Semiconductor Chip Market Report Scope & Overview:

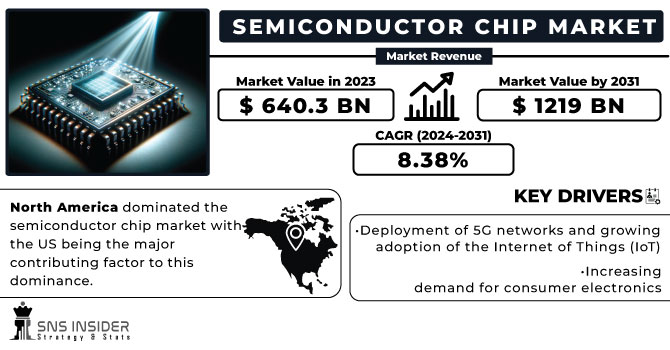

The Semiconductor Chip Market size was valued at USD 640.3 billion in 2023 and is expected to grow to USD 1219 billion by 2031 and grow at a CAGR of 8.38% over the forecast period of 2024-2031.

The semiconductor chip market growth is driven by the increasing demand for advanced technology and the rapid expansion of the digital era. As the world becomes more interconnected, the need for faster, more efficient, and more powerful electronic devices continues to rise. This has led to a surge in the production and consumption of semiconductor chips.

Get More Information on Semiconductor Chip Market - Request Free Sample Report

One of the key factors contributing to the growth of the semiconductor chip market is the continuous innovation and development in the field of microelectronics. Technological advancements have led to the creation of smaller, more powerful, and energy-efficient chips, enabling the production of high-performance electronic devices. This has not only enhanced the functionality of various products but has also opened up new possibilities for industries such as healthcare, telecommunications, and aerospace. Furthermore, the increasing adoption of artificial intelligence (AI), the Internet of Things (IoT), and cloud computing has further fueled the demand for semiconductor chips. These emerging technologies heavily rely on the processing power and data storage capabilities provided by these chips. As a result, the semiconductor chip market is expected to witness substantial growth in the coming years. The industry faces issues such as fluctuating demand, intense competition, and the constant need for research and development. Additionally, geopolitical factors and trade tensions can impact the global supply chain, affecting the production and distribution of semiconductor chips.

A semiconductor chip, also known as an integrated circuit (IC), is a fundamental component in modern electronics. It is a small electronic device made from a semiconductor material, typically silicon, that contains a multitude of electronic components such as transistors, diodes, and resistors. These components are interconnected to perform various functions, including amplification, switching, and memory storage. The semiconductor chip plays a crucial role in the functioning of electronic devices, enabling the processing and transmission of electrical signals. It serves as the brain of computers, smartphones, and countless other devices, allowing them to perform complex tasks efficiently and reliably.

Market Dynamics

Drivers

-

Deployment of 5G networks and growing adoption of the Internet of Things (IoT)

-

Increasing demand for consumer electronics

The increasing demand for consumer electronics serves as the primary driving force behind the semiconductor chip industry. Consumer electronics, such as smartphones, laptops, and televisions, have become an integral part of our daily lives. With each passing day, the demand for these devices continues to surge, fueled by advancements in technology and the ever-growing desire for convenience and connectivity. As a result, the semiconductor chip industry has experienced a significant boost. As more individuals seek to acquire the latest gadgets and upgrade their existing devices, manufacturers must produce a greater quantity of semiconductor chips to meet this demand. This surge in production not only benefits the semiconductor chip industry but also stimulates technological advancements and innovation.

Restrain

-

Increasing complexity and cost associated with developing advanced semiconductor chips

Opportunities

-

Increasing adoption of electric vehicle

The automotive industry's shift towards electric vehicles (EVs) and autonomous driving technologies is driving the demand for semiconductor chips used in advanced driver-assistance systems (ADAS) and in-vehicle infotainment systems. When it comes to the adoption of electric vehicles, Europe and China have emerged as leaders, with a significant proportion of new vehicle sales being electric, ranging from 22-27% in 2022. In contrast, the United States’ adoption of electric vehicles is low as compared to Europe and China, accounting for 6-8% of new vehicle sales.

