Semiconductor Assembly and Packaging Services Market Size

Get More Information on Semiconductor Assembly and Packaging Services Market - Request Sample Report

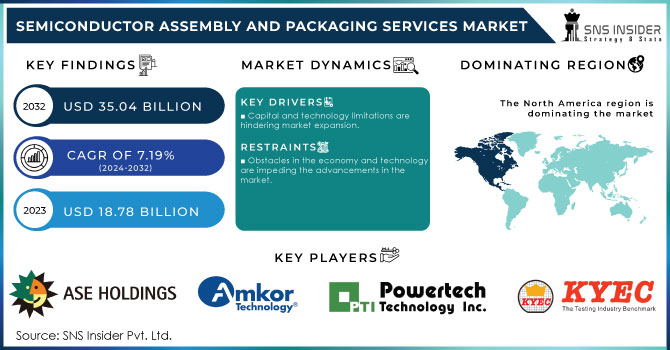

The Semiconductor Assembly and Packaging Services Market size was valued at USD 18.78 Billion in 2023 and expected to reach USD 35.04 Billion by 2032 with a growing CAGR of 7.19% over the forecast period 2024-2032.

There is a significant increase in the Semiconductor Assembly and Packaging Services Market due to the growing need for electronics and the rising complexity of semiconductor devices. With the advancement of technology, there is an increasing demand for innovative packaging solutions that can aid in miniaturization, boost performance, and improve thermal management. Reasons for this increase involve the growth of sectors like automotive electronics, consumer electronics, and telecommunications, which are depending more on advanced semiconductor technologies. Moreover, efforts by governments, like India's production-linked incentive plan, are strengthening local semiconductor production capabilities. This regulatory assistance is intended to lessen reliance on imports and establish India as a leading global center for semiconductors. Businesses are also dedicating resources to researching and developing in order to enhance and streamline assembly and packaging methods.

The market for semiconductor assembly and packaging Services is set to see significant growth, especially with the plan from CG Power and Industrial Solutions Ltd. to launch a ₹7,600 crore outsourced semiconductor assembly and test (OSAT) facility in Sanand, Gujarat. This establishment, collaborating with Renesas Electronics Corporation from Japan and Stars Microelectronics from Thailand, has the goal of manufacturing a maximum of 15 million units per day. The collaboration has been awarded benefits through the India Semiconductor Mission (ISM) initiative, showcasing the Indian government's dedication to enhancing domestic semiconductor production and lessening reliance on imports. The OSAT sector plays a crucial role in the semiconductor value chain by providing important assembly, packaging, and testing Service Type needed for industries like automotive, consumer electronics, and 5G technology. The joint venture intends to produce a variety of products, from traditional packages such as QFN and QFP to more sophisticated packages like FC BGA and FC CSP. The government's backing and investment underscore a substantial move toward improving semiconductor manufacturing in India. by teaming up, well-known companies like CG Power and Renesas aim to boost innovation and enhance effectiveness in the industry to meet the increasing worldwide need for semiconductor products. This strategic move is an important step in positioning India as a strong player in the global semiconductor industry, making a substantial impact on the growth of assembly and packaging Service Type market.

Semiconductor Assembly and Packaging Services Market Dynamics

Drivers

-

Capital and technology limitations are hindering market expansion.

The semiconductor assembly and packaging Service Type sector is confronted with major obstacles because of the considerable initial investment needed to obtain sophisticated equipment such as Fan-Out Wafer-Level Packaging (FOWLP) and Through-Silicon Via (TSV) technologies. These state-of-the-art solutions are vital for guaranteeing optimal efficiency and shrinking in size, especially in fast-expanding fields like AI, 5G, and high-performance computing. Setting up manufacturing facilities that adhere to strict industry regulations requires a large investment, which includes purchasing equipment and creating the infrastructure needed to uphold accuracy and excellence. with ongoing technological advancements, manufacturers need to regularly update their equipment to stay competitive, resulting in higher operational expenses. The intricate nature of these sophisticated packaging procedures also requires a well-trained workforce, increasing labor expenses. Smaller companies struggle to compete with industry giants who have the financial and technological resources to maintain innovations and meet changing market needs. This significant obstacle for new entrants limits competition and hinders innovation in the market, enabling established players to control. Despite the growing demand for semiconductor Service Type in different industries, the obstacles presented by increasing operational costs and other factors are hindering market growth.

Restraints

-

Obstacles in the economy and technology are impeding the advancements in the market.

The Semiconductor Assembly and Packaging Services Market encounters notable obstacles due to the substantial initial investments needed for cutting-edge technologies like Fan-Out Wafer-Level Packaging (FOWLP) and Through-Silicon Via (TSV). These technologies, crucial for meeting the needs of growing industries such as AI, 5G, and high-performance computing, need a significant initial investment to guarantee that production facilities adhere to strict quality and precision criteria. The high costs of establishing modern manufacturing facilities hinder new competitors, reducing competition and stifling innovation in the market. Furthermore, the rapid technological progress requires continuous updates and upkeep of equipment, leading to an increase in operational expenses. The complicated nature of semiconductor packaging procedures requires a proficient staff, leading to increased labor expenses. Due to this, small businesses frequently face challenges in competing against big, established companies with the capabilities to adjust to fast-paced transformations. Although there is increasing need for semiconductor Service Type due to technological advancements, financial and technical obstacles are limiting the market's expansion.

