Soil Testing Equipment Market Report Scope & Overview:

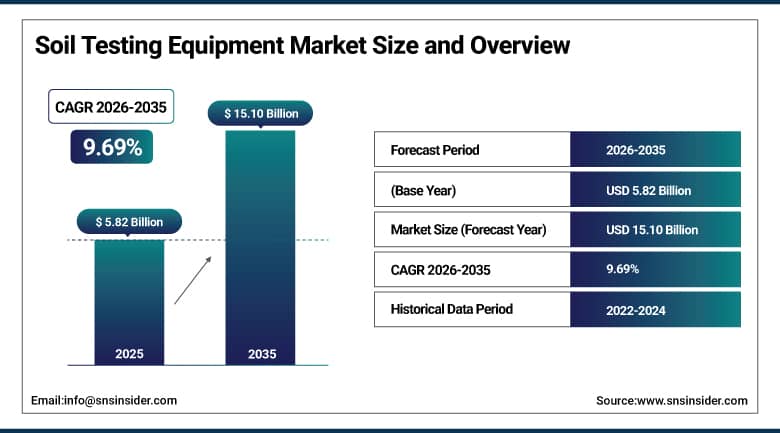

The Soil Testing Equipment Market was valued at USD 5.82 Billion in 2025 and is expected to reach USD 15.10 Billion by 2035, growing at a CAGR of 9.69% from 2026–2035.

The global soil testing equipment market is experiencing sustained growth driven by the dual imperatives of precision agriculture adoption and infrastructure safety compliance. Accurate soil analysis is the foundational data requirement for optimizing fertilizer application, irrigation scheduling, and crop selection decisions that drive both farm productivity and environmental compliance. In construction and civil engineering, geotechnical soil testing determines foundation design parameters, bearing capacity, and slope stability calculations that are legally mandated before major infrastructure development begins. Rising awareness of nutrient-based fertilizer optimization, climate-smart agriculture investment, and environmental soil contamination monitoring are collectively expanding the market beyond traditional agricultural and construction demand. Government regulatory frameworks across North America, Europe, and Asia Pacific are strengthening soil quality monitoring requirements in both agricultural and infrastructure sectors, creating compliance-driven procurement that sustains demand through economic cycle variations.

Martin Lishman launched a new range of soil testing kits in May 2025, offering rapid pH, conductivity, and NPK (nitrogen-phosphorus-potassium) analysis for field-based agricultural assessment. The launch targets commercial farmers and agronomists seeking portable, immediate-result testing alternatives to laboratory submission workflows, directly addressing the time-to-insight gap that delays fertilizer application optimization decisions during critical crop growth windows.

Market Size and Forecast

- Market Size in 2026E: USD 6.38 Billion

- Market Size by 2035: USD 15.10 Billion

- CAGR: 9.69% from 2026 to 2035

- Fastest Growing Region: North America

- Largest Region: Asia Pacific

To Get More Information On Soil Testing Equipment Market - Request Free Sample Report

Soil Testing Equipment Market Trends

- Rising adoption of IoT-enabled soil testing systems is improving real-time data monitoring and precision agriculture capabilities.

- Growing demand for portable soil testing equipment is enabling faster on-site analysis and decision-making.

- Increasing government support for precision agriculture is accelerating soil testing equipment adoption globally.

- Expanding automation in laboratories and research facilities is improving testing efficiency and accuracy.

- Rising infrastructure and construction activities are increasing demand for geotechnical soil testing solutions.

