Silicon Tetrachloride Market Report Scope & Overview:

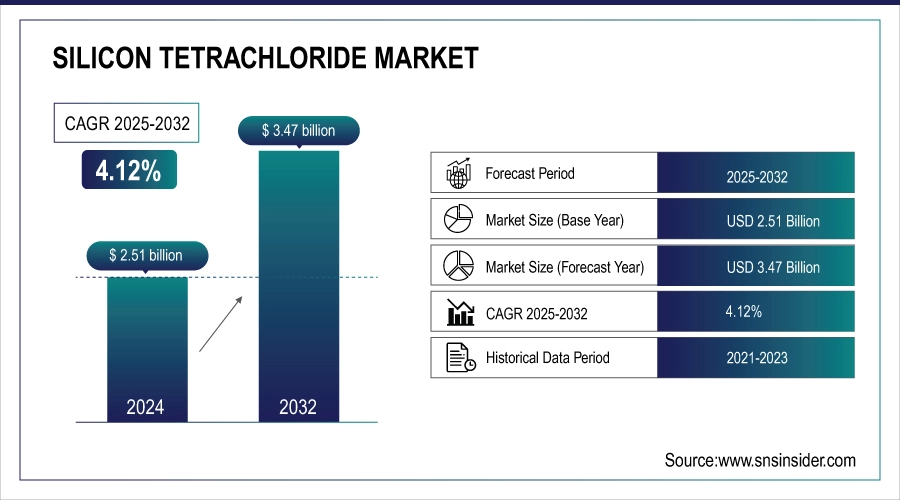

The Silicon Tetrachloride Market size was valued at USD 2.51 Billion in 2024 and is projected to reach USD 3.47 Billion by 2032, growing at a CAGR of 4.12% during 2025-2032.

The silicon tetrachloride market is experiencing notable growth driven by increasing demand in fiber optics, semiconductors, and solar photovoltaics, with expansion fueled by technological advancements in high-purity chemical manufacturing and rising renewable energy adoption. According to the U.S. Department of Energy, the U.S. installed 33 GW of solar capacity in 2023, significantly boosting silicon tetrachloride usage in polysilicon production. Furthermore, the International Energy Agency reported global solar PV additions of 510 GW in 2023, underscoring strong industrial uptake. Companies such as Wacker Chemie and OCI are scaling production capacities to strengthen their silicon tetrachloride market share, reflecting competitive industry dynamics. In terms of government-backed initiatives, China’s Ministry of Industry and Information Technology emphasized policies to enhance domestic polysilicon output, supporting market expansion. With growing focus on advanced material integration, the silicon tetrachloride market analysis indicates continued momentum, while innovation in fiber optics and electronics further adds to the silicon tetrachloride market size.

Silicon Tetrachloride Market Size and Forecast

-

Market Size in 2024: USD 2.51 Billion

-

Market Size by 2032: USD 3.47 Billion

-

CAGR: 4.12% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Silicon Tetrachloride Market - Request Free Sample Report

Key Silicon Tetrachloride Market Trends

-

Demand from solar PV industry rising as silicon tetrachloride becomes essential for photovoltaic material production.

-

Recycling and reuse of silicon tetrachloride by-products gaining momentum to reduce waste and environmental impact.

-

Chemical producers forming long-term collaborations with telecom companies for consistent optical fiber raw material supply.

-

Localized silicon tetrachloride manufacturing increasing to minimize reliance on Asian exports and strengthen supply chains.

-

Adoption of digital monitoring and automation technologies improving operational efficiency and safety in production plants.

-

Development of low-carbon and eco-friendly production technologies accelerating to meet global sustainability requirements.

-

Expansion of polysilicon manufacturing capacities in developing regions supporting rapid semiconductor industry growth.

-

Stringent regulations driving safer logistics, packaging, and storage practices for hazardous silicon tetrachloride handling.

Silicon Tetrachloride Market Growth Drivers:

-

Increasing Demand for Semiconductors and Electronics Accelerates Silicon Tetrachloride Market Growth

The surge in global demand for semiconductors, driven by advancements in consumer electronics, automotive technologies, and artificial intelligence, is significantly boosting the need for silicon tetrachloride. As a key precursor in the production of high-purity silicon wafers for microchips, the silicon tetrachloride market is poised for substantial growth. According to the Semiconductor Industry Association, federal investments of approximately $20 billion to $30 billion in semiconductor design and R&D through 2030 are expected to sustain the United States' leadership in chip design, further driving the demand for silicon tetrachloride.

