Wind Turbine Composites Material Market Size Analysis

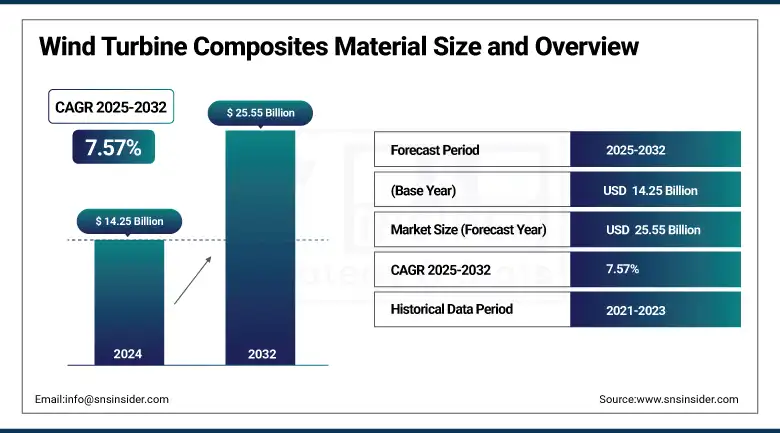

The Wind Turbine Composites Material Market size was valued at USD 14.25 billion in 2024 and is expected to reach USD 25.55 billion by 2032, growing at a CAGR of 7.57% over the forecast period of 2025-2032.

The wind turbine composites material market analysis shows the demand for lightweight and stronger blade materials as one of the market's primary growth motivators. The trend towards larger and higher-power wind turbines in both onshore and offshore applications has greatly increased the need for materials to resist high mechanical loading while maintaining structural integrity. Lightweight composites, including glass fiber and carbon fiber, play an important role in reducing the total weight of the turbine, improving power efficiency, and performance of the blade. They allow for longer blades that also capture more wind to produce more power. Furthermore, their high strength-to-weight ratio leads to low transportation and installation costs, thus increasing their applicability to modern wind turbine design which drive the wind turbine composites material market growth.

To Get more information On Wind Turbine Composites Material - Request Free Sample Report

In February 2023, DOE's Advanced Materials & Manufacturing Technologies Office issued a USD 30 million funding opportunity to spur the development of composite materials and additive manufacturing approaches for large wind turbine blades, including offshore designs.

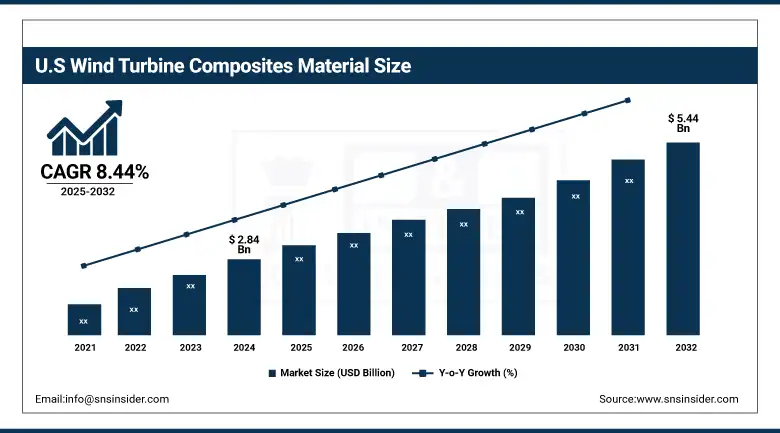

The U.S. wind turbine composites material market size was USD 2.84 billion in 2024 and is expected to reach USD 5.44 billion by 2032 and grow at a CAGR of 8.44% over the forecast period of 2025-2032. The U.S. was the leader of the North American market, supported by federal clean energy legislation like the Inflation Reduction Act (IRA), which drives tax credits and incentives for wind energy development and domestic manufacturing. This has resulted in a dramatic increase in manufacturing capacity for composite blade materials components such as turbine blades, towers, and nacelles. Manufacturers in the U.S. are investing in automation and sustainable composite technologies to meet demand and reduce dependency on imported parts.

