Semiconductor Device Market Size

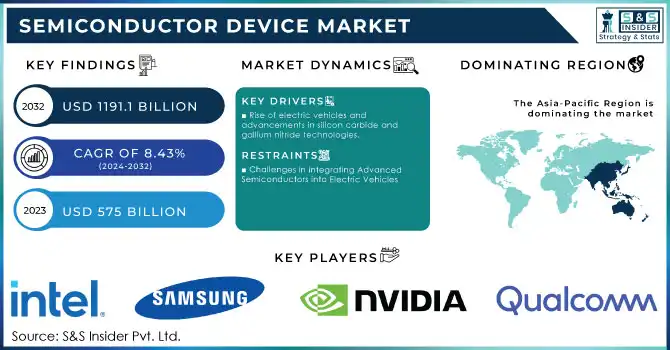

The Semiconductor Device Market Size was valued at USD 575 Billion in 2023 and is expected to reach USD 1191.1 Billion by 2032, and grow at a CAGR of 8.43% over the forecast period 2024-2032.

The semiconductor device market is set to witness substantial growth, fueled by advancements in IoT, AI, and related technologies. IoT adoption across industrial, automotive, and consumer sectors is driving demand for high-performance and energy-efficient semiconductor components.

Get More Information on Semiconductor Device Market - Request Sample Report

Sectors like smart home automation and industrial IoT solutions are expected to lead this surge. Similarly, AI advancements, including machine learning and edge computing, demand cutting-edge hardware like GPUs and custom AI processors, further strengthening the market. AI’s role in hardware optimization could allow the semiconductor sector to capture up to 50% of the AI technology stack’s total value, as compared to 10-30% in other domains, per Redline Group.

The automotive sector, particularly electric vehicles (EVs) and autonomous driving, significantly contributes to growth. EVs, which rely on semiconductors for power management and sensors, are expanding, communication technologies like 5G, essential for. Industry leaders like Mediate are propelling innovation with products such as the Dimensity 9400 chipset, which supports generative AI and gaming applications, showcased alongside 5G and IoT technologies at the "Technology Diaries" event, achieving a 3% market penetration rate. Satellite IoT applications and CubeSats are revolutionizing connectivity, offering low-latency communication in underserved regions and driving innovation in agricultural sensors. These innovations underscore the semiconductor market’s critical role in powering transformative technologies across AI, IoT, automotive, and beyond, cementing its growth trajectory.

Semiconductor Device Market Dynamics

Drivers

-

Rise of electric vehicles and advancements in silicon carbide and gallium nitride technologies.

The rapid adoption of electric vehicles (EVs) is a critical driver for the semiconductor device market, as EVs depend on advanced semiconductor technologies for electric drivetrains, battery management systems, power inverters, and charging infrastructure. The semiconductor content in EVs significantly surpasses that of traditional internal combustion engine vehicles, Fueled by regulatory mandates for carbon neutrality and growing consumer preference for sustainable transportation, leading to a sharp rise in demand for silicon carbide (SiC) and gallium nitride (GaN) semiconductors. These materials offer superior energy efficiency, faster switching speeds, and enhanced thermal performance, making them indispensable for EVs.Silicon carbide technology is transforming power electronics by enabling faster charging, higher power density, and better thermal management. Advanced SiC power semiconductors are expected to boost EV powertrain efficiency by 10–15%, extending driving range and minimizing energy loss. Similarly, innovations such as silicon anode batteries, capable of ultra-fast charging—delivering up to 186 miles of range in just five minutes—are driving demand for state-of-the-art semiconductor solutions. Moreover, the expansion of EV charging infrastructure, including "plug-and-charge" and AI-driven systems, is creating additional opportunities for semiconductor devices in communication and energy management systems. Leading companies such as Tesla, BYD, and Charge Point are incorporating these innovations to meet the evolving demands of the EV ecosystem, the semiconductor device market is poised for unprecedented growth. This expansion not only supports advancements in sustainable mobility but also reshapes the global automotive and energy landscapes, cementing the role of semiconductors as a cornerstone of future technologies.

Restraints

-

Challenges in Integrating Advanced Semiconductors into Electric Vehicles

The integration of advanced semiconductor technologies into electric vehicle (EV) systems presents several market restraints that could impact the pace of EV adoption. One of the main challenges lies in the compatibility between new semiconductor technologies and existing automotive systems. As automotive manufacturers incorporate silicon carbide (SiC) and gallium nitride (GaN) semiconductors, ensuring seamless integration with legacy systems becomes a critical concern. These next-generation semiconductors offer better power efficiency and thermal management, but their integration into complex EV systems requires high-level engineering expertise. The need for precise calibration to ensure that these new semiconductor components function effectively with established systems can significantly delay product development timelines.

Moreover, manufacturing challenges also play a major role. Advanced semiconductor components, especially SiC and GaN, require new, highly specialized fabrication processes that are not only expensive but also limited in production capacity. This results in supply chain bottlenecks, which are exacerbated by the ongoing semiconductor shortages. Additionally, manufacturers must contend with issues related to testing and validation of these materials in high-performance applications, such as EV drivetrains and battery management systems., highlighting the increasing importance of these technologies but also raising the stakes in terms of efficient production and integration.