The urgent requirement for supportive policies and investment strategies in the Semiconductor Assembly and Packaging Services Market is emphasized by the interaction of high costs and technological complexity.

Semiconductor Assembly and Packaging Services Market Segment Analysis

by Service Type

In 2023, assembly Service Type became the leading sector in the semiconductor assembly and packaging Service Type market, securing a substantial revenue share of 64.44%. The rise is due to the growing need for high-performance electronic devices, requiring more advanced packaging solutions. Leading firms like Amkor Technology and ASE Group have been actively improving their range of Service Type. Amkor has recently introduced its new 3D Advanced Package Solutions, utilizing innovative packaging technologies to cater to the needs of AI and IoT applications. Likewise, ASE has increased its capability for Fan-Out Wafer-Level Packaging (FOWLP), a technology that aids in shrinking devices and improving performance. The collaboration between CG Power and Renesas Electronics in setting up a new OSAT facility in Gujarat, India, highlights the shift of companies towards investing in assembly Service Type to increase capacity and cater to the expanding market demands. Supported by significant funding and government benefits, the establishment is dedicated to manufacturing various semiconductor packages, emphasizing the significance of assembly Service Type in the market. The emphasis on assembly Service Type not only boosts the quick expansion of consumer electronics but also strategically places companies in the competitive semiconductor industry.

by Application

In 2023, the Semiconductor Assembly and Packaging Services Market saw the consumer electronics sector dominate with a revenue share of 29.44%. The increasing need for cutting-edge electronic devices like smartphones, tablets, and smart home gadgets is fueling this dominance. Samsung Electronics and Apple Inc. are major players in the industry, regularly introducing innovative products that require sophisticated packaging solutions. An example Samsung introduced its newest Galaxy smartphone lineup with improved camera functions and AI integration, using advanced semiconductor packaging to improve performance and efficiency. Apple unveiled the M2 chip, specifically created for their newest MacBook and iPad models, demonstrating a notable enhancement in both speed and power usage. The importance of semiconductor assembly and packaging Service Type in enabling high-performance consumer electronics is highlighted by the successful launch of these products. Moreover, major players in the industry like TSMC are making significant investments in packaging technologies, such as 3D packaging and System-on-Chip (SoC) solutions, to address the changing needs of the consumer electronics market. These advancements show the continuous creativity in the assembly and packaging Service Type sector, highlighting its crucial position in aiding the expansion of the consumer electronics industry.

Semiconductor Assembly and Packaging Services Market Regional Outlook

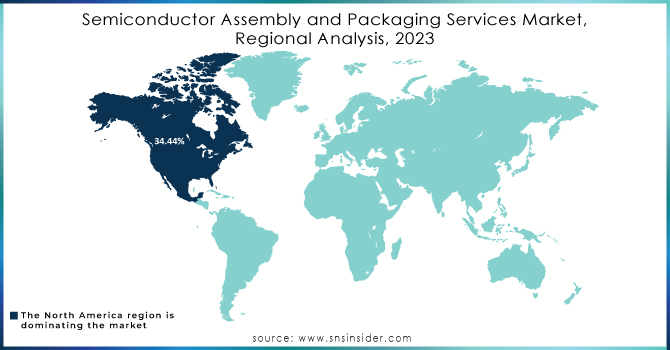

In 2023, North America held the largest market share in semiconductor assembly and packaging Service Type, accounting for 34.44% of total revenue. There are notable advancements happening in the area, especially in the United States, with large investments being made to strengthen semiconductor-manufacturing abilities. The CHIPS and Science Act was passed to dedicate USD 52 billion for semiconductor research and manufacturing in order to boost local production and decrease dependence on international suppliers. Intel and Micron Technology are increasing their activities, with Intel revealing intentions to build new assembly and testing facilities in Arizona. Texas Instruments is increasing its manufacturing presence in Texas to address the growing need for semiconductor packaging solutions in sectors such as automotive and consumer electronics. Canada is also progressing in this industry, as companies such as Denso are setting up packaging operations to meet the increasing demand for automotive semiconductors due to the growing popularity of electric vehicles and advanced driver-assistance systems (ADAS). The cooperation between businesses and governmental organizations in North America is predicted to strengthen the region's position as a leader in the global market for semiconductor assembly and packaging Services.

The Asia-Pacific region is quickly becoming the top market for semiconductor assembly and packaging Services, with a strong demand from industries like consumer electronics, automotive, and telecommunications fueling its growth. Nations such as China, South Korea, and Taiwan are leading the way in this expansion. In China, the government's emphasis on being self-reliant in semiconductor production has resulted in substantial financial backing for domestic firms. For instance, TSMC (Taiwan Semiconductor Manufacturing Company) is increasing the size of its manufacturing and assembly plants in China to improve its production capacities. Similar progress is being seen in South Korea, as Samsung Electronics opens a new assembly and packaging plant in Pyeongtaek to aid in the manufacturing of advanced chips for 5G and AI technology. Furthermore, SK Hynix is increasing its packaging operations in order to keep up with the increasing need for high-performance computing solutions.China's Semiconductor Manufacturing International Corporation (SMIC) has revealed intentions to enhance its advanced packaging capabilities to meet the demands of high-performance uses. These efforts showcase the firm dedication of Asia-Pacific nations to improve their semiconductor assembly and packaging Service Type capabilities, establishing the region as a significant player in the international market.

