STD Self-Testing Market Report Scope & Overview:

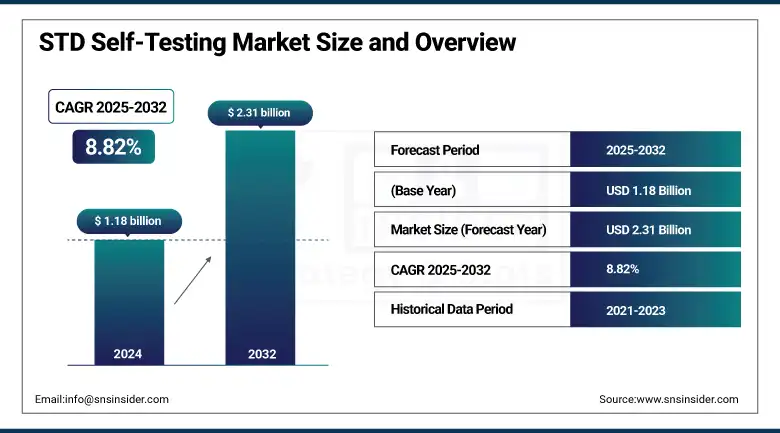

The STD self-testing market size was valued at USD 1.18 billion in 2024 and is expected to reach USD 2.31 billion by 2032, growing at a CAGR of 8.82% over the forecast period of 2025-2032.

The global STI self-testing market is growing with the prevalence of STIs, increasing awareness related to sexual health, and the growing preference of consumers for at-home diagnostic solutions. Advances in rapid molecular testing and rising approvals, including FDA clearance, are driving adoption. Digital health platforms that make the test as simple as delivery and tracking results also help build the market. Rising prevalence due to public health campaigns for early detection is anticipated to propel market growth significantly throughout the forecast period.

To Get more information On STD Self-Testing Market - Request Free Sample Report

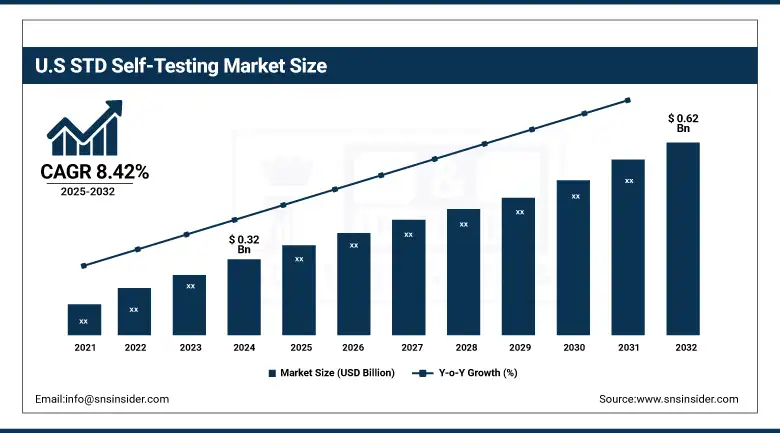

The U.S. STD self-testing market size was valued at USD 0.32 billion in 2024 and is expected to reach USD 0.62 billion by 2032, growing at a CAGR of 8.42% over the forecast period of 2025-2032.

The U.S. is dominating the North America STD self-testing market trend on account of robust FDA-cleared product approvals, high penetration of telehealth access, and public health programs, such as the CDC’s TakeMeHome HIV self-test distribution program. These market dynamics have resulted in higher uptake and consumer confidence in home testing options.

In February 2025, Abbott reported that it had obtained 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its self-collected molecular test for sexually transmitted diseases (STIs). This regulatory achievement is a major step forward in allowing users to test for STIs at home using Abbott's molecular diagnostics platform.

