Gypsum Board Market Report Scope & Overview:

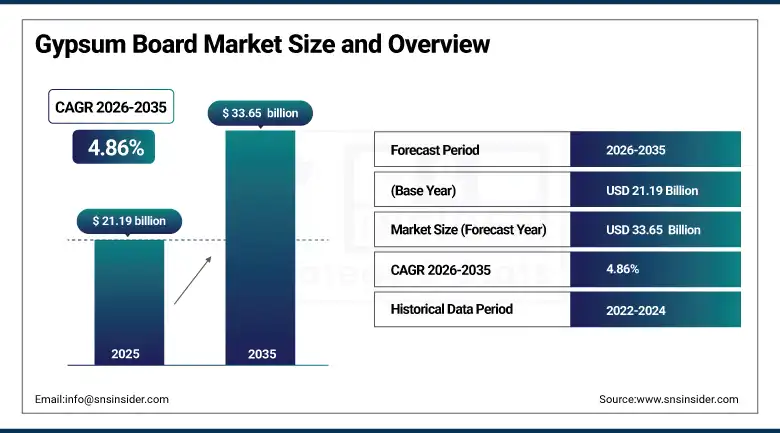

The Gypsum Board market was valued at USD 21.19 billion in 2025 and is expected to reach USD 33.65 billion by 2035, growing at a CAGR of 4.86% from 2026–2035.

Gypsum board, also widely known as drywall, plasterboard, or wallboard depending on regional terminology, is the dominant interior wall and ceiling surfacing material in modern construction across virtually every building type from residential single-family homes through large commercial office towers, healthcare facilities, educational institutions, and industrial buildings, having displaced the plaster and lath systems it replaced through a combination of dramatically faster installation, significantly lower labor cost, superior fire resistance properties arising from gypsum's inherent chemically bound water content that absorbs heat during combustion, and the ability to incorporate specialty performance characteristics including enhanced moisture resistance, sound attenuation, mound inhibition, and impact resistance through targeted formulation adjustments that make a single product category serve the diverse performance requirements of different building zones and occupancy types.

The Global Gypsum Association's 2025 market assessment confirming that over 27 billion square meters of gypsum board are produced annually worldwide reflects both the technology's extraordinary commercial penetration of the global construction market and the scale of the demand opportunity that continuing urbanization, housing shortfall remediation programmes, and commercial real estate development across emerging economies represent for the gypsum board industry over the 2026 to 2035 forecast period.

Market Size and Forecast

-

Market Size in 2026E: USD 22.22 Billion

-

Market Size by 2035: USD 33.65 Billion

-

CAGR: 4.86% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Gypsum Board Market - Request Free Sample Report

Gypsum Board Market Trends

-

Growing adoption of high-performance specialty gypsum board products including mound and moisture resistant boards for bathroom and kitchen applications, impact-resistant boards for high-traffic corridors and abuse-prone commercial spaces, and sound-attenuating multi-layer board assemblies for multi-family residential construction where noise transmission between units is a leading tenant satisfaction determinant and increasingly a regulatory compliance requirement.

-

Increasing use of synthetic gypsum recovered from power plant and industrial flue gas desulphurization processes as the primary raw material source for gypsum board manufacturing in markets with abundant synthetic gypsum supply, supporting both the circular economy credentials of gypsum board as a recycled material product and the raw material supply security of manufacturers in regions where natural gypsum mining access is constrained.

-

Rising adoption of lightweight gypsum board formulations incorporating expanded perlite, glass microspheres, or alternative lightweight aggregates that reduce panel weight by 15 to 25% versus standard formulations, reducing installation labor ergonomic injury risk, improving handling productivity on multi-story commercial construction sites, and enabling thinner panel formulations without sacrificing performance characteristics.

-

Expanding gypsum board application in green building certification programmes including LEED, BREEAM, and GREEN MARK where gypsum board's contribution to indoor air quality through its low volatile organic compound emission profile, thermal mass contribution to energy performance, and compatibility with recyclable building envelope assemblies provides certification credit points that sustainable building developers value.

