Smart Helmet Market Report Scope & Overview:

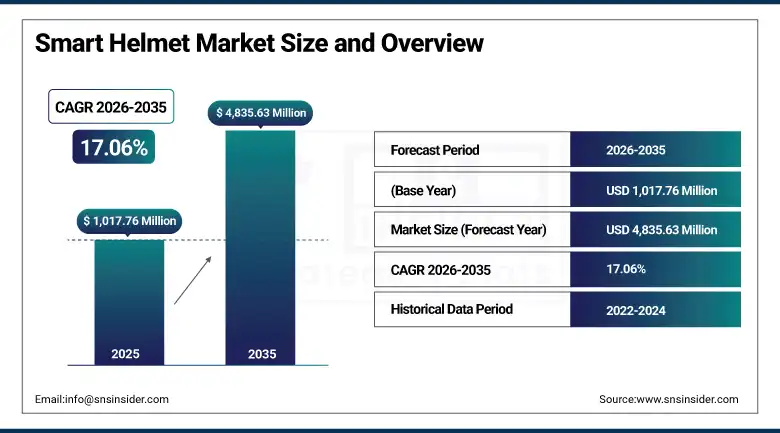

The Smart Helmet Market was valued at USD 1,017.76 Million in 2025 and is expected to reach USD 4,835.63 Million by 2035, growing at a CAGR of 17.06% from 2026–2035.

The global smart helmet market is growing at an exceptional pace. Smart helmets are advanced protective headgear integrating electronic systems including Bluetooth communication, GPS navigation, augmented reality head-up displays, action cameras, IoT sensors, and fitness tracking capabilities that transform conventional passive protection into connected intelligent wearable platforms. Growing demand for safety and connectivity, particularly among motorcyclists, cyclists, construction workers, and industrial field workers, is driving adoption across both consumer leisure and enterprise safety application categories.

In 2024, Forcite Helmet Systems launched the Forcite MK1S smart motorcycle helmet with enhanced AI-powered collision detection, integrated 4K front camera with image stabilisation, and improved Bluetooth mesh communication range enabling rider-to-rider communication at extended distances. The MK1S’s collision detection system automatically alerts emergency contacts with GPS location when a crash event is detected, creating a connected safety capability whose life-saving potential sustains premium pricing in the safety-conscious motorcycle commuter and touring rider market.

Market Size and Forecast

-

Market Size in 2026E: USD 1,191.46 Million

-

Market Size by 2035: USD 4,835.63 Million

-

CAGR: 17.06% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: North America

To Get more information On Smart Helmet Market - Request Free Sample Report

Smart Helmet Market Trends

-

Integration of augmented reality head-up displays is creating advanced smart helmets with navigation, communication, and real-time riding information capabilities

-

Adoption of smart helmets in construction, mining, and industrial environments is increasing due to enhanced worker safety, monitoring, and communication features

-

LiDAR and collision warning technologies are being incorporated into cycling and e-bike helmets to improve rider awareness and road safety

-

Advancements in lightweight materials such as carbon fiber and high-performance composites are improving comfort and usability of smart helmets

-

5G connectivity is enabling real-time data transmission, video streaming, cloud-based navigation, and emergency communication functions in next-generation smart helmets

U.S. Smart Helmet Market Outlook

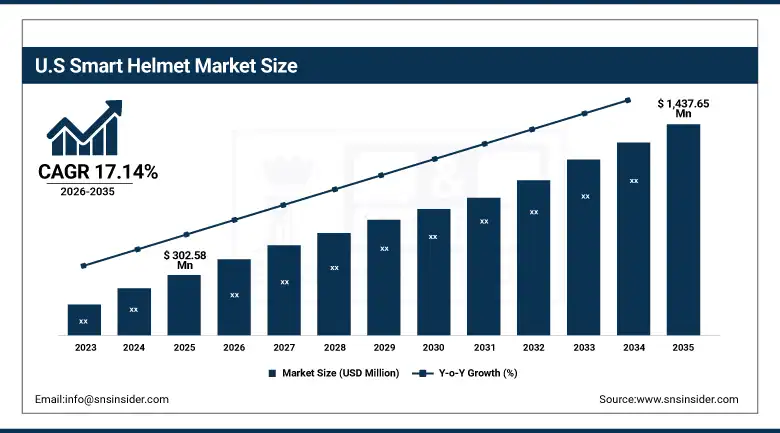

The U.S. Smart Helmet Market was valued at approximately USD 302.58 Million in 2025 and is expected to reach approximately USD 1,437.65 Million by 2035, growing at a CAGR of approximately 17.14%.