The introduction of chiplets, a technology designed to enable modular semiconductor designs, is also reshaping the landscape but introduces new complexities in system integration and testing. These innovations aim to revolutionize semiconductor design and manufacturing but add layers of difficulty in terms of scalability and standardization across EV manufacturers. Thus, the challenges related to the integration, testing, and scaling of advanced semiconductor technologies remain a significant restraint for the EV sector’s growth, potentially delaying the widespread adoption of next-gen EVs.

Semiconductor Device Market Segment Analysis

By Device

Integrated circuits (ICs) dominate the semiconductor device market, accounting for around 40% of revenue in 2023. Their widespread use across industries like consumer electronics, automotive, telecommunications, and industrial automation contributes to this market share. ICs are critical for devices such as smartphones, computers, home appliances, and EVs, due to their compact size, efficiency, and ability to integrate multiple functions on a single chip. Their demand is particularly strong in consumer electronics, automotive (including electric drivetrains and ADAS), and emerging technologies like 5G and IoT. Despite challenges such as supply chain disruptions and high manufacturing costs, advancements in fabrication techniques ensure ICs remain vital, with continuous innovation maintaining their leadership in the semiconductor market.

By End-User Application

In 2023, the consumer segment captured the largest share of the semiconductor device market, accounting for around 34% of the revenue. This dominance is primarily driven by the widespread use of semiconductors in consumer electronics such as smartphones, laptops, tablets, smart TVs, and wearables. The increasing demand for more powerful, efficient, and compact devices continues to fuel the growth of semiconductor technologies. As consumer preferences evolve toward higher performance, connectivity, and advanced features, semiconductors play a crucial role in enabling innovations like 5G connectivity, AI integration, and enhanced processing power. The consumer electronics sector's rapid technological advancements ensure that it remains the largest end-user of semiconductor devices, sustaining robust market growth.

Semiconductor Device Market Regional Outlook

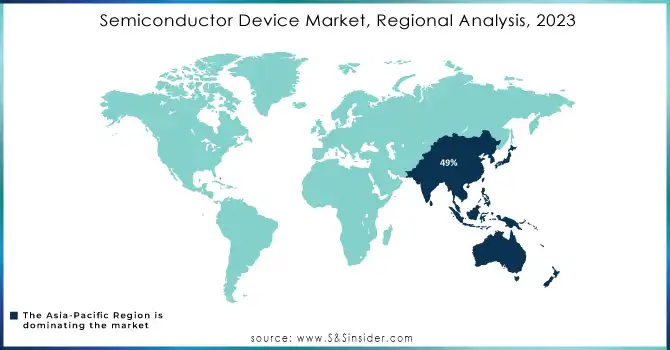

In 2023, the Asia-Pacific region dominated the semiconductor device market, capturing around 49% of the revenue. This is largely attributed to the region's strong semiconductor manufacturing base, with countries like China, South Korea, Japan, Taiwan, and Singapore being key players. Asia-Pacific is home to major semiconductor companies, such as Taiwan Semiconductor Manufacturing Company (TSMC), Samsung, and SK Hynix, which lead global production. The region’s well-established supply chain, coupled with advanced semiconductor fabrication technologies, enables it to meet the growing demand from various industries, including consumer electronics, automotive, and telecommunications. Furthermore, the expansion of 5G networks, the rise of electric vehicles, and the growing adoption of IoT devices in Asia-Pacific further boost the demand for semiconductors. With its dominant position in production and technological advancements, Asia-Pacific is expected to continue leading the semiconductor market in the coming years.

In 2023, North America emerged as the fastest-growing region in the semiconductor device market, driven by significant investments in technology, research and development, and infrastructure. The United States, in particular, plays a crucial role, hosting major semiconductor companies such as Intel, Qualcomm, and Micron Technology. The region is experiencing a surge in demand for semiconductor devices across industries, including automotive, consumer electronics, and industrial automation. The push for electric vehicles (EVs), autonomous driving, and 5G infrastructure has accelerated the need for advanced semiconductor technologies in North America. Additionally, government initiatives like the CHIPS Act aim to boost domestic semiconductor manufacturing and reduce reliance on imports, further fueling market growth. With its focus on innovation and infrastructure development, North America is expected to maintain its position as a key growth driver in the global semiconductor market.

