risk. As the prevalence of diabetes is increasing globally, semaglutide’s durable GLP-1 action. In addition, obesity is slated to grow at the fastest rate with a CAGR of around 10.83% throughout the forecast period of 2026–2035, owing to the rising global obesity prevalence and the drug’s effectiveness for substantial weight reduction. Wegovy's FDA approvals and the increasing prevalence of health issues related to obesity.

Distribution Channel, Retail Pharmacies Lead, And Online Pharmacies Grow the Fastest

The retail pharmacies held the largest revenue share of around 56.61% in the semaglutide market in 2024, owing to easy availability, robust distribution, and increasing consumer inclination for easy prescription refill orders.

The online pharmacies segment, however, is projected to register the highest CAGR of around 11.49% during the forecast period of 2025-2032, fuelled by the growing digital acceptance, ease, private buying, and broader telemedicine. The increasing prevalence of obesity and diabetes is driving patients toward more convenient treatments, including Ozempic and Wegovy.

Semaglutide Market Regional Insights:

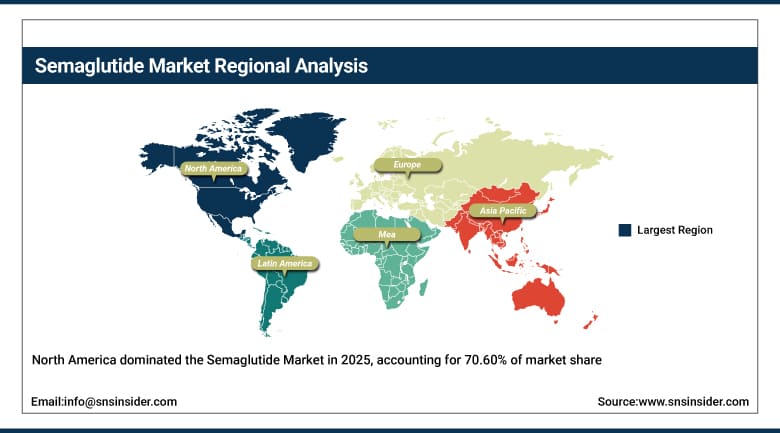

North America Semaglutide Market Insights

North America accounted for the highest revenue share of approximately 70.60% in 2025 of the semaglutide market, owing to the high rates of obesity and type 2 diabetes, especially in the U.S. Robust healthcare systems, the early uptake of innovative GLP-1 therapies including Ozempic and Wegovy, and favorable reimbursement are additional elements that help maintain market leadership. Aggressive direct-to-consumer marketing, increasing access campaigns, and strong regulatory approvals expedite regional adoption as well.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Semaglutide Market Insights

Asia Pacific emerges as the fastest-growing region with the highest CAGR of 11.71%, as a result of an explosion of type 2 diabetes and obesity, particularly in countries including China, India, Japan, and South Korea. Urbanization, immobility, and diet are increasing the incidence of diseases. In addition, an increase in healthcare spending, increased insurance coverage, and the increasing recognition of GLP-1 therapies, including semaglutide, are increasing demand.

Europe Semaglutide Market Insights

The second largest revenue share in the semaglutide market is held by Europe, owing to increasing diabetes and obesity cases in countries including Germany, the U.K., and France. Adoption is driven by supportive healthcare systems, physician uptake, and regulatory approvals over the likes of the EMA. Moreover, public health efforts that encourage the use of GLP-1 therapies, alongside growing awareness and access to branded semaglutide products, are further expanding the regional share of the industry.

Latin America (LATAM) and Middle East & Africa (MEA) Semaglutide Market Insights

Semaglutide adoption is growing in Latin America and the Middle East, where obesity and the prevalence of type 2 diabetes are increasing. Health awareness, insurance penetration, and growth in urban healthcare infrastructure favour market growth. The likes of Brazil, Mexico, Saudi Arabia, and the UAE are all set to become significant growth areas with demand for injectable and oral forms of semaglutide rising steadily.

Semaglutide Market Competitive Landscape:

Novo Nordisk is a global leader in diabetes care and obesity management, specializing in innovative biopharmaceuticals, including insulin, GLP-1 analogs, and weight-management therapies. The company emphasizes patient-centric solutions, clinical efficacy, and accessibility, while expanding its semaglutide portfolio to meet growing demand. Novo Nordisk’s focus on research, regulatory approvals, and global distribution strengthens its position in chronic-disease treatment and supports advancements in obesity and metabolic-care solutions worldwide.

-

January 2025: The FDA approved a higher-dose Wegovy injection, boosting obesity treatment effectiveness and expanding Novo Nordisk’s global semaglutide portfolio, meeting rising demand for advanced weight-management therapies.

Eli Lilly is a global pharmaceutical company focused on diabetes, obesity, oncology, immunology, and neuroscience. The company develops innovative therapies that improve patient outcomes and adherence, including oral and injectable solutions. Eli Lilly combines clinical research excellence with scalable manufacturing and global distribution, strengthening its position in chronic-disease management and delivering accessible, effective treatments in high-demand therapeutic areas.

-

August 2024: Positive Phase 3 trial results for oral semaglutide were announced, enhancing patient adherence and convenience, strengthening Eli Lilly’s position in type 2 diabetes and obesity management markets.

Pfizer is a global biopharmaceutical leader engaged in the discovery, development, and commercialization of innovative medicines and vaccines. The company focuses on oncology, immunology, rare diseases, and metabolic disorders, leveraging strategic partnerships to expand access and accelerate growth. Pfizer emphasizes global market expansion, especially in emerging regions, ensuring that novel therapies are accessible while addressing unmet medical needs in diabetes, obesity, and other chronic conditions.

-

November 2024: Pfizer partnered with Biocon to co-develop GLP-1 therapies, including semaglutide biosimilars, targeting emerging markets in Asia and Latin America, expanding access and accelerating market growth.

Semaglutide Market Key Players:

-

Novo Nordisk A/S

-

Eli Lilly and Company

-

Pfizer Inc.

-

Teva

-

Sun Pharma

-

Zydus

-

Cipla

-

Lupin

-

Biocon

-

Intas

-

Catalent

-

Lonza

-

Samsung Biologics

-

CVS

-

Walgreens

-

Walmart

-

Amazon Pharmacy

-

Ro

-

Hims & Hers

-

Calibrate

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.79 Billion |

| Market Size by 2035 | USD 72.34 Billion |

| CAGR | CAGR of 10.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Ozempic, Wegovy, Rybelsus, Others) • By Route of Administration (Parenteral, Oral) • By Application (Type 2 Diabetes Mellitus, Obesity, Others) • By Distribution Channel(Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., Teva, Sun Pharma, Zydus, Cipla, Lupin, Biocon, Intas, Catalent, Lonza, Samsung Biologics, CVS, Walgreens, Walmart, Amazon Pharmacy, Ro, Hims & Hers, Calibrate, and other players. |

Frequently Asked Questions

The Semaglutide Market was valued at USD 27.79 Billion in 2025.

The market is expected to reach USD 72.34 Billion by 2035.

The market is projected to grow at a CAGR of 10.04% over the forecast period from 2026 to 2035.

The market growth is primarily driven by the rising prevalence of obesity and type 2 diabetes, increasing awareness of chronic disease management, and growing demand for advanced therapeutic drugs.

Semaglutide is widely used for the treatment of type 2 diabetes and weight management / obesity treatment.

Get in Touch