The U.S. is the most commercially sophisticated smart helmet market within the dominant North American region. Bell Helmets, LIVALL, Sena Technologies, and Forcite’s North American distribution collectively define the U.S. commercial landscape. OSHA’s industrial head protection standards, the motorcycle safety community’s above-average technology adoption, and the cycling commuter market’s safety investment create diverse domestic demand channels. The construction sector’s growing IoT safety investment, the motorcycle touring community’s communication system adoption, and the military’s advanced smart helmet programme create structured procurement across consumer, industrial, and government end-user categories.

LIVALL launched the EVO21 smart cycling helmet in 2024 with enhanced rear-facing radar detection through integrated Garmin Varia compatibility, automatic brake light activation, and group riding communication that creates a comprehensive connected cycling safety platform. The EVO21’s integration of multiple safety and connectivity features in a single commercially accessible helmet demonstrates the consumer smart helmet market’s progression toward all-in-one safety platforms whose adoption creates above-average per-unit commercial value in the premium cycling and e-bike commuter market segment.

Smart Helmet Market Segment Analysis

-

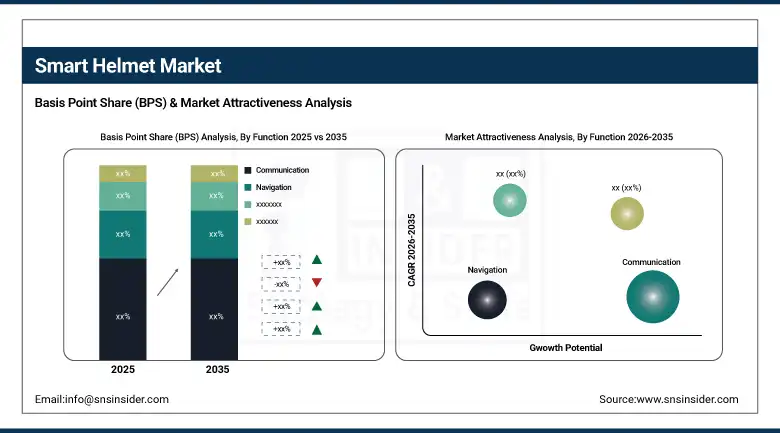

By Function, the Communication segment dominated the Smart Helmet Market with approximately 38% share in 2025, , while the Navigation segment is the fastest growing with a CAGR of 18.90%.

-

By Technology, the Bluetooth segment dominated the Smart Helmet Market with approximately 45% share in 2025, while the Augmented Reality/AR segment is the fastest growing.

-

By End User, the Consumer segment dominated the Smart Helmet Market with approximately 74% share in 2025, while the Industrial segment is the fastest growing.

By Function, communication dominates, navigation grows fastest

Communication retained the dominant function position with approximately 38% of the smart helmet market in 2025. Helmet-integrated Bluetooth communication’s ability to enable motorcycle rider-to-rider, rider-to-passenger, and rider-to-phone hands-free communication creates the most commercially established smart helmet feature whose adoption across the motorcycle touring and commuter community creates consistent procurement. Sena, Cardo, and UCLEAR’s Bluetooth helmet communication systems collectively demonstrate the commercial infrastructure that sustains communication feature’s dominant market position across both standalone Bluetooth communicator retrofits and integrated smart helmet systems. Industrial hand-free communication for construction, mining, and hazardous environment coordination creates enterprise communication helmet procurement whose safety compliance motivation sustains above-average per-unit commercial value.