The U.S. Soil Testing Equipment Market Outlook

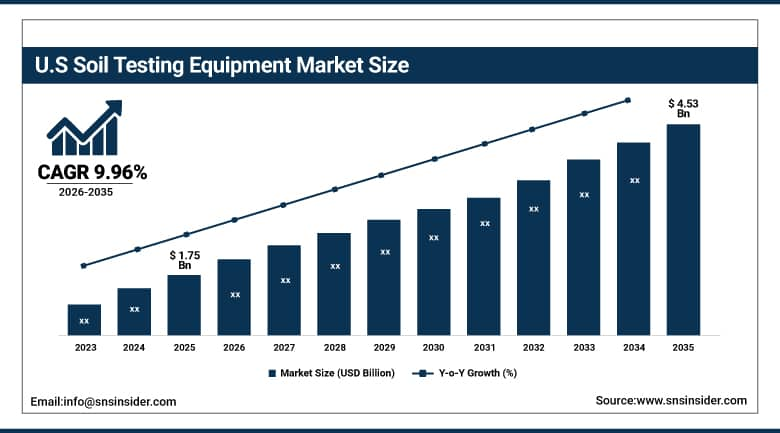

The U.S. Soil Testing Equipment Market was valued at approximately USD 1.75 Billion in 2025 and is expected to reach approximately USD 4.53 Billion by 2035, growing at a CAGR of approximately 9.96%.

Demand in the U.S. market is driven by the convergence of precision agriculture investment across the country’s extensive farm belt, EPA soil contamination remediation monitoring requirements, and the infrastructure construction sector’s geotechnical testing mandate under federal and state building safety standards. The USDA’s Natural Resources Conservation Service promotes routine soil testing as a prerequisite for conservation programme participation, creating regulatory motivation for systematic equipment adoption across American farming operations. University extension services and private agronomic consulting firms collectively represent a large commercial customer segment whose laboratory equipment procurement sustains consistent demand independent of farm commodity price cycle variation.

Thermo Fisher Scientific introduced its next-generation portable X-ray fluorescence soil analyzer in 2024, enabling rapid in-field heavy metal contamination screening for environmental remediation projects and brownfield development assessments. The instrument reduces laboratory turnaround time from days to minutes for screening-level contamination decisions, directly supporting the accelerated remediation timelines that regulatory agencies are requiring for contaminated site clearance approvals.

Soil Testing Equipment Market Segment Analysis

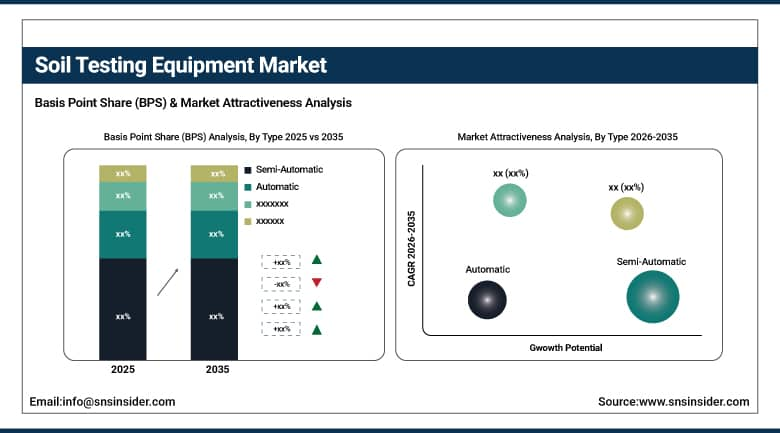

- By Type, semi-automatic equipment dominated the soil testing equipment market with approximately 49% share in 2025. Automatic equipment is the fastest-growing segment with a CAGR of around 8.20% during 2026–2035.

- By Test Type, physical tests held the largest market share of nearly 41% in 2025. Residual tests are projected to be the fastest-growing segment with a CAGR of approximately 8.70% through the forecast period.

- By Application, agriculture dominated the market with an estimated share of about 58% in 2025. Construction is the fastest-growing application segment with a CAGR of nearly 8.50% during 2026–2035.

By Type, semi-automatic dominates, automatic grows fastest

Semi-automatic soil testing equipment retained the dominant type position in the soil testing equipment market in 2025. Its commercial leadership reflects the practical operational preferences of the mid-sized laboratory and field-testing operator segments that represent the majority of global soil testing activity. Semi-automatic equipment reduces manual processing effort and operator-dependent variability relative to fully manual alternatives while remaining accessible at cost points that smaller commercial laboratories, agricultural extension services, and regional construction testing firms can accommodate within standard capital equipment budgets. The format’s compatibility with existing laboratory workflows, familiar operator interfaces, and established calibration procedures sustains its specification preference among buyers who prioritize operational continuity alongside productivity improvement.

