Shingles Vaccine Market Report Scope & Overview:

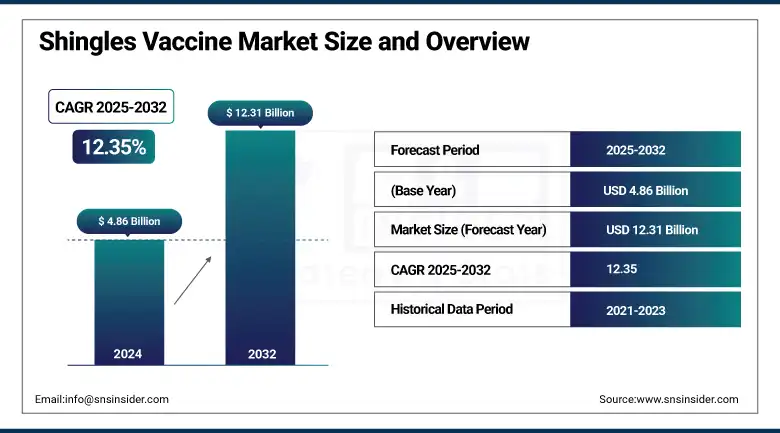

The shingles vaccine market size was valued at USD 4.86 billion in 2024 and is expected to reach USD 12.31 billion by 2032, growing at a CAGR of 12.35% over the forecast period 2025-2032.

Rising incidence of shingles among elderly populations and the inclusion of shingles vaccinations into national immunization campaigns are driving strong expansion of the shingles vaccine market.

For instance, according to the CDC, about 1 in 3 Americans will develop shingles-caused by the reactivation of the varicella virus-in their lifetime, with approximately 1 million new cases reported annually.

Fuelled by the rising incidence of herpes zoster infection among aging populations and the expansion of government-backed immunization programs shingles vaccine market is growing significantly.

The World Health Organisation (WHO) estimates that by 2025, the global population aged 60 will nearly double by 2050, reaching 2.1 billion, hence stressing the need for preventative immunization. Government statistics for the UK show a 31.2% shingles vaccination coverage rate for patients aged 70 and a 74.9% rate for those aged 76 in 2021–2022. The current shingles vaccine market trend revolves mostly around these government-sponsored projects and demographic changes.

To Get more information On Shingles Vaccine Market - Request Free Sample Report

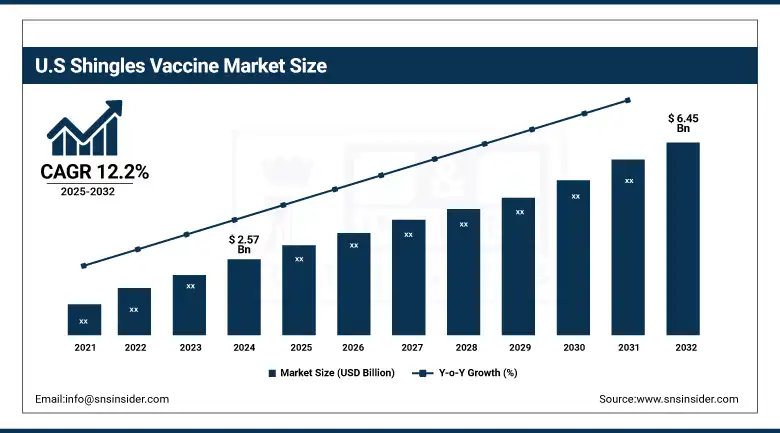

The main causes of the shingles vaccine market growth include changing demographics related to aging and rising illness burden. Utilizing the CDC, the U.S. government stresses shingles vaccination for adults 50 years of age and above; therefore, include it in regular preventative treatment. Reflecting high disease frequency and advanced healthcare infrastructure, the U.S. shingles vaccine market held a commanding 87% share of the North American market in 2024, accounted for USD 2.57 billion in 2024, and is expected to reach USD 6.45 billion by 2032 with a CAGR of 12.2% over the forecast period. Since 2017, around 90 million doses of Shingrix have been given in the U.S.

Shingles vaccines included in national immunization campaigns and advantageous reimbursement policies in the U.S. and Europe have greatly raised coverage and acceptance. Government projects highlighting the momentum of the market include Germany's inclusion of shingles vaccination into its national program and the UK’s robust adult vaccination campaigns.

Market Dynamics

Drivers

-

Government Initiatives and National Immunization Campaigns Are Extending the Availability of the Shingles Vaccination

Crucial factors accelerating the global uptake of shingles vaccines are their inclusion in national immunization campaigns and their execution under strong government support. With the CDC and WHO strongly recommending the use of Shingrix, a recombinant vaccination with over 90% effectiveness, many nations have included shingles vaccination into their official adult immunization schedules.