For instance, in June 2023, Wacker Chemie AG expanded its semiconductor-grade polysilicon production in Germany, boosting the demand for silicon tetrachloride as a precursor for high-purity silicon used in microchips and other semiconductor applications.

U.S. Silicon Tetrachloride Market Insights

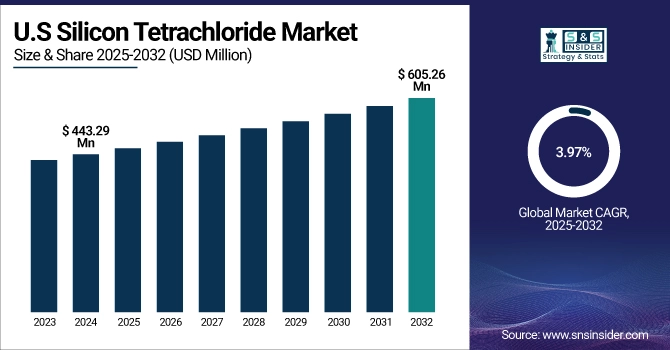

The U.S. Silicon Tetrachloride Market size was valued at USD 443.29 million in 2024 and is projected to reach USD 605.26 million by 2032, growing at a CAGR of 3.97% during 2025-2032.

In North America, the U.S. dominates the Silicon Tetrachloride Market due to its robust semiconductor and electronics manufacturing ecosystem. The country’s government has actively supported domestic semiconductor production through the CHIPS and Science Act, which allocates billions of dollars for research, development, and manufacturing incentives. Major Silicon Tetrachloride Companies in the U.S. are expanding production facilities to meet rising demand for high-purity silicon used in semiconductors, solar panels, and optical fibers. Canada, while growing rapidly in clean energy and advanced materials, still plays a secondary role compared to the U.S.

-

Expansion of Renewable Energy Initiatives Boosts Silicon Tetrachloride Market Demand

The global shift towards renewable energy sources, particularly solar power, is increasing the demand for silicon tetrachloride. Silicon tetrachloride is a crucial intermediate in the production of high-purity silicon used in photovoltaic cells. As countries invest in clean energy infrastructure, the need for efficient and cost-effective solar panels grows, thereby driving the silicon tetrachloride market. The International Energy Agency reports that solar energy capacity has been expanding rapidly, further emphasizing the importance of silicon tetrachloride in meeting renewable energy goals.

For instance, in 2023, the International Energy Agency reported that global renewable energy capacity grew by nearly 50%, increasing demand for photovoltaic cells and, consequently, silicon tetrachloride used in producing high-purity silicon for solar panels.

Silicon Tetrachloride Market Restraints:

-

Environmental Regulations Impact Silicon Tetrachloride Production Processes Restricts the Growth of the Silicon Tetrachloride Market

Stringent environmental regulations regarding the production and handling of hazardous chemicals, including silicon tetrachloride, pose challenges to market growth. The chemical industry faces increasing pressure to adopt sustainable practices and reduce emissions. Compliance with these regulations often requires significant investments in technology and infrastructure, potentially increasing production costs and affecting the profitability of silicon tetrachloride manufacturers. The European Chemicals Agency has outlined strict guidelines for the safe handling of silicon tetrachloride, necessitating adherence to ensure market access.

Silicon Tetrachloride Market Opportunities:

-

Government Incentives Support Growth in the Renewable Energy Sector, Creating Growth Opportunities in the Silicon Tetrachloride Market

Government policies and incentives aimed at promoting renewable energy sources present opportunities for the silicon tetrachloride market. Subsidies, tax credits, and grants for solar energy projects can stimulate demand for photovoltaic cells, thereby increasing the need for silicon tetrachloride in their production. The U.S. Department of Energy's Solar Energy Technologies Office has been instrumental in funding research and development initiatives that enhance the efficiency and affordability of solar technologies, indirectly boosting the silicon tetrachloride market.

For instance, in March 2024, the U.S. Department of Energy announced $30 million in funding for advanced solar technology research, enhancing photovoltaic efficiency and indirectly increasing the demand for silicon tetrachloride in high-purity silicon production.

Key Silicon Tetrachloride Market Segment Highlights

-

By Grade, Electronics Grade led with ~58% share in 2024; Technical Grade fastest growing (CAGR 4.18%).