Need Any Customization Research On Semiconductor Device Market - Inquiry Now

Key Players

Some of the major players in Semiconductor Device market with their product:

-

Intel Corporation (Microprocessors, Integrated Circuits)

-

Samsung Electronics (Memory Chips, Processors, Display Drivers)

-

Taiwan Semiconductor Manufacturing Company (TSMC) (Foundry Services, Integrated Circuits)

-

NVIDIA Corporation (Graphics Processing Units (GPUs), AI Processors)

-

Qualcomm Incorporated (Mobile Processors, Modems, RF Chips)

-

Advanced Micro Devices, Inc. (AMD) (Microprocessors, GPUs, System-on-Chip (SoC))

-

Broadcom Inc. (Semiconductor Components, Network and Broadband Chips)

-

Texas Instruments Incorporated (Analog Semiconductors, Processors, Sensors)

-

Micron Technology, Inc. (Memory Chips, DRAM, NAND Flash)

-

Infineon Technologies AG (Power Semiconductors, Sensors, Automotive Chips)

-

STMicroelectronics N.V. (Microcontrollers, Power Devices, Sensors)

-

Analog Devices, Inc. (Signal Processing Chips, Sensors, Amplifiers)

-

NXP Semiconductors N.V. (Automotive Chips, Security ICs, Processors)

-

Renesas Electronics Corporation (Microcontrollers, Automotive Chips, Power Semiconductors)

-

ON Semiconductor Corporation (Power Management ICs, Sensors, Automotive Semiconductors)

-

MediaTek Inc. (Mobile SoCs, Wireless Chips, Smart TV Chips)

-

ASML Holding N.V. (Photolithography Machines, Semiconductor Equipment)

-

Maxim Integrated Products, Inc. (Analog ICs, Power Management Chips, Sensors)

-

Sony Corporation (Image Sensors, Semiconductor Devices for Consumer Electronics)

-

KLA Corporation (Semiconductor Process Control Equipment, Metrology Systems)

List of companies that supply raw materials for the semiconductor device market:

-

Dow Inc.

-

DuPont de Nemours, Inc.

-

Air Products and Chemicals, Inc.

-

BASF SE

-

JSR Corporation

-

Tokyo Ohka Kogyo Co., Ltd. (TOK)

-

Wacker Chemie AG

-

Linde plc

-

Momentive Performance Materials

-

Heraeus Group

Recent Development

-

January, 2024: Intel unveiled its new Intel Core 14th Gen processors at CES 2024, introducing the flagship Intel Core i9-14900HX with 24 cores, designed for gamers, creators, and professionals. The launch also includes the Intel Core mobile processor Series 1, offering efficient, balanced performance for mainstream mobile users with thin-and-light devices.

-

November , 2024: Samsung Electronics completed the installation of equipment for its next-generation semiconductor R&D complex, NRD-K, at the Giheung Campus.

-

January, 2024: NVIDIA unveiled the GeForce RTX 40 SUPER Series GPUs, including the RTX 4080 SUPER, RTX 4070 Ti SUPER, and RTX 4070 SUPER, designed to enhance gaming and creative experiences with AI-powered features. Starting at $599, these GPUs deliver up to 52 shader TFLOPS and 836 AI TOPS, offering superior performance for next-gen games and creative applications.

-

November, 2024: AMD's Ryzen 7 7800X3D has been praised as the best gaming CPU, outperforming Intel's top models in gaming frame rates while being more power-efficient and cost-effective.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 575 Billion |

| Market Size by 2032 | USD 1191.1 Billion |

| CAGR | CAGR of 8.43% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device Type (Discrete Semiconductors, Optoelectronics, Sensors, Integrated Circuits) • By End-User Application (Automotive, Communication (Wired and Wireless), Consumer, Industrial, Computing/Data Storage, Government (Aerospace & Defense)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Intel Corporation, Samsung Electronics, Taiwan Semiconductor Manufacturing Company (TSMC), NVIDIA Corporation, Qualcomm Incorporated, Advanced Micro Devices (AMD), Broadcom Inc., Texas Instruments Incorporated, Micron Technology Inc., Infineon Technologies AG, STMicroelectronics N.V., Analog Devices Inc., NXP Semiconductors N.V., Renesas Electronics Corporation, ON Semiconductor Corporation, MediaTek Inc., ASML Holding N.V., Maxim Integrated Products Inc., Sony Corporation, and KLA Corporation are key players in the semiconductor device market. |

| Key Drivers | • Rise of electric vehicles and advancements in silicon carbide and gallium nitride technologies. |

| Restraints | • Challenges in Integrating Advanced Semiconductors into Electric Vehicles. |

Frequently Asked Questions

Ans: Intel Corporation, Samsung Electronics, Taiwan Semiconductor Manufacturing Company (TSMC), NVIDIA Corporation, Qualcomm Incorporated, Advanced Micro Devices (AMD), Broadcom Inc., Texas Instruments Incorporated, Micron Technology Inc., Infineon Technologies AG, STMicroelectronics N.V., Analog Devices Inc., NXP Semiconductors N.V., Renesas Electronics Corporation, ON Semiconductor Corporation, MediaTek Inc., ASML Holding N.V., Maxim Integrated Products Inc., Sony Corporation, and KLA Corporation are key players in the semiconductor device market.

Ans: Major trends include the growth of AI and machine learning, the expansion of 5G networks, increased use of semiconductor devices in electric vehicles, and the continued miniaturization of electronics.

Ans: Asia-Pacific is dominating in Semiconductor Device market.

Ans: The key market driver for the Semiconductor Device Market will be the growing demand for advanced technologies in consumer electronics, automotive, and industrial applications, fueled by innovations in IoT, AI, and 5G.

Ans: The Semiconductor Device Market Size was valued at USD 575 Billion in 2023, and is expected to reach USD 1191.1 Billion by 2032.

Get in Touch