-

Growing off-site construction and modular building techniques incorporating gypsum board into factory-fabricated wall panel assemblies that are transported to construction sites and erected without on-site drywall installation, reducing construction programme duration, improving installation quality control, and expanding gypsum board demand in the modular and prefabricated construction segment.

The U.S. Gypsum Board Market Outlook

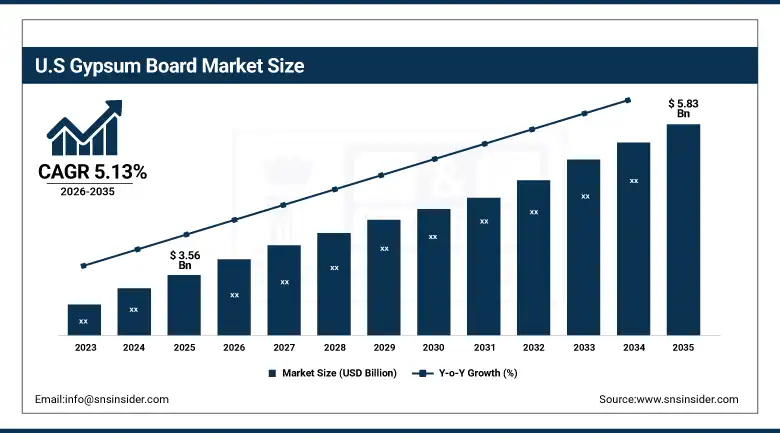

The U.S. Gypsum Board Market was valued at approximately USD 3.56 billion in 2025 and is expected to reach approximately USD 5.83 billion by 2035, growing at a CAGR of 5.13%.

The United States is the world's most mature and technically sophisticated gypsum board market, where USG Corporation, National Gypsum, CertainTeed (Saint-Gobain), Georgia-Pacific, and American Gypsum collectively dominate manufacturing across a network of plants strategically located near both natural gypsum mining operations and synthetic gypsum supply from utility power plants, with plant locations selected to minimize the freight cost that dominates gypsum board distribution economics given the product's high weight-to-value ratio and fragility in transport. The U.S. residential construction market's sustained supply deficit, estimated at three to five million housing units below demand by various analyses, is supporting elevated new residential construction starts that drive foundational gypsum board demand, while the enormous existing residential building stock of over 140 million housing units generates a large and relatively recession-resistant renovation and repair demand base.

The U.S. National Fire Protection Association's building code requirements for fire-rated gypsum board assemblies in residential multi-family, commercial, and institutional construction, combined with the International Building Code's adoption across the majority of U.S. jurisdictions mandating fire-rated construction in specific building components, create a regulatory compliance demand driver for Type X and enhanced Type C fire-rated gypsum board products that sustains premium-tier demand independent of discretionary construction activity cycles.

Gypsum Board Market Segment Analysis

-

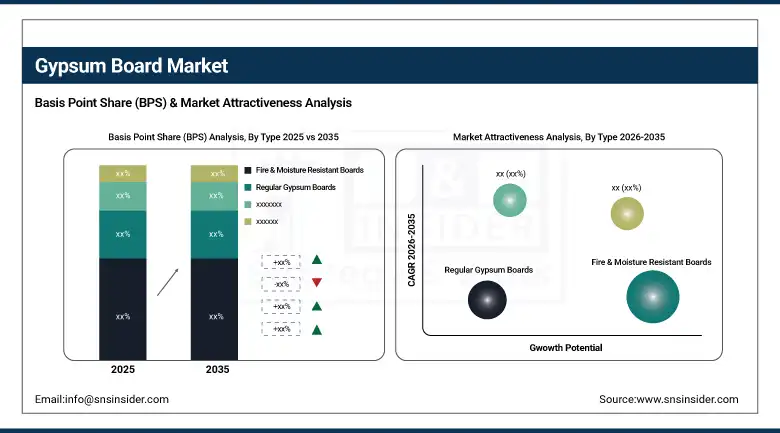

By Type, Fire & Moisture Resistant Boards dominated with approximately 48.13% in 2025; Regular Gypsum Boards is the fastest-growing segment at a CAGR of 5.80%.

-

By Installation Method, screwing into studs held approximately 54.38% in 2025; Gluing to concrete is the fastest-growing at a CAGR of 6.31%.