-

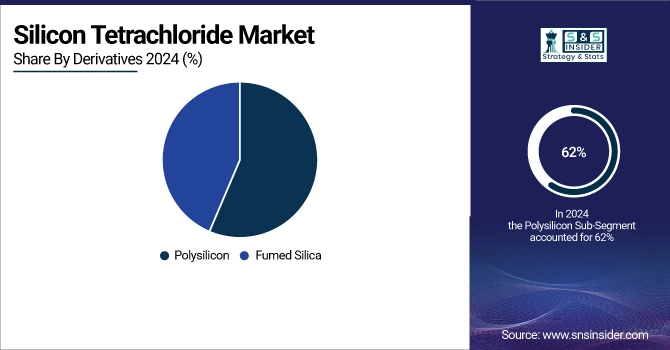

By Derivatives, Polysilicon dominated ~62% in 2024; Fumed Silica fastest growing (CAGR 4.22%).

-

By Application, Chemical Intermediate led ~43% in 2024; Optical Fiber Preform is the fastest growing (CAGR 4.30%).

-

By End-use Industry, Electronics held ~37% in 2024; Telecommunications is the fastest growing (CAGR 4.90%).

Key Silicon Tetrachloride Market Segment Analysis

-

By Type, Electronics Grade Leads Market While Technical Grade Registers Fastest Growth

In 2024, the Electronics Grade segment dominated the Silicon Tetrachloride market with a 58.20% share, driven by rising demand for high-purity silicon in semiconductor manufacturing, consumer electronics, and automotive technologies. U.S. Department of Energy investments in semiconductor R&D and expansions by major manufacturers have boosted electronics-grade consumption. Meanwhile, the Technical Grade segment is projected to be the fastest-growing from 2025 to 2032, with a CAGR of 4.18%, fueled by diverse applications in chemicals and materials, derivatives like fumed silica and polysilicon, and government initiatives promoting industrial growth and infrastructure development, further elevating Silicon Tetrachloride demand.

-

By Derivatives, Polysilicon Dominates While Fumed Silica Shows Rapid Growth

In 2024, the Polysilicon derivative segment dominated the Silicon Tetrachloride market with a 61.50% share, driven by strong demand for photovoltaic cells and semiconductors. The rapid expansion of global solar energy capacity, as reported by the International Energy Agency, has heightened the need for polysilicon, increasing silicon tetrachloride consumption. Meanwhile, the Fumed Silica derivative segment is projected to be the fastest-growing from 2025 to 2032, with a CAGR of 4.22%, fueled by its applications in silicones, adhesives, and coatings. Advancements in manufacturing and rising demand for high-performance materials in automotive, construction, and electronics sectors further boost fumed silica use.

-

By Application, Chemical Intermediate Leads While Optical Fiber Preform Shows the Fastest Growth

In 2024, the Chemical Intermediate application segment dominated the Silicon Tetrachloride market with a 42.70% share, driven by rising demand in chemicals, materials, and manufacturing industries. The steady growth of the U.S. chemical sector has further increased silicon tetrachloride consumption in chemical applications. Simultaneously, the Optical Fiber Preform segment is projected to be the fastest-growing from 2025 to 2032, with a CAGR of 4.30%, fueled by the expanding telecommunications sector and rising demand for high-speed internet. This growth underscores the increasing use of silicon tetrachloride in producing optical fibers for modern communication infrastructure.

-

By End-use Industry, Electronics Leads While Telecommunications Grow Fastest

In 2024, the Electronics end-use industry dominated the Silicon Tetrachloride market with a 36.90% share, driven by its critical role in semiconductor manufacturing for smartphones, laptops, and wearables. Major electronics companies expanding production capacities have further increased silicon tetrachloride consumption. Simultaneously, the Telecommunications industry is projected to be the fastest-growing from 2025 to 2032, with a CAGR of 4.90%, fueled by rising demand for high-speed internet, 5G network expansion, and enhanced data transmission. This growth is expected to boost silicon tetrachloride use in optical fibers and other telecommunications components, highlighting its importance in modern communication infrastructure.

Key Silicon Tetrachloride Market Regional Highlights

-

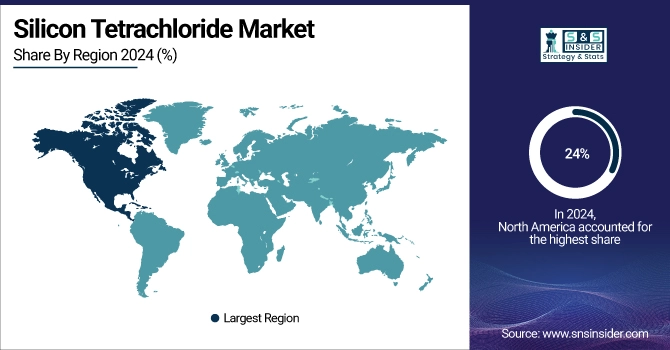

North America dominates the Silicon Tetrachloride Market with ~24% in 2024.