Wind Turbine Composites Material Market Dynamics

Drivers

-

Increasing Demand for Lightweight, High-Strength Blade Materials Drives the Market Growth

The booming trend of bigger and efficient wind turbines, in particular offshore, has considerably boosted the consumption of composite materials such as glass fiber and carbon fiber. With superior stiffness relative to weight, these materials allow longer blades that produce more power with less stress on turbine parts. The use of lighter composites also simplifies transport and reduces installation costs. This change encourages for more energy efficiency, reduced LCOE (levelized cost of energy), as well as an extended lifetime. The use of composites is increasing as manufacturers and developers search for high-performance materials that can survive the most arduous conditions.

In October 2023, the US Department of Energy's (DOE) National Renewable Energy Laboratory (NREL), with IACMI, received USD 4.1 million in federal funding to support research that can help create lighter, longer wind turbine blades utilizing next-generation composite materials.

Restrain

-

High Manufacturing and Recycling Costs of Composite Materials May Hamper the Market Growth

Carbon fiber, in particular, is an energy-intensive process and requires complex molding techniques, making it an expensive material to produce, despite its performance advantages in wind turbines. In addition, traditional composites are hard and costly to recycle, which is a serious obstacle for their end-of-life management. As the industry faces growing sustainability scrutiny, the non-biodegradable waste from retired turbine blades has raised eyebrows. This impedes larger-scale use of composites, especially in price-sensitive regions or smaller projects. There are efforts toward touring, recyclable or bio-based substitutes, but this is still under evolution.

Opportunities

-

Innovation in Recyclable and Sustainable Composite Solutions Creates an Opportunity in the Market

There is a great opportunity with recyclable, bio-based, and thermoplastic composite materials that minimize environmental footprint but retain comparable mechanical performance. Tier one suppliers are investing in next-gen resin systems and modular blade designs to support circular economy objectives. This is especially since thousands of old turbines are facing retirement in the next 10 years. Utilizing green composites will enable wind projects to meet increasingly stringent environmental requirements and contribute to long-term sustainability, which drive the wind turbine composites material market trends.

In December 2024, the US DOE's Wind Energy Technologies Office funded USD 20 million in new investments in materials for recyclable wind turbine blade technologies that can facilitate a transition to a circular economy in composite design.

Wind Turbine Composites Material Market Segmentation Analysis

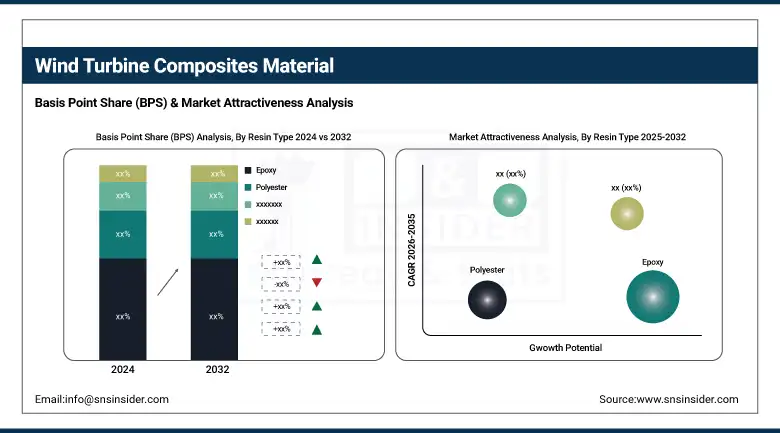

By Resin Type

Epoxy held the largest wind turbine composites material market share, around 52%, in 2024. It is owing to being responsive to mechanical properties, effective in adhesion, highly resistant to chemicals, and having excellent fatigue performance, which is a critical minimum requirement for construction of modern wind turbine blades. Plastic epoxies are typically combined with glass or carbon fibers to yield lightweight and high strength composites that are capable of withstanding extreme environmental conditions (i.e., temperature, humidity, and UV). They form strong, permanent bonds, making them ideal for the large turbine blades used in both onshore and offshore installations.

