Semiconductor Laser Market Report Scope & Overview:

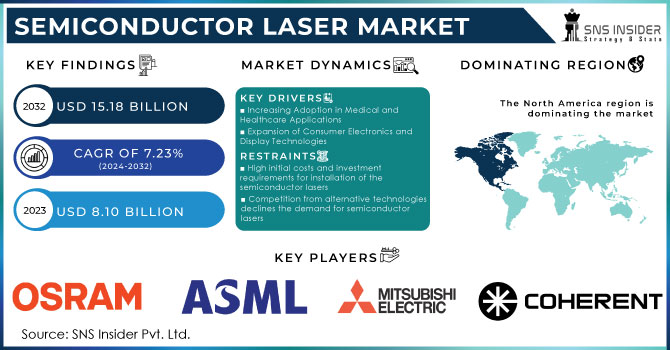

The Semiconductor Laser Market Size was valued at USD 8.10 billion in 2023 and is expected to reach USD 15.18 billion by 2032 and grow at a CAGR of 7.23% over the forecast period 2024-2032.

The semiconductor laser market has been experiencing rapid growth, governed by the progression of technologies, expansion of needs for high-speed data transmission, and a greater variety of electronics with in-built semiconductor lasers. The semiconductor laser market is boosted further by the need for more efficient and space-saving types of lasers, growing investments in R&D, and the increase of semiconductor laser applications in emerging markets, such as LiDAR systems in driverless cars and optical sensors. The US government has allocated over USD 5 billion to its semiconductor R&D sector. This amount is part of the Chips and Science Act as the country seeks to improve its position in the focused area. Moreover, it facilitates a conducive environment for implementing, testing, and building commercial solutions targeted at overcoming critical barriers. The investment comes after an earlier amount of USD 162 million was announced for the specifically invested area.

Semiconductor Laser Market Size and Forecast:

-

Market Size in 2023: USD 8.10 billion

-

Market Size by 2032: USD 15.18 billion

-

CAGR: 7.23% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

Get More Information on Semiconductor Laser Market - Request Sample Report

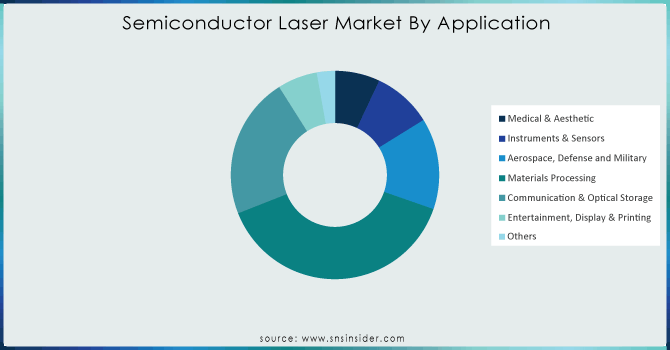

The material processing market is one of the major drivers of the semiconductor laser market and is used in cutting, welding, engraving, and additive manufacturing processes. The volume of the global market for laser systems in materials processing in 2023 is USD 23.5 billion. The high intensity and precision of the semiconductor laser beam allow it to complete tasks without wasting any material. For instance, in selective laser sintering or direct metal laser sintering, laser beams are used to join powdered particles into a solid object. Their precision and non-contact nature mean that they can be used to measure things like the thickness or irregularities of an object and easily locate defects without compromising the product.

Semiconductor Laser Market Trends:

-

Increasing demand for high-speed data transmission and optical communication systems is significantly driving the adoption of semiconductor lasers in telecom and data center applications.

-

Growing usage in consumer electronics, including smartphones, 3D sensing, and facial recognition technologies, is expanding the application scope of semiconductor lasers.

-

Advancements in laser technologies such as quantum cascade lasers and vertical-cavity surface-emitting lasers (VCSELs) are enhancing efficiency, performance, and miniaturization.

-

Rising adoption in industrial applications, including material processing, cutting, welding, and additive manufacturing, is boosting market growth.

-

Expanding use in healthcare for medical diagnostics, imaging, and therapeutic procedures is contributing to increased demand for precision laser solutions.

-

Strong growth in automotive applications, particularly in LiDAR systems for autonomous vehicles and advanced driver-assistance systems (ADAS), is creating new opportunities.