For patients aged 70, the UK government recorded a 31.2% coverage rate; for patients aged 76, the coverage percentage was 74.9%. The acceptance of SKYZoster by South Korea into its immunization campaign shows even more the worldwide momentum for government-sponsored immunization campaigns. Reiterating its public health focus, the CDC's March 2021 recommendations identified the shingles vaccine as a necessary preventive care tool even during the epidemic. Together with new product approvals such as SK Bioscience's SKYZoster in Malaysia, these governmental decisions are increasing vaccine availability and driving shingles vaccine market growth.

Restrain

-

Lack of Awareness and Vaccine Hesitancy Affect Shingles Vaccine Uptake in Several Regions

Many countries' shingles vaccination market is still limited by a continuous ignorance of shingles and the advantages of immunization, combined with vaccine reluctance. Though organizations such as the CDC and WHO have strong recommendations, vaccination rates in many nations remain below ideal; the UK boasts only a 31.2% coverage rate for those aged 70 in 2021–2022. Even if health officials advise vaccinations, low rates of acceptance are caused in part by misinformation, worries about possible adverse effects, and cultural views regarding adult vaccination.

Furthermore, complicating efforts to boost coverage, especially in low-and middle-income nations, are logistical issues including limited vaccination availability and distribution restrictions in rural areas. The CDC's continuous public health campaigns and the classification of shingles immunization as a necessary preventive care service are steps toward addressing these barriers, but significant gaps remain. These elements will keep reducing the effect of shingles vaccination campaigns and hamper the general growth of the worldwide shingles vaccination industry without focused educational initiatives and better outreach.

Segmentation Analysis

By Product

With 92% of the shingles vaccine market share, Shingrix led the market and accounted for its great efficiency, safety profile, and general approval by health authorities helps to explain this supremacy. Approved for adults 50 and over as well as for immunocompromised adults aged 18 and over, Shingrix is a recombinant adjuvanted vaccination. Strong recommendations from the CDC and EMA result from its great efficacy of over 90% in preventing shingles as well as post-herpetic neuralgia. Among U.S. adults 60+ in 2023, the CDC found a 34.5% shingles vaccination coverage.

In the U.S., its inclusion in the adult immunization schedule and strong CDC support have driven widespread adoption.

For instance, aiming to streamline administration and boost accessibility, GSK's new prefilled syringe presentation of Shingrix was approved for assessment by the U.S. FDA in January 2025. This will simplify the distribution of vaccines for medical practitioners, so perhaps increase immunization rates.

The SKYZoster category is expected to grow at the fastest CAGR of 14.44%, particularly in the Asia Pacific. Included in South Korea's national immunization program, the reasonably priced live attenuated vaccination SKYZoster provides a substitute for others. Following its second worldwide certification and therefore helping its growth in developing nations, SKYZoster got regulatory clearance in Malaysia in January 2023. Government support and continuous clinical research are likely to propel SKYZoster's expansion, especially in areas with limited resources.

By Vaccine Type

With 94% of the shingles vaccine market in 2024 occupied by the segment of recombinant vaccines, for older and immunocompromised persons, especially, recombinant vaccines such as Shingrix are recommended because of their great efficacy and safety. The CDC and EMA recommend recombinant vaccines as the first-line option for shingles prevention. With a large share going towards recombinant technology, the U.S. government spent approximately USD 9 billion on vaccine R&D in 2023. This has led to high adoption rates and robust shingles vaccine market growth.

Rising concerns about infectious illnesses and increased adoption of vaccination programs, especially in developing nations are likely to drive a consistent growth in the sector of live attenuated vaccines. As vaccine coverage grows, their long-lasting immunity makes them indispensable for work on world health.