Market Dynamics:

Drivers:

-

Increase in STDS On a Global Basis is Creating a Conducive Market Environment

The growing global load of sexually transmitted diseases (STDs) is one of the major factors accelerating the need for self-testing solutions. Sexually transmitted infections, CT and NG in particular, are highly prevalent among AYAS and frequently asymptomatic or diagnosed late when AYAS have already experienced multiple visits to the clinic. Moreover, high prevalence of HIV, syphilis, and trichomoniasis in different areas further underscores the pressing requirement for developed, scalable, and accessible diagnostic methods. This growing prevalence is encouraging governments, healthcare organizations, and diagnostics companies to increase investments in the development and distribution of self-testing solutions to limit the spread of diseases and to ensure early treatment.

The WHO reports that over 1 million STIs that can be cured (chlamydia, gonorrhea, syphilis, and trichomoniasis) are acquired every day around the world, with 374 million new infections in 2020 alone.

The CDC has recently published over 2.4 million cases of chlamydia, gonorrhea, and syphilis in the year 2023, and with nearly 48% of those infections being among those between the ages of 15 to 24.

-

Government and NGO Initiatives for STD Screening are also Contributing Towards the Market Growth

Global efforts by governments and NGOs to prevent the spread of STDs with awareness campaigns, free screenings, and public health programs are on the rise. For example, self-testing kits are frequently distributed by community-based organizations in high-risk populations (sexually active youth, key populations including the lesbian, gay bisexual, transgender, and intersex, and men who have sex with men (MSM)). Another strategy to make routine screening more accessible and to increase participation is for companies and public health departments to collaborate to send at-home testing kits through the mail or to community centers. This, in turn, is eliminating the stigma around STDs and the need to test often, which is, in turn, directly driving the market for STD self-testing kits.

The first-ever over-the-counter (OTC) home test for chlamydia, gonorrhea, and trichomoniasis. The test (March 2025) received Food and Drug Administration (FDA) marketing authorization, with new regulations guiding access.

In July 2025, India’s ICMR announced rapid diagnostic tests, and among them the test for syphilis, would be rolled out in rural health centers and sub-centers, enabling greater and earlier detection in remote communities.

Australia’s TGA gave the green light for its first at-home chlamydia and gonorrhea self-test for women (Nov 2024), as STIs rise and stigma toward testing needs to disappear.

Restraints:

-

Unawareness and Health Illiteracy are Hindering the Market Growth

A significant hurdle in the STD self-testing market growth is the low level of knowledge and comprehension among people (especially in emerging countries) related to STDs and the need to test for these promptly. People are unaware that these kits are available, or they don’t know how to use them, or when to use them. This low health literacy promotes underdiagnosis and ongoing transmission of STIs. Moreover, misconceptions about STDs and STD testing, typically perpetuated by a lack of formal sex education, deter people from getting tested proactively, even in the presence of test kits. Notwithstanding advertising or educational efforts, self-testing solutions have little dissemination or effect.

Segmentation Analysis:

By Type of Infection/Disease Tested

The CT/NG testing segment held a dominant STD self-testing market share of 28.2% in 2024, on account of the high prevalence and burden of these two infections, especially among sexually active individuals below the age of 30 years. Such infections are frequently asymptomatic, and their underdiagnosis can result in untreated transmission to the partners if not screened regularly. The need for consumer-convenient, private, and rapid testing has compelled consumers to use self-testing CT/NG kits, largely due to public health endorsement in this direction and easy access to FDA-/CE- CE-CE-approved home collection and testing kits for these infections.

The HIV testing segment is expected to register the fastest CAGR during the forecast period due to an increase in global efforts for early diagnosis, a surge in the acceptance of antiretroviral treatment (ART), and the decrease in stigma associated with HIV testing. Rapid oral swab and blood-based test kits for HIV have advanced through new technology, are accessible to consumers from online retailers and pharmacies, and have the potential to increase self-testing. Furthermore, regulatory approvals and recommendations by international health authorities have helped bolster the public's confidence in using HIV self-tests as an initial instrument for detecting the virus.

