Shipping Software Market Report Scope & Overview:

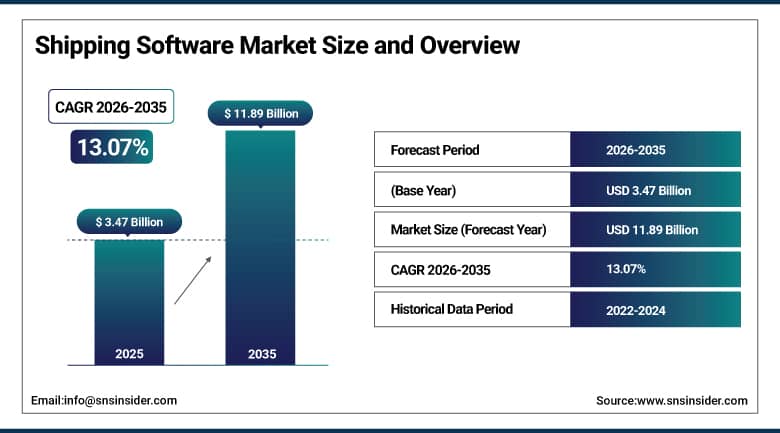

The Shipping Software Market was valued at USD 3.47 Billion in 2025 and is expected to reach USD 11.89 Billion by 2035, growing at a CAGR of 13.07% from 2026–2035.

The global market for shipping software is growing at a fast pace due to the rapid rise of e-commerce, globalization of the supply chain, and digitalization of logistics processes. Shipping software allows for automating such activities as rate shopping, carrier selection, shipment tracking, customs clearance, and last mile management for shippers, freight forwarders, third party logistics service providers, and retailers. The development of the shipping software market is largely determined by such factors as the explosive growth of cross-border e-commerce, increasing carrier capacity competition, environmental regulations demanding the calculation of the carbon footprint, and utilization of artificial intelligence for optimal routing and rate negotiations.

In 2024, Shippo announced the launch of its AI-powered rate intelligence engine that analyses historical shipment data, carrier performance metrics, and real-time capacity signals to automatically select the optimal carrier and service level for each shipment based on the shipper's configurable cost-speed-reliability preference weighting.

Market Size and Forecast:

-

Market Size in 2026E: USD 3.92 Billion

-

Market Size by 2035: USD 11.89 Billion

-

CAGR: 13.07% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Shipping Software Market - Request Free Sample Report

Shipping Software Market Trends:

-

AI-powered rate optimization is improving carrier selection and reducing shipping costs.

-

Cloud-based shipping platforms are gaining adoption due to scalability and lower upfront costs.

-

Cross-border shipping solutions are expanding to support customs compliance and international trade.

-

Integration of last-mile delivery management is enhancing shipment visibility and customer experience.

-

Sustainability tracking features are being adopted to monitor emissions and support ESG goals.

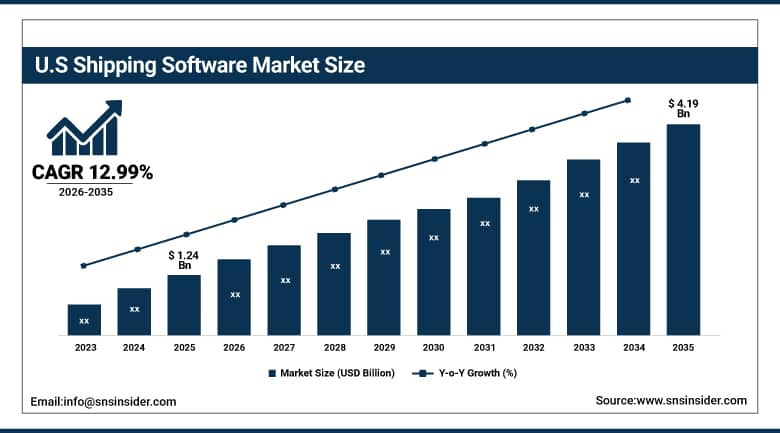

U.S. Shipping Software Market Outlook:

The U.S. Shipping Software Market was valued at approximately USD 1.24 Billion in 2025 and is expected to reach approximately USD 4.19 Billion by 2035, growing at a CAGR of approximately 12.99%.