Navigation is the fastest-growing function at 18.90% CAGR because GPS-based motorcycle navigation’s heads-up display integration eliminates the smartphone mounting requirement that conventional navigation creates, improving rider safety whose attention diversion elimination creates safety motivation beyond mere convenience. Each motorcycle helmet that integrates turn-by-turn AR navigation creates commercial differentiation whose functionality premium sustains specification in the premium touring and commuter motorcycle market. Logistics rider navigation for last-mile delivery creates industrial navigation smart helmet procurement whose operational efficiency improvement creates structured enterprise adoption motivation.

By End User, consumer dominates, industrial grows fastest

Consumer end users retained the dominant position with approximately 74% of the smart helmet market in 2025. Motorcyclists’ above-average technology adoption and willingness to invest in premium safety gear, cyclists’ growing smart helmet interest for urban commuting safety, and adventure sports participants’ recording and communication function preference collectively create the consumer market’s dominant position. Each new smart helmet product generation that improves communication range, navigation capability, or camera quality creates upgrade procurement whose consumer market’s enthusiast engagement sustains commercial momentum through product cycle iterations.

Industrial end users are the fastest-growing segment because construction, mining, and hazardous manufacturing environment deployment of smart helmets for worker safety monitoring creates structured corporate procurement whose occupational safety compliance motivation sustains investment through budget cycle variation. Each construction site that deploys smart helmets with fall detection, location tracking, and gas exposure monitoring creates enterprise procurement whose worker safety investment delivers measurable accident frequency reduction and insurance cost benefit. The mining sector’s remote operation environment creates particular smart helmet communication and monitoring value whose operational necessity sustains premium specification.

By Technology, Bluetooth dominates, AR grows fastest

Bluetooth retained the dominant technology position with approximately 45% of the smart helmet market in 2025. Bluetooth’s universal smartphone compatibility, mature safety certification, and low power consumption create the most commercially accessible wireless connectivity foundation for smart helmet communication, audio, and phone interface capability. Each motorcyclist who adopts Bluetooth helmet communication creates procurement whose installed base compounds with the global motorcycle market’s growth. The Bluetooth SIG’s progressive standard development, including Bluetooth 5.x’s extended range and mesh networking capability, creates technology infrastructure whose advancement sustains commercial relevance across successive smart helmet product generations.

AR technology is the fastest-growing because heads-up display integration’s ability to overlay navigation, speed, communication alerts, and environmental data on the rider’s field of view without requiring eye movement from the road creates safety and convenience value whose commercial realisation through helmet-integrated optics and projector miniaturisation is progressively reducing production cost toward commercially accessible price points. JARVISH’s AR helmet and industry development programmes collectively demonstrate the commercial AR helmet trajectory whose cost reduction creates mainstream adoption motivation as production scale economics improve.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Smart Helmet Market Insights

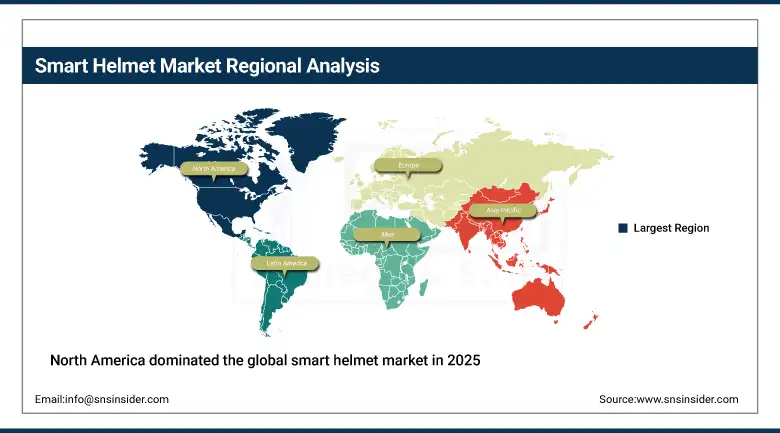

North America dominated the global smart helmet market in 2025 and is simultaneously the fastest-growing regional market. The United States accounts for approximately 87.4% of North American revenues through Bell Helmets, Sena, LIVALL, and Forcite’s commercial operations. The U.S.’s above-average motorcycle touring culture, the cycling commuter market’s safety investment, and the construction sector’s IoT safety programme create the world’s most commercially diverse smart helmet demand environment whose multiple application categories sustain above-average market growth.