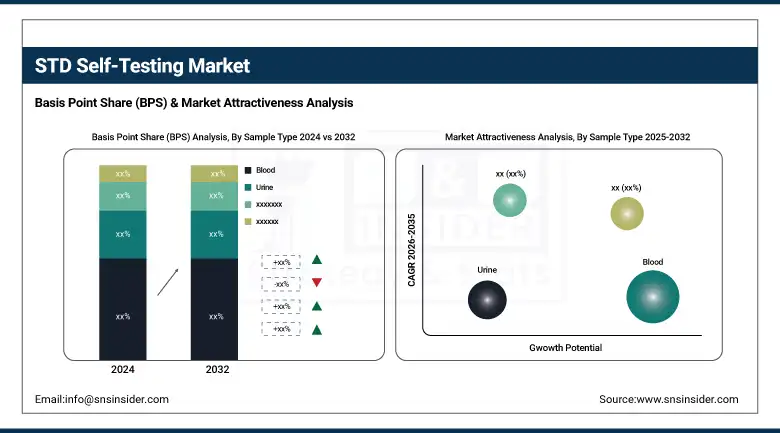

By Sample Type

The blood segment dominated the STD self-testing market with 39.24% market share in 2024, as it is largely utilized for identifying diseases, such as HIV and syphilis, where serological analysis is crucial for accurate diagnosis. For some diseases, blood-based self-tests have proven to be both more accurate and sensitive than their urine-based equivalents, and with consumer confidence increased by regulatory approvals for such kits. Furthermore, the high performance of blood-based testing to identify infections during the window period has established blood testing as a preferred option by healthcare workers and end-users.

The swab type (vaginal, rectal, oral, and urethral) is expected to be the fastest-growing segment during the forecast period owing to the increasing need for spontaneously non-invasive user user-friendly sample collection strategies and the expanding market of at-home kits in CT/NG and other genital tract infections. Swab-based testing is specifically popular among the younger demographic and those who value privacy, comfort, and convenience. In addition, the technological developments in sample collection devices and the regulatory premise for swab-based self-testing kits are driving the penetration in both developed and developing markets.

By Technology

In 2024, the lateral flow assays (LFA)/rapid diagnostic tests segment led the STD self-testing market with a 29% market share owing to its cost-effective nature, ease of use, and rapid results. These tests are easy to use, which are perfect for at-home testing or personal professional testing without the use of any special equipment or having a professional for assistance. Their low sample replacement and portability make them widely used among individuals, otherwise wary of privacy and convenience. Being able to produce results in minutes has made LFA-based kits the most popular choice for screening some of the most prevalent STDs, including chlamydia, gonorrhoea, and HIV.

The molecular diagnostics segment is expected to be the fastest-growing segment during the forecast period, supported by the growing need for more accurate and sensitive testing methodologies. Molecular diagnostics, also known as nucleic acid amplification tests (NAATs), provide a high level of sensitivity for the detection of infection, even in the nascent phase. The more reliable solutions are now gaining popularity as consumer and healthcare provider awareness about false negatives and shortcomings of rapid tests increases.

By End-User

The home users (direct-to-consumer) segment held the largest share in the STD self-test market in 2024 with a 42.25% market share, as consumers were looking for more privacy, ease, and discreet ways of testing themselves. The increasing awareness about sexual health and the shame that comes with going to clinics back and forth to get tested for STDs has further encouraged consumers to choose at-home self-testing kits. This trend has been exacerbated by the rise of e-commerce platforms and telehealth services, allowing consumers to easily purchase FDA- and CE-approved self-testing kits.

The clinics/community health centers segment is anticipated to witness the fastest growth during the forecast period due to public health initiatives and outreach among marginalised and high-risk populations. Based on limited available data and self-testing kits are becoming more widely used by these health care centers, in part to broaden access and alleviate the demand on conventional diagnostic systems. Community-based distribution and promotional campaigns are also promoting self-testing in semi-clinical care settings where provider assistance remains available. This hybrid model is an intermediary between user-led autonomy and clinical assistance, to support and facilitate higher uptake of self-testing of STIs in wider population groups.