-

The U.S. Silicon Tetrachloride Market in North America leads with a market share of ~74% in 2024, while Canada exhibits the fastest growth.

-

Europe holds ~20% share in 2024, with Germany being the leading country.

-

Asia Pacific shows the fastest growth with ~46.20% share in 2024 and a CAGR of 4.32% during 2025–2032.

-

Middle East & Africa holds ~5% share, with the UAE leading the region.

-

Latin America accounts for ~6% share, with Brazil being the dominant country.

Key Silicon Tetrachloride Market Regional Analysis

North America Silicon Tetrachloride Market Insights

In 2024, North America emerged as a key region in the Silicon Tetrachloride Market due to its robust semiconductor and electronics manufacturing sectors. The United States leads regional growth, supported by the CHIPS and Science Act, which invests heavily in domestic semiconductor production and R&D. Canada is witnessing rapid expansion from increased applications in clean energy and high-performance materials. Major Silicon Tetrachloride Companies are also expanding production for high-purity silicon, reinforcing North America’s influential position in the global market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Silicon Tetrachloride Market Insights

Europe plays a significant role in the global market, driven by Germany’s strong industrial and chemical sectors and France’s focus on renewable energy technologies. EU policies promoting low-carbon technologies and high-tech manufacturing strengthen Europe’s presence in the Silicon Tetrachloride (SiCl4) Industry. Increased semiconductor wafer production and photovoltaic applications across Germany and France further contribute to regional growth, reflecting Europe’s stable yet influential role in the Global Silicon Tetrachloride Market.

-

Germany Silicon Tetrachloride Market Insights

In Europe, Germany leads due to its strong industrial base, chemical manufacturing capabilities, and high adoption of semiconductor technologies. The country supports the Silicon Tetrachloride (SiCl4) Industry with advanced infrastructure and government-backed initiatives for high-tech manufacturing. France is another key player, focusing on renewable energy and photovoltaic technology development. Together, Germany and France drive Europe’s market, leveraging policy incentives and growing production capacities to meet the increasing demand for high-purity silicon in chemicals, semiconductors, and solar panel applications.

Asia-Pacific Silicon Tetrachloride Market Insights

Asia Pacific dominates the global market and is the fastest-growing region, driven by China’s leadership in silicon production for semiconductors and solar panels. India’s expanding electronics, solar, and telecommunications industries contribute significantly to growth, while Japan innovates in advanced materials and photovoltaic applications. Government incentives and large-scale investments in renewable energy infrastructure are supporting regional expansion, highlighting the Asia Pacific’s critical role in Silicon Tetrachloride Market Trends.

-

China Silicon Tetrachloride Market Insights

In the Asia Pacific region, China is the dominant country, producing a substantial portion of the world’s silicon and driving demand for Silicon Tetrachloride in semiconductors and photovoltaic applications. The Chinese government’s policies to support renewable energy and electronics manufacturing further strengthen market growth. India is emerging rapidly, fueled by its expanding electronics, solar, and telecommunications sectors, making it a key market for high-purity silicon and optical fiber production. Japan maintains its competitive edge through advanced material innovation, semiconductor R&D, and photovoltaic technology development, supporting regional dominance in the Silicon Tetrachloride Market.

Latin America (LATAM) and Middle East & Africa (MEA) Silicon Tetrachloride Market Insights

The LATAM region, comprising Latin America and the Middle East & Africa, is witnessing steady growth. Brazil leads Latin America with industrial expansion and rising solar power initiatives, while the UAE and Saudi Arabia are driving regional growth with infrastructure and technology investments. Government support for high-purity silicon applications in renewable energy and chemicals further encourages Silicon Tetrachloride Market Growth, positioning LATAM as an emerging and promising region despite economic and infrastructural constraints.

Competitive Landscape for Silicon Tetrachloride Market:

Shin-Etsu Chemical is a leading global chemical company founded in 1926 and headquartered in Tokyo, Japan. It operates in several business segments, including Life Environment Materials, Functional Materials, and Electronics & Information Materials. The company is renowned for its production of polyvinyl chloride (PVC) resins, semiconductor silicon, and photomask substrates.

-

In May 2024, Shin-Etsu Chemical announced the development of new silicone products for personal care applications, enhancing texture and functionality in cosmetics.