Automatic soil testing equipment is the fastest-growing segment because the commercial drivers for automation investment are strengthening across the market’s most commercially significant customer categories simultaneously. Commercial soil testing laboratories serving large agricultural clients face volume pressure that manual and semi-automatic workflows cannot resolve without proportional headcount growth whose cost makes automation investment commercially compelling. Research institutions running multi-parameter soil characterization programmes benefit from the result consistency and dataset integrity that automated systems deliver relative to human-operated alternatives. Regulatory compliance documentation requirements are simultaneously strengthening across environmental monitoring programmes, creating demand for the traceable, audit-ready data records that automated systems generate more reliably than manual workflows.

By Application, agriculture dominates, construction grows fastest

Agriculture retained the dominant application position in the soil testing equipment market in 2025, reflecting the foundational role of soil analysis in crop production decision-making and the regulatory incentive frameworks that government agricultural support programmes use to promote systematic soil testing adoption. Every agronomic intervention from fertilizer application rate to irrigation scheduling to crop variety selection improves in precision and economic efficiency when based on accurate soil composition data. The commercial scale of global agricultural soil testing demand reflects both the frequency of testing cycles across large-scale farming operations and the growing adoption of site-specific soil management practices that require finer spatial resolution testing than historical field-average approaches provided.

Construction is the fastest-growing application in the soil testing equipment market because infrastructure development activity is expanding at above-average rates across the geographies where soil testing regulatory requirements are most stringent and least historically complied with. Asia Pacific’s extraordinary infrastructure investment programme, encompassing road, rail, bridge, and urban development projects whose combined capital value represents the largest construction wave in human history, is generating geotechnical soil testing demand whose aggregate scale is progressively transforming construction into the most commercially significant new growth driver in the soil testing equipment market across the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Soil Testing Equipment Market Insights

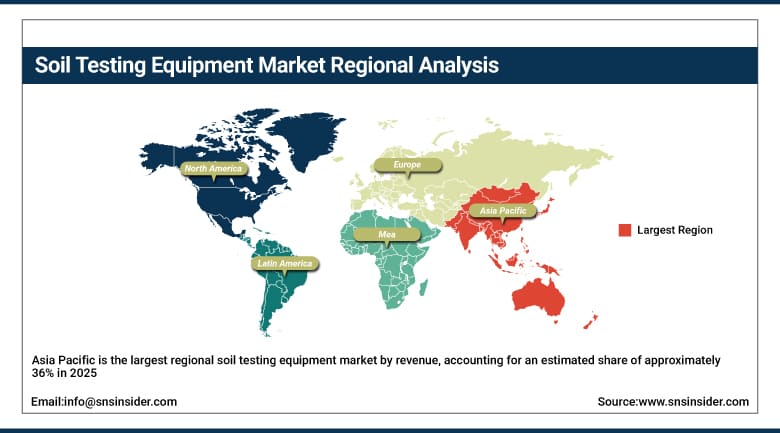

Asia Pacific is the largest regional soil testing equipment market by revenue, accounting for an estimated share of approximately 36% in 2025. This is driven by the region’s combination of the world’s largest agricultural land area, the most intensive infrastructure construction programme, and rapidly tightening environmental soil monitoring regulations across China, India, Japan, South Korea, and Southeast Asia. China accounts for approximately 48.6% of Asia Pacific revenues through its extraordinary combination of large-scale commercial agriculture, the world’s most extensive infrastructure development programme, and government-mandated soil quality monitoring across agricultural and industrial land use categories.