By Distribution Channel

The retail pharmacies segment dominated the STD self-testing market in 2024, due to on-site testing knowledge, trust from consumers, and off-the-shelf availability. Many consumers also buy a self-testing kit from the local pharmacy as they can have it immediately, and the pharmacist can offer a small amount of advice on how it works. Since collaborations between diagnostic companies and large pharmacy chains have guaranteed a steady supply of approved test kits on store shelves. Retail pharmacies also rely on walk-in foot traffic and impulse purchases, especially in urban and suburban areas where sexual health is more widely understood.

The online pharmacies/e-commerce platforms segment is expected to grow with the highest CAGR during the forecast period due to rising digitalization in healthcare, coupled with rising consumer inclination for concealed and private purchasing, which has resulted in higher demand for online shopping. These are channels that let people now compare two, even three different testing kits at once, read up on user reviews, and get a product delivered right to the door, frequently with the option of a wrapped-up telehealth consultation. The online distribution segment in the STD self-testing market has been expanding due to internet facilities, convenience, privacy, and the increasing number of internet users in developed and developing regions.

Regional Analysis:

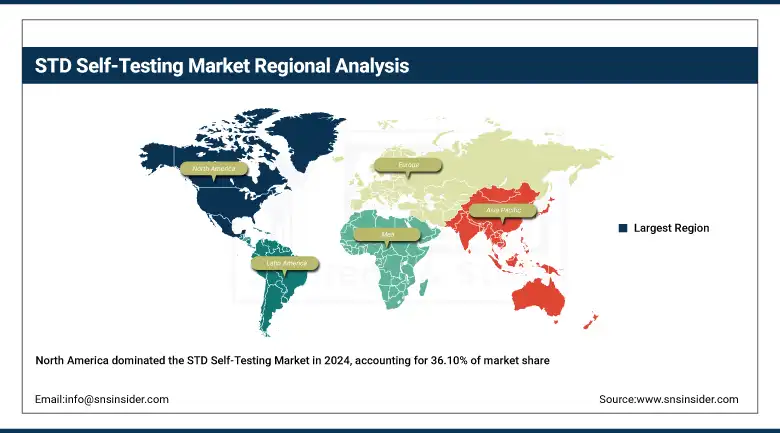

North America dominated the STD self-testing market in 2024 with a 36.10% share due to a significant amount of funding from key players with strong regulation, extensive awareness, networking, and a nuanced push of digital health. The market in the region is driven by the well-established healthcare sector, government-impelled programs to encourage sexual health, and a commanding market position of key market players, including Abbott, Quest Diagnostics, and Everlywell. The 510(k) and De Novo clearances at the FDA for at-home STI tests have driven consumer confidence and opened the floodgates for viable test-yourself options.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific to grow fastest in global STD self-testing market with a 9.36% CAGR over the forecast period, owing to escalating awareness about sexual wellness, increased penetration of Internet and smartphones, and a greater range of affordable and easy-to-use test kits. Countries, such as China, India, and Southeast Asian countries are seeing STD infection rates rise, and social stigma that deters people from going to clinics, encouraging demand for private and home-based testing. Government schemes, foreign assistance, and public health infrastructure are also spurring rapid growth in the market in the region.

In Europe, the STD self-testing market is growing at a significant rate, due to growing awareness and increasing incidence of STDs and the emergence of private, convenient, and confidential testing. Governments and health organizations throughout the region are pushing the importance of early detection through public health campaigns and the common availability of self-test kits. Also, regulatory pushes, such as IVDR being implemented open doors for certified self-tests, adding trust and usage. Those with strong healthcare infrastructure, such as Germany and the U.K., are leading the way, with increasingly popular digital health platforms offering online access to self-testing.

The STD self-testing market analysis is also growing at a moderate rate in Latin America, with the rise in awareness regarding sexual health, support from non-governmental organizations (NGOs), and better healthcare availability in urban areas. Social stigma and access are still barriers, particularly in rural areas, but increasing interest in discreet and easy testing is driving adoption.