The United States is the world's most commercially developed shipping software market, reflecting the country's mature e-commerce ecosystem, high parcel volume per capita, competitive multi-carrier landscape, and technology-forward logistics industry. The U.S. market is characterized by high adoption of cloud-based multi-carrier shipping platforms among both SME retailers and enterprise shippers, intense competition between platform providers including Shippo, EasyPost, ShipStation, Stamps.com, Pitneyship, and enterprise TMS vendors including Oracle, SAP, and MercuryGate. The IRS-recognized deductibility of shipping software subscription costs, the complexity of domestic zone-based carrier pricing, and the UPS-FedEx-USPS-regional carrier competitive landscape that creates rate optimization opportunity collectively sustain the U.S. market's structural demand for software-based shipping management.

EasyPost expanded its U.S. shipping API platform in 2024 with the launch of its Carrier Accounts Marketplace, enabling enterprise e-commerce platforms and fulfilment software vendors to offer their merchant customers negotiated carrier rates from a pre-contracted carrier portfolio without requiring individual merchant-carrier volume commitments.

Shipping Software Market Segment Analysis:

-

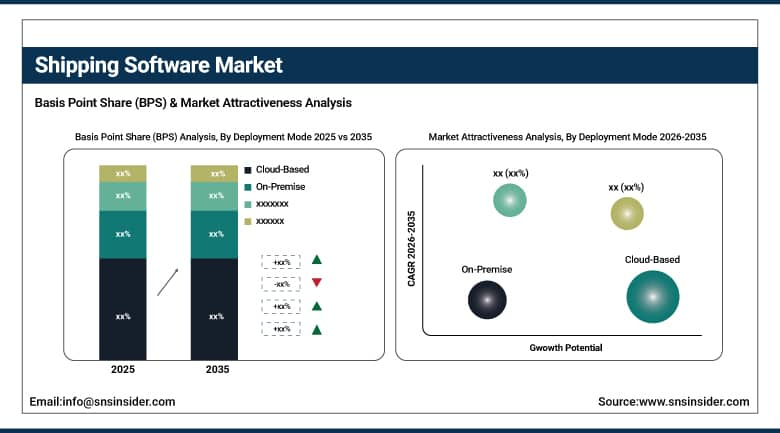

By Deployment Mode, the Cloud-Based segment dominated the shipping software market with 71.6% share in 2025, driven by the subscription model's lower total cost of ownership, faster deployment timelines, automatic feature updates, and carrier connectivity maintenance that eliminates the infrastructure burden of on-premise installations whose API maintenance requirements create ongoing IT resource consumption.

-

By Software Type, the Transportation Management System segment dominated the shipping software market with 34.2% share in 2025, while the Freight Management Software segment is the fastest growing as cross-border trade volume expansion and freight rate volatility.

-

By Enterprise Size, the Large Enterprises segment dominated the shipping software market with 58.3% share in 2025, while the Small & Medium Enterprises segment is the fastest growing as cloud-based multi-carrier shipping platforms lower the technology adoption barrier through subscription pricing.

-

By End-Use Industry, the Retail & E-Commerce segment dominated the shipping software market with 41.7% share in 2025, driven by e-commerce merchants' multi-carrier rate shopping requirement, consumer expectation for real-time tracking.

By Deployment Mode, cloud-based dominates, on-premise serves regulated enterprise

The use of cloud-based shipping software maintained the position of the preferred shipping software deployment model with an adoption rate of 71.6%. This was because cloud-based software was favored due to its ability to conform to the principles of the subscription economy where operating expenses were more preferable than capital expenses in IT investments, carrier API connectivity challenges managed by the cloud provider for all the customers and not individually by the customer, and a continuous release strategy that guarantees that cloud-based customers have access to the latest features.