Polyester held a significant wind turbine composites material market share. It is due to cost-effectiveness, availability, and processing ease, polyester was a dominant segment for turbine blade production and among a major share in the overall wind turbine composites material market for structural and non-structural turbine components. Polyester resin, with lower mechanical strength and thermal resistance than epoxy, is a common resin type used in small to medium-sized turbine blades, nacelle covers, and other parts with moderate performance requirements.

By Fiber Type

Glass Fiber composites segment held the largest market share, around 68%, in 2024. It is due to the excellent combination of mechanical properties, low cost, manufacturing efficiency, and lightweight nature offered by glass fiber. Because of its good strength-to-weight ratio, corrosion resistance, and low cost, glass fiber is a common material used in producing wind turbine blades, nacelles, and other such structural components. The property is ideal for both onshore and offshore turbines, where the most important thing is that it focuses on durability and fatigue-oriented, which can make our end product last longer.

Carbon fiber has a significant market share in the wind turbine composites material market. It can be attributed to its high stiffness-to-weight ratio, high stiffness, and excellent fatigue resistance, which are key properties for the next generation of large high-performance wind turbine blades. With the need to utilize bigger wind turbines to harness increased amounts of energy, particularly in offshore settings, this has led to carbon fibre composites playing an ever-expanding role in the use of spar caps and load-bearing structures where minimization of mass and structural performance is of critical importance.

By Application

Blades segment held the largest market share, around 75%, in 2024.The growth in offshore methods has driven the need for longer, lighter turbine blades, made from advanced composites. Modern blades reach structural lengths of more than 80 meters which makes them one of the biggest structures built by mankind, and which in turn is driving the need for sustainable, well-performing materials that have to be permanent under extreme dynamic mechanical loading for decades. In addition to this, the global transition to renewable energy heralded by massive wind farm developments has continued to drive up blade production and cement this segment as the largest consumer of composites materials.

Nacelles held a significant market share in the wind turbine composites material market. It is because nacelles are crucial in the development of wind turbines as they house the major components of turbines, including the gearbox, generator, and drive train. These enclosures shall be not only lightweight but also rugged enough to safeguard inner systems against the impact of the surrounding environment, especially moisture, UV, and mechanical stress, since it is common to have offshore and high-altitude installations. For nacelle construction, composite materials, especially fiberglass, are used owing to their anti-corrosive nature, easy molding to complex shapes, and reduced weight for the complete nacelle while maintaining its strength.

Wind Turbine Composites Material Market Regional Outlook

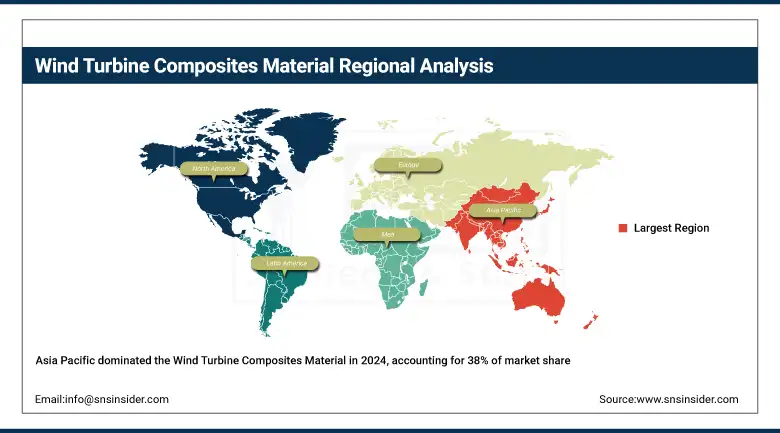

Asia Pacific wind turbine composites material market held the largest market share, around 38%, in 2024. It is owing to rapid industrialization, growing renewable energy targets, and large-scale wind power installations in countries such as China, India, and Japan. It has significant government backing, lower-cost manufacturing, and investment in offshore wind. Countries like China are taking the lead in global wind energy development, both onshore and offshore. This leadership is supported by advancements in cutting-edge composite materials, which enable the production of increasingly larger turbine blades. These innovations contribute significantly to cost efficiencies, reinforcing the region’s dominant position in the global wind energy market.