Canada contributes approximately 12.6% of North American revenues through its motorcycle touring market, the growing cycling commuter community, and the construction sector’s smart safety equipment adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Smart Helmet Market Insights

Europe is a technically sophisticated smart helmet market where EU’s road safety regulation, ECE 22.06 helmet standard’s progressive safety requirement, and the motorcycle touring culture’s technology adoption create structured demand. Germany accounts for approximately 22.3% of European revenues through its motorcycle touring sector’s above-average technology specification, the construction sector’s worker safety investment, and the cycling commuter market’s smart helmet adoption.

The United Kingdom, France, and Italy are significant secondary markets where motorcycle culture, cycling safety legislation, and industrial safety regulation create consistent smart helmet procurement across consumer and enterprise end-user categories.

Asia Pacific Smart Helmet Market Insights

Asia Pacific is a rapidly growing smart helmet market, driven by China’s enormous motorcycle and e-bike market whose regulatory safety mandate creates above-average smart helmet demand, India’s two-wheeler market’s growing safety awareness, Japan’s motorcycle technology adoption, and the industrial sector’s worker safety investment. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary two-wheeler market scale, Beijing BaBaALi Technology and domestic smart helmet manufacturer development, and the government’s road safety programme.

India’s rapidly growing motorcycle market and South Korea’s technology adoption create significant secondary markets whose combined procurement sustains Asia Pacific’s growing commercial momentum.

MEA & Latin America Smart Helmet Market Insights

UAE leads MEA revenues at approximately 38.4% through its luxury motorcycle market’s premium smart helmet specification, the construction sector’s smart safety adoption, and the technology sector’s wearable innovation investment. Brazil leads Latin American revenues at approximately 44.2% through its large motorcycle market’s growing safety investment, the construction sector’s occupational safety programme, and the cycling community’s smart helmet adoption.

Saudi Arabia’s motorcycle market and South Africa’s industrial sector create significant MEA secondary markets whose smart helmet procurement reflects progressive road and workplace safety standard adoption.

Market Dynamics

Growth Drivers: Motorcycle safety technology adoption and industrial worker safety regulation creating dual demand vectors

Growing safety consciousness among motorcyclists, cyclists, and adventure sports participants is the consumer smart helmet market’s most commercially compelling growth driver. The documented fatal accident risk reduction that connected safety features including fall detection emergency alerting, rear collision warning, and hands-free communication create creates consumer motivation whose safety value sustains premium pricing above conventional helmet alternatives. Each new smart helmet product generation that demonstrates safety technology improvement creates consumer upgrade motivation whose compound growth with the global two-wheeler market’s expansion sustains above-average commercial momentum.

Industrial worker safety regulation’s progressive strengthening creates non-discretionary enterprise smart helmet procurement whose compliance character sustains investment through economic cycle variation. OSHA’s head protection standard evolution toward connected safety systems, the mining industry’s IoT worker monitoring programme, and the construction sector’s real-time safety monitoring investment collectively create structured enterprise smart helmet demand whose occupational safety motivation creates above-average per-unit commercial value.

Restraints: High cost limiting mass market adoption and battery life constraint reducing practical operational use

Smart helmet’s premium pricing relative to conventional helmet alternatives, typically 3-5 times the cost of standard safety helmets, creates adoption barriers in cost-sensitive consumer and enterprise markets whose value calculation must demonstrate financial justification beyond safety motivation alone. Each potential buyer whose safety awareness is insufficient to justify the premium investment creates a market penetration ceiling that price reduction through manufacturing scale and component cost reduction must progressively eliminate.

Battery life limitation in current smart helmet designs, where communication and display features reduce operational duration to 8-12 hours before recharging, creates practical limitations for long-distance motorcycle touring and full-day industrial deployment whose operational duration requirements exceed battery capacity. Each product generation’s battery technology improvement reduces but does not eliminate this constraint whose resolution requires either battery capacity increase or power consumption reduction through more efficient electronics.