India represents the most commercially significant emerging growth market within Asia Pacific. The Soil Health Card scheme, which has distributed hundreds of millions of soil nutrient analysis reports to Indian farmers, has created mass-market awareness of soil testing’s value that is progressively translating into commercial equipment demand. India’s rapid infrastructure development under the National Infrastructure Pipeline is simultaneously creating growing geotechnical soil testing demand across civil construction and urban development projects.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Soil Testing Equipment Market Insights

North America is the fastest-growing regional soil testing equipment market at approximately 10% CAGR, with the United States accounting for approximately 82.5% of North American revenues. The U.S. market’s growth is driven by the precision agriculture sector’s technology investment, EPA contaminated site remediation monitoring, and the infrastructure sector’s geotechnical testing requirements under federal and state construction safety regulations. USDA conservation programme participation requirements for soil testing are creating consistent institutional demand that sustains market activity independent of commodity price cycles.

Canada contributes approximately 17.5% of North American revenues through its substantial commercial agricultural sector, mining industry soil monitoring requirements, and construction sector geotechnical testing activity across major urban development and infrastructure programmes. Canadian environmental regulations governing soil contamination monitoring at industrial sites create specialized testing equipment demand whose compliance-driven nature sustains procurement through economic cycle variations.

Europe Soil Testing Equipment Market Insights

Europe is a mature and technically sophisticated soil testing equipment market where EU agricultural policy, environmental regulations, and construction safety standards collectively sustain consistent demand across all major application categories. Germany accounts for approximately 22.3% of European revenues through its large commercial agricultural sector, world-class precision farming technology adoption, and a construction industry whose geotechnical testing standards are among the most rigorous in the world. EU nitrate directive compliance requirements for agricultural soil nutrient monitoring create a regulatory procurement floor that sustains demand across European farming operations regardless of crop commodity price dynamics.

The United Kingdom, France, and the Netherlands are significant secondary European markets where precision agriculture adoption, environmental soil monitoring investment, and infrastructure development activity collectively sustain above-average soil testing equipment demand. The EU’s Farm to Fork strategy, which sets ambitious soil health monitoring targets as part of the European Green Deal, is creating new regulatory motivation for systematic soil testing equipment investment across member state agricultural sectors whose adoption has historically been voluntary rather than mandated.

MEA & Latin America Soil Testing Equipment Market Insights

The Middle East and Africa and Latin America are growing soil testing equipment markets where expanding agricultural commercial investment, infrastructure development activity, and government food security programmes are creating demand for soil analysis capabilities. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through Vision 2030’s agricultural self-sufficiency investment, which is funding precision farming programmes in the Kingdom’s arid farming regions where soil nutrient management is critical to productivity. The region’s infrastructure construction programmes are simultaneously generating geotechnical testing demand.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its extraordinary commercial agricultural sector, which operates some of the world’s largest soybean, corn, and sugar cane farms whose precision nutrient management programmes require systematic multi-point soil testing across large land areas. Brazil’s infrastructure construction activity and environmental soil monitoring requirements under IBAMA regulations create additional non-agricultural testing demand that diversifies the Brazilian market’s commercial base.

Market Dynamics

Growth Drivers: Precision agriculture investments, expanding infrastructure development, and growing government soil quality compliance regulations are driving demand for soil testing equipment

The foundational growth driver for the soil testing equipment market is the commercial and regulatory recognition that soil health data is the prerequisite for every productive intervention in agriculture and every safe intervention in infrastructure development. Precision agriculture’s commercial adoption is creating systematic multi-parameter, high-frequency testing demand that replaces the infrequent, basic analysis that traditional farming practices employed. Each precision farming technology investment programme creates proportional soil testing equipment demand whose scale grows with the sophistication of the management system it supports.

Infrastructure development regulatory requirements create a legally mandated procurement floor that sustains construction application soil testing demand through economic cycles. Every major foundation, road, dam, and bridge construction project requires geotechnical soil testing whose results directly determine structural design specifications. As developing market infrastructure programmes accelerate, this mandated demand pool expands proportionally with construction investment volume, creating a commercially reliable and growing market segment.

Restraints: High capital cost of advanced automated equipment limiting adoption among small-scale farmers and institutions

Capital cost remains the primary adoption barrier for advanced soil testing equipment in developing markets and among small-scale farming operations where the return on investment calculation requires high equipment utilization rates that smaller operations cannot guarantee. Entry-level portable testers are commercially accessible, but the laboratory-grade automated systems that deliver the result precision and throughput that commercial precision agriculture programmes require carry procurement costs that exceed the capital budgets of small farm operations and under-resourced agricultural extension agencies.