Challenges

-

The shrinking size of chips, coupled with the need for higher performance

Impact of Russia-Ukraine War:

The ongoing conflict between Russia and Ukraine affected global supply chains, which are already strained due to the pandemic. Of particular concern is the chip shortage, as both nations control significant supplies of key raw materials essential for semiconductor production. Ukraine, in particular, plays a crucial role as it is home to two major suppliers of neon, a vital ingredient in chip manufacturing. Unfortunately, these suppliers, Ingas and Cryoin, have been forced to halt their operations as Moscow intensifies its attack on Ukraine. This war not only threatens to drive up prices but also exacerbates the already critical shortage of semiconductors. It is worth noting that a staggering 56% of the world's semiconductor-grade neon, which is essential for the lasers used in chip production, originates from these two Ukrainian companies. Prior to the invasion, Ingas alone produced an impressive 15,000 to 20,000 cubic meters of neon per month. Their customers spanned across Taiwan, Korea, China, the United States, and Germany, with approximately 72% of their output dedicated to the chip industry.

Impact of Recession:

The semiconductor industry can be heavily impacted by the ongoing recession because it is highly dependent on external economic factors. This is because the industry heavily depends on consumers, who tend to reduce their spending during recessions or financial crises. Consequently, a downturn in the economy can lead to a decrease in demand for semiconductor products. Moreover, such a downturn will disrupt the supply chain by limiting access to raw materials required for production or reducing the availability of workers to fulfill orders. Additionally, semiconductor companies may be compelled to raise their prices due to higher production costs. Furthermore, economic downturns often prompt investors to withdraw their investments from the stock market and other sectors of the economy. A notable example occurred in August 2022 when investors' demand decreased, resulting in a 4.6% decline in the Philadelphia semiconductor index, with all 30 members experiencing losses.

Market segmentation

By Type

-

Logic Chips

-

Microprocessors

-

Microcontrollers

-

-

Memory Chips

-

Random-Access Memory (RAM)

-

Read-Only Memory (ROM)

-

-

Analog Chips

-

Complex Systems-on-a-Chip

-

Application-Specific Integrated Chips (ASICs)

By End-use

-

Automotive

-

Computing

-

Consumer Electronics

-

Wireless Communication

-

Industrial

-

Military

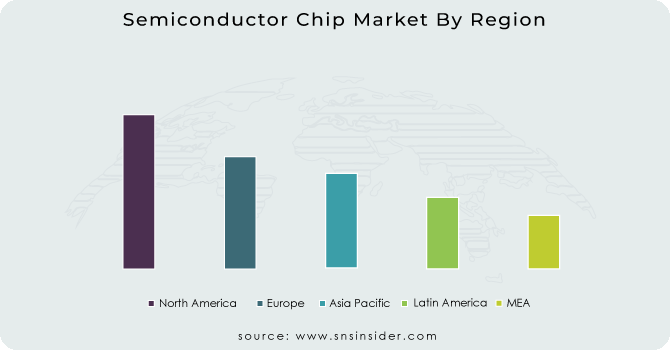

Regional Analysis

North America dominated the semiconductor chip market with the US being the major contributing factor to this dominance. As the leading chip manufacturer, the US has been instrumental in driving the growth of this industry. However, recent developments have raised concerns about the country's diminishing share in the global semiconductor manufacturing landscape. In July 2022, Congress took a significant step to address this issue by passing the CHIPS Act of 2023. This legislation aims to bolster domestic semiconductor manufacturing, design, and research, thereby strengthening both the economy and national security. It also seeks to reinforce America's chip supply chains, which have become increasingly vulnerable due to the country's declining manufacturing capacity.

Over the years, the US has witnessed a decline in its share of modern semiconductor manufacturing capacity, plummeting from 37% in 1990 to a mere 12% in July 2022. This erosion is attributed to the ambitious investments made by other countries governments in chip manufacturing incentives, while the US government has lagged behind in this regard. Moreover, the allocation of federal funds towards chip research has remained stagnant in relation to the country's GDP, whereas other nations have considerably intensified their research endeavors.