Dow Inc. is a multinational materials science company established in 1897 and headquartered in Midland, Michigan, USA. It operates through various segments, including Packaging & Specialty Plastics, Industrial Intermediates & Infrastructure, and Performance Materials & Coatings. Dow's offerings in the silicone sector contribute to the silicon tetrachloride market, particularly in applications related to electronics and construction materials.

-

In April 2024, Dow announced a partnership with Circusil to build North America's first commercial-scale silicone recycling plant, slated to begin operations in Q4 2024.

Heraeus is a family-owned technology company founded in 1851 and headquartered in Hanau, Germany, with a focus on precious and special metals, medical technology, quartz glass, and sensors. The company's Semiconductor & Electronics division produces high-purity fused silica and preform materials, processes that historically involve silicon tetrachloride as a feedstock.

-

In September 2024, Heraeus launched the SOFIA initiative for sustainable optical-fiber production, targeting lower-carbon preform manufacturing and improved process efficiency.

Momentive Performance Materials Inc., headquartered in Waterford, New York, USA, is a global leader in the development and production of specialty chemicals and materials. Established in 2006, the company operates in various sectors, including electronics, automotive, construction, and consumer goods. Momentive offers a range of products such as silicones, silanes, and quartz, which are integral to the production of silicon tetrachloride.

-

In June 2024, Momentive announced the expansion of its silicone manufacturing facility in Ohio to meet the growing demand for high-performance materials in the electronics industry.

Silicon Tetrachloride Market Key Players:

-

Wacker Chemie AG

-

Shin-Etsu Chemical Co., Ltd.

-

OCI Co., Ltd.

-

Shaanxi Nonferrous Tianhong Silicon

-

Tokuyama Chemicals (Zhejiang) Co., Ltd.

-

Tangshan Sunfar Silicon

-

Henan Silane Technology

-

Zhejiang Zhongning Silicon Industry

-

Dow Inc. (Dow Corning)

-

Momentive Performance Materials

-

Heraeus Holding

-

American Elements

-

Kanto Denka Kogyo

-

Taiyo Nippon Sanso

-

Qinyang Guoshun Chemical

-

Hubei Heyuan Gas Co., Ltd.

-

Hubei Jingxing Service and Technology Co., Ltd.

-

Shanghai Wechem Chemical

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.51 Billion |

| Market Size by 2032 | USD 3.47 Billion |

| CAGR | CAGR of 4.12% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Grade (Electronics Grade, and Technical Grade) •By Derivatives (Fumed Silica, and Polysilicon), •By Application (Chemical Intermediate, Optical Fiber Preform, Commercial Catalyst, and Others) •By End-use Industry (Chemicals, Electronics, Oil & Gas, Telecommunications, Pharmaceuticals, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Wacker Chemie AG, Tokuyama Corporation, Shin-Etsu Chemical Co., Ltd., OCI Co., Ltd., Shaanxi Nonferrous Tianhong Silicon, Tokuyama Chemicals (Zhejiang) Co., Ltd., Shandong Xinlong Group Co., Ltd., Tangshan Sunfar Silicon, Henan Silane Technology, Zhejiang Zhongning Silicon Industry, Dow Inc. (Dow Corning), Momentive Performance Materials, Heraeus Holding, American Elements, Kanto Denka Kogyo, Taiyo Nippon Sanso, Qinyang Guoshun Chemical, Hubei Heyuan Gas Co., Ltd., Hubei Jingxing Service and Technology Co., Ltd., and Shanghai Wechem Chemical |

Frequently Asked Questions

Ans: The market is expanding with semiconductor-grade production increases, Wacker Chemie and OCI capacity expansions, and growing PV demand, reflecting the U.S. 33 GW and global 510 GW installed solar capacity in 2023.

Ans: Electronics (36.9% share in 2024), chemicals, and telecommunications are major consumers, driven by semiconductor fabrication, optical fiber production, and photovoltaic material manufacturing.

Ans: Growth is driven by a global semiconductor demand supported by $20–30 billion federal investments, renewable energy expansion, and increasing solar PV additions totaling 510 GW in 2023.

Ans: Silicon tetrachloride (SiCl?) is primarily used in producing high-purity silicon for semiconductors, photovoltaic cells, and optical fibers, with over 33 GW of solar capacity installed in the U.S. in 2023.

Ans: The Silicon Tetrachloride Market was valued at USD 2.51 billion in 2024 and is projected to reach USD 3.47 billion by 2032, growing steadily due to renewable energy and semiconductor demand.

Get in Touch