Technical expertise requirements for equipment calibration, maintenance, and result interpretation create operational adoption barriers in markets where agricultural and laboratory science training infrastructure is limited. Investing in equipment without concurrent investment in operator training and technical support creates underutilization that reduces the commercial return from equipment procurement and discourages subsequent investment in more capable systems.

Opportunities: IoT-integrated smart soil sensors creating continuous monitoring markets

IoT-integrated soil sensor technology represents the most commercially disruptive development opportunity in the soil testing equipment market. Continuous in-field soil monitoring through embedded sensor networks that transmit real-time moisture, temperature, pH, and nutrient data to farm management platforms creates a fundamentally different commercial model from periodic equipment-based testing. This sensor-as-a-service approach expands the soil data market beyond equipment procurement into recurring subscription revenue streams that provide more predictable commercial outcomes for technology suppliers.

Government investment programmes in developing markets represent a commercially significant near-term demand expansion opportunity. India’s soil health programme, Brazil’s precision agriculture support initiative, and agricultural modernization programmes across Southeast Asia are funding equipment procurement, laboratory establishment, and farmer training at a scale that is progressively creating the institutional capacity for systematic soil testing whose market impact extends beyond the direct government procurement to the commercial demand it stimulates among private sector farming operations.

Recent Developments:

- 2025: Martin Lishman launched a new range of portable soil testing kits in May 2025, offering rapid field-based pH, conductivity, and NPK analysis that enables agronomists and commercial farmers to obtain immediate soil health data during field operations, reducing laboratory turnaround time dependency for routine nutrient management decisions across cropping season management programmes.

- 2024: Thermo Fisher Scientific introduced its next-generation portable XRF soil analyser in 2024, enabling rapid in-field heavy metal contamination screening for environmental remediation and brownfield development assessment. The instrument reduces analysis turnaround from laboratory-submission timelines to immediate on-site results for screening-level decision support.

- 2024: ELE International expanded its geotechnical soil testing equipment portfolio in 2024 with enhanced automated compaction and CBR (California Bearing Ratio) testing systems, targeting the growing demand from road construction, airport development, and infrastructure project site investigation programmes across Asia Pacific and Middle Eastern markets.

Soil Testing Equipment Market Key Players are:

- Thermo Fisher Scientific Inc.

- ELE International

- Humboldt Mfg. Co.

- Controls Group S.p.A.

- Martin Lishman Ltd.

- LaMotte Company

- Gilson Company Inc.

- Alfa Testing Equipment S.r.l.

- Matest S.p.A.

- Aimil Limited

- FANN Instrument Company

- UTEST Material Testing Equipment

- Cooper Research Technology

- Durham Geo Slope Indicator (DGSI)

- AgroCares B.V.

- Spectrum Technologies Inc.

- Decagon Devices (Meter Group)

- Stevens Water Monitoring Systems

- Sentek Technologies

- ICT International Pty Ltd.

Soil Testing Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.82 Billion |

| Market Size by 2035 | USD 15.10 Billion |

| CAGR | CAGR of 9.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Semi-Automatic, Automatic, Manual) •By Test Type (Residual Tests, Physical Tests, Chemical Tests, Mechanical Tests) •By Application (Agriculture, Construction, Research & Academia, Environmental Monitoring, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific Inc., ELE International, Humboldt Mfg. Co., Controls Group S.p.A., Martin Lishman Ltd., LaMotte Company, Gilson Company Inc., Alfa Testing Equipment S.r.l., Matest S.p.A., Aimil Limited, FANN Instrument Company, UTEST Material Testing Equipment, Cooper Research Technology, Durham Geo Slope Indicator (DGSI), AgroCares B.V., Spectrum Technologies Inc., Decagon Devices (Meter Group), Stevens Water Monitoring Systems, Sentek Technologies, ICT International Pty Ltd. |

Frequently Asked Questions

Get in Touch