Get Customized Report as per Your Business Requirement - Enquiry Now

In 2024, China commissioned 39 GW of new offshore wind projects continuing to lead the world in new wind capacity additions and strengthening the need for higher-performance composites in blades, nacelles, and more.

North America wind turbine composites material market held a significant market share and is the fastest-growing segment in the forecast period. It is due to strict renewable energy policies, growing installations of wind power, and a well-established base of manufacturing. The blistering pace of clean energy development in the region has led to investments in wind farms and domestic component manufacturing in both the U.S. and Canada. Advanced technology dissemination in composite fabrication and increased interest in energy independence from the North American power infrastructure are important drivers in the utilization of local wind turbine components made from high-performance composites, primarily blades and nacelles.

In April 2024, several U.S.-based manufacturers of wind components announced they would expand factories to take advantage of tax credits linked to the IRA in order to help reach the national goal of doubling offshore and onshore wind installations by 2030.

Europe held a significant market share in the forecast period. It is owing to its aggressive carbon neutrality goals and accelerated offshore wind expansion. With the EU mandating clean energy growth, anticipation for lightweight, durable composites in turbine componentry demands high attention. Germany, the UK, and the Netherlands are spearheading the utilization and development of offshore wind investments, infrastructure, and the emphasis on the use of recyclable and eco-efficient composite consumption

In April 2025, a US private equity firm secured a €1 billion buy-out of Norwegian offshore wind installation firm Havfram, highlighting investor confidence in not only Europe’s offshore wind growth but also the supply chain for composite-intensive turbine systems.

Key Players in the Wind Turbine Composites Material Market

The major wind turbine composites material companies are TPI Composites, Hexcel Corporation, Teijin Limited, Toray Industries, LM Wind Power, Vestas Wind Systems, Siemens Gamesa Renewable Energy, Gurit Holding, Suzlon Energy, and Mitsubishi Chemical.

Recent Development in the Wind Turbine Composites Material Market

-

In February 2025, BodoMoller Chemie & DowAksa signed a strategic alliance agreement concerning advanced carbon fiber composites supply, including fabrics and prepregs, to maximize the performance and durability of blades.

-

In June 2024, DowAksa Ileri Kompozit secured a USD 300million, four-year supply agreement with global leader Vestas Wind Systems to provide advanced composite materials for wind turbine blades.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 14.25 Billion |

| Market Size by 2032 | USD 25.55 Billion |

| CAGR | CAGR of 7.57% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Epoxy, Polyester, Vinyl Ester) • By Fiber Type (Glass Fiber, Carbon Fiber) • By Application (Blades, Nacelles, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | TPI Composites, Hexcel Corporation, Teijin Limited, Toray Industries, LM Wind Power, Vestas Wind Systems, Siemens Gamesa Renewable Energy, Gurit Holding, Suzlon Energy, Mitsubishi Chemical. |

Frequently Asked Questions

Challenges include high manufacturing and recycling costs of composites, supply chain constraints, and limited recyclability of traditional materials.

Asia-Pacific held the largest market share, driven by large-scale installations and manufacturing capacity.

The rise in wind energy installations, demand for lighter, durable blade materials, and supportive government policies for renewable energy.

Glass fiber and epoxy resin dominate the market due to their high strength-to-weight ratio, cost-effectiveness, and wide application in blades and nacelles.

The market was valued at USD 13.25 billion in 2024 and is projected to grow at a CAGR of around 7.57% from 2025 to 2032.

Get in Touch