Regional Analysis

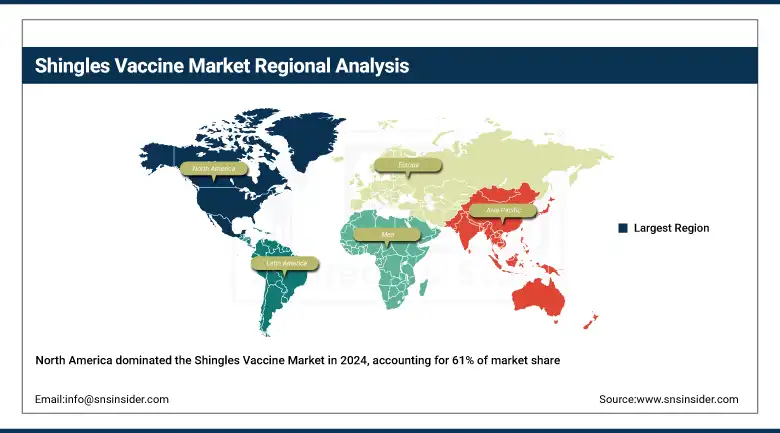

North America continues to dominate the global shingles vaccination market share of about 61% in 2024. Strong government support of preventative healthcare, excellent healthcare infrastructure, and a high frequency of shingles help to explain this dominance. The United States, in particular, leads the region, holding an 83% share of the North American shingles vaccine market share in 2024. Together with favourable payment regulations and extensive awareness campaigns, the U.S. government's inclusion of shingles vaccinations in the National Immunization Program has resulted in significant vaccination uptake. With headquarters in the area, major industry companies like GSK and Merck help to better position North America using ongoing product innovation and wide-ranging distribution networks. The high vaccination recommendation for the area, particularly among the elderly, and the quick acceptance of recombinant vaccines such as Shingrix have helped to accelerate market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is a lucrative region in the shingles vaccine market analysis. The area gains from better public knowledge of the need for immunization, more accessible vaccines, and good government policies. Higher coverage rates have come from nations such as Germany, the United Kingdom, and France, including shingles vaccinations in their national immunization campaigns. Particularly, Germany stands out because of its established healthcare system and large elderly population, which raises shingles risk and hence the need for vaccines. Government-sponsored campaigns combined with the broad availability of recombinant vaccines like Shingrix have driven market growth throughout Europe. With a trade value of about USD 29.2 billion in 2023, the European Union is a top exporter of vaccines for human medicine, therefore highlighting the strong vaccination manufacturing and distribution capacity of the area.

With a projected CAGR of 13.33% from 2025 to 2032, Asia Pacific is expected to have the fastest expansion in the shingles vaccine market. A big and expanding older population, increasing disposable incomes, and major changes in healthcare regulations and infrastructure drive this fast expansion. Lower- and middle-income nations in the area, such as China and India, show significant unmet medical needs that drive market expansion even more. Adoption rates of recombinant vaccines such as Shingrix throughout different Asian countries have been sped by continuous endorsement and approval. Particularly, Japan has shown an amazing increase since its fast-aging population is more likely to have shingles. Public awareness campaigns combined with government projects to incorporate shingles vaccinations in national immunization campaigns are helping to increase vaccination rates throughout the area. The Asia Pacific market is thus evolving from a nascent stage to a major force in the global landscape, with both multinational and local companies expanding their presence.

The LAMEA region-which includes Latin America, the Middle East, and Africa-remains a smaller but steadily growing segment of the global shingles vaccine market. Rising government attention on preventative healthcare, more knowledge of shingles and its consequences, and initiatives to enhance vaccine availability help this area to grow. Still, constraints on market growth include lower disposable incomes, inadequate healthcare facilities, and different degrees of public awareness.

Key Players

The key Shingles Vaccine Companies are GlaxoSmithKline (GSK), Vaccitech, Jiangsu Recbio Technology Co., Ltd., Merck & Co., Inc., GeneOne Life Science, Pfizer Inc., SK bioscience, BioNTech SE, Changchun BCHT Biotechnology Co., Curevo Inc., and others.

Recent Developments

-

GSK said in April 2024 that its ZOSTER-049 study demonstrated Shingrix offers adults 50 years of age and above over 10 years of protection against shingles.

-

Dynavax began dosing volunteers in a Phase 1/2 trial for their novel vaccine under development in June 2024.

-

Starting a Phase 1/2 study to evaluate the safety and immunological response of their mRNA-based shingles vaccine candidates in February 2023, Pfizer and BioNTech.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.86 Billion |

| Market Size by 2032 | USD 12.31 Billion |

| CAGR | CAGR of 12.35% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Shingrix, SKYZoster, and Zostavax) • By Vaccine Type (Live Attenuated Vaccine, and Recombinant Vaccine) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | GlaxoSmithKline (GSK), Vaccitech, Jiangsu Recbio Technology Co., Ltd., Merck & Co., Inc., GeneOne Life Science, Pfizer Inc., SK bioscience, BioNTech SE, Changchun BCHT Biotechnology Co., Curevo Inc., and others. |

Frequently Asked Questions

The Shingrix segment dominated the Shingles Vaccine Market.

Government initiatives and national immunization campaigns are extending the availability of shingles vaccination.

The CAGR of the Shingles Vaccine Market is 12.35% during the forecast period of 2025-2032.

The North American region dominated the Shingles Vaccine Market in 2023.

The projected market size for the Shingles Vaccine Market is USD 12.31 billion by 2032.

Get in Touch