On-premise shipping software retains a commercially significant position in highly regulated industries including pharmaceuticals, aerospace, and defense whose data sovereignty requirements, ERP integration architecture, and export control compliance mandate internal system deployment. Each on-premise installation's higher implementation cost and longer deployment timeline is offset by the greater control over data residency, customization depth, and integration architecture that regulated enterprise customers require for compliance with FDA, ITAR, and export administration regulation requirements.

By Software Type, transportation management systems dominate, freight management grows fastest

In 2025, Transportation Management Systems were still the leading form of software used in the shipping software market, commanding 34.2% market share. The business success of TMS systems is based on the comprehensive nature of its coverage, from carrier management to shipment tracking and performance analytics, which makes it the system of record for enterprise shippers with complex multi-modal freight operations. As all Fortune 500 companies adopt these TMS systems for their businesses in manufacturing, retail, and distribution, the platform gains an already established client base in terms of which more business revenue can be consistently generated.

Freight Management Software is the fastest growing software type because cross-border trade volume expansion, freight rate volatility, and carrier capacity unpredictability create demand for platforms that optimize mode selection and carrier tendering across air, ocean, rail, and truck simultaneously. Each freight rate spike episode that exposes the cost of manual carrier tendering and mode selection motivates investment in software platforms whose optimization algorithms create consistent freight cost reduction even in volatile market conditions.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.3% |

|

Europe |

Germany |

22.1% |

|

Asia Pacific |

China |

38.7% |

|

Middle East & Africa |

UAE |

31.4% |

|

Latin America |

Brazil |

43.8% |

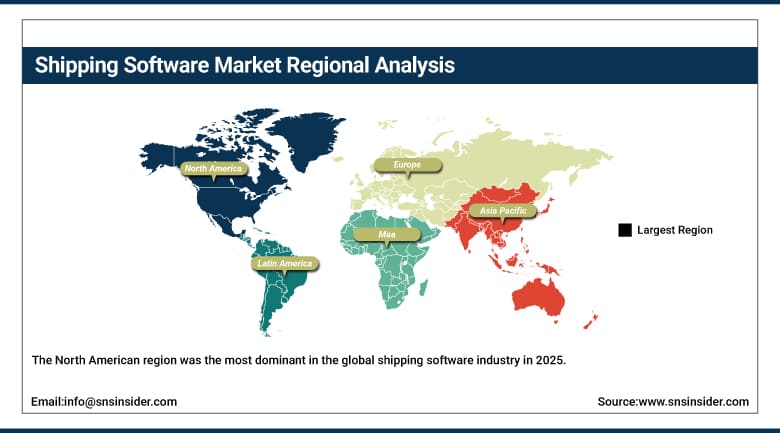

North America Shipping Software Market Insights

The North American region was the most dominant in the global shipping software industry in 2025, with the United States contributing about 82.3% of the revenue generated in the region. Commercial dominance of the US market is characterized by its advanced e-commerce environment leading to creation of the second-highest number of parcels in the world, the competitive multicompany market making rate optimization possible, and advanced technological inclination of logistics companies in the US, who invest in digital technologies, leading to high software penetration levels.

Canada makes up the remaining 17.7% of the regional revenue, thanks to its developing e-commerce market, complicated shipping process into the US, which calls for software that can handle shipping across the two countries, and rising competition between Canada Post, Purolator, and other domestic carriers.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Shipping Software Market Insights

This market represents strategic value for shipping software sales because the EU's unified market necessitates cross-border intra-European shipments, GDPR imposes data protection restrictions on vendors, and Europe's fragmented national postal service systems and parcel carriers present an opportunity for multi-carrier management solutions in 27 member states of the EU and the UK after Brexit. Germany constitutes approximately 22.1% of European revenues due to its status as the EU's largest e-commerce market, its role as a home to manufacturing and industrial shippers that face freight management complexities, and Deutsche Post DHL Group's international logistics network of which the associated software investments have resulted in above average market development.

Secondary markets like the UK, France, Netherlands, and Benelux represent strong secondary markets as e-commerce prevalence, international shipment complexity, and logistics hub location provide consistent demand for shipping software and motivates higher platform adoption than the market's size.