-

By Application, Ceilings & Wall Coverings dominated with approximately 49.25% in 2025; Gypsum Board Partitioning is the fastest-growing at a CAGR of 6.37%.

-

By End User, Residential maintained the largest share at approximately 53.91% in 2025; Commercial is the fastest-growing at a CAGR of 5.95%.

By Type, Fire & Moisture Resistant dominates, regular boards are expected to grow fastest

Fire and Moisture Resistant Boards retained the dominant type position with approximately 48.13% of the gypsum board market in 2025, reflecting the growing share of total gypsum board consumption that building code mandatory fire-rated construction and wet area moisture protection requirements represent across both new construction and renovation applications in all major markets. The proliferation of multi-family residential construction where party wall and floor-ceiling assembly fire rating requirements mandate Type X or enhanced fire-rated board in all separating assemblies, combined with the specification of moisture-resistant board in all bathroom, kitchen, and laundry room wet area installations regardless of building type, collectively ensure that specialty board products now constitute a significant plurality of total gypsum board consumption in developed market construction.

Regular Gypsum Boards are the fastest-growing segment at a CAGR of 5.80% through 2035, reflecting the base volume growth opportunity from the construction boom in emerging markets across Asia Pacific, the Middle East, Africa, and Latin America where both residential and commercial construction programmes are deploying gypsum board for the first time at scale, replacing the conventional plaster, brick infill, and concrete masonry wall systems that have historically dominated interior construction in these markets. The cost efficiency, installation speed, and design flexibility advantages of regular gypsum board relative to traditional masonry interior wall construction are proving compelling to developers in emerging markets where construction labor productivity and project schedule compression are becoming competitive priorities alongside material cost.

By End User, Residential dominates, commercial is expected to grow fastest

Residential end users retained the dominant position with approximately 53.91% of the gypsum board market in 2025, reflecting the global residential construction market's status as the primary driver of gypsum board demand volume through the combination of new housing construction serving the world's growing and urbanizing population and the home renovation and repair market that generates consistent gypsum board replacement demand from the vast existing residential building stock in mature markets.

Commercial applications are the fastest-growing end user at a CAGR of 5.95% through 2035, as the combination of office tower construction in rapidly growing Asian cities, hospitality and retail development supporting the growing consumer spending of expanding Asian and Middle Eastern middle classes, healthcare and educational facility construction responding to public investment in social infrastructure, and the renovation of ageing commercial building stock in developed markets collectively create a diversified and growing gypsum board demand base that is less cyclical than residential construction alone.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.3% |

|

Europe |

Germany |

24.1% |

|

Asia Pacific |

China |

53.6% |

|

Middle East & Africa |

UAE |

26.8% |

|

Latin America |

Brazil |

42.7% |

North America Gypsum Board Market Insights

North America is a large and mature gypsum board market with the United States accounting for approximately 85.3% of North American revenues. The region's market characteristics reflect an established industry with high per-capita gypsum board consumption driven by the prevalence of light-frame wood and steel construction across residential and commercial building types, well-developed regional manufacturing infrastructure minimizing freight costs to major construction markets, and a regulatory environment whose building codes create substantial demand for specialty fire-rated and moisture-resistant board products alongside standard construction grades. The U.S. housing supply deficit is providing sustained new residential construction demand that supplements the large and resilient renovation market across the existing housing stock.

Europe Gypsum Board Market Insights

Europe is a technically sophisticated gypsum board market characterised by strong adoption of drylining and partition system construction in both new build and renovation of the existing building stock, high awareness of gypsum board's acoustic, fire, and thermal performance capabilities, and the presence of major European manufacturers including Saint-Gobain, Knauf, and Etex whose product innovation sustains performance differentiation above commodity price competition from imports. Germany accounts for approximately 24.1% of European revenues as the region's largest construction market, where the combination of high residential construction quality standards, extensive commercial renovation of the post-reunification building stock, and strong export-oriented manufacturing sector investment sustaining industrial and commercial construction activity creates consistent high-volume gypsum board demand.