Need Any Customization Research On Semiconductor Assembly and Packaging Services Market - Inquiry Now

Key Players

Some major companies in the Semiconductor Assembly and Packaging Services Market along with notable products they offer:

-

ASE Technology Holding Co., Ltd. (Advanced Packaging Solutions)

-

Amkor Technology, Inc. (System-in-Package (SiP) Solutions)

-

JCET Group (Integrated Circuit (IC) Packaging)

-

Tianshui Huatian Technology Co., Ltd. (Wafer-Level Packaging)

-

Powertech Technology Inc. (3D IC Packaging)

-

Unisem Group (Flip Chip Packaging)

-

Siliconware Precision Industries Co., Ltd. (SPIL) (Chip-On-Board (COB) Packaging)

-

King Yuan Electronics Co., Ltd. (QFN and BGA Packages)

-

STATS ChipPAC Ltd. (Fan-Out Wafer-Level Packaging (FOWLP))

-

ChipMOS Technologies Inc. (Multi-Chip Package (MCP))

-

UTAC Holdings Ltd. (Lead Frame Packages)

-

Walton Advanced Engineering, Inc. (Microelectronic Packaging)

-

Hana Micron, Inc. (Molded Packaging Solutions)

-

Lingsen Precision Industries, Ltd. (High-Density Packaging)

-

Carsem Malaysia (Automotive and Consumer Electronics Packaging)

-

Celestica Inc. (Electronics Manufacturing Service Type)

-

Nexperia (Discrete and Logic Devices)

-

Infineon Technologies AG (Power Semiconductors)

-

Rudolph Technologies, Inc. (Yield Management Solutions)

-

ON Semiconductor Corporation (Analog and Power Solutions)

-

Others

Recent Development

-

In January 2024, Foxconn collaborates with HCL Group to set up Chip Packaging Unit in India: Foxconn, a Taiwanese tech company, has joined forces with India's HCL Group to create a semiconductor packaging and testing unit in India. Foxconn has put in $37.2 million to acquire a 40% ownership in this OSAT (Outsourced Semiconductor Assembly and Testing) facility.

-

In July 2024, Infineon and Amkor signed a Memorandum of Understanding to enhance sustainability throughout their semiconductor supply chain. This agreement aims to encourage sustainable practices in designing, packaging, and testing semiconductor products, in line with the companies' goals to minimize environmental effects.

-

In April 2024, ATX Group inaugurated a $55 million plant in Melaka, Malaysia, marking its first facility outside of China and aiming to enhance its semiconductor packaging and test Service Type. This establishment is projected to generate 2,000 employment opportunities and enhance Malaysia's expanding electronics and electrical (E&E) supply chain, strengthening the country's attractiveness as a semiconductor-manufacturing center.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 18.78 Billion |

| Market Size by 2032 | USD 35.04 Billion |

| CAGR | CAGR of 7.19% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Assembly Service Type, Testing Service Type) • By Application (Communication, Computing and networking, Industrial, Consumer electronics, Automotive electronics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ASE Technology Holding Co., Ltd., Amkor Technology, Inc., JCET Group, Tianshui Huatian Technology Co., Ltd., Powertech Technology Inc., Unisem Group, Siliconware Precision Industries Co., Ltd. (SPIL), King Yuan Electronics Co., Ltd., STATS ChipPAC Ltd., ChipMOS Technologies Inc., UTAC Holdings Ltd., Walton Advanced Engineering, Inc., Hana Micron, Inc., Lingsen Precision Industries, Ltd., Carsem Malaysia, Celestica Inc., Nexperia, Infineon Technologies AG, Rudolph Technologies, Inc., ON Semiconductor Corporation, and others. |

| Key Drivers | • Capital and technology limitations are hindering market expansion. |

| RESTRAINTS | • Obstacles in the economy and technology are impeding the advancements in the market. |

Frequently Asked Questions

Ans: The Assembly services segment dominated the Semiconductor Assembly and Packaging Services Market.

Ans: The major growth factor of the Semiconductor Assembly and Packaging Services Market is the increasing demand for advanced packaging technologies driven by the rapid expansion of applications in sectors such as consumer electronics, automotive, AI, and 5G.

Ans: The Semiconductor Assembly and Packaging Services Market grow at a CAGR of 7.19% over the forecast period of 2024-2032.

Ans: North America dominated the Semiconductor Assembly and Packaging Services Market in 2023

Ans: The Semiconductor Assembly and Packaging Services Market size was valued at USD 18.78 Billion in 2023 and it is expected to reach USD 35.04 Billion by 2032

Get in Touch