-

Continuous R&D investments and collaborations among semiconductor manufacturers and photonics companies are accelerating innovation and commercialization of next-generation laser technologies.

Market Dynamics

Drivers

-

Increasing Adoption in Medical and Healthcare Applications

The increased adoption of semiconductor lasers is evident in the medical and healthcare industry. These lasers are popular for their high precision, efficiency, and adaptability. Often, they are used in different types of medical applications, including surgery, diagnosis, and therapy. This laser technology can produce highly focused and controllable beams. Optical coherence tomography is an imaging technique deployed in the analysis and examination of the retina and other tissues. In this case, the segment of imaging requires laser technology in terms of operations. The current global status, where chronic illnesses are increasingly reported, requires sophisticated diagnostic tools. In this case, the non-invasive treatment method deploys light-sensitive compounds that are activated by particular wavelengths of light to destroy the target cells. For Example, Photodynamic Therapy (PDT) is effective in the treatment of numerous conditions, including cancer and skin problems, which further justifies the application and the growing demand for semiconductor lasers in the healthcare sector.

-

Expansion of Consumer Electronics and Display Technologies

Consumer electric products like barcode scanners, optical drives, and laser printers are the consumer devices that use semiconductor laser technology. In the retail sector, the increasing popularity of display technologies is contributing to the demand for semiconductor lasers. In particular, smart TV and projector applications characterize the rising demand for high-quality products, people expect their home entertainment systems to have high resolution, bright images, and shaded colors. The laser market can benefit from the demand for AR and VR products as well. Currently, both AR and VR devices are widely used in gaming, education, and many professional areas. However, the technologies require laser sources that are compact and efficient to run; the equipment’s efficiency is necessary since high variability and resolution are needed. To solve these problems, semiconductor lasers can be used to create realistic episodes, and thus they will experience great demand in the future.

Restraints

-

High initial costs and investment requirements for installation of the semiconductor lasers

Manufacturing processes are complicated and require high precision, advanced techniques, and expensive machinery. The use of high-purity semiconductor laser substrates only increases the total investment. For small and medium-sized enterprises, this is a huge barrier. SMEs often do not possess the necessary funding to build top-quality facilities and hire highly professional labor. As a result, many interested players cannot enter the semiconductor laser market. High costs may also prevent certain applications from adopting semiconductor lasers due to the availability of a cheaper alternative.

-

Competition from alternative technologies declines the demand for semiconductor lasers

The competition for the semiconductor laser market arises from alternative laser technologies. Manufacturers of solid-state lasers and fiber lasers have been on the lookout for methods to produce high-power light more efficiently. Both technologies offer advantages over the existing semiconductor lasers that suffer because they are easy to make. In industrial processes, for example, fiber lasers dominate the application because they are robust and very efficient; the high-power levels that they operate at make them vulnerable. At the same time, the beam quality of solid-state lasers makes them superior in providing a stable beam for various applications, including in scientific and medical fields. There is stiff competition in the market for the semiconductor laser led by the existence of alternative better technologies.

Market Segmentation

By Type

The fiber optic lasers led the market segment in 2023 with a market share of over 35.18%. The fiber optic lasers administer stable and accurate focused light beams. Light is transmitted by these laser diodes with the help of fiber optic cables. With the help of increasing, decreasing, and permitting power streams to the diodes, semiconductor lasers work by charging semiconductor chips with power.

The vertical cavity emitting laser is growing with a stable CAGR of 8.61% during 2024-2032. VCSELs are utilized in communication devices and data centers. This is primarily attributed to the rising data center investment and the increasing sale of 5G devices.

By Application

The largest share in 2023 was held by the materials processing segment with a market share of 38.70%. The increased spending in manufacturing automotive component cutting tends to increase demand for industrial cutting, and it is an alternative way of cutting that has potential quality, precision, and precision advantages. In the heavy machinery industry and automotive component manufacturing, laser cutting is mainly used to cut metal of varying sizes. The laser cutting application for material processing is one example of the usage of semiconductor lasers. In this particular situation, a high-powered laser beam is used to melt or vaporize a substance along a predetermined course, which results in a straight, clean cut.

The instruments & sensors segment is projected to grow at the highest CAGR during the projected period 2024-2032. Increased funding across IoT devices will drive market growth on a nearly consistent basis. The rise in the global market is driven by increasing sales of IoT devices as well as the increasing need for devices founded on advanced technology.