Asia Pacific Shipping Software Market Insights

Asia Pacific is home to the world’s fastest growing regional shipping software market, due to China’s extensive e-commerce system, the rapid growth of cross-border e-commerce in Southeast Asia, and the rapid growth of India’s domestic e-commerce industry, leading to logistic challenges, which drive the adoption of shipping software. China makes up 38.7% of the revenue share in Asia Pacific with Alibaba's Cainiao logistics network, the JD Logistics' technology platform, as well as the massive volume of domestic parcels in the country, requiring complex management, thus generating demand for automation.

India, Japan, South Korea, and Southeast Asian countries such as Indonesia, Thailand, and Vietnam constitute secondary regions with above average growth rates for shipping software due to e-commerce growth, infrastructure development, and increased cross border transactions, thus sustaining Asia Pacific's position as the world's fastest growing region in terms of growth until 2035.

MEA & Latin America Shipping Software Market Insights

The UAE leads MEA revenues at approximately 31.4% through its position as the region's logistics hub, the Dubai International Airport and Jebel Ali Port's freight volume creating demand for freight management software, and the country's digital economy initiative driving e-commerce growth that creates last-mile delivery software adoption. Saudi Arabia's Vision 2030 logistics investment and South Africa's growing e-commerce market are significant secondary contributors to MEA shipping software market development.

Brazil leads Latin American revenues at approximately 43.8% through its dominant position as the region's largest e-commerce market, the complexity of Brazil's state-level tax system (ICMS) creating demand for software that manages fiscal document generation and compliance across 26 states, and the growing domestic parcel carrier competition creating multi-carrier rate optimization opportunity. Mexico and Colombia are significant secondary markets whose cross-border US trade and growing domestic e-commerce create consistent shipping software demand.

Market Dynamics:

Growth Drivers: E-commerce expansion driving multi-carrier shipping complexity and cloud platform adoption lowering SME adoption barriers

E-commerce expansion is the main commercially significant driver in the shipping software space, as any additional percentage points of the move of retail trade onto online channels will create similar percentage growth in parcel volumes, which adds complexity in handling multiple carriers, thus spurring investment in shipping software. The anticipated growth of the global e-commerce market, rising from approximately $6 trillion in 2024 to $12 trillion by 2030, will provide a growing business case whose shipping requirements grow in parallel, fueling the above-average shipment software market growth irrespective of adoption rate improvement.

The uptake of cloud-based platforms is lowering the SME barrier to entry for shipping software by avoiding up-front investments in infrastructure, allowing subscription-based pricing based on shipment volume, and coming with pre-integrated carrier connections, which eliminates the necessity of API integrations for individual businesses. With each SME merchant that switches to a cloud-based shipment software, recurring revenue is generated in line with their shipment volume, with the net retention rate reflecting how deeply the software has been integrated into their operations.

Restraints: Carrier API fragmentation creating integration complexity and data security concerns in cloud-based shipping platforms

The fragmentation of carrier APIs in integration complexity means that each carrier's API, authentication process, rate structures, and service offerings will need to be integrated, adding up to an ongoing investment in maintaining those integrations. Every time a carrier API changes, there is potential risk of disrupting shippers' operations depending on rate shopping capabilities and label creation in real-time, which necessitates continued investments in platform reliability.

Cloud-based shipping platforms face issues with data security as shipments include personally identifiable information, trade secrets, or technical data controlled for export, which make shippers liable to GDPR, CCPA, ITAR, and other regulatory frameworks regarding data security. In the event of breaches occurring across logistics technology players, such data breaches set back confidence in the technology overall and favor on-premises installations for the most security-sensitive shippers.

Opportunities: AI-powered shipping optimization creating measurable ROI and cross-border e-commerce complexity driving international shipping software demand

AI-based shipping optimization constitutes the most promising commercial application on the horizon for shipping software providers, as predictive algorithms built off of carrier performance metrics, rates, and capacity lead to quantified savings on shipping costs that enable faster adoption of the solution based on its ROI. Each AI shipping optimization vendor showing an ability to reduce its customers' shipping expenses by 15-20 percent via predictive analysis gains an advantage over the competition in the form of increased revenue thanks to shorter sales cycles.