To tackle these challenges head-on, the CHIPS Act of 2022 includes provisions for semiconductor manufacturing grants, research investments, and an investment tax credit specifically tailored for chip manufacturing. These measures aim to incentivize and support the growth of the domestic semiconductor industry. Additionally, the Semiconductor Industry Association (SIA) advocates for the implementation of an investment tax credit for semiconductor design, further bolstering the sector's development. By enacting these measures, the US government aims to reclaim its position as a global leader in semiconductor manufacturing and design. The CHIPS Act of 2022 represents a crucial step towards revitalizing the country's chip industry, ensuring its long-term competitiveness, and safeguarding its economic and national security interests.

Need any customization research on Semiconductor Chip Market - Enquiry Now

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of the Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

Key Players

The major key players are Infineon Technologies AG, L3Harris Technologies, QUALCOMM, Intel Corp., NXP Semiconductors, Inc., Kioxia Holdings Corp., Advanced Micro Devices, Inc., Micron Technology Inc., Samsung Electronics Co. Ltd., STMicroelectronics N.V., Texas Instruments Inc., and other key players mentioned in the final report.

Infineon Technologies AG-Company Financial Analysis

Recent Development:

-

In June 2023, Advanced Micro Devices (AMD) unveiled its latest artificial intelligence chip, the MI300X, as part of its ongoing competition with chipmaker Nvidia. This advanced chip is set to revolutionize the field of AI-powered business tools.

-

In April 2023, Infineon Technologies AG and Schweizer Electronic AG joined forces to develop an innovative solution aimed at enhancing the efficiency of silicon carbide (SiC) chips. Their collaborative effort focuses on embedding Infineon's high-performance 1200 V CoolSiC™ chips directly onto printed circuit boards (PCBs). This breakthrough technology not only extends the range of electric vehicles but also reduces overall system costs.

-

In Jan 2023, NXP Semiconductors introduced a 28nm RFCMOS radar one-chip IC family. This pioneering development caters to the needs of next-generation Advanced Driver Assistance Systems (ADAS) and autonomous driving systems, marking a significant milestone in the industry.

-

In Aug 2022, Intel Corporation made an announcement regarding its Semiconductor Co-Investment Program (SCIP). This unique initiative introduces a novel funding model to the capital-intensive semiconductor industry, revolutionizing the way investments are made in this sector.

| Report Attributes | Details |

| Market Size in 2023 | US$ 640.3 Bn |

| Market Size by 2031 | US$ 1219 Bn |

| CAGR | CAGR of 8.38% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Logic Chips, Memory Chips, Analog Chips, Complex Systems-on-a-Chip, and Application-Specific Integrated Chips (ASICs)) • By End-use (Automotive, Computing, Consumer Electronics, Wireless Communication, Industrial, Military, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Infineon Technologies AG, L3Harris Technologies, QUALCOMM, Intel Corp., NXP Semiconductors USA, Inc., Kioxia Holdings Corp., Advanced Micro Devices, Inc., Micron Technology Inc., Samsung Electronics Co. Ltd., STMicroelectronics N.V., Texas Instruments Inc. |

| Key Drivers | • Deployment of 5G networks and growing adoption of the Internet of Things (IoT) • Increasing demand for consumer electronics |

| Market Restraints | • Increasing complexity and cost associated with developing advanced semiconductor chips |

Frequently Asked Questions

ANS: Yes, you can ask for the customization as pas per your business requirement.

Ans: The United States is the leading chip manufacturer, while China is making desperate attempts to dominate the chip market. China has been making exponential investments to enhance its production capacity of microchips and acquire advanced production technology. In contrast, other countries governments have ambitiously invested in chip manufacturing incentives, whereas the U.S. government has not prioritized this area. In response to these challenges, Congress passed the CHIPS Act of 2022.

Ans: Geopolitical tensions and trade disputes between major economies can disrupt the global supply chain, affecting the semiconductor chip market. Additionally, the industry is highly competitive, with numerous players vying for market share, which can lead to price wars and margin pressures.

Ans. The Semiconductor Chip Market is Projected to Reach USD 1219 Bn by 2031.

Ans. The Semiconductor Chip Market is growing at a CAGR of 8.38 % Over the Forecast Period 2024-2031.

Get in Touch