Need any customization research on Semiconductor Laser Market - Enquiry Now

Regional Analysis

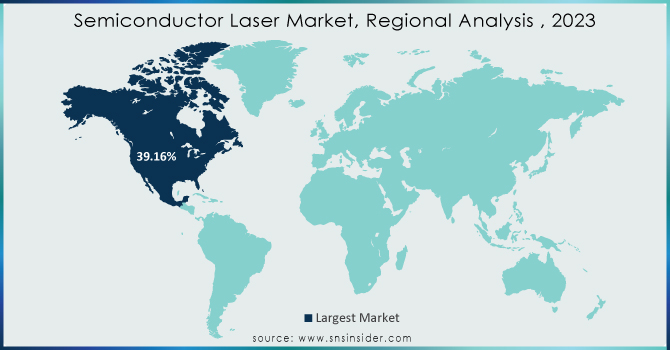

North America is dominating the region with a market share of over 39.16% in 2023. Several factors contribute to this growth, such as the robust semiconductor industry, rising investment in research and development, and a large number of market players in this specific application genre in the market. Moreover, this market dominates because of its technological innovation, high preceding power of laser-based technologies, and high inclination towards advanced application.

The semiconductor laser market in Europe is the second-largest market and growing at significant CAGR of 7.75% for the forecast period. Various factors that contribute to this growth are the increasing impact of laser-based applications in telecommunications, automotive, healthcare, and manufacturing.

Asia-Pacific is also growing fast with a substantial CAGR from 2024-2032. This is mainly because of the expansion of the telecommunications, manufacturing, and healthcare business in the region. Additionally, the semiconductor laser market growth will be influenced by product availability associated with consumer electronics and end-use industry changes toward technological innovation.

Key Players

The key players in the Semiconductor Laser market are Osram Licht AG, ASML Holding NV, Coherent Inc., Mitsubishi Electric, Huaguang Photoelectric, Hans Laser Technology Ltd, Panasonic Corporation, IPG Photonics, Rohm Co. Ltd, Sharp Corp., Axcel Photonics Inc., Trump GmbH, Sumitomo Electric Industries Ltd, ASML Holding, & Other Players.

Recent Development

-

In April 2024, Sony announced the commencement of operations with several production lines at their new fab in Thailand, aiming to increase production capacity and improve efficiency to meet the growing demand for high-performance semiconductor devices.

-

In December 2023, ROHM launched the RLD90QZW8 high-power laser diode, suitable for applications requiring distance measurement and spatial recognition. This laser diode enhances performance and output, crucial for automation technologies like AGVs and AVs.

-

In November 2023, AFRL launched the Semiconductor Laser Indoor Propagation Range (SLIPR) at Kirtland AFB, providing innovative solutions for laser development for the US military.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 8.10 billion |

| Market Size by 2032 | USD 15.18 Billion |

| CAGR | CAGR of 7.23 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (GaN, GAAS, SiC, INP, SIGE, GAP, Others) • By Application (Medical & Aesthetic, Instruments & Sensors, Aerospace, Defense, and Military, Materials Processing, Communication & Optical Storage, Entertainment, Display & Printing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Osram Licht AG, ASML Holding NV, Coherent Inc., Mitsubishi Electric, Huaguang Photoelectric, Hans Laser Technology Ltd, Panasonic Corporation, IPG Photonics, Rohm Co. Ltd, Sharp Corp., Axcel Photonics Inc., Trump GmbH, Sumitomo Electric Industries Ltd, ASML Holding |

| Key Drivers | • Increasing Adoption in Medical and Healthcare Applications • Expansion of Consumer Electronics and Display Technologies |

| RESTRAINTS | • High initial costs and investment requirements for installation of the semiconductor lasers • Competition from alternative technologies declines the demand for semiconductor lasers |

Frequently Asked Questions

Ans: North America is the dominating region in the Semiconductor Laser Market in 2023.

Ans: The material processing segment by application is dominating the Semiconductor Laser Market.

Ans: The increasing adoption of semiconductor lasers in healthcare sector raises the growth of the Semiconductor Laser Market.

Ans: The Semiconductor Laser Market size was USD 8.10 billion in 2023 and is to reach USD 15.18 billion by 2032.

Ans: The Semiconductor Laser Market is to grow at a CAGR of 7.23%.

Get in Touch