The Middle East & Africa (MEA) has also been observing a proliferation in the use of STD self-testing kits due to that the growth is moderate in the region. The rising number of urban population is becoming more concerned about health, and they are ready to take preventive measures for sexual health, even in the younger generation. As governmental CHCs and foreign funding initiatives to promote sexual health awareness continue to reshape the landscape, the environment for self-testing solutions is in the process of being gradually transformed.

Key Players:

The std self-testing market companies are OraSure Technologies, bioLytical Laboratories, Mylan, bioMérieux, Chembio Diagnostics, Abbott Laboratories, Everlywell, LetsGetChecked, MyLab Box, Nurx, Thorne HealthTech, TestCard, Fastep (Assure Tech), Atomo Diagnostics, iCare Diagnostics, Health Testing Centers, Labcorp, Quest Diagnostics, EverlyDx, Premier Biotech, and other players.

Recent Developments:

-

November 2023, LetsGetChecked, a healthcare solutions company with a global presence, reported that the U.S. FDA has awarded De Novo classification to its Simple 2 home collection system. This clearance makes LetsGetChecked's test the first FDA-approved home sample collection system for chlamydia and gonorrhea available both online and in retail outlets throughout the U.S.

-

October 2024, Atomo Diagnostics, a medical device technology company headquartered in Australia, has received a USD 2.44 million grant from the Australian Government under the CRC-P Industry Program administered by the Department of Industry, Science and Resources (DISR). The funding is to develop a new rapid syphilis test intended for professional point-of-care and at-home self-testing use.

-

October 2024 Quest Diagnostics unveiled a new diagnostic service designed to improve access and efficiency in testing and treating many prevalent genital tract infections (GTIs). The new solution is one aspect of Quest's overall plan to grow personalized and convenient test solutions.

STD Self-Testing Market Report Scope:

Report Attributes Details Market Size in 2024 USD 1.18 Billion Market Size by 2032 USD 2.31 Billion CAGR CAGR of 8.82% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Type of Infection/Disease Tested (HIV, CT/NG Testing, Chlamydia, Gonorrhea, Syphilis, Herpes Simplex Virus (HSV), Trichomoniasis, Human Papillomavirus (HPV), Hepatitis B & C, Others (e.g., Mycoplasma genitalium))

• By Sample Type (Blood, Urine, Saliva, Swab (vaginal, rectal, oral, urethral))

• By Technology (Lateral Flow Assays (LFA) / Rapid Diagnostic Tests, Molecular Diagnostics (e.g., PCR-based), Immunoassays (ELISA, etc.), Other Advanced Testing Technologies)

• By End User (Home Users (Direct-to-Consumer), Clinics / Community Health Centers, Hospitals / Healthcare Facilities, Diagnostic Laboratories)

• By Distribution Channel (Online Pharmacies / E-commerce Platforms, Retail Pharmacies, Supermarkets / Hypermarkets, Others (e.g., NGOs, public health programs))Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles OraSure Technologies, bioLytical Laboratories, Mylan, bioMérieux, Chembio Diagnostics, Abbott Laboratories, Everlywell, LetsGetChecked, MyLab Box, Nurx, Thorne HealthTech, TestCard, Fastep (Assure Tech), Atomo Diagnostics, iCare Diagnostics, Health Testing Centers, Labcorp, Quest Diagnostics, EverlyDx, Premier Biotech,

Frequently Asked Questions

North America dominated the STD Self-Testing Market in 2024.

The “Blood” segment dominated the STD Self-Testing Market.

Government and NGO Initiatives for STD Screening are also Contributing Towards the Market Growth.

The STD Self-Testing Market was USD 1.18 billion in 2024 and is expected to reach USD 2.31 billion by 2032.

The STD Self-Testing Market is expected to grow at a CAGR of 8.82% from 2025 to 2032.

Get in Touch