Opportunities: AR heads-up display commercialisation and industrial IoT safety mandate expansion

AR heads-up display smart helmet commercialisation represents the most commercially premium near-term opportunity whose rider safety and navigation convenience creates value proposition that Bluetooth communication alone cannot match. Each AR helmet product that achieves production cost reduction toward USD 500-800 price accessibility creates mainstream adoption motivation whose commercial scale compounds with the motorcycle touring market’s technology appreciation.

Industrial IoT safety mandate expansion creates the most commercially certain enterprise smart helmet procurement growth whose occupational safety regulation compliance creates non-discretionary investment. Each new construction, mining, or industrial safety regulation that mandates connected worker monitoring creates structured procurement whose aggregate across global industrial sector safety programme expansion sustains above-average industrial smart helmet market development.

Recent Developments:

-

2024: Forcite Helmet Systems launched the Forcite MK1S smart motorcycle helmet in 2024 with enhanced AI-powered collision detection, integrated 4K front camera with image stabilisation, and improved Bluetooth mesh communication range enabling automatic emergency contact alerting on crash detection.

-

2024: LIVALL launched the EVO21 smart cycling helmet in 2024 with enhanced rear-facing radar detection through Garmin Varia integration, automatic brake light activation, and group riding communication creating a comprehensive connected cycling safety platform.

-

2024: Sena Technologies launched the Sena 50S motorcycle communication system with integrated AI noise control in 2024, featuring mesh intercom capability for multi-rider group communication at expanded range and improved voice clarity in high-noise riding environments.

Smart Helmet Market Key Players

-

Bell Helmets

-

Sena Technologies Inc.

-

LIVALL Tech Co., Ltd.

-

Forcite Helmet Systems

-

Lumos Helmet US

-

JARVISH INC

-

Crosshelmet

-

Beijing BaBaALi Technology Co., Ltd.

-

Intelligent Cranium Helmets LLC

-

H&H Sports Protection USA Inc.

-

TVS Motor Company

-

Hedkayse

-

MapmyIndia

-

TORC Helmets

-

Nexsys Co., Ltd.

-

360fly Inc.

-

LifeBEAM Technologies

-

Cardo Systems

-

Schuberth GmbH

-

AGV Helmets (Dainese)

Smart Helmet Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1017.76 Million |

| Market Size by 2035 | USD 4835.63 Million |

| CAGR | CAGR of 17.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Function/Feature (Communication, Navigation, Head-Up Display/HUD, Action Camera/Recording, Fitness & Activity Tracking, Others) • by Technology (Bluetooth, Wi-Fi, GPS, Augmented Reality/AR, IoT Integration, Others) • by End User (Consumer/Motorcyclists & Cyclists & Sports, Industrial/Construction & Mining & Manufacturing, Defence & Military, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Bell Helmets, Sena Technologies Inc., LIVALL Tech Co., Ltd.. Forcite Helmet Systems, Lumos Helmet US, JARVISH INC, Crosshelmet, Beijing BaBaALi Technology Co., Ltd., Intelligent Cranium Helmets LLC, H&H Sports Protection USA Inc., TVS Motor Company, Hedkayse, MapmyIndia, TORC Helmets, Nexsys Co., Ltd., 360fly Inc., LifeBEAM Technologies, Cardo Systems, Schuberth GmbH, AGV Helmets (Dainese) |

Frequently Asked Questions

The Smart Helmet Market is expected to grow at a CAGR of 17.06% from 2026 to 2035.

The Smart Helmet Market was valued at USD 1,017.76 Million in 2025.

Growing demand for safety and connectivity features including integrated communication systems, and industrial worker safety regulation creating dual commercial demand growth vectors.

Communication dominated the Smart Helmet Market with approximately 38% share in 2025 (SNS confirmed), while Navigation is the fastest growing with a CAGR of 18.90%.

Consumer dominated the Smart Helmet Market with approximately 74% share in 2025 (SNS confirmed), while Industrial is the fastest growing segment.

Get in Touch