Asia Pacific Gypsum Board Market Insights

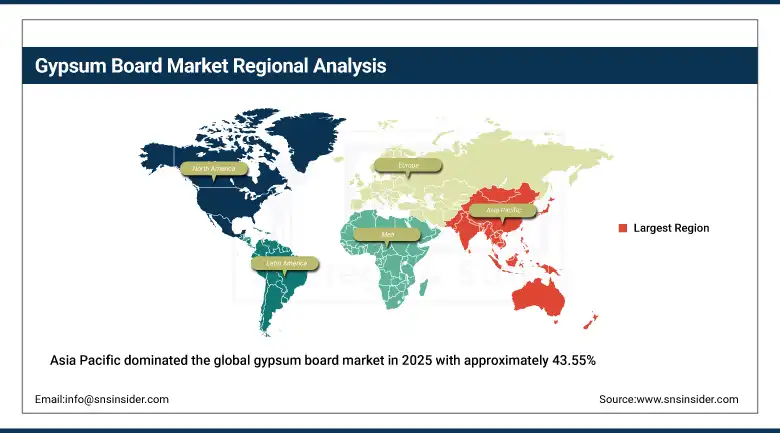

Asia Pacific dominated the global gypsum board market in 2025 with approximately 43.55% of revenues, anchored by China's position as both the world's largest gypsum board producer and consumer, combined with India's rapidly growing construction sector, Japan and South Korea's renovation activity, and the enormous infrastructure investment programmes across Southeast Asian nations. China accounts for approximately 53.6% of Asia Pacific revenues through its extraordinary annual construction volume encompassing both the continued urbanization of hundreds of millions of rural residents and the ongoing renovation and redevelopment of the building stock from earlier urbanization phases. The Chinese market is supplied by both major international manufacturers including Knauf and Saint-Gobain who operate Chinese production facilities and a substantial domestic manufacturing industry whose scale and cost position serves the price-sensitive volume segments of Chinese construction.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Gypsum Board Market Insights

The Middle East and Africa and Latin America are growing gypsum board markets where the combination of substantial new construction investment in Gulf Cooperation Council infrastructure and residential programmes, large-scale affordable housing construction initiatives across African nations, and Latin American commercial and residential construction expansion are creating growing demand for gypsum board as a superior alternative to traditional masonry interior wall systems. UAE leads MEA gypsum board revenues at approximately 26.8% of regional revenues through its extraordinary construction programme encompassing luxury residential towers, hospitality and retail developments, and commercial office buildings across Dubai and Abu Dhabi that consistently specify gypsum board ceiling and partition systems from Knauf, Saint-Gobain, and domestic producers.

Market Dynamics

Growth Drivers: Rising housing construction, increasing infrastructure investments, and growing renovation activities are driving market demand.

The primary structural growth drivers for the Gypsum Board Market are the global housing construction expansion driven by the accumulated residential supply deficit in developed economies where construction underperformance relative to household formation rates over the past decade has created housing shortfalls requiring sustained elevated construction activity to address, combined with the first-time adoption of modern interior construction techniques including gypsum board systems by the expanding residential and commercial construction programmes of Asian, African, and Latin American emerging economies whose rising income levels and urbanization rates are creating the demand for faster, better-performing, and more cost-effective interior construction solutions that gypsum board uniquely provides. The commercial renovation market's sustained investment in improving the energy performance, acoustic quality, and interior aesthetics of the enormous existing commercial building stock in mature markets is providing an additional and relatively recession-resistant demand source that supplements new construction volume.

Restraints: Raw material price volatility, high logistics costs, and cyclical construction demand are limiting market growth.

A significant restraint on the gypsum board market is the sensitivity of manufacturing economics to the energy cost of the calcination process that converts raw gypsum into the calcium sulphate hemihydrate plaster of Paris that gypsum board manufacturing requires, where natural gas price volatility translates directly into manufacturing cost variation that manufacturers in markets with limited ability to pass energy cost increases through to construction market customers must absorb in margin compression. The weight and fragility of gypsum board create freight cost economics that limit the competitive radius from manufacturing plants to approximately 300 to 500 kilometers for standard products in most markets, restricting competitive dynamics to regional markets and requiring manufacturers to maintain extensive local production capacity near construction demand centers rather than consolidating at fewer, larger, and potentially lower-cost production facilities.