Cross-border e-commerce is a long-term growth opportunity that will generate demand for shipping software solutions capable of providing international shipments from beginning to end through their ability to facilitate customs declarations, duties and taxes calculations, sanctions checks, and currency conversion. New customs systems implemented in each nation bring about more integrations for e-commerce players to keep up with their operations growth without the need for more compliance personnel.

Recent Developments:

-

2024: Shippo launched its AI-powered rate intelligence engine that analyses historical shipment data and real-time carrier capacity signals to automatically select the optimal carrier for each shipment, achieving average shipping cost reductions of 12–18% for SME customers across its multi-carrier platform.

-

2024: EasyPost launched its Carrier Accounts Marketplace in the U.S., enabling enterprise e-commerce platforms to offer their merchant customers negotiated carrier rates from a pre-contracted carrier portfolio without requiring individual merchant volume commitments.

-

2024: Oracle Transportation Management released its AI-driven dynamic routing optimization module that integrates real-time traffic, weather, and carrier capacity data to optimize multi-stop route planning for last-mile delivery operations, reducing delivery cost per stop by up to 14% in enterprise pilot deployments.

-

2024: Flexport expanded its digital freight platform with AI-powered supply chain visibility tools providing real-time shipment status, predictive delay identification, and proactive exception management across ocean, air, and ground modes for enterprise logistics customers.

-

2023: SAP Transportation Management integrated carbon emissions tracking and Scope 3 reporting capabilities into its TMS platform, enabling enterprise shippers to measure carrier-level carbon intensity, model modal shift scenarios, and generate emissions reduction pathway reports aligned with SBTi disclosure requirements.

Shipping Software Market Key Players:

-

Oracle Corporation

-

SAP SE

-

Manhattan Associates, Inc.

-

Blue Yonder Group, Inc.

-

MercuryGate International, Inc.

-

Descartes Systems Group Inc.

-

Trimble Inc.

-

Alpega Group

-

3Gtms, Inc.

-

Shippo, Inc.

-

EasyPost, Inc.

-

ShipBob, Inc.

-

ShipStation (Auctane)

-

Stamps.com (Auctane)

-

Pitneyship (Pitney Bowes Inc.)

-

Flexport Inc.

-

project44, Inc.

-

FourKites, Inc.

-

Samsara Inc.

-

Netsol Technologies Inc.

Shipping Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.47 Billion |

| Market Size by 2035 | USD 11.89 Billion |

| CAGR | CAGR of 13.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment Mode (Cloud-Based, On-Premise) • By Software Type (Transportation Management System, Warehouse Management System, Order Management System, Fleet Management Software, Freight Management Software, Others) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By End-Use Industry (Retail & E-Commerce, Manufacturing, Healthcare & Pharmaceuticals, Food & Beverage, Automotive, Oil & Gas, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Oracle Corporation, SAP SE, Manhattan Associates, Inc., Blue Yonder Group, Inc., MercuryGate International, Inc., Descartes Systems Group Inc., Trimble Inc., Alpega Group, 3Gtms, Inc., Shippo, Inc., EasyPost, Inc., ShipBob, Inc., ShipStation (Auctane), Stamps.com (Auctane), PitneyShip (Pitney Bowes Inc.), Flexport Inc., project44, Inc., FourKites, Inc., Samsara Inc., Netsol Technologies Inc. |

Frequently Asked Questions

The Shipping Software Market is expected to grow at a CAGR of 13.07% from 2025 to 2035.

The Shipping Software Market was valued at USD 3.47 Billion in 2025.

Accelerating global e-commerce growth creating multi-carrier parcel and freight management complexity, and AI-powered shipping optimization platforms delivering measurable freight cost reduction that shortens enterprise adoption cycles.

Cloud-Based deployment dominated the Shipping Software Market with 71.6% share in 2025, driven by subscription pricing, carrier integration maintenance, and automatic feature deployment advantages over on-premise alternatives.

The Transportation Management System segment dominated the Shipping Software Market with 34.2% share in 2025, while Freight Management Software is the fastest growing segment driven by cross-border trade expansion and freight rate volatility.

Get in Touch