Opportunities: Product innovation in smart gypsum boards, growth of modular and off-site construction, and rising demand from emerging markets are creating strong growth opportunities.

The development of smart gypsum board products incorporating integrated phase change thermal mass materials that store and release heat to reduce building energy consumption, thin-film solar photovoltaic coatings that generate electricity from ceiling and wall surfaces, and embedded sensor arrays enabling real-time structural health monitoring of building envelopes represent the frontier of gypsum board product innovation whose commercialization over the 2026 to 2035 forecast period could create premium product categories with substantially higher per-square-meter revenue than current specialty boards. The rapid growth of modular and off-site construction methodologies that incorporate gypsum board into factory-assembled wall, floor, and ceiling panels creates a new distribution channel for gypsum board manufacturers who can partner with modular construction companies to supply volumetrically consistent, quality-assured panels that feed manufacturing processes rather than on-site installation.

Recent Developments:

-

February 2026: USG Corporation (Gebr. Knauf KG) introduced an expanded range of ultra-lightweight gypsum board products for residential renovation applications, incorporating advanced hollow-microsphere aggregate technology reducing panel weight by 22% versus standard formulations while maintaining equivalent fire and structural performance characteristics.

-

2025: Saint-Gobain expanded its Gyproc specialty gypsum board range with new acoustic performance products targeting multi-family residential construction in Europe and North America, incorporating constrained layer damping technology achieving STC ratings previously achievable only through multiple-layer assemblies with added mass.

-

2025: Knauf Gypsum inaugurated a new manufacturing facility in Rajasthan, India, expanding its Indian production capacity to meet rapidly growing demand from residential and commercial construction projects in northern India where the company had been supply-constrained relative to available demand.

Gypsum Board Market Key Players are:

-

USG Corporation (Gebr. Knauf KG)

-

Saint-Gobain (CertainTeed, Gyproc)

-

Knauf Gypsum

-

National Gypsum Company

-

Georgia-Pacific LLC

-

American Gypsum (Eagle Materials)

-

Etex Group (Siniat)

-

LaFarge Holcim (Lafarge Plasterboard)

-

Yoshino Gypsum Co. Ltd.

-

Boral Limited

-

Pabco Gypsum

-

Temple-Inland

-

VANS Building Products Ltd.

-

Continental Building Products

-

Shreeji Gypsum Ltd.

-

Armstrong World Industries

-

BNBM Group

-

Taishan Gypsum Co. Ltd.

-

Formosa Plastics Corp.

-

Beijing New Building Materials

Gypsum Board Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.19 Billion |

| Market Size by 2035 | USD 33.65 Billion |

| CAGR | CAGR of 4.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Regular Gypsum Boards, Fire & Moisture Resistant Boards, Others) • By Installation Method (Screwing into Studs, Gluing to Concrete, Others) • By Application (Ceilings & Wall Coverings, Gypsum Board Partitioning, Others) • By End User (Residential, Commercial, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | USG Corporation (Gebr. Knauf KG), Saint-Gobain (CertainTeed, Gyproc), Knauf Gypsum, National Gypsum Company, Georgia-Pacific LLC, American Gypsum (Eagle Materials), Etex Group (Siniat), LaFarge Holcim (Lafarge Plasterboard), Yoshino Gypsum Co. Ltd., Boral Limited, Pabco Gypsum, Temple-Inland, VANS Building Products Ltd., Continental Building Products, Shreeji Gypsum Ltd., Armstrong World Industries, BNBM Group, Taishan Gypsum Co. Ltd., Formosa Plastics Corp., and Beijing New Building Materials. |

Frequently Asked Questions

Asia Pacific dominated with approximately 43.55% of revenues in 2025.

Fire & Moisture Resistant Boards dominated with approximately 48.13% of revenues in 2025.

Global housing construction expansion addressing structural residential supply deficits combined with first-time adoption of modern gypsum board interior construction in rapidly developing Asian and African construction markets and commercial renovation investment sustaining demand in mature markets.

The Gypsum Board Market was valued at USD 21.19 billion in 2025.

The Gypsum Board Market is expected to grow at a CAGR of 4.86% from 2026 